France reported this week that its summer hosting of Euro 2016, Europe’s soccer championships, added $1.26 billion to its economy.

This is good news, for sure, and worth celebrating.

But here’s the thing: Why doesn’t France put as much effort into supporting its businesses and markets as it does its soccer franchises?

After all, the country has an entrepreneurship problem—as in, business growth and its labor market are struggling.

A lot of the blame lies at the feet of its labyrinthine web of regulations, which the Organization for Economic Cooperation and Development (OECD) once called “unnecessarily complex.” Barriers to entry in several key industries, including architecture, accounting and legal services, are prohibitively high, which has decimated the country’s labor market in the last few years. More than 25 percent of all working-age French under the age of 25 are unemployed right now, a meaningfully higher rate than for youth in the European Union (18 percent unemployment), United States (10 percent) and Japan (4 percent). Household savings rates are skyrocketing, consumer confidence is on life support and investments growth has been sluggish.

As a result of all this, economic growth in France is among the worst for major EU economies. There it will remain, sadly, unless officials commit to strengthening competition by streamlining its tax system and reforming regulations. But at least it has some great soccer clubs.

Surging Demand for California Munis

By comparison, look at California, whose economy just surpassed France’s in size. Say what you will about the state and some of its colorful residents, it’s successful because it recognizes talent and fosters an environment in which innovation and entrepreneurism can thrive. Silicon Valley is seeing a boom right now, which has helped the state government generate budget surpluses. Debt is being paid down, and the state’s rainy-day savings account is growing. This has contributed to California enjoying its highest credit rating since the turn of the century, Bloomberg reports, and caused demand for its municipal debt to climb.

At the same time, California munis can be volatile because state revenue depends on wealthy taxpayers whose incomes are tied closely to the stock market. According to Bloomberg, the top 1 percent of earners paid half of the state’s income tax revenue in 2014.

It shouldn’t come as a surprise to anyone, then, that California has one of the highest Gini coefficients, a measure of economic inequality, in the nation. Although some might balk at this, I think it’s proof there are huge, life-changing opportunities in California, and in the U.S. in general, that can turn “regular folk” into billionaires almost overnight.

Speaking of which, check out our latest slideshow, “10 Living, Self-Made Billionaires.”

Small Business Optimism in the U.S. Is Soaring Right Now

As further proof that France should do more to open up its economy, look at what President-elect Donald Trump’s pledge to lower taxes and slash regulations is doing to business optimism here in the U.S. Last month, the Index of Small Business Optimism soared a phenomenal 7.4 points to 105.8, its highest reading since 2004. The National Federation of Independent Business (NFIB), which conducts the survey, reported that attitudes toward capital spending and job creation in particular surprised to the upside. Research firm Evercore ISI called it a “blowout report,” and I have to agree.

In their commentary, the NFIB’s William Dunkelberg and Holly Wade expressed cautious optimism that the incoming administration could satisfactorily relax some of the regulatory burden on businesses.

“Politicians say they want to create jobs, but their regulations and laws… only increased the cost of hiring a worker, and that is not good for job creation,” they wrote.

(Consider compliance-related paperwork alone. In fiscal year 2015, Americans spent a jaw-dropping 9.78 billion—yes, billion—hours complying with federal rules and regulations, according to a recent report from the Office of Management and Budget (OMB). That’s up nearly 4 percent from 2014.)

Many chief executives of large multinationals have been very receptive to Trump’s proposals, taking him at his word that he can succeed at fostering an improved business environment in the U.S. Ford recently scrapped plans for a Mexico factory, while Fiat Chrysler announced a $1 billion investment in Michigan and Ohio, expected to create up to 2,000 new jobs. After meeting with the president-elect this week, Jack Ma, founder and CEO of Chinese ecommerce site Alibaba, said he was committed to adding 1 million U.S. companies to his hugely popular online shopping platform. The chief executive of active wear company Under Armour told CNBC that it would be bringing jobs back to the U.S., specifically Baltimore, where it’s headquartered. And on Thursday, Amazon unveiled plans to grow the number of its full-time, U.S.-based jobs by 100,000—from 180,000 today to over 280,000 by 2018.

