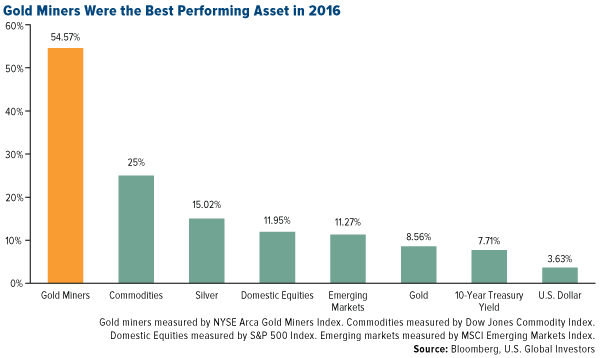

You could say gold miners struck gold in 2016. The group, as measured by the NYSE Arca Gold Miners Index, finished the year up an amazing 55 percent, handily beating all other asset classes shown below.

Miners were followed by commodities at 25 percent and silver at 15 percent. Gold finished up 8.6 percent, its first positive year since 2012, when it gained 7.1 percent. (Keep your eyes peeled for our forthcoming annual periodic table of commodity returns, one of our perennially popular pieces!)

I find it curious that many in the financial media continue to have a bias against gold, even though it generated better returns in 2016 than 10-year Treasuries and the U.S. dollar, which performed half as well. And when it was up as much as 28 percent in the summer, they still didn’t have anything positive to say, arguing it had gone up too much.

(Gold traders, on the other hand, have a much different opinion about the metal right now. A group of traders recently surveyed by Bloomberg revealed they are the most bullish on gold since the end of 2015, soon before it rallied in its best first half of the year since 1974. The traders cited geopolitical concerns, both in the U.S. and Europe, as well as stronger demand in 2017.)

|

And isn’t it interesting that the same media figures who are biased against gold are usually the same ones who seem to have only disparaging things to say about Brexit and President-elect Donald Trump? What they don’t realize is that if Brexit and Trump succeed, so too do the U.K. and the U.S. Are they hoping Brexit and Trump will fail so they can be proved right?

The smart people realize personal politics must be put aside. Despite supporting Hillary Clinton during the primaries, Warren Buffett now says he is behind the president-elect—because he knows that if the U.S. does well, he does well too. Despite campaigning hard against Trump, President Barack Obama says now we should all be rooting for Trump, regardless of our politics.

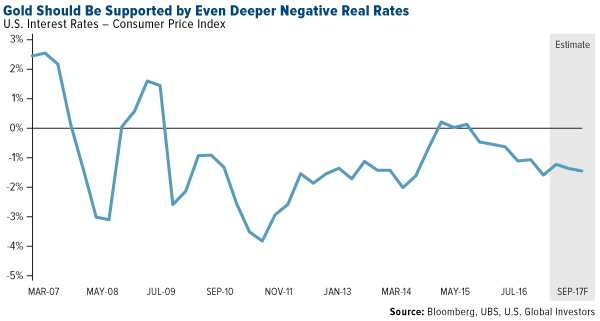

Negative Real Rates Should Drive Gold Prices

But back to gold. Coming up on January 28, we have the Chinese New Year, when demand for the yellow metal historically has risen, along with prices. This will be the year of the fire rooster, one of whose lucky colors is gold.

Throughout 2017, the precious metal should be supported by even deeper negative real rates, which could fall to their lowest level in two years as inflation outpaces nominal interest rate increases, according to UBS. In October, Federal Reserve Chair Janet Yellen suggested there might be some benefit in allowing inflation to exceed the central bank’s target rate of 2 percent before another hike is considered, which is good news for gold. Numerous times in the past I’ve shown that the yellow metal has tended to rise when real rates—what you get when you subtract inflation from the federal funds rate—fell into negative territory.

“Federal Reserve interest rate hikes could weigh on gold prices in the near term,” according to UBS’s house view. “But as real rates fall more deeply into negative territory through the next year, we expect prices to rise toward $1,350 an ounce.”

