Certain economic concepts have been a source of frustration to investors over the years. The movement of bond prices up or down to bring existing bonds in line with prevailing interest rates would be one example. We could be seeing declining bond prices over the next ten years when interest rates adjust higher as the economy strengthens. Our reasoning for this will be dissected later in this piece.

The most baffling economic concept for many common stock investors could come into play over those same years. Common stocks perform the best when the economy is lousy and perform poorly when the economy is at its best. Why does poor macroeconomic performance correlate with strong stock markets, and why do strong economic times make for mediocre to poor index performance?

When we are in the depths of the deepest recessions, the Federal Reserve Board pumps money into the financial system and brings down short-term interest rates. In many cases, policy makers in Washington D.C. pull strings or pass legislation which provides fiscal stimulus. In effect, money is shoved into the system and the economy itself.

Despite dismal earnings growth or earnings contraction, stocks rise. In many cases these rallies are huge in percentage. Think of the explosive moves to the upside in 1982-1983, 1991, 2003 and 2009. In 2009, a truly unknown stock picker from Seattle running a small mutual fund was invited onto stock market business channels because they couldn’t find anyone else to be optimistic.

All the money created by the Fed needs to have a home because it is not being used to buy homes or cars or to grow businesses; all of which are activities inhibited by lousy economic conditions. Bonds and stocks receive a great deal of that money and are driven up in price. The most confounding aspect is that only 20% of investors consider themselves bullish at market lows in the middle of these recessions.1 Therefore, it is the movement of money into the system and the under-ownership of common stocks which drives these explosive markets.

The reverse of what happens in economic recessions occurs in strong economic environments. Business owners grow their business or buy property and dip into their common stock ownership for capital. Folks buy houses and cars, borrowing money which drives up the price (interest rates). The Federal Reserve raises short-term interest rates as demand forces longer-term rates higher. Overall business optimism causes investors to be fully invested. The higher interest rates lure current income investors away from stocks paying competitive dividends.

At Smead Capital Management, we like to say that in good economic times, Main Street outperforms Wall Street. Where is the U.S. stock market on the time continuum between the pit of a recession/friendly Fed policies and booming economic times/unfriendly Fed tightening? Where are we on investor sentiment related to these cycles?

As long-duration stock pickers and contrarians, we make no effort to time the stock market, but need to know where the money is currently residing. Here are our best thoughts:

1. We believe we are nowhere near a recession.

Source: Bloomberg. Data for the time period 3/31/1980 to 11/30/2017.

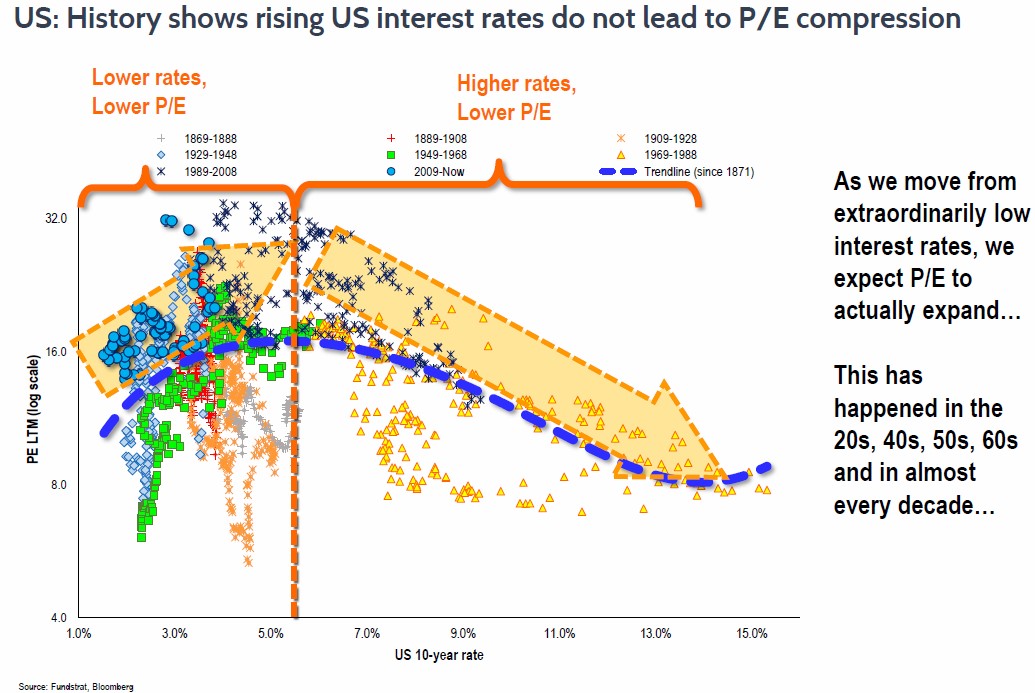

2. The Fed is tightening from very low interest rate levels.

Source: Fundstrat Fall 2016 “State of the Market”, page 52. Data for the time period 1/1/1869 to 12/31/2016.

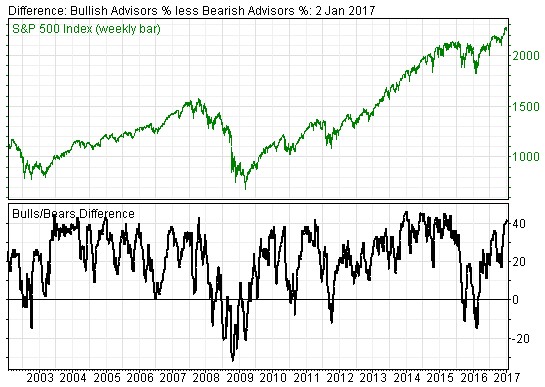

3. Professional sentiment for stocks is dangerously high on an intermediate basis.

Source: Investors Intelligence. Data for the time period 1/1/2003 to 1/2/2017.

