Key Points

- Can the sharp rally in stocks be solely attributed to the results of the presidential election?

- Confidence is rising among business leaders, consumers and investors…will it be rewarded?

- Investor sentiment (as always, perhaps) is likely to be a key determinate of equity market behavior in 2017.

In conjunction with the publishing of a summary of Schwab's 2017 outlook across asset classes; this report is a more detailed summary of my 2017 outlook, with a dash of rear-view mirror analysis of the year just ended. Each of the broad topics discussed below will be further unpacked over the next couple of months in individual reports.

What a difference a couple of months make. Much of the stock market’s sharp rally since the presidential election has been credited with, well, the presidential election. There is no question we are witnessing rising business, consumer and investor confidence in keeping with the more business-friendly proposed policies of the incoming Trump administration. That said you could have looked in the rearview mirror on Election Day and seen an improvement in the economy along with a return to positive earnings growth.

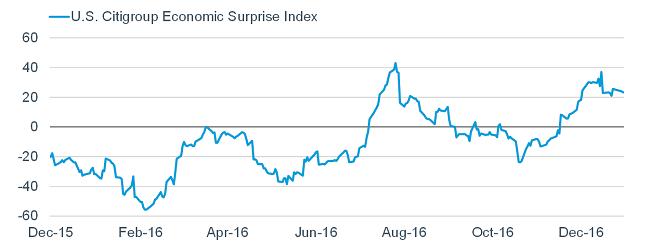

Economic inflection

As you can see in the chart below, the surge in the Citigroup Economic Surprise Index began in the third week of October. This index measures how data releases have compared to consensus expectations.

Source: FactSet, as of December 30, 2016.

Remember, this index measures relative change, not absolute growth. But it emphasizes the power of rate of change and offers an opportunity to again relay one of my mottos: Better or worse usually matters more than good or bad when it comes to the stock market. In other words, when things stop getting worse and begin to get better (the inflection point), it’s typically the launch pad for stocks given that they are one of the key leading economic indicators. A common error of equity investors is waiting until the economic data is good, instead of keying off the inflection point from deteriorating to improving.

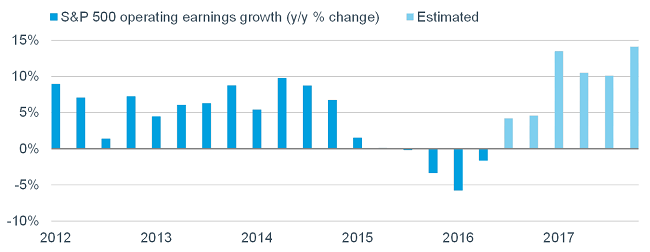

Earnings inflection

The inflection point has also occurred in corporate earnings, as you can see in the chart below. Aggregate S&P 500 earnings spent four consecutive quarters in an earnings recession; with the third quarter of 2016 marking the turn from negative to positive. However, earnings actually bottomed in the first quarter (at the low in year-over-year change); helping to explain the market’s 25% move from the February 2016 low to December's high.

Source: Thomas Reuters, Yardeni Research, Inc, as of December 30, 2016. 3Q16-4Q17 based on estimated earnings growth.

The jump in earnings growth to 12% currently expected for 2017 helps ease a valuation concern. On forward 12-month earnings, the S&P is presently trading at a 17 multiple; only slightly higher than the 20-year median. And as you can see in the table below, inflation remains (for now) in a “sweet spot” of sorts for valuations historically.

Source: Bureau of Labor Statistics, FactSet, as of November 30, 2016. Inflation is y/y % change based on core CPI. P/Es based on forward 12-month earnings.

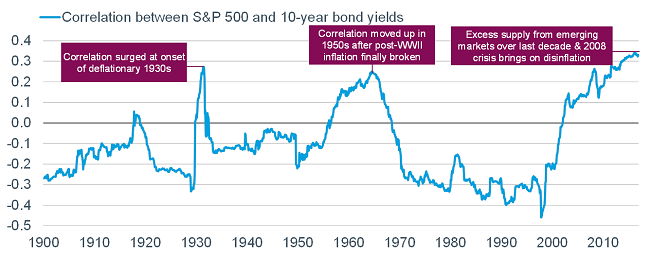

Bond yield inflection

Another factor impacting stocks in 2016 were bond yields, but perhaps not as many might have expected. The 10-year Treasury yield fell sharply in the first half of the year, but rebounded equally sharply in the second half of the year. We have all been taught that rising bond yields cause trouble for stocks…but not always.