As I’ve said many times before, there’s a lot of uncertainty surrounding Trump, who will be sworn into office one week from today. At the same time, businesses and investors clearly like what they’re hearing. Appearing on CNBC this week, legendary economist Robert Shiller perfectly summarized this distinction, saying that “nervousness can go along with optimism.” Although he didn’t vote for Trump, Shiller acknowledges that animal spirits are running high, adding that he sees the Trump equities rally spilling over into the housing market this year.

|

Joining Shiller in offering a balanced assessment of Trump is my old friend Alexander Green, whose writing skills I admire and opinions I greatly respect. In his most recent blog post, Alexander makes a convincing case against Trump’s protectionism, which are “not good for the economy or the market” and “undermines American economic growth.” Although investors have moved billions into the stock market since the election, the Trump rally could easily turn into the Trump correction, Alexander says, “unless he changes his tune” on international trade.

“Why does a flat-panel HDTV that cost more than $10,000 in 2003 cost less than $400 today? Globalization,” he writes. “How can you walk into a Marshalls store and buy a fine cashmere sweater for 35 bucks? Globalization. Why does an $8 million supercomputer from 20 years ago sit in your pocket and cost less than $200? Globalization.”

U.S. Economy Could Get a Boost in the Near Term

The World Bank contributed to the wave of good news this week, making encouraging projections for the U.S. economy in light of Trump’s business-friendly policies. In its flagship report on global economics, the financial institution explained that expansionary fiscal policies—including tax cuts and plans to upgrade America’s infrastructure—could boost U.S. economic growth as high as 2.5 percent this year and 2.9 percent in 2018.

This would be a welcome surprise, as growth slowed considerably in 2016 to 1.6 percent, down from 2.6 percent in 2015, according to the World Bank.

China Likely to Remain Top Engine of Global Growth

The good news isn’t limited to the U.S. Across the Pacific Ocean, China saw its producer price index (PPI) in December rise 5.5 percent, its fastest pace in more than five years and fourth consecutive positive reading after 54 straight negative ones.

The country’s PPI, which measures prices received by producers at the first commercial sale, is strengthening on higher commodity prices. What’s more, there’s an 85 percent correlation between China’s PPI and its nominal GDP, according to Evercore ISI, so growth in the world’s second-largest economy should pick up some steam this year.

“Based on history, the PPI’s increase of +3.3. percent year-over-year (y/y) in the fourth quarter suggests +15 percent y/y nominal GDP growth,” the firm wrote. It estimates fourth-quarter growth to be more than 8.8 percent and more than 9.6 percent in the first quarter of this year.

Meanwhile, the country’s purchasing manager’s index (PMI) has remained at or above 50—indicating manufacturing expansion—for the past six months, which is bullish for commodity prices.

Chinese demand for commodities, which were up 25 percent in 2016, is indeed skyrocketing, with imports of oil, iron ore, copper and soybeans reaching all-time highs last year. This helped solidify the country’s role as the world’s top engine of economic growth once again, contributing an estimated 33.2 percent to global economic expansion, according to China’s National Bureau of Statistics.

It’s expected we’ll see a repeat of outsize commodity demand this year, which should support prices.

Looking at copper, further support should come in the form of market deficits, which are expected to widen until at least 2020. As investment bank Jefferies explained in a note last week, “unexpected disruptions”—including undercapitalization of mines and the risk of labor strikes at Chile’s Escondida, the world’s largest copper mine—will likely add to supply constraints.

“From a supply perspective, the outlook for mined commodities is very bullish,” Jefferies added.

That includes gold. As a friend recently reminded me, China’s official gold holdings account for only 2 percent of its foreign reserves. Two percent! That’s remarkably low, far lower than most large economies. (In the U.S., it’s around 75 percent, according to the World Gold Council.) China is obviously interested in supporting its currency, and since it sold off quite a lot of U.S. Treasuries in the past year—Japan is now the top holder of U.S. government debt—it will likely need to substantially build up its gold reserves.