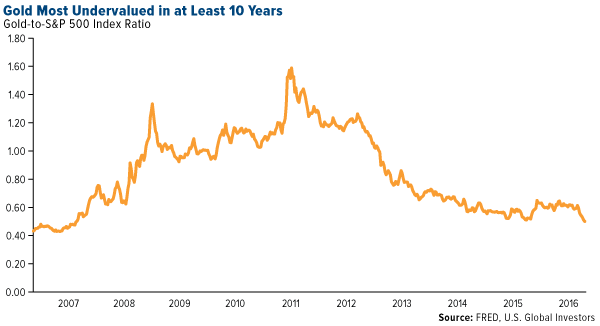

Gold Extremely Undervalued

Since Election Day, domestic stocks have rallied 6.5 percent while gold has dropped as much as 7.6 percent. What this means is gold is looking extremely undervalued compared to the S&P 500, which should appeal to value investors.

Look at the gold-to-S&P 500 ratio below. The lower the ratio, the more undervalued the metal is compared to blue-chip stocks. In fact, gold is at its most undervalued in at least 10 years right now.

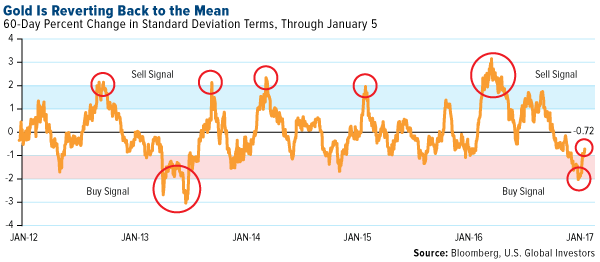

Technically, gold still appears oversold, down almost one standard deviation now. As you can see, it’s moving back to its mean for the 60-day period, but there’s still time to capture potential growth.

Commodities Show Resilience Despite Strengthening U.S. Dollar

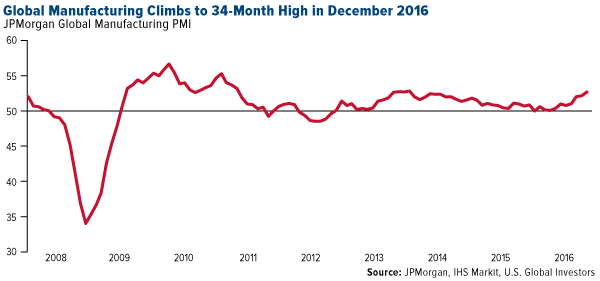

Commodities were the second-best asset class this year because manufacturers and trade are showing improvement.

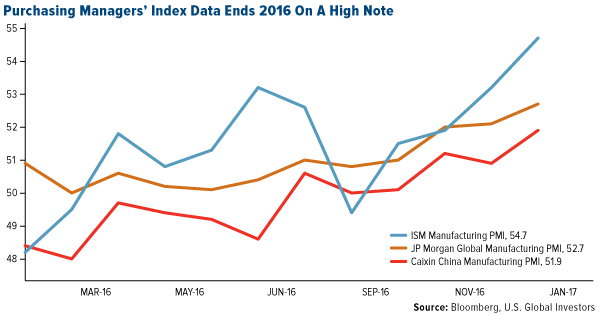

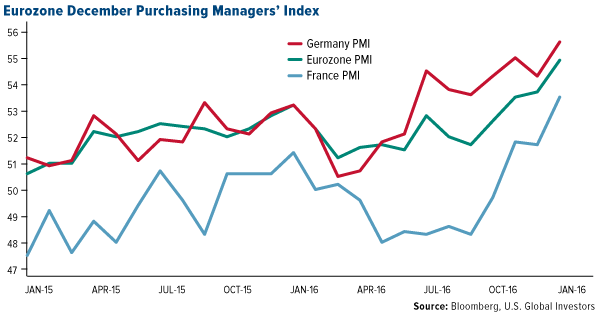

Global manufacturing expanded for the fourth straight month in December, reaching 52.7, its highest reading since February 2014. The individual U.S., Germany, Japan, and eurozone PMIs all hit their highest posts in at least a year, building on a strengthening uptrend that’s been in place since September. International trade volume expansion hit a 27-month high, according to Markit. And despite the “negative” consequence of Brexit, the U.K. Manufacturing PMI posted an amazing 56.1, up from 53.4 in November.

As for commodities, I’m pleased they’ve shown resilience in the face of a strengthening U.S. dollar. CLSA analyst Christopher Wood touched on this very topic in his recent edition of “GREED and fear,” writing that “the renewed dollar strength post Trump’s victory has not been accompanied by renewed commodity weakness. Rather the reverse has happened, with copper rallying, for example, on presumed hopes of increased demand triggered by Trump’s infrastructure policies.”