As you can see in the chart below, we are presently in the third major era of a positive correlation between bond yields and stock prices.

Source: FactSet, The Leuthold Group, as of December 30, 2016. Rolling 10-year correlation between monthly % change in S&P 500 and 10-year bond yields.

All three periods were characterized by deflation/disinflation; during which time yields were rising from an extremely low base, thereby not breaching a level which would choke off growth. In addition, if bond yields are rising due to growth improving, but without inflation taking off, stocks tend to do well in this environment.

Looking ahead

Early in 2017 we will all start grappling with the connection (or possible lack thereof) between campaign promises and policy reality. President-elect Trump has elevated tax cuts/reform, increased fiscal spending, and regulatory overhaul to the top of the priority spectrum—all laudable pro-growth policies. However, the continued pressing of his isolationist, anti-trade, and pro-tariff promises could serve as a detrimental offset to the pro-growth agenda, highlighted below.

I liked this comment from Oxford Economics: “Recent Treasury Secretary [Steven Mnuchin] and Commerce Secretary [Wilbur Ross] nominations indicate a desire to press hard on the fiscal accelerator while using the trade brake pedal with parsimony." Let’s hope.

Tax reform

Even unpacking what appear to be the more economically-beneficial proposals yields concerns about whether reality will resemble the promises. Having served on President Bush’s bi-partisan tax reform commission in 2005, I am personally thrilled that comprehensive tax reform—or at least corporate tax reform—is on the agenda. However, the devil—as always—is in the details.

History has shown that when it comes to tax reform, what is ultimately legislated can vastly differ from what was originally proposed. The other rub is the cost: According to the Tax Policy Center, Trump’s tax plan would add about $6 trillion to federal debt over the next ten years, and more than $20 trillion over the next 20 years. Even with rosy growth assumptions applied (i.e., "dynamic scoring"), the math around deficits/debt is fairly ugly.

The benefit of corporate tax reform is bit clearer. The U.S. marginal corporate tax rate is nearly 39% when including state/local taxes; ranking it highest among all global industrial countries. The median rate for the other 34 OECD countries is less than 25%. An important caveat though relates to ample deductions offered in the U.S. tax code—such that the actual effective tax rate for U.S. non-financial companies averaged about 25% as of 2016’s second quarter. But even from that base a move down to somewhere in the 15-20% range could help corporate bottom lines immensely.

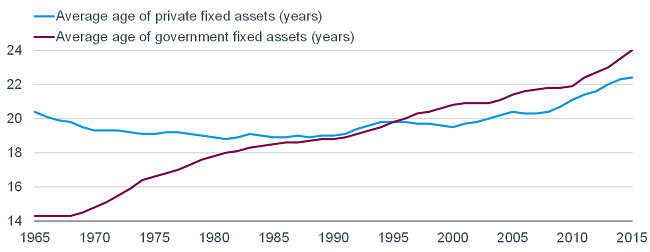

Infrastructure spending

Much of U.S. infrastructure is either busted or significantly aged (see chart below highlighting the latter). Having just flown in and out of LaGuardia Airport over the holiday break I can personally attest to that. As presently detailed, the Trump administration favors private/public partnerships as opposed to federally-funded spending. Given the lessons learned in 2009 about just how "shovel ready" projects actually were, these plans are likely to take some time to put together; meaning this component of fiscal stimulus could be more of a 2018 story.

Source: Bureau of Economic Analysis, FactSet, as of December 31, 2015.

Regulatory reform

Could the bull market in corporate compliance be coming to an end? Fewer regulations means lower compliance costs for companies—certainly among financial companies which might see a lessened burden from changes to the Dodd-Frank legislation. As my friend Ed Yardeni—one of Wall Street’s best economists—noted in his final missive of the year:

"This could lead to another wave of destructive crony capitalism, the kind that contributed to the financial crisis of 2008. Or else, combining the talents of America’s smartest dealmakers, savviest business executives, and high-powered technology leaders could boost growth in America, especially if lower corporate and personal income tax rates revive animal spirits…"

I am hoping for the latter.