The People’s Bank of China (PBoC) has been accumulating gold, even if the rate has slowed recently, but imagine if it decided to boost holdings up from 2 percent of foreign reserves to 10 percent, which is more in line with other countries. That would have a monumental impact on the price of the yellow metal.

At this point, there’s no evidence the PBoC plans to follow such a route, but the possibility is there, with huge implications for gold.

January 12, 2017Gold Looks Undervalued Says Frank Holmes |

January 12, 2017U.S. Global Investors’ Gold-Oriented Funds Earn 5-Star Ratings from Morningstar |

January 11, 2017How Will Gold Miners Fare In 2017? |

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.39 percent. The S&P 500 Stock Index fell 0.10 percent, while the Nasdaq Composite climbed 0.96 percent. The Russell 2000 small capitalization index gained 0.35 percent this week.

- The Hang Seng Composite gained 1.79 percent this week; while Taiwan was up 0.07 percent and the KOSPI rose 1.35 percent.

- The 10-year Treasury bond yield rose 2 basis points to 2.39 percent.

Domestic Equity Market

Strengths

- Consumer discretionary was the best performing sector of the week, increasing by 0.83 percent versus an overall decrease of -0.11 percent for the S&P 500.

- Illumina was the best performing stock for the week, increasing 14.90 percent.

- Airbus has taken the sales crown from Boeing. The company booked 321 net orders in December, running its 2016 total to 731, beating the 668 orders won by Boeing.

Weaknesses

- Real estate was the worst performing sector for the week, falling -2.25 percent versus an overall decrease of -0.11 percent for the S&P 500.

- Endo International was the worst performing stock for the week, falling -20.25 percent.

- Chipotle lowered its expectations for the upcoming quarter. The Mexican fast casual chain said its fourth-quarter earnings will be between $0.50 per share and $0.59 per share, much lower than analysts' expectations of $0.96 per share. Additionally the company said same store sales will fall 4.8 percent, worse than expectated.

Opportunities

- Amazon is adding 100,000 jobs in the U.S. The "full-time, full benefit" jobs will be added over the next 18 months according to the company. Many of the jobs will be in new fulfillment centers and will range from engineering to software-development roles, according to a press release. The company continues to grow by leaps and bounds.

- Mars is buying a pet health company for $9.1 billion. The candy and pet food maker acquired VCA Inc., paying a 30 percent premium over its Friday closing price.

- Takeda is buying Ariad Pharmaceuticals in a $5.2 billion deal. Takeda bought the company to help grow its drug portfolio.

Threats

- With the Dow struggling to break 20,000 and Inauguration Day approaching, there are murmurs about the stock market's near-term performance. The S&P 600 — comprised of small-cap stocks — is flashing one such warning sign about the market's next move, according to Andrew Adams, a market strategist at Raymond James. Small-cap stocks were the biggest winners of the post-election rally. The Russell 2000, a separate index that tracks companies with a market capitalization of $1 billion or less, outpaced gains on the benchmark large-cap S&P 500, even as both rose to records. However, small caps have failed to build on their market-leading gains since the election, creating a reason for caution, Adams said. "The S&P 600 Small Cap Index has basically gone sideways for over a month now, and even appeared to break down below support on Monday before rallying back over the line yesterday," he wrote in a note on Wednesday.

- The Environmental Protection Agency is going after Fiat Chrysler. The EPA is alleging that the carmaker manipulated its software in some diesel cars to get around emissions standards, similar to the Volkswagen scandal. Shares of the company fell 9.5 percent for the day on the news.

- President-elect Donald Trump has officially killed the drug industry's buzz. At a press conference Wednesday, Trump said that drug companies were "getting away with murder," and suggested that the U.S. government needed to negotiate drug pricing. The comments came while drug executives and investors gathered in San Francisco, at one of the largest industry conferences of the year. The chill this cast among executives at the JPMorgan Healthcare conference was palpable. Those, both with drugs on the market and that have drugs in development, said the concern is that Trump will scare investors away from the industry. If investors start to shy away from investing in risky new medicine, that could keep treatments from making it all the way through the drug development process, they said.