China’s commodities trading volume has also been impressive, maintaining its rank as the world’s heaviest for the seventh consecutive year.

Of course, price appreciation for commodities and natural resources is inflationary for consumer goods. Because of possibly rising gasoline prices, U.S. drivers are expected to spend about $52 billion more at the gas pump this year compared to 2016, according to GasBuddy’s 2017 Fuel Price Outlook. Three-dollar gas will likely become a reality again in several large cities, including New York, Los Angeles, Chicago and Seattle.

Whatever you end up paying, make it a point this year to stay optimistic. Not only does being optimistic help you stay healthy, both mentally and physically, but it also allows you to see the opportunities that others might not.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average rose 1.02 percent. The S&P 500 Stock Index climbed 1.70 percent, while the Nasdaq Composite rose 2.56 percent. The Russell 2000 small capitalization index jumped 0.75 percent this week.

- The Hang Seng Composite gained 2.04 percent this week, while Taiwan was up 1.28 percent and the KOSPI rose 1.12 percent.

- The 10-year Treasury bond yield fell 2 basis points to 2.41 percent.

Domestic Equity Market

Strengths

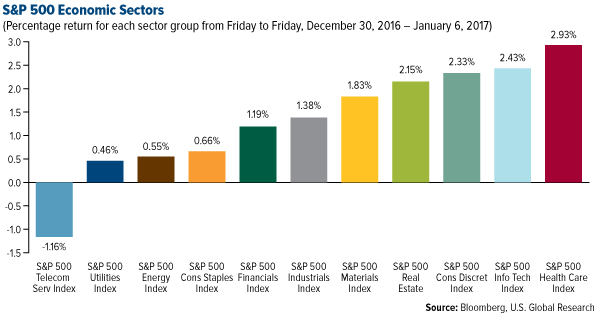

- Health care was the best performing sector of the week, increasing by 2.93 percent versus an overall increase of 1.70 percent for the S&P 500.

- Xerox was the best performing stock for the week, increasing 21.91 percent.

- Weight Watchers jumped by 20 percent after a Tweet from Oprah and a new diet ranking. The company had the fourth-best diet in U.S. News & World Report's new ranking of eating plans on Wednesday, while major investor and board member Oprah Winfrey Tweeted a new advertisement supporting it.

Weaknesses

- Telecommunications was the worst performing sector for the week, falling 1.16 percent versus an overall increase of 1.70 percent for the S&P 500.

- Kohl’s was the worst performing stock for the week, falling 16.10 percent.

- Macy's is closing 68 of its stores. The closings represent about 15 percent of Macy's store base and will affect nearly 4,000 employees. Macy's also said it expects to earn an adjusted $2.95 to $3.10 a share for fiscal-year 2016, down from its previous estimate of $3.15 to $3.40.

Opportunities

- There's finally some good news from the retail sector. Gap announced that sales at stores that have been open at least one year rose by 4 percent versus a year ago, compared with the 1.7 percent drop that analysts were anticipating. Gap raised its full-year profit forecast.

- Publishing powerhouse Meredith Corp. has reportedly approached Time Inc. about a potential merger, according to Alex Sherman at Bloomberg.

- Frontier Airlines is planning to go public. The low-cost carrier has hired Deutsche Bank, JPMorgan and Evercore to help with its initial public offering, The New York Times reports.

Threats

- Barron's Magazine couldn't find anyone that thinks the stock market will tank in 2017. Once again, all the analysts were in agreement that "this bull market has legs.” Such one-sided bullish consensus could be a contrarian sign.

- Department store stocks got crushed after some flagship brick-and-mortar stores reported weak holiday sales. These included JC Penney, Nordstrom, Macy's, Kohl's, and Dillard’s.

- Tesla missed on deliveries for 2016. The electric-car maker reported 22,200 deliveries for the fourth quarter, bringing its 2016 total up to 76,230. This is considerably below the 80,000 to 90,000 vehicles that Tesla had expected to deliver.

The Economy and Bond Market

Strengths

- U.S. manufacturing ended 2016 on a strong note, according to two surveys of the industry. The December purchasing managers’ index data from the Institute of Supply Management and Markit Economics topped expectations.

