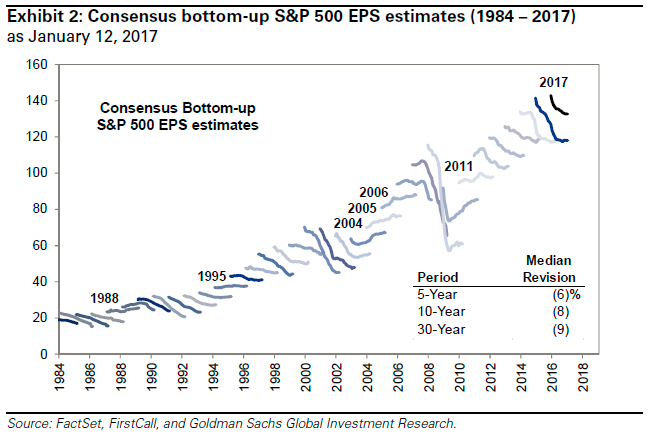

Forward P/E ratios are a bit of a joke. Why? Because Wall Street analysts overestimate prospective earnings 80% of the time. Chart 1 shows only six years since 1984 with conservative forecasts, offering objective proof – as if needed – that Wall Street is not your friend.

Sell-side biases should come as no surprise. So why bring it up? Looking at the white space, we notice a common feature in years with conservative forecasts. The years 1988, 1995, 2004-06, and 2011 were all preceded by bullish “sector-thrust” signals.

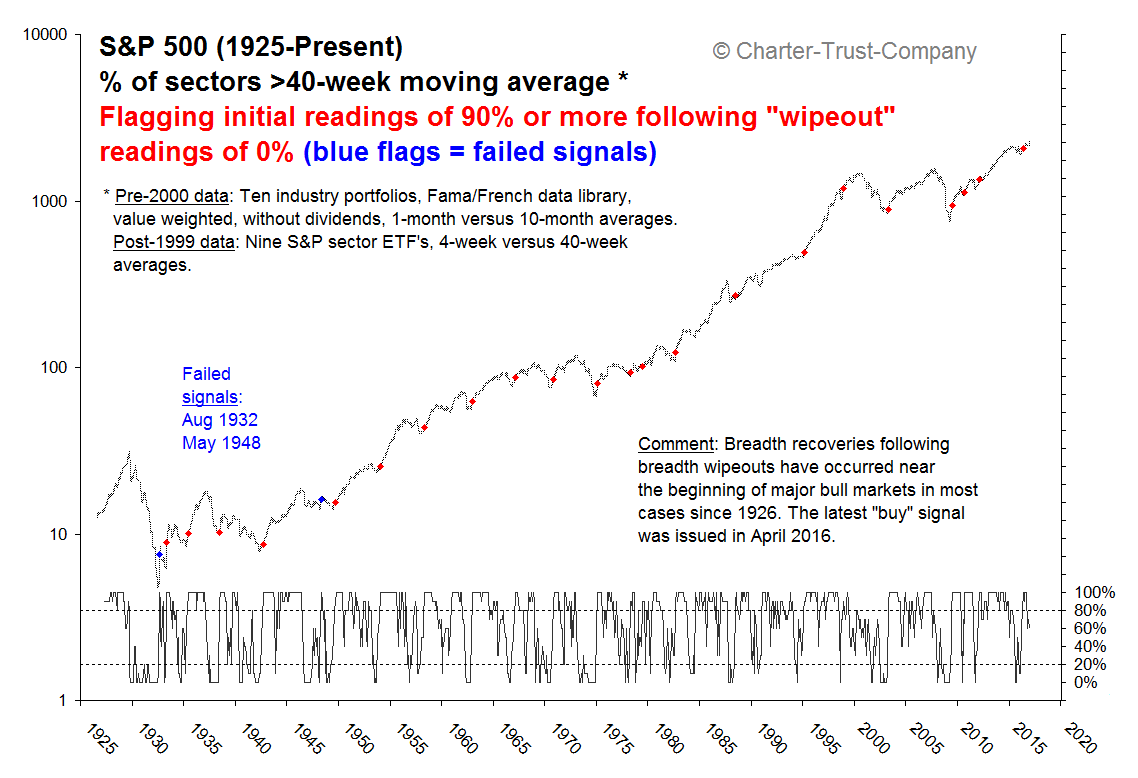

Our sector-thrust model, shown in Chart 2, has a respectable track record over many decades. We outlined this model in April 2016 when a bullish signal was observed. The model posits that cyclical bull markets arise when all sectors recover from a breadth “wipeout” condition. It appears that all sectors must click into forward gear to ensure a self-feeding bull market. Conversely, a troubled sector – such as energy in 2015, or finance in 2008 – can suppress the entire market.

This makes sense from an earnings perspective. Turmoil in the energy sector impacts profitability all around. Why? Because energy companies purchase materials, technology, and industrial goods. If one sector sneezes, others are likely to catch cold. But when all sectors return to health, one should expect a positive ripple effect on earnings.