Ideological shift

One of our themes at Schwab for the New Year is "regime change." It refers to the aforementioned shift toward fiscal stimulus—and away from monetary stimulus being the only game in town. But there is another equally powerful regime change coming and that is between ideologies. In characteristically blunt terms—but perhaps surprising given his non-political stance historically—Ray Dalio, founder and head of Bridgewater, the world’s largest hedge fund, had this to say in a LinkedIn influencer article titled "Reflections on the Trump Presidency, One Month After the Election:"

"…it is increasingly obvious that we are about to experience a profound, president-led ideological shift that will have a big impact on both the US and the world. This will not just be a shift in government policy, but also a shift in how government policy is pursued. Trump is a deal maker who negotiates hard, and doesn’t mind getting banged around or banging others around. Similarly, the people he chose are bold and hell-bent on playing hardball to make big changes happen in economics and in foreign policy (as well as other areas such as education, environmental policies, etc.)."

Dalio went even bolder when opining that the "new administration hates weak, unproductive, socialist people and policies, and it admires strong, can-do, profit makers. It wants to, and probably will, shift the environment from one that makes profit makers villains with limited power to one that makes them heroes with significant power."

Animal spirits awakening

The summary of Schwab’s 2017 outlook highlighted "animal spirits" as having awakened after a long slumber. A final quote from Dalio that bears consideration: "Regarding igniting animal spirits, if this administration can spark a virtuous cycle in which people can make money, the move out of cash (that pays them virtually nothing) to risk-on investments could be huge."

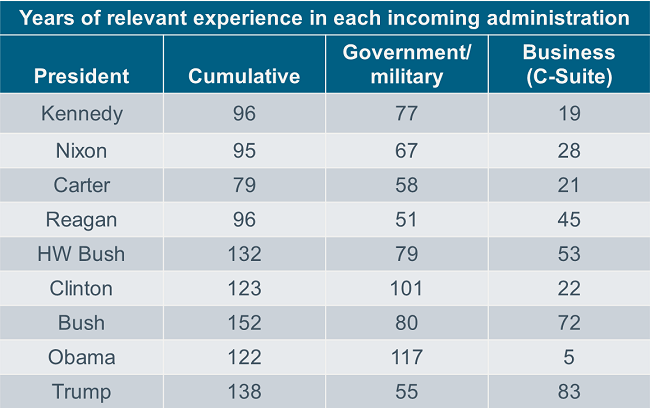

For those looking for a more business-oriented administration, look no further than the significant difference in the incoming administration’s business experience relative to prior administrations.

Administration counts the President, Vice President, Chief of Staff, Attorney General, and secretaries of State, Defense, Treasury and Commerce. Source: Bridgewater Associates, L.P.

The business-friendly approach is having a decidedly positive impact on business confidence, with the chart below one of several well-watched indicators.

Source: The Duke University/CFO Magazine Business Outlook Survey, as of December 31, 2016. Quarterly survey that measures CFOs' expectations for the economy and their company.

Optimism, with a dose of caution

We share the optimism as it relates to the U.S. stock market in 2017 and believe it will outperform developed market international equities. But the trajectory of gains will likely not be as fierce as witnessed immediately post-election; and we do expect bouts of volatility for several possible reasons, including:

- The aforementioned transition between Trump’s candidacy and Trump's presidency

- Inflation or growth could heat up enough that the Fed would have to be more aggressive than expected hiking rates

- Continued U.S. dollar strength would tighten financial conditions and hurt multi-nationals’ earnings

I was pleased to see the consolidation occur in the final couple of weeks in 2016. That is a healthier pattern for equities than a "melt-up" with no pauses. As I often opine, investor sentiment (as a contrarian indicator) may hold the key to the shorter-term volatility we might witness.

As per data from Bespoke Investment Group (BIG), after a two-year span in which the S&P 500 never went more than 34 trading days without making a 52-week high, U.S. stocks went 285 days without a new high. It wasn’t until the “Brexit” vote that the S&P 500 was able to break out of its range and end what was the longest streak without a 52-week high since the early days of the bull market.

