We would like to take this opportunity to extend our warmest Holiday Wishes to all of our clients and their advisers. 2016 certainly was a year for the history books – from the Brexit surprise to the November surprise; the year certainly was not one that improved the reputation of pollsters! The global investment landscape has changed considerably in the last 30 days, and there is no shortage of pundits opining on what the Trump Administration means for the capital markets. After a hike of 25 bps on December 14th, what will the Fed do in 2017? What happens to infrastructure spending? Trade policy? Health care? Before we move to the important themes that we think will impact capital markets in 2017, we think a look back at 2016 is appropriate.

2016 – Year in Review

If there was one word we could use to describe the equity markets in 2016 it would be RESILIENCY. On three separate occasions the market experienced a material decline only to be followed by a full recovery:

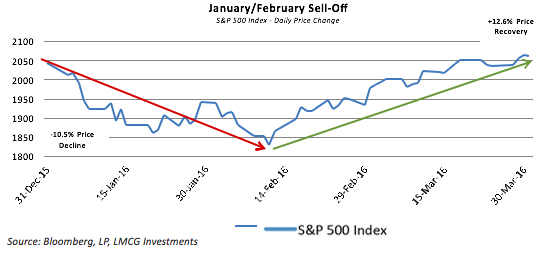

Decline #1 (Jan 1st – Feb 15th)

As oil declined to $26/barrel and credit spreads widened, equity markets plum- meted. As of mid-February, many equity indices had experienced declines of 10% or more, only to be followed by a strong recovery when oil prices seemed to find a floor.

By the end of the first quarter, virtually all of the damage had been reversed – investors were willing to move back into a “risk-on” mode.

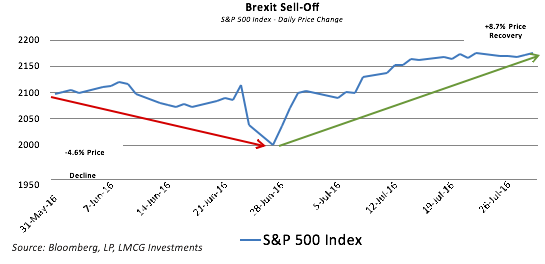

Decline #2: (end of June)

A surprise referendum in the UK to leave the European Union startled world markets. The pollsters (and the bookies!) had gotten it wrong and the uncertainty caused a major level of consternation among investors. Again, global markets sold off as economists and others debated what the referendum’s impact would be on the UK and the Eurozone. But a funny thing happened on the way to the correction – markets were calmed by assurances from pundits and politicians that a smooth transition would avoid major economic dislocation – and maybe we can even get the referendum reversed!

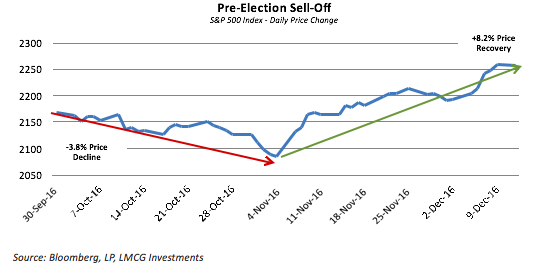

Decline #3: (September 30th – Nov 4th)

October witnessed a pick-up in volatility – which is consistent with the historical pattern in the month preceding a Presidential election. Uncertainty is the biggest contributor to volatility as the polls ebbed and flowed and the outlook for certain sectors changed frequently. The net result was a drawdown of about -4% in the week before the election. The day before the election (Monday November 7th) witnessed a significant bounce as investors began to discount the certainty of a Democratic victory – the status quo being a bit more comfortable than the unknown accompanying a Trump Administration.

As the results came in on Election night, and the media coverage went from the possibility to the likelihood to the certainty that Trump had pulled off the upset victory, equity markets around the world and the US futures market sold off precipitously. Again, fear of the unknown seemed to be the prevailing sentiment. But when the dust settled and US markets opened on Wednesday November 9th, a rally began that has driven many market indices to new highs.

Investor behavior can be hard to figure. 2016 finds us in the 8th year of a bull market expansion in the S&P 500. While there have been some dips along the way, this bull market is the 2nd longest in duration and 3rd in terms of price change (over 200%) in history1. With S&P company earnings only recently turning positive quarter over quarter (i.e., Q3 2016 vs. Q3 2015)2; valuations have become a bit stretched.

Fixed Income

Unlike the equity markets, fixed income securities have been more trend following. The trend was positive for the first nine months of the year – since then largely negative. As interest rates dwindled to all-time lows in the summer, fixed income returns were robust for the first three quarters of the year, with the Barclays US Aggregate Bond Index posting a year-to-date total return of 5.8% through September 30, 20163. With a moderate decline of less than 1% in October, the Index slid -2.3% in November, posting its worst calendar month return since October of 2008. The Federal Reserve increased interest rates this month for only the second time since the Financial Crises. Third quarter US GDP numbers were recently revised higher – to over 3%4. Unemployment remains below 5%. These factors all pointed to a weak environment for fixed income in the fourth quarter.