- Americans ended 2016 with higher confidence in the U.S. economy than they have expressed at any other point since 2008. Gallup's Economic Confidence Index averaged +9 in December, up eight points from November.

- Average hourly earnings climbed 2.9 percent from December 2015, marking the swiftest year-on-year growth since the financial crisis, the Department of Labor reported. The figure rose 0.4 percent in December from the previous month, beating expectations for a 0.3 percent pickup.

Weaknesses

- The U.S. private sector added fewer jobs in December than Wall Street analysts had predicted, pointing to signs that the pace of job growth has slowed as the labor market nears full employment. The non-farm private sector added 153,000 jobs last month, according to data from payroll processor ADP on Thursday. That’s below the 175,000 that analysts surveyed by Bloomberg had forecast, and a fall-off from the 215,000 non-farm private sector jobs added in November.

- The U.S. presidential election results may have been in, but uncertainty was a dominant theme at the Federal Reserve’s December meeting, making it that much more difficult to predict the central bank’s next moves and dampening the market’s reaction to the minutes released from that meeting, economists and strategists said.

- Mortgage applications continued to decline at the end of 2016, consistent with a trend that has persisted since the end of November along with the advent of higher interest rates based on expectations of rising growth and inflation under the incoming Trump administration. Applications decreased 12 percent to December 30, from two weeks earlier, according to data from the Mortgage Bankers Association, which included seasonal adjustments to account for the Christmas holiday.

Opportunities

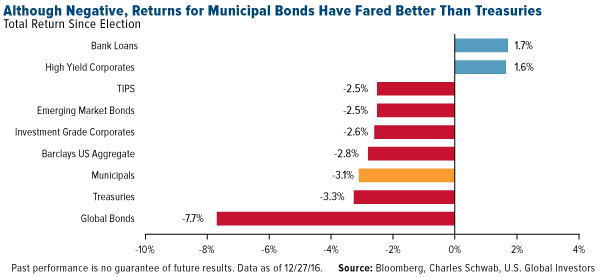

- There has been much attention to the recent rise in interest rates, with many investors believing muni bonds have been harder-hit than other sectors of the bond market—Treasuries, in particular—due to the results of the 2016 U.S. election. Since November 8, yields on most fixed-income sectors have risen, resulting in negative total returns. Nevertheless, munis have actually outperformed Treasuries since the election, posting a return of -3.1 percent compared with -3.3 percent for Treasuries.

- According to Blackstone’s Vice Chairman, the combination of tax cuts on corporations and individuals, more constructive trade agreements, dismantling regulation of financial and energy companies, and infrastructure tax incentives will push the 2017 real growth rate above 3 percent for the U.S. economy. Productivity will improve for the first time since 2014.

- According to HSBC, the "euphoria" surrounding the dollar will end once reality sets in. "The USD rally will reverse as belief in Trump-flation turns to realization that the scale of policy overhaul is relatively modest ('Trump-lite'), and that the results are underwhelming as a consequence ('Trump-failure')," they wrote. "We expect a retracement from mid-year to the end of the year." A retrenchment of the dollar would help multi-national and export-oriented companies.

Threats

- Trump's pick to head the SEC has a history of defending big banks. Transition sources say that Trump will nominate Jay Clayton, a Wall Street lawyer, to head up the Securities and Exchange Commission. He represented multiple banks during the financial crisis including Barclays, Bear Stearns and Goldman Sachs.

- According to Blackstone Vice Chairman’s predictions for 2017, increased economic growth, inflation moving toward 3 percent, and renewed demand for capital will push interest rates higher across the board and the 10-year U.S. Treasury yield will approach 4 percent.

- Already halfway into the 2017 fiscal year, things are not looking good for many states. Twenty-four states have already reported lower-than-expected general fund revenue collections, according to a report by the National Association of State Budget Officers. That’s just one shy of the full 2016 fiscal year, when 25 states reported revenue that trailed what was budgeted.

