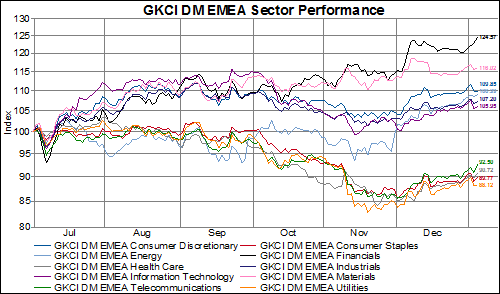

Over the last month, the average European bank has outperformed the broad developed market by about 7%, with more than half of them registering double-digit relative outperformance.

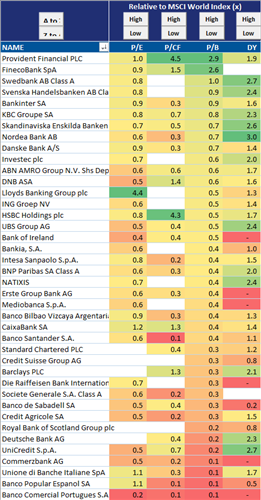

Meanwhile, all but three of these Financials sector stocks currently trade at a significant discount to the P/BV of the broader market– in some cases, up to 90%.

The surge in European Financials (black line, up more than 24%) really began to dominate performance about six months ago.

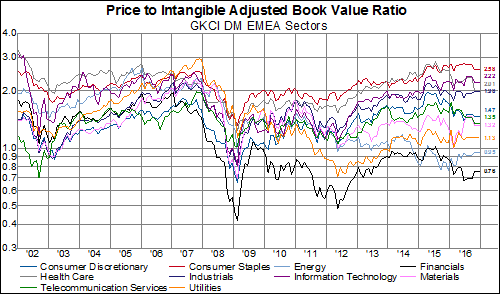

Valuations, however, remain depressed– especially in light of the fact that the leaders of the bull market since the GFC (Consumer Staples, Information Technology) regained pre-crisis valuation levels nearly two years ago.

While these kinds of conditions might peak the interest of some investors, we believe there is ample reason to remain cautious on European banks in general. Peter Zeihan, who regular readers will recognize as our go-to geopolitical strategist, recently published a post detailing why that is the case (Europe’s Next Crisis). Stay tuned for more of Peter’s thoughtful analysis as we prepare the transcript from our latest chat.

© GaveKal Capital

Read more commentaries by GaveKal Capital