*Difference: Bullish Advisors % less Bearish Advisors %: 2 Jan 2017

4. We believe the U.S. economy is likely to surprise to the upside.

Source: BofA Merrill Lynch “Tracking the U.S. Consumer, September 16, 2016.

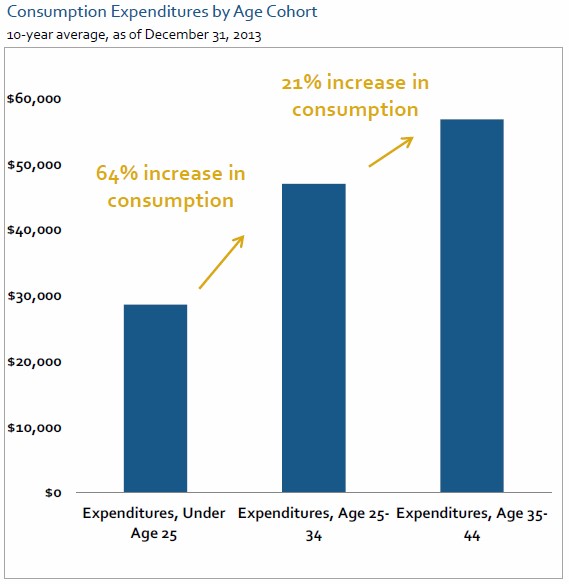

5. The S&P 500 Index is leveraged to technology and high P/E ratios— not to demographic tailwinds.

Source: MorganStanley Investment Perspectives. As of 12/31/2013.

6. Stock pickers could earn their living.

Top three tech stocks in the S&P 500 represent 8.13% of the S&P 500, whereas the top three homebuilders represent only 0.12%.

Source: Fund as of 12/31/2016.

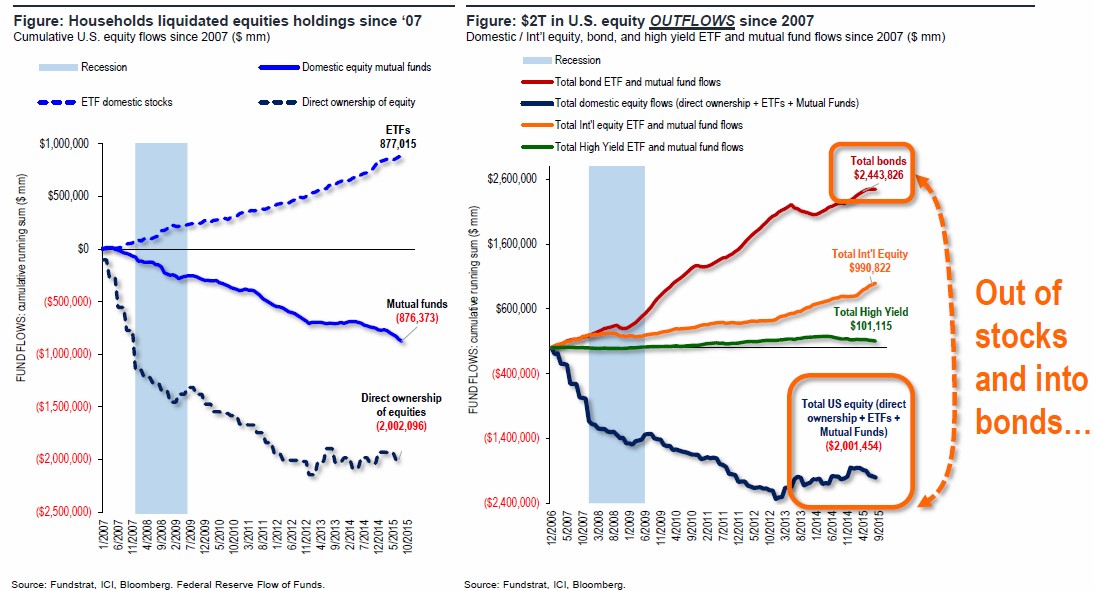

7. Investors are likely to get confounded in the next five years.

Source: 30 Fundstrat. As of 9/2/2015.

8. “Investing is the only sphere of life where victory, security and success is always to the minority and never to the majority.” —John Maynard Keynes

When the economy grows on a real basis at more than 4% for a significant period of time, excesses build up in the system and over-confidence begins to bedevil the future. At that point, we believe the Federal Reserve Board will tighten credit enough to invert the yield curve (short-term rates higher than long-term rates). Historically, when you get a booming economy, high demand for money, and an inverted yield curve, you get a bear market. In my years in the investment business, we inverted the yield curve in 1980-1982, 1987, 1994, 1999-2000 and 2006-2007. Only one of these episodes failed to see a 20% or greater decline in U.S. stock prices, which occurred in 1994 (we called it a “stealth” bear market). Three of those aforementioned declines were greater than 30% in the S&P 500 Index.2

So, where are we now? We believe the U.S. presidential election might be the watershed event that separates the era of lower interest rates/scared common stock investors from higher interest rates/enthusiastic common stock investors. We believe that earnings growth could be easier on Main Street and passive investing could get inhibited by rising interest rates and mute the index returns.

Our companies have balance sheet strength, consistent free cash flow and are less susceptible to the negative impact of higher interest rates. We are emphasizing industries and companies which would benefit from household formation—financials, home builders, and consumer discretionary firms. Lastly, we love an aging population and its basic need of more medicine over the next ten years. This next era in the stock market could very well be tougher, but our stock picking discipline is built for times such as these.

1 Investors Intelligence

2 Bloomberg

© 2016 Smead Capital Management, Inc. All rights reserved.