Investor optimism on the rise

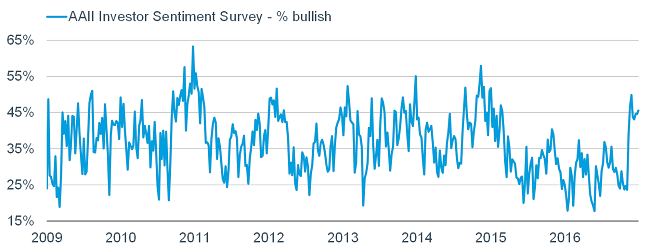

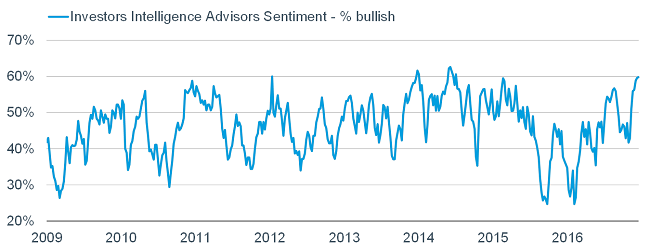

But with the surge in the market has come the commensurate surge in investor sentiment. Two of the more popular sentiment measures come from American Association of Individual Investors and Investors Intelligence (the latter being the sentiment of investment newsletter writers). Heading into and in the early weeks of 2016, bullish sentiment was plumbing the depths of despair. But the finale of the year was an entirely different story, as you can see in the charts below.

Source: American Association of Individual Investors (AAII), FactSet, as of December 30, 2016.

Source: FactSet, as of December 16, 2016.

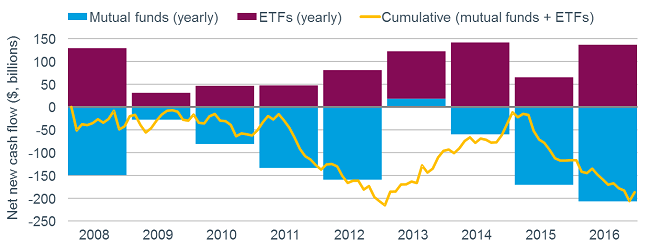

Remember, investor sentiment—at extremes—tends to act as a contrarian indicator; so measures such as those above bear close watching. The good news is that although optimism may be a tad too frothy, these are attitudinal measures of investor sentiment. There are also behavioral measures of investor sentiment, and here’s where the story gets juicier. The most common behavioral sentiment indicator is fund flows. The chart below shows what we have been highlighting for much of this bull market: investors’ distaste for U.S. equities—even including the more popular exchange-traded funds (ETFs) along with traditional mutual funds.

Source: Investment Company Institute (ICI), as of November 30, 2016. Chart plots domestic equity net new cash flow.

There has been barely a spec of renewed interest in U.S. stocks—surprising perhaps given how ferocious the rally has been. Herein lays an opportunity for the market. After years of shunning stocks in favor of bonds and other more defensive asset classes, the burst of performance—and the optimism that’s accompanied it—could finally spark some buying interest in U.S. equities. And there is a lot of runway ahead of us on that front.

In sum

We remain optimistic that this is an ongoing secular bull market in U.S. stocks; and the risk of it ending swiftly is low. Bear markets tend to sniff out economic recessions and with growth accelerating from its below-trend pace, the risk of that is also low. Sentiment-related economic indicators have recently soared, including the stock market itself—and specifically financial stocks; consumer sentiment, the Housing Market Index (HMI), the Small Business Optimism Index. In addition, credit spreads have behaved well and the yield curve has generally steepened. All of this suggests improving growth and low near-term recession risk.

Ironically though, one of my concerns is that the market’s rally could become more of a "melt-up." As good as they feel (for investors in the market) while they're underway, they don’t tend to end well; so keep an eye on investor sentiment for overt signs of excess optimism. Remember the power of discipline and periodic rebalancing. Enjoy the ride, but don't get greedy.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

(0117-SPY2)

© Charles Schwab

© Charles Schwab

Read more commentaries by Charles Schwab