The Economy and Bond Market

Strengths

- The World Bank says global growth will pick up slightly in 2017. It lowered its 2017 global growth forecast to 2.7 percent from its June outlook of 2.8 percent, but that would still be ahead of the 2.3 percent growth that we saw in 2016.

- U.S. small business optimism surged in December. The National Federation of Independent Business (NFIB) survey of small business optimism rose 7.4 points to 105.8 in December. The gain was the largest one-month jump since 1980 and the highest level since 2004.

- If not for Puerto Rico, 2016 would have been a remarkably safe year for investors in the $3.8 trillion municipal bond market, at least when it comes to securities that are rated by Moody’s Investors Service. Just four issuers graded by the company defaulted on their obligations for the first time, all of them arms of the Caribbean territory. Without that, it would have been the second year since 2014 without a default, a rarity even for a sector known as a haven.

Weaknesses

- S&P Global Ratings lowered Dallas’s general obligation bond rating to AA- from AA, with a negative outlook. The downgrade reflects its view that expected continued deterioration in the funded status of the city’s police and fire pension system, coupled with growing carrying costs for debt, pension and other postemployment benefit obligations, is significant and negatively affects Dallas’s creditworthiness.

- Initial jobless claims came in at 255,000, above the forecasted 247,000 and the prior week’s 235,000.

- Retail sales, excluding auto and gas, for December came in flat, missing expectations for growth of 0.4 percent.

Opportunities

- According to Jim Grabovac, managing director at McDonnell Investment Management, “the risk of rates falling is something that’s not being factored into the present outlook. There’s always potential for a global policy mishap, particularly given the lack of government experience of the incoming administration.” Falling rates would be positive for bonds.

- According to BCA, a combination of accelerating economic growth and still-accommodative monetary policy will cause the U.S. Treasury curve to bear-steepen in the first half of 2017. In a curve-steepening environment, bullet trades should outperform barbells.

- American contractors are getting their shovels ready for the incoming Donald Trump administration, and they plan to boost payrolls to take on new projects. Three out of four U.S. construction firms expect to increase head count this year, according to a survey released Tuesday by the Associated General Contractors of America and Sage Construction and Real Estate. The bullish outlook is apparently based on high hopes that Trump will make good on campaign promises to invest hundreds of billions of dollars in federal spending on new infrastructure projects.

Threats

- Jeff Gundlach, CEO of DoubleLine Capital, held his latest "Just Markets" webcast on Tuesday night highlighting his recent thoughts about the U.S. economy and global markets. Gundlach said it’s possible the recent rise in bond yields could continue, with the U.S. Treasury 10-year yield possibly hitting 3 percent.

- According to Jan Hatzius, the chief economist at Goldman Sachs, there are three key risks to the economy in 2017, including trade protectionism, European politics and China.

- Next Wednesday, the Federal Reserve's Beige Book of economic anecdotes and the December consumer price index (CPI) report warrant close attention. Core CPI has surprised on the downside in recent months, with the three-month annualized rate slowing to 1.7 percent. Other noteworthy U.S. data will be industrial production (Wednesday), the National Association of Home Builders (NAHB) survey (Wednesday) and housing starts (Thursday). The latter two releases will tell if higher bond yields are leading to a slowdown in the housing market.

Gold Market

This week spot gold closed at $1,197.37, up $24.52 per ounce, or 2.09 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 1.42 percent. Junior tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index climbed just 0.39 percent. The U.S. Trade-Weighted Dollar Index finished the week down by 1.00 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

Jan-12 |

U.S. Initial Jobless Claims |

255k |

247k |

237k |

|

Jan-13 |

U.S. PPI Final Demand YoY |

1.5% |

1.6% |

1.3% |

|

Jan-17 |

Germany ZEW Survey Expectations |

19.0 |

-- |

13.8 |

|

Jan-17 |

Germany ZEW Survey Current Situation |

65.0 |

-- |

63.5 |

|

Jan-18 |

Germany CPI YoY |

1.7% |

-- |

1.7% |

|

Jan-18 |

Eurozone Core CPI YoY |

0.9% |

-- |

0.9% |

|

Jan-18 |

U.S. CPI YoY |

2.1% |

-- |

1.7% |

|

Jan-19 |

ECB Main Refinancing Rate |

0.000% |

-- |

0.000% |

|

Jan-19 |

U.S. Housing Starts |

1189k |

-- |

1190k |

|

Jan-19 |

U.S. Initial Jobless Claims |

252k |

-- |

247k |

|

Jan-19 |

China Retail Sales YoY |

10.7% |

-- |

10.8% |

Strengths

- The best performing metal for the week was gold, up 2.09 percent and closely followed by silver.

