“What the New Year brings to you will depend a great deal on what you bring to the New Year.”

- Vern McLellan

The most outrageous predictions of 2017

Saxo Bank of Denmark (a bank I hold no grudges against, so don’t assume I am on a mission here) have in recent years been high on entertainment value when publishing their now (in)famous list of Outrageous Predictions for the year to come, some of which are highly controversial. The 2017 list, which you can find here, contains the usual mix of more plausible predictions combined with some truly outrageous ones. Amongst their 2017 predictions, I find the following particularly thought-provoking:

- The high yield default rate exceeds 25%.

- Brexit never happens as the UK Bremains.

- Italian banks are the best performing equity asset.

I am not into making outrageous predictions myself but, if I were, and given the fact that I have a rather wicked sense of humour, my outrageous prediction # 1 for 2017 would probably be for either David Cameron or Hilary Clinton to participate in the 2017 edition of BBC’s flagship entertainment show Strictly Come Dancing. As Ed Balls just learned, that particular show provides an excellent platform to resurrect a fading political career (he probably got more votes for his dancing skills than he did in the last parliamentary elections, but that is an altogether different story). Having said that, only last month did I promise not to make fun of politicians anymore, so let’s drop the ball right there.

Even if 2017 is not likely to be particularly high on entertainment value, it could certainly be high on drama, which makes this Absolute Return Letter particularly challenging. As you may recall from previous years, the January letter is always about the mine field laid out in front of us. What could cause 2017 to be a year to remember? What could possibly go horribly wrong? At this point in time, I see many potential problems. I have some concerns about the US. I see dark clouds gathering over Europe, and I see very slippery conditions in many emerging markets (‘EM’). In other words, lots of markets around the world appear to be accident prone but for very different reasons, which I shall get back to in a moment.

A flicker of good news

However, before I go there, let me share with you a glimmer of hope; a twinkle of optimism that you don’t find too often in the Absolute Return Letter. Not that I am a born pessimist – actually far from it. I just learned many moons ago that, when it comes to investing, good news is the last thing you should spend your energy and resources on. The secret to being a good investor is to focus on risk management and to be well prepared for bad news.

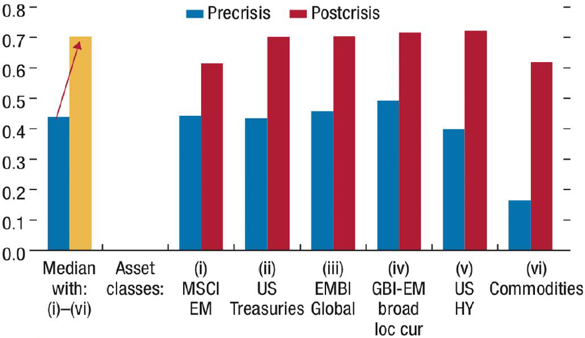

Long term readers of the Absolute Return Letter will know that I have always been of the opinion that we have never properly exited the global financial crisis (the ‘GFC’) of 2007-08. One of the conditions I have used to make my point is the high correlation between risk assets, and how life as an investment manager has become complicated as a result of that.

Prior to the GFC, you could fairly safely assume that diversification across a number of risk assets would dramatically reduce the overall volatility risk, but not anymore. The GFC changed how risk assets correlate with each other (chart 1), and when the correlation between risk assets approaches one, diversification does little to reduce the overall volatility risk.

Chart 1: Correlation among major asset classes pre- & post-GFC

Source: Business Insider, IMF, April 2015

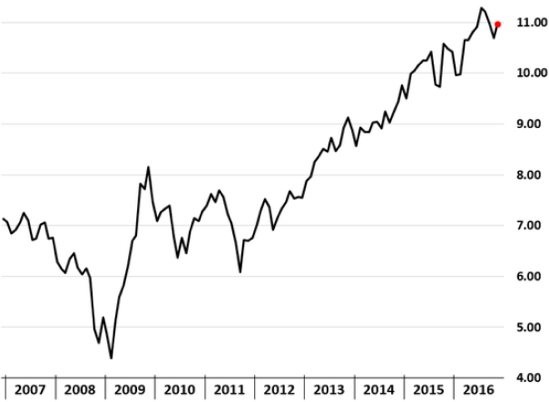

Now the good news - it looks as if the correlation between risk assets – or at least between different types of equity risk – is finally coming down (chart 2). As you can see, the correlation between the S&P 500 and the average equity sector has fallen quite dramatically over the last six months. This is not the only dynamic that needs to change for me to become more optimistic, but it is an important one. Expect me to dig deeper on this topic at some point in 2017.

Chart 2: Average correlation of weekly returns between S&P 500 and S&P sectors

Source: The Daily Shot, BNP Paribas, December 2016

Growing nationalism

As we enter 2017, what should we worry most about? One factor appears to be standing out head and shoulders above everything else, and that is what is usually classified as growing nationalism. It forced the UK out of the EU, and it got Trump elected in the US, but I am not even convinced that the true driver is just growing nationalism.