Gold Market

This week spot gold closed at $1,172.58, up $20.31 per ounce, or 1.76 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 6.75 percent. Junior tiered stocks underperformed seniors for the week, as the S&P/TSX Venture Index climbed just 3.81 percent. The U.S. Trade-Weighted Dollar Index essentially finished the week down slightly by 0.2 percent, but with significant inter-week volatility.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

Jan-2 |

Caixin China PMI Mfg |

50.9 |

51.9 |

50.9 |

|

Jan-3 |

Germany CPI YoY |

1.4% |

1.7% |

0.8% |

|

Jan-3 |

U.S. ISM Manufacturing |

53.7 |

54.7 |

53.2 |

|

Jan-4 |

Eurozone CPI YoY |

0.8% |

0.9% |

0.8% |

|

Jan-5 |

U.S. ADP Employment Change |

175k |

153k |

215k |

|

Jan-5 |

U.S. Initial Jobless Claims |

260k |

235k |

263k |

|

Jan-6 |

U.S. Change in Nonfarm Payrolls |

175k |

156kk |

178k |

|

Jan-6 |

U.S. Durable Goods Orders |

-4.6% |

-4.5% |

-4.6% |

|

Jan-12 |

U.S. Initial Jobless Claims |

265k |

-- |

235k |

|

Jan-13 |

U.S. PPI Final Demand YoY |

1.5% |

-- |

1.3% |

Strengths

- Palladium is starting this year as the best performer among the precious metals, heading for its biggest gain since March, reports Bloomberg. The metal rose 11.17 percent for the week on bets that carmaker demand will grow following positive U.S. and Chinese manufacturing data. Pollution control in China remains a problem, but in the U.S. some auto manufacturers are going to idle some auto plant capacity as dealer inventories are too high.

- Gold traders and analysts surveyed by Bloomberg this week were the most bullish in a year. Those surveyed cited worries over U.S. and European political developments as well as expectations for stronger demand in the Lunar New Year. “Chinese New Year this year will fall on the last week of January, which suggests jewelry purchases are likely to hit their season peak in the next couple of weeks,” Vyanne Lai of the National Australia Bank said.

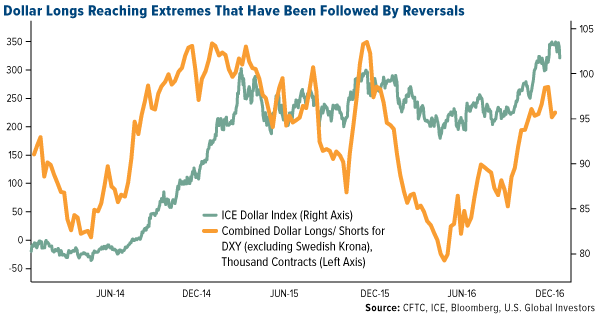

- Investors spooked by a pullback in Treasury yields, saw the U.S. dollar run into a brick wall on Thursday, reports Bloomberg. According to traders, long positions were flushed out from the crowded trade as the dollar broke through a 21-day moving average support level. “The growing backlash against the dollar coincides with more-sober outlooks on whether President-elect Donald Trump’s plans to boost fiscal spending will achieve rapid reflation,” continues another Bloomberg note. As the chart above shows, the net long position is approaching earlier highs and this typically sets the market up for a correction.

Weaknesses

- The worst performing precious metal for the week was gold with just a 1.79 percent rise; however, this is the second week of positive performance for gold following seven weeks of losses.

- Investors pulled $2.27 billion out of the world’s largest ETF backed by gold in December, which is the biggest loss since May of 2013, reports Bloomberg. A look at BullionVault’s Gold Investor Index (measuring the balance of client buyers against sellers), also looks a bit dimmer. The index fell to 55.5 versus 59.3 in November, retreating from a five-year high.

- Gold imports in India have hit a 13-year low, according to a Rediff.com article. Although gold demand increased immediately following the government’s demonetization of 500 and 1000 rupee notes in November, the metal fell sharply in December. In tonnage terms, 2016 gold imports were the lowest since 2003, according to GFMS TR. The organization has estimated the official gold import in 2016 at 492 tonnes, the article continues.

Opportunities

- RBC Capital Markets notes that according to its seasonality analysis on gold, the strongest and most consistent positive price performance for the metal is observed in January and February. The group has re-profiled its quarterly forecasts for 2017, putting gold at $1,245 an ounce. “Overall, in our view, a cautious march higher will occur, but gold prices will likely be at least partially held back by some macro headwinds,” the report continues.