- Gold surged above $1,200 an ounce this week on the back of President-elect Trump’s press conference which provided little detail regarding any economic stimulus plans, reports Bloomberg. “Expectations are so high that we think there are greater chances that traders may feel that they did not get what they bargained for,” Naeem Aslam, chief market analyst at Think Markets said. “Under such a scenario, we could see gold continue its rally.”

- In preparation for Chinese Lunar New Year, Asian buyers have stepped up their purchases of gold, sending the yellow metal to a five-week high. In the past 10 years, January has been gold’s strongest calendar month. Other positive news in the gold space comes from Toachi Mining this week. The company reported results from its ongoing drilling at the La Plata gold-rich volcanogenic massive sulfide (VMS) project in Ecuador. One of the highlights of the release was the intersect of 15.89 meters grading at 7.63 grams per tonne gold, 49.74 grams per tonne silver, 11.82 percent zinc and 0.97 percent lead.

Weaknesses

- The worst performing metal for the week was palladium, down 0.71 percent, the only precious metal to lose ground this week after a strong start for the year with a gain of 10.38 percent. Hedge fund managers bet wrong for a second week, reports Bloomberg, becoming so bearish on gold lately that many missed the biggest rally since early November. Investors cut bets on higher prices for an eighth straight week just as gold extended its rebound, the article continues.

- Detour Gold fell as much as 8.1 percent earlier in the week, underperforming all of its gold mining peers while the gold price advanced, reports Bloomberg. The company’s Detour Lake mine is at least 33 million tonnes behind in total tonnage mined, according to a note from CIBC on January 8. CIBC noted that additional financing may be needed if further capex is required for stripping. Detour was downgraded to “buy” from “top pick” at Cormark Securities.

- UBS says that Freeport-McMoRan investors should use caution when it comes to a new Indonesian mining law that needs additional clarity, writes Bloomberg. UBS analyst Andreas Bokkenheuser believes the law could be a “large negative” if it requires the company to convert its Contract of Work (COW) into a mining license. An analyst at Scotiabank agrees, explaining this is negative for Freeport as the new law requires miners to divest stake down to 49 percent and to give up its COW agreement. Bloomberg writes that the company can no longer export semi-processed metal after regulations allowing shipments lapsed on Wednesday, although the mine is continuing to operate.

Opportunities

- In a note this week, UBS says it is optimistic on the prospect of fiscal policy boosting U.S. growth looks to be priced in, as much more evidence may now be needed before yields and the dollar can move higher. Former U.S. Treasury Secretary Lawrence Summers said last week that investors are far too sanguine about the risks of Trump’s policies, reports Bloomberg, which analysts at Eurasia Group said could contribute to a level of global instability not seen since WWII. A median estimate of analysts and traders in a Bloomberg survey think gold could rally to $1,300 by year-end. Merk also out with an interesting note on how gold reacts during presidential transition years this week. “Since Nixon took the U.S. dollar off the gold standard in 1971, there have been seven Presidential transition years,” the group writes. On average, the S&P 500 was negative for those seven calendar years of transition while the average gains for gold was 14.8 percent. One theory behind this? Policy disappointment of a new incoming administration.

- Christopher Mahon of Baring Asset Management is seeking shelter in gold this year, reports Bloomberg. Mahon has one major conviction about 2017, which is that central-bank bashing by politicians will become the new normal. In the past few months Mahon has built up a 4 percent allocation to bullion in his 1.7 billion pound fund. The precious metals team at HSBC has also made its forecast for gold in the New Year, maintaining a bullish stance on the metal. The team forecasts a gold price of $1,282 an ounce in 2017 and $1,310 in 2018.