Where Do We Go from Here? – The Year Ahead

With a resilient equity market and a challenging bond market in 2016 – what does 2017 have in store for investors?

As loyal Unfiltered readers know, we are loathe to make any prognostication in terms of total equity market direction for 2017. We believe there are far too many moving parts that will impact equity prices – so any forecast is somewhat meaningless. However, we do believe there are some important themes that have emerged (and continue to emerge) that will impact capital market returns. At LMCG Investments, we intend to keep them squarely in our sights:

Theme 1: Asset Allocation decisions will be key – and interest rates will be a major determinant of those decisions.

Asset allocation is always an important driver of overall returns. But when we look at the challenges in the global capital markets in 2017, we believe that thoughtful asset allocation – and the ability to tactically adjust allocations – will be a critical component of return.

The liquidity that has been pumped into the system both through the Federal Reserve Bank’s maintaining low interest rates as well as their QE programs have resulted in what can safely be called an ex- tended benign period of interest rates. This environment has been conducive to a positive environment for US equities. We think those days may be over.

We have seen interest rates tick up in the 4th quarter and a material decline in bond prices. This will have a trickle-down impact on a number of sectors and industries. Earlier in 2016 – when yields were lower – we saw how high dividend paying stocks were bid up in price – becoming de facto bond surrogates. But as rates edged higher, many of these stocks lost their luster. Bank stocks got a big boost from an improving interest rate spread picture since this can improve their profitability. Technology stocks – typically viewed as growth stocks – also can be negatively impacted with higher rates as future earnings get discounted with a higher factor, reducing expected future earnings. The strength of the housing market and consumer sentiment are both subject to the vagaries of expected changes in interest rates. Interest rates influence currency as well. We finish 2016 with the US dollar strengthening again relative to major trading partners, and, at increasingly excessive levels, certain US industries may begin to suffer.

Beyond interest rates - will there be tough trade talk next year? If the Affordable Care Act is rolled back, what impact will it have on certain health care industries? Will a more bullish energy policy result in opportunities (and threats) for certain energy companies – and energy importing nations like China? In a strong, core investment program, we think these issues need to be considered – not left to chance.

Theme 2: Increased volatility could be the rule not the exception

Whether you voted for the President-elect or not – there are certain observations one can make about him that (at least we think) are hard to argue with: He speaks his mind; he is unconventional; he is willing to make waves. Many of these qualities were obviously what helped get him elected – but some of these same qualities will result in “headline” risk – whereby certain sectors (e.g., health care, energy) may exhibit fits and starts as policy ideas get floated or headlines break. As we know, capital markets have a tendency to prefer the status quo – so we believe one characteristic of the equity markets in 2017 will be added volatility, or added risk. While additional risk in an asset class is not a good thing – it should present opportunities for active managers to exploit. Sectors and/or stocks will become oversold or overbought, and a nimble investor will have opportunities to take advantage of those dislocations. This leads us to our final theme:

Theme 3: Active management may enjoy a resurgence.

“Truly successful decision-making relies on a balance between deliberate and instinctive thinking.” – Malcolm Gladwell (Blink: The Power of Thinking Without Thinking, 2005)

2016 witnessed a continuation of the debate between active and passive management, and passive vehicles saw net gains. Of course this debate has been going on since the development of passive vehicles in the 1970’s. From time to time, the argument resurfaces – especially when, as in 2016, active equity managers have a difficult time outperforming passive alternatives. But these comparisons tend to be one-sided – they are typically focused on returns – rarely do they discuss risk. For example, in 2015 the contribution to returns within the S&P 500 was heavily concentrated in just four names – the FANG stocks: Facebook, Amazon, Netflix and Alpha- bet (Google). If you owned an equally-weighted (at January 1, 2015) portfolio of just these four names, your total return in 2015 would have outpaced the total return of the S&P 500 by 81.8% (83.2% from the four FANG names vs. 1.4% for the S&P 500)2!. However, if you decided to buy this equally-weighted four stock portfolio at the beginning of 2016 instead, the YTD performance of your port- folio would have lagged the performance of the S&P 500 by -3.6% through December 12th (FANG +9.1% vs. +12.7% S&P 500). With an index fund the investor gets a diversified portfolio for low fees – but does it make sense to hold these types of stocks without regard for valuation or risk?

And perhaps more importantly – if the general level of volatility moves up in 2017 as described above – a passive investment will ride the “volatility wave” – holding on to positions that have been overbought and not being able to add to positions that are oversold. We think being nimble will be important. The recent post-election rally provides one such example – financials, notably banks, advanced significantly on the expectations of higher interest rates. The Global MultiCap team decided that was an opportunity to capture some of these gains, and lightened up on the banks.

In summary, we are constructive about global equity markets in 2017 – but we think the advantage will be with active managers who can adjust exposures in their portfolios in real time.

Sources:

1 Investopedia

2 FactSet Research Systems, Inc.

3 Bloomberg, LP

4 U.S. Department of Commerce

© LMCG Investments

Read more commentaries by LMCG Investments