- UBS says that 2017 will be a year that holds plenty of macro and political uncertainties, which should keep precious metals on investors’ radars. The U.K. Supreme Court decision to trigger Article 50, the inauguration of U.S. President-elect Trump and his first 100 days in office, the French and German presidential elections, and the 2017 Indian budget are all major political events that the group highlights as potential market movers.

- Chronically low productivity and labor force growth will make it difficult for central banks to contain inflation once it does begin to accelerate, writes BCA Research in its year-end report. Global bond yields will rise only modestly in 2017, the group believes, but could begin to surge as the decade wears on. In the report entitled “The Long and Winding Road to Stagflation,” the group goes on to say: For the next few years, the likelihood of a disorderly rise in inflation is extremely low. Beyond then, however, the risk is that inflation surprises to the upside, perhaps significantly so.

Threats

- In a report released Friday, ABN Amro said that gold could sink below $1,100 an ounce on the back of strong U.S. data. “As long as U.S. real yields rise, and there are no major inflation fears, gold prices will go lower,” the bank says. Analyst Georgette Boele added that the last leg of a powerful rally in the dollar is in full swing, aided by higher equities, expectations of further rate hikes, and expectations of a strong uplift in the U.S., reports Bloomberg.

- There are numerous factors creating a more positive environment for gold right now, writes ICBC Standard Bank. Trump’s increasingly protectionist Tweets, the U.S. 10-year yields falling by 24 basis points, and a jump in European CPI, have all contributed to the metal being up almost 5 percent from its December lows. “However, we think this is a false dawn for gold.” Despite this near-term sentiment for the metal, the bank says a more sustainable turn in gold will likely have to wait until mid-year, by which time “we think disappointment on the lack of policy delivery by a congested Congress and the U.S. debt ceiling will start to dominate the news flow.”

- HSBC believes that one of the puzzling things about December’s FOMC meeting was the contradiction between the unchanged growth and inflation forecasts for 2017, and the rise in the median projection for rate hikes this year, from two to three. The meeting minutes show that the outcome of the presidential election led many policymakers to change their view regarding the “risks” to their forecasts. An article on Business Insider even notes the disagreement seen within the Fed, based on the meeting minutes. The article states, “The most salient discord appeared to be between the view of Fed economists, or ‘staffers’ and the sitting policymakers.” HSBC also noted in its report that these minutes show the policymakers’ uncertainty about the fiscal outlook, which could suggest there is no intention to hike the federal funds rate in the near-term. HSBC continues by explaining that it sees the next rate hike taking place in June, followed by another in December.

Energy and Natural Resources Market

Strengths

- Manufacturing PMIs across the world all finished 2016 on a high note. China’s Manufacturing PMI, the engine of global economic growth, hit a four- year high, rising to 51.9. This is the sixth-straight month of growth, marking the strongest upturn in Chinese manufacturing conditions since January of 2013. The uptrend in manufacturing PMIs across the globe marks a very positive note for commodities as they positively correlate with this important economic indicator.

- The best performing sector for the week was the S&P/TSX Composite Gold Index. The index rose 7.4 percent on the back of rallying gold prices as the yellow metal rebounded from an oversold condition, and benefited from U.S. dollar weakness caused by rallying Chinese renminbi prices.

- Freeport-McMoRan Inc., the largest U.S. copper producer, was the best performing stock this week, finishing up 13 percent. The stock rose following appreciating copper prices, as investors sought to gain exposure to the reflation trade.

Weaknesses

- Natural gas prices fell violently this week as weather forecasters expect warmer than normal seasonal temperatures. The price of the commodity fell 7.5 percent as weekly inventory drawdowns came in well below seasonal norms.

- The worst performing sector this week was the S&P Oil & Gas Refining & Marketing Index. The index fell 1.6 percent as gasoline inventories rose 8.3 million barrels, the largest amount in at least year.

- The worst performing stock for the week was Bunge LTD, a major agribusiness and food producer. The company fell 2.9 percent after analysts downgraded earnings expectations for peer companies, expecting greater competition from South American crops in 2017.

Opportunities

- The Chinese renminbi surged 87 basis points on speculation of central bank intervention, posting its biggest two-day gain on record. The move took many strategists by surprise as China has been burning through foreign exchange reserves in an attempt to curb the renminbi’s depreciation. The move should prove bullish for base metals and materials which are heavily dependent on Chinese import demand.