- Scotiabank hosted a teach-in by Klondex Mines President and CEO Paul Huet recently, and in its latest report, Scotiabank shares four key takeaways from the meeting: 1) Work is advancing on the Hollister project with more updates coming, 2) True North continues delivering positive surprises as operations ramp up, 3) stronger quarter-over-quarter production from Fire Creek and Midas is expected in the fourth quarter of 2016, and 4) the recently-acquired Aurora project offers longer-term upside potential. Bloomberg reports the latest from Goldcorp this week as well – the company will buy 9.5m shares of Auryn Resources, at a 20-percent premium to the prior closing price.

Threats

- Decades of divergence between stocks and bonds could be ending, says Sanford C. Bernstein & Co., which would mean a shift in investor assumptions, reports Bloomberg. A new era with rising inflation could see equities and bonds return to the historic positive correlation they’ve displayed since 1763, according to analysts led by Inigo Fraser Jenkins. “If the path of inflation is set to be generally upward from here then we should expect this correlation to rise,” they stated. This will make it harder for investors to diversify, and also suggests that a 10 percent allocation to gold and gold stocks might be a prudent addition to a portfolio in these circumstances to broaden an investors diversification mix.

- ICBC believes that the real rates reversal has been good for gold, but doesn’t think that it will last. The group says it seems too soon for markets to give up on the Trumponomics reflation trade, maintaining its view that the current rally is about to lose steam. ICBC adds that a more sustainable turn will have to wait until mid-year, and that gold could get a much stronger bid if the policy ping-pong between fiscal hawks and doves becomes stuck.

- Citigroup shared its outlook for gold in its January 13 report, saying that in the medium-term higher real rates and a stronger dollar could send prices lower. Citi says the gold price is more likely to drop to $1,100 an ounce than stay above $1,200 in the second quarter. In addition, two top gold forecasters from BNP Paribas SA and Rising Glory Finance both see gold prices returning to three figures this year, a price level last seen in 2009. Both cite the outlook for higher U.S. interest rates weighing on non-yield bearing bullion, reports Bloomberg.

Energy and Natural Resources Market

Strengths

- U.S. dollar weakness spurs bids for commodities. The U.S. dollar is beginning to show signs of weakness as it is breaking below the 50-day moving average, a key measure of price momentum used by investors globally. The currency has been a major underperformer year-to-date which has helped commodities start 2017 off with a bang.

- The best performing sector for the week was the S&P/TSX Composite Diversified Metals & Mining Sub Industry index. The index rose 13.7 percent on the back of rallying copper and base metal prices this week which gave a boost to company earnings.

- Vale SA, the Brazilian major iron ore producer, was the best performing stock this week finishing up 20 percent. The stock rose on the back of an incredible 5.6 percent rally in iron ore prices this week.

Weaknesses

- Crude oil was the worst performing commodity this week falling 2.6 percent. The drop in the price of oil was driven by skepticism across the globe as investors question the ability of OPEC members to coordinate production cuts.

- The worst performing sector this week was the S&P/TSX Composite Oil and Gas Exploration and Production Sub Industry Index. The index fell 3.4 percent as crude oil prices dropped 2.8 percent on as a result of larger than expected inventory builds.

- The worst performing stock for the week was Devon Energy Corp, an independent natural gas and petroleum producer in North America. The company fell 4.4 percent on the back of a downgrade from analysts at Wells Fargo & Company who argue the company’s growth may lag peers in 2017.

Opportunities

- Gold prices rose to a seven-week high as hedge funds boost bullish bets for the first time in nine weeks. As we approach Chinese New Year and President-elect Donald Trump’s inauguration, demand for the shiny metal is rising. These catalysts should provide support to the metal’s new level over the short-term and potentially help the metal rally further as we enter into unchartered political territory.

- Copper prices rallied to a two-month high this week as China revealed record imports of the metal. In addition to the falling U.S. dollar which is adding fuel to the metal’s rally, commodity imports in China jumped again in the month of December which is supporting renewed strength for copper demand and the entire base metals complex.

