KEY TAKEAWAYS

- Economic momentum, fiscal policy likely to be enacted by mid-2017, and a more business-friendly regulatory environment may help real GDP growth accelerate to a range closer to 2.5% in 2017.

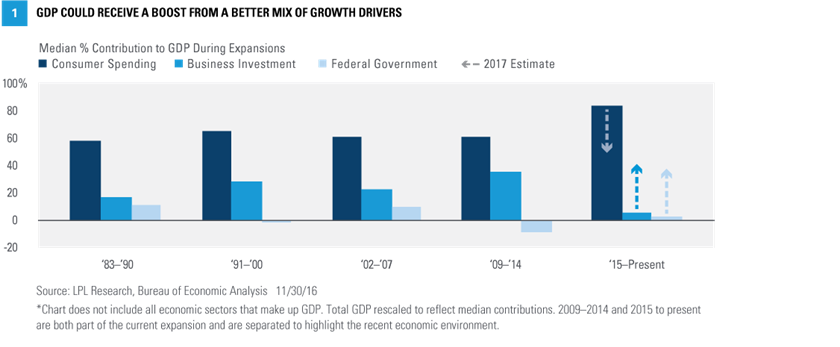

- Faster growth would likely include a shift in growth drivers from an emphasis on the consumer to a mix that includes manufacturing, capital expenditures, and government spending.

- If we meet the Fed’s forecasts for the economy, labor market, and inflation in 2017, the Fed is likely to raise rates twice during the year, with three times more likely than one.

In 2016, the U.S. economy navigated some difficult challenges including low oil prices, a strong dollar, tightening financial conditions, and the threat of deflation. As we turn the calendar to 2017, concerns have shifted. Oil prices have stabilized; while the dollar, despite receiving a post-election boost, is unlikely to create the kinds of headwinds it created over the last three years. Increased anxiety over deflation in 2015 and early 2016 has flipped to “reflation” concerns. Conversations about fiscal austerity, through mechanisms like budget sequestration that left the economy relying on monetary stimulus through the Federal Reserve (Fed), have turned to a drum beat for fiscal stimulus through tax reform and infrastructure spending while the Fed slowly normalizes monetary policy. We have even started to see steadying in the manufacturing sector, following contraction under the influence of low oil prices, a strong dollar, and weaker global growth. Although the economy remains more fragile than during most prior expansions, these turning points have marked the economy’s ability to navigate a challenging period.

MOMENTUM SHIFTS

Taking into account all of these milestones, we believe the economic recovery that began in mid-2009 will likely pass its eighth birthday in 2017, as leading economic indicators continue to suggest low odds of a recession starting next year. However, the risk of a recession due to a policy mistake has risen over the course of 2016. The pro-growth policies likely to be enacted in the first half of 2017 by Trump, including corporate and personal tax cuts, increased spending on infrastructure and defense, and deregulation, may help to boost economic growth in 2017 and 2018 and increase the economy’s potential growth rate (while changing the mix of growth drivers). However, they may also lead to some of the “overs” that tend to emerge at the end of expansions (overconfidence, overborrowing, overspending), naturally accelerating the economic cycle and bringing a recession sooner than otherwise might have been the case.

Focusing on 2017, between the economic momentum that started in late 2016, the boost from fiscal policy likely to be enacted by mid-2017, and a more business-friendly regulatory environment, real gross domestic product (GDP) growth may accelerate to a range closer to 2.5% in 2017, after spending most of the first seven-plus years of the expansion averaging just over 2.1%. The boost in 2017 comes as the main drivers of growth shift from an emphasis on the consumer to a mix that includes manufacturing, capital expenditures, and government spending [Figure 1]. Potential contribution from trade (net exports) remains a wild card, as the Trump administration’s trade policies, while attempting to shift the balance of exports and imports, may have a dampening impact on long-term trade growth. In addition, the deficit could make a comeback as a key economic topic for markets and policymakers in the aftermath of a potential shift to fiscal stimulus through lower taxes and increased infrastructure and military spending.

Of course, new risks could be around the corner. The Fed may start raising rates in earnest, if slowly, after a one-year hiatus between December 2015 and December 2016. Raising rates at this stage would simply reflect an improving economy, but finding the proper pace for rate increases will be a challenge. President-elect Donald Trump has expressed intentions to renegotiate trade agreements, but will face the challenge of improving them without starting a harmful trade war. And although fiscal stimulus may give a boost to growth, long-term challenges for the federal debt and budget deficit loom in the background.

PATH TO NORMALIZATION

Federal Reserve Is Fueling Up

At the start of 2016, the disconnect between the Federal Reserve and the federal funds futures market about the anticipated future direction of monetary policy was striking. The Fed, which had just initiated its first tightening cycle in more than 11 years in December 2015, anticipated raising rates by 200 basis points (2.0%)* over the course of 2016 and 2017, which would put the fed funds target rate at around 2.375% by the end of 2017. Meanwhile, the market was pricing in just four 25 basis point hikes over the course of 2016 and 2017, putting the fed funds target rate at just 1.375% by year-end 2017. The 100 basis point disparity, the equivalent of four 25 basis point rate hikes, was so wide that it led to a number of destabilizing global imbalances in the first few months of 2016, which in turn contributed to the financial market turmoil over the first six weeks of the year.