- Palladium started 2017 with a 12.2 percent rally. The rally was sparked by positive data coming out of the world’s two largest economies--manufacturing in the U.S. and China both came out as positive, particularly in the automotive sectors, a primary driver for palladium demand. In addition, only six days into the New Year, London has already broken legal limits for toxic air and China is in a crisis as the entire country faces severe smog. This environmental epidemic should act as a positive catalyst for palladium demand, the key component in catalytic converters.

- Capital expenditure cuts by miners will magnify metal shortages over 2017, according to Reuters. Capital expenditures have steadily dropped over the course of the last four years as companies have struggled to maintain their balance sheets. In 2016 alone, miners are estimated to have slashed capital expenditures by 24 percent or $52.3 billion in total. The result should be positive for metals prices, as the lack of capital expenditures has historically created tremendous imbalances, constraining supplies around the globe and boosting growth prospects.

Threats

- Gasoline demand may be peaking. Over the course of the last two years cheap oil prices have helped keep gasoline prices low and push demand higher; however, demand has steadily dropped off as prices have recovered, with consumption falling to 8.75 million barrels per day from 9.75 million, the lowest level in two years. With consumers moving toward compact vehicles and more electric vehicles entering the marketplace, gasoline consumption will be further challenged moving into the future.

- Iron ore prices will pull back this year according to RBC Capital Markets, who ranked first in predicting commodity prices in 2016. The firm believes that current prices are not sustainable at current levels as holdings at ports in China are showing signs of abundant supply. Holdings rose 2.7 percent in the final week of the year alone, rising to an all-time high.

- November U.S. factory orders plunged the most since august 2014. The month of October prior to the election posted one of the highest results last year rising 2.6 percent; however, November’s report came in at negative 2.4 percent despite a rally in defense aircraft orders. The slowdown should be reflected in weaker demand for industrial metals.

China Region

Strengths

- Happy New Year! The Philippines Composite Stock Index soared 5.64 percent in the first week of 2017, leading the charge in a week that saw a rise in all regional indices.

- Singaporean year-over-year GDP beat expectations; analysts were looking for a gain of 0.3 percent but actual numbers came in showing a growth rate of 1.8 percent.

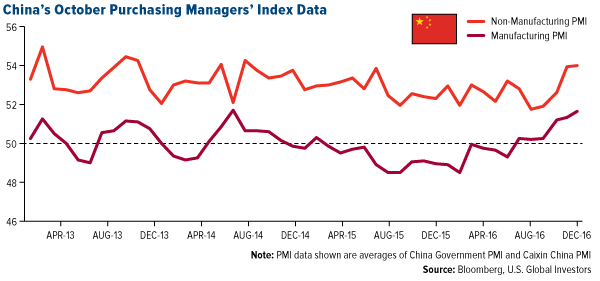

- The Caixin China Manufacturing PMI came in at 51.9 for the December period, well ahead of expectations for a flat 50.9 print. Official manufacturing PMI came in just shy of expectations—at 51.4 vs. 51.5 expected—while official non-manufacturing PMI was a 54.5, down from last month’s 54.7. The Caixin Services PMI, on the other hand, was a 53.4, up from last month’s 53.1.

Weaknesses

- Nikkei Malaysia PMI came in flat at a 47.1, still languishing at its lowest level of the past year. The Nikkei Philippines Manufacturing PMI came in at 55.7, down from the prior month’s 56.3.The Nikkei Indonesia Manufacturing PMI dropped to 49.0 for the December period, down from its previous print of 49.7 for November.

- The Hang Seng Consumer Services Index finished the week as the weakest sector in the Hang Seng Composite Index (HSCI), up only 39 basis points since last Friday’s trading.

- Bloomberg News reports that India is forecasting its growth will slow to a three-year low even before accounting for possible effects of PM Narendra Modi’s demonetization scheme.

Opportunities

- Morgan Stanley analysts upgraded Hong Kong-listed technology hardware and optics producer Sunny Optical Technology Group Co. Ltd. (2382 HK) this week, suggesting the company may have a “rosy” 2017 outlook, hold and continue to gain share, and grow with Chinese original equipment manufacturers in the handset and automotive industries. The stock was one of the HSCI’s top gainers for the week, rising just under 10 percent in that timeframe.

- The Lunar New Year holidays begin later this month, which may bring some positive sentiment and seasonality to the coming weeks.