- Despite a warm winter thus far with patches of cold fronts, the fundamentals for natural gas remain strong and intact. A larger-than-expected withdrawal from storage was reported by the EIA of 151 billion cubic feet (bcf) versus consensus estimates of 143 bcf which gave way to rallying natural gas prices this week. A positive read-through for natural gas.

Threats

- China posted its worst export number since 2009 as the prospect of a U.S. trade war looms. The world’s largest trading nation posted weak data for 2016 as exports fell by 7.7 percent, the second annual decline in a row. Despite no concrete action being taken yet by the Trump administration, it is clear that negative foreign trade relations and the anti-globalization movement will be key threats to commodities in 2017.

- U.S. crude oil inventories rose far more than forecasted last week. Inventories increased by 4.1 million barrels last week according to the U.S. Department of Energy when analysts estimated 930,000 barrels. In addition, inventories of gasoline, which oil is refined into, rose by 5 million barrels where inventories were estimated at 2.1 million barrels. A negative read-through for medium-term crude oil fundamentals.

- Indonesia will allow certain exports of low-grade nickel ore in 2017. After much debate, the government of Indonesia allowed the restrictions to lapse, which may result in an immediate boost of raw nickel exports potentially closing the estimated 80,000 ton deficit in the months to come. The tight fundamental dynamics surrounding nickel supply will now reverse, ultimately a negative read for nickel prices this year.

China Region

Strengths

- Singapore’s Straits Times Index closed up 2.11 percent for the week, finishing the last five trading days as the region’s best performer. Korea also had a solid week, with the KOSPI up 1.35 percent and the December unemployment rate in Korea coming in better than expected at a low 3.4 percent.

- December foreign direct investment in China popped back up to 5.7 percent.

- The best-performing sector in the Hang Seng Composite Index this week was materials, up 3.74 percent. The HSCI itself rose 1.79 percent for the week, and even its weakest sector for the week (telecommunications) still rose more than 1 percent in that timeframe.

Weaknesses

- Year-over-year exports in China for the December period missed expectations, coming in down 6.1 percent versus expectations for a drop of only 4.0 percent.

- The Shanghai Composite finished out the week as one of the region’s worst-performing indices, dropping 1.32 percent in the last five trading days.

- Year-over-year retail sales in Singapore came in slightly weaker than expected, up only 1.1 percent, worse than an anticipated gain of 1.7 percent.

Opportunities

- The Lunar New Year holidays begin later this month, which likely means relatively more consumer spending and traveling throughout the region. Air Asia (AIRA MK), for example, received a bump this week following an upgrade and attention to a statement from Malaysian authorities noting a strong uptick in Chinese tourist arrivals last year after new visa procedures were introduced.

- China’s iron ore imports surged in 2016 to a record, above 1 billion metric tons, reports Bloomberg, citing unexpectedly strong steel production and lower local mine output. Last year iron ore surged over 80 percent as the Asian nation added stimulus to sustain economic growth. Justin Smirk, senior economist at Westpac Banking, said in an email this week that imports should “continue to rise through 2017.”

- In 2016 China approved 227 projects worth $246.55 billion, the state planner announced this week. According to Reuters, China’s National Development and Reform Commission (NDRC) approved 23 fixed-asset projects in December. China will invest $173.57 billion between 2016 and 2018 in a three-year plan to develop information infrastructure, the article continues.

Threats

- Rhetoric remains elevated and many details remain unclear with respect to U.S. trade policies under the incoming Trump administration. China’s trade troubles could be set to stay, warned the Ministry of Commerce on Thursday following Donald Trump’s comments regarding the prospect of a “border tax” under his administration, reports the South China Morning Post. “In 2017, the trade situation remains complicated and severe,” Sun Jiwen with the Ministry of Commerce said. “External demand is weak, trade protectionism is exacerbating, the unstable and uncertain factors are increasing, and downward pressure on trade is piling up.”

- U.S. President-elect Trump’s nominee for Secretary of State, Rex Tillerson, stated that Beijing must be denied access to reclaimed reefs in the disputed South China Sea. While China’s foreign ministry issued a relatively measured response to the remarks, reports Bloomberg, the threat from Tillerson raises the prospect of a more antagonistic U.S. approach to Beijing’s military buildup in the area.