As of late 2016, the Fed has raised rates just once more, at its final meeting of the year in December, leaving the fed funds target rate at about 0.625%. If its outlook for the economy, labor market, and inflation is met, the Fed said it would raise rates 75 basis points in 2017 and 75 basis points in 2018, leaving the fed funds target rate 2.125% at the end of 2018. Meanwhile, the market now sees roughly two hikes in 2017 and two in 2018, putting the fed funds target rate around 1.825% at year-end 2018. At around 25 basis points, the disagreement on the path of rates over the next two years is likely to prove much more manageable for global markets to absorb than the 100 basis point gap at the start of 2016.

Our view is that we may meet the Fed’s forecasts for the economy, labor market, and inflation in 2017, leading the Fed to raise rates twice during the year. The economy might receive a boost from fiscal stimulus, which can lead to a virtuous cycle of added confidence and the release of what economists colorfully refer to as the economy’s “animal spirits,” where greater confidence leads to increased activity. If this happens, it will push GDP growth above its currently muted potential, tighten resources, increase labor costs, and ultimately drive inflation. Given this possibility, our estimate of two rate hikes has an upward bias with three hikes more likely than one, especially if inflation moves above 2.0% and remains there, as we expect.

*Basis points (bps) refer to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, and is used to denote the percentage change in a financial instrument.

PRESSURE INCREASES ON LABOR MARKET

The disconnect between the Fed and the market regarding the path of interest rates will likely narrow further in 2017; however, the disconnect between the Fed and the market on the labor market will likely widen. The market may view a potential slowdown in the pace of job creation as a recession signal, while the Fed may continue to see it as consistent with a labor market near full employment.

Since early 2010, the unemployment rate has dropped from nearly 10% to the most recent reading of 4.6%, a new cycle low. In its most recent set of economic projections (released in mid-December 2016), the Fed’s policy arm, the Federal Open Market Committee (FOMC), projected the unemployment rate at 4.5% by the end of 2017, just a modest improvement from current levels. Fed Chair Janet Yellen has noted that although the unemployment rate is not the perfect measure of slack in the labor force, if she had to focus on just one number, that would be it. Of course Yellen has often noted that the Fed watches a “broad range of labor market indicators” to gauge the health of the labor market. On balance, all but a handful of these indicators have returned to their pre-Great Recession levels.

One of the reasons the Fed cares about the labor market is that less slack in the labor market leads to wage pressures. Wages represent around two-thirds of business costs and, over time, higher wages lead to higher inflation. Wage inflation (as measured by the year-over-year gain in average hourly earnings) has moved from a low of near 1.5% in 2012 to near 3.0% at the end of 2016, but has not yet reached its pre-Great Recession pace of 4 – 4.5%. But the market, and perhaps even the Fed, may be surprised by how quickly wages could accelerate toward pre-Great Recession levels even if job creation slows in 2017.

In the six years from early 2010 (when the U.S. economy began regularly creating jobs again after the end of the Great Recession) to mid-2016, the economy created a total of just under 15 million jobs, or an average of just under 200,000 per month. Since the middle of 2016, job creation has slowed to 175,000 per month and is likely to slow further over the course of 2017. A few Fed officials are on record saying monthly job growth as low as 80,000 per month would be sufficient to push the unemployment rate lower, but the center of gravity of the Fed probably sees that number closer to 100,000 – 125,000. As we look ahead to 2017, we continue to expect a slowdown in job creation as the recovery matures, but in our view it would take a slowdown to around 25,000 – 50,000 jobs per month to signal that a recession is imminent. The market, on the other hand, may see a fairly typical later-cycle slowdown in jobs to the 100,000 to 125,000 per month range as a recession signal.

INFLATION BUBBLES UP, BUT DOESN’T BOIL OVER

In the aftermath of the Great Recession, inflation expectations have swung between concerns over hyper-inflation in the years following the launch of quantitative easing (QE) in 2009 to concerns about deflation in late 2015, as the impact of sharply lower oil prices and plenty of spare global capacity exacerbated already slow GDP growth. In general, slow economic growth, spare capacity (available labor and production resources), and the globalization of product and labor markets have all acted as restraints on inflation in recent years, and except for a few brief periods in 2009 and early 2015, the Consumer Price Index (CPI) has exhibited neither hyperinflation (as feared in response to central bank “money printing”) nor protracted deflation. Instead, the CPI experienced stagnant or declining (but still positive) growth, also known as disinflation, for much of this recovery. Fears of deflation by late 2015 had led to ramped-up efforts by central banks outside the U.S. to expand QE and a year-long delay in the Fed raising rates a second time.

By the second half of 2016, in the U.S. at least, the factors pushing inflation higher may have begun to win the battle over disinflationary forces, marking an important transition for the economy [Figure 2]. For most of 2015 and 2016, as headline CPI was held down by falling oil prices, inflation in the service sector (which accounts for 80% of GDP and two-thirds of the CPI) accelerated to a new cycle high of 3.0%. Goods prices (one-third of the CPI), which have been in a deflationary environment for most of the past three years, remained in negative territory for the majority of 2016, but as oil prices stabilized near $45/barrel in late 2016, goods deflation began to give way to year-over-year price increases. If oil and gasoline prices stay in their recent ranges, the CPI for commodities will turn positive in early 2017 and push overall CPI above the Fed’s 2% target.

Despite a slow rate of growth, the economic expansion that’s been in place since the end of the Great Recession has been very durable. While there are increased risks from a possible policy mistake, the potential positive economic impact of tax reform and a looser regulatory environment is likely to help the expansion continue, or even accelerate, in 2017.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide or be construed as providing specific investment advice or recommendations for your clients. All performance referenced is historical and is no guarantee of future results.

Any economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal and potential illiquidity of the investment in a falling market.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments, and exports less imports that occur within a defined territory.

© LPL Financial

Read more commentaries by LPL Financial