- Chinese investors traded a record volume of commodity futures last year, Bloomberg News reports, up some 27 percent from the prior year, constituting a fifth-straight year in higher aggregate trading volume.

Threats

- Rhetoric remains elevated and many details remain unclear with respect to U.S. trade policies under the incoming Trump administration.

- The largest U.S. ETF focusing on China—the iShares China Large-Cap ETF— suffered among the biggest outflows in emerging markets, as total assets in the ETF dropped to the lowest level in a decade.

- Yuan weakness and capital outflows from China remain an ongoing threat. While the renminbi did claw back a record two-day gain against the U.S. dollar this week, weakness set in again on Friday as Goldman Sachs advised clients that the best times to bet against the currency have been following major interventions like the one this week, presumably designed to squeeze short sellers. This weekend China also releases its latest FX reserve number, which has hovered around 3 trillion and remains intimately tied to yuan weakness (or perceived weakness).

Emerging Europe

Strengths

- Hungary was the best performing country this week, gaining 2.7 percent this week. Industrial production rose 0.6 percent year-over-year in November, reversing a 2.1 percent fall in October. November retail sales year-over-year rose by 4.7 percent above the expected 3.8 percent and prior 2.6 percent.

- The Russian ruble was the best performing currency this week, gaining 3.3 percent against the dollar. Inflows continue into Russian bonds and equity funds, as investors speculate that Russia will benefit this year from higher oil prices after OPEC delivers its output cut deal. Brent crude oil dropped slightly this week, closing at $56.70 per barrel.

- Health care was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst performing country this week, losing 1.3 percent. Turkey will extend the government’s state of emergency powers by another three months following the deadly New Year’s attack claimed by Islamic State, as the country struggles to contain rising terrorist threats. The state of emergency had been due to expire on January 19, enacted after the failed July 15 coup.

- The Turkish lira was the worst performing currency this week, losing 3.4 percent against the dollar. President Recep Erdogan once again asked banks to cut rates in order to support the economy. Investors must doubt that the Turkish central bank will act against Erdogan’s will and hike rates to stop the currency fall and get on top on the rising inflation problem.

- The industrial sector was the worst performing sector among eastern European markets this week.

Opportunities

- The eurozone manufacturing PMI matched the flash estimate of 54.9, which is the highest level in five and half years. The strong eurozone PMI reading was mostly supported by Germany’s three-year high reading of 55.6 and France’s five-year high reading of 53.5. Several emerging European economies reported very strong PMI data as well: Poland 54.3, Russia 53.6, and Czech Republic 53.8. All of these PMI numbers signal strong fourth-quarter growth.

- Marine Le Pen, who leads the far-right Front National party in France and is a candidate in April’s presidential election, has said that Russia’s annexation of Crimea was not illegal, explaining that a referendum was held and residents of Crimea chose to rejoin Russia. If she wins the presidency on April 17, Vladimir Putin will gain more support from the West.

- Czech Republic posted a 62 billion koruna ($2.4 billion) budget surplus last year versus the original plan for a 70 billion koruna deficit, mostly attributable to lower government spending and higher tax collection boosted by economic growth. The result has helped to boost investor demand for Czech government bonds, cutting the yield of 10-year notes to 0.49 percent, or 23 basis points above comparable yields on German notes, from 2.5 percent three years ago.

Threats

- Mike Harris points out in his Turkish strategy report that Turkey is likely to remain among the most vulnerable markets globally. That vulnerability will likely last at least through early March, but it could see a rebound once Erdogan gets his Executive Presidency. We do not know when or if the referendum will happen, but it could be as soon as mid-March.

- The European Central Bank said Banca Monte dei Paschi Spa needs about 8.8 billion euros ($9.2 billion) to bolster its balance sheet, almost twice the amount the Italian lender had sought to raise in a failed capital increase. The Italian government approved as much as 20 billion euros to bailout banks.

- The initial reading of euro-area inflation for December revealed acceleration to 1.1 percent year-over-year from 0.6 percent. The majority of the rise is due to energy prices and to a lesser extent food, alcohol and tobacco costs. The only part of the rise that appears domestically generated may be linked to the volatile costs of package holidays in Germany and could be reversed in January, according to Bloomberg economist David Powell.

© US Global Investors