- Yuan weakness and capital outflows from China remain an ongoing threat. Foreign exchange reserves came in lower once again over the weekend, and while 3 trillion USD is hardly a paltry amount, taken in conjunction with a generally weaker yuan, the drop continues to merit investor attention.

Emerging Europe

Strengths

- Turkey was the best performing country this week, gaining 5.7 percent. The Istanbul Exchange rebounded sharply on Thursday after measures were announced to support the falling Turkish lira. Eregli Demir ve Celik Fabrikalari, a steel producer, was the best performing equity, gaining 16.7 percent in the past five days.

- The Hungarian forint was the best performing currency this week, gaining 1.3 percent against the U.S. dollar. Hungary will probably suspend unconventional monetary easing after inflation in December rose 1.8 percent from a year earlier (the most since July of 2013).

- The materials sector was the best performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst performing country this week, losing 1.3 percent. The Greek unemployment rate dropped slightly to 23 percent in October. It has come down from record highs but remains more than double the euro zone’s average of 9.8 percent in November.

- The Turkish lira was the worst performing currency this week, losing 2.2 percent against the U.S. dollar. Turkey’s central bank took limited measures to support its falling currency. First it cut foreign exchange reserve requirements by 50 basis points. Then it tightened liquidity, not offering any bank funding at 8 percent via the one-week repo auction. Local banks had to borrow at 10 percent via the overnight lending rate. Lastly, it cut the interbank borrowing limit to TRY 11 billion. The lira is also the worst performing currency year-to-date, declining against the U.S. dollar by 5.4 percent.

- The consumer staples sector was the worst performing sector among eastern European markets this week.

Opportunities

- According to the World Bank, global economic growth will accelerate to 2.7 percent in 2017 from 2.3 percent in 2016. Growth will not only accelerate in the United States, but also in resource-exporting countries, foremost Russia and Brazil. The World Bank is more optimistic about Russia’s outlook than the Russian economy minister himself, projecting growth of 1 to 1.5 percent.

- Eurozone industrial production rose to 1.5 percent in November, up from -0.1 percent in October, raising hopes that GDP in the final quarter of 2016 will come in above the 0.3 percent figure recorded in the third quarter.

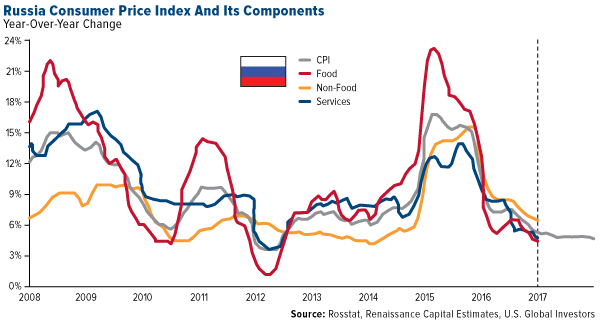

- Inflation in Russia decreased to 5.4 percent by the end of 2016 from 5.8 percent in November and 12.9 percent in 2015. The RenCap Securities research team believes that inflation will continue to decline further below 5 percent this year and that the central bank of Russia will lower its policy rate toward 8 percent by the end of this year (with the first 50 basis points rate cut on March 24).

Threats

- Moody’s stated that Turkish bank profits will be hit significantly this year by increasing non-performing loans. The group also warned of a “general worsening” in the country’s investment climate. Moody’s further commented that gross non- performing loans are expected be above 4 percent by the end of the year, a level which is said would require increased provisioning expenses, and could reduce the bank’s profitability.

- U.S. intelligence officials informed President-elect Donald Trump about unsubstantiated reports received in which the Russian government compiled potentially damaging personal and financial information on him. Trump and Russia both deny the legitimacy of this report.

- Poland’s opposition suspended a nearly month-old blockade of the parliament on Thursday. Investors largely ignored the longest disruption to legislative work since Poland’s democratic revolution in 1989, with the zloty, government bonds and Warsaw stocks all advancing since mid-December. Moody’s and Fitch will present their review of Polish ratings late in the week.

© US Global Investors