As you may recall, national income is ultimately shared between capital and labour, and I think capital has belittled labour for too long by taking an ever larger share of national income. Frustrated by the stagnation in living standards, the man on the street wants something to change. The decision to vote for Brexit (or Trump) was a plea for change, as much as it was a sign of growing nationalism. When your own living standards are under pressure, the last thing you want is an army of immigrants to come in and put you under even more pressure.

Stagnating economic growth and low – or even negative – real wage growth has created a deep level of dissatisfaction that the electorate chose to use politically, and the Brexiters (and Trump) took advantage in spades.

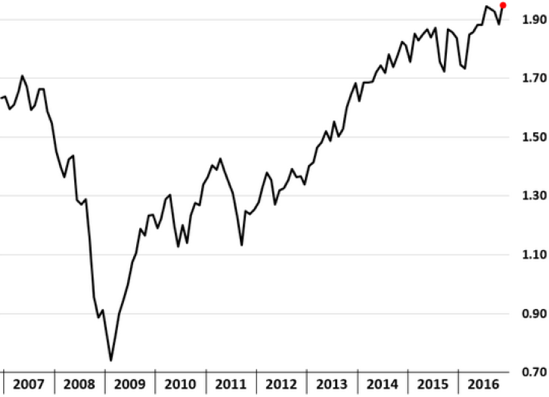

For the first time in 150 years, the average Brit is now facing falling real wages (chart 3). That the low or negative growth in wages is driven by entirely different factors and have nothing whatsoever to do with Brussels is being conveniently ignored.

Chart 3: UK real wage growth

Source: Bloomberg, Bank of England, The Daily Shot, December 2016

Note: The chart shows 10-year moving average of real wages based on weekly pay and the CPI. Data from 2016 onwards is based on BoE projections.

Meanwhile, the political leadership in the UK is facing a very tricky year, with the real opposition to the ruling Conservative Party coming not from the Labour Party but from inside its own ranks. The Brexiters want Theresa May to act now, even if all logic would suggest that the country may be better off counting to 10 before any moves are made.

As 2017 progresses, we face important elections in the Netherlands, Germany and France. The Dutch will kick it all off on the 15th March with the extreme right-wing leader of the Freedom Party, Geert Wilders, currently in pole position. On the 23rd April, the French will be asked to choose their next president. If no outright winner is found in the first round, a run-off between the top two will be held on the 7th May. German general elections will follow in the autumn. The date hasn’t been set yet, but German law prescribes the 2017 elections to take place in either September or October.

Radical forces in all three countries are on the roll and, given what happened in the UK and the US last year, and what happened in Berlin just before Christmas, nothing should be taken for granted.

As far as nationalism is concerned, we are also about to learn whether Trump walks like he talks, and we are saddled with a certain Mr. Putin in Russia, who clearly knows how to take advantage of rising nationalistic sentiment. All in all, 2017 could shape up to be a most interesting year.

The (over)valuation of US equities

That said, growing nationalism and the implications of negative real wage growth are by no means the only things we should worry about as we enter 2017. In the US, equities are very expensive irrespective of how they are valued (charts 4 a-b). Investors have ignored fundamentals in recent years and instead focused on the liquidity provided by the Fed through QE and other means of monetary policy.

Chart 4a: S&P 500 price/EBITDA (trailing)

Chart 4b: S&P 500 price/sales (trailing)

Source: Bloomberg, The Daily Shot, December 2016

This has created equity valuations in the US that almost certainly will come back and bite investors in the derriere at some point. The only question is whether it is going to happen this year or …?

Take chart 4a (price/EBITDA). When acquisitions are made, most companies are acquired at valuations well below 10x EBITDA. If the average company in the S&P 500 now trades at 11x EBITDA, interesting M&A deals are likely to be few and far between. Companies on the acquisition trail simply cannot justify to pay 12x, 13x or even 14x EBITDA for their acquisition target, removing an important pillar for higher equity prices.

Chart 4a also confirms a point I have made in previous Absolute Return Letters, i.e. that US equities are very expensive on a cash earnings (EBITDA) basis. Many US companies ‘mislead’ investors by reporting solid EPS numbers (by buying back their own shares), but chart 4a tells a very different story.

Europe’s colourful menu of challenges

Let’s return to Europe for a minute or two, as there is an entire menu of potential problems to choose from. The constitutional crisis in the EU could worsen dramatically if either the Netherlands, France or Germany were to choose the ‘wrong’ leader later this year. Putin, who is clearly on a roll at present, could quite possibly upset the cards even further – in particular if the new leadership is relatively inexperienced.

In Italy, the banking crisis is an accident waiting to happen. Most Italian banks are seriously undercapitalised and will need many billions of euros of new equity capital (see the story here). However, under European law, equity investors must take the first hit before the government steps in, but how that will all unfold in Italy, only time can tell.

Given the size of the Italian economy compared to the Greek one, you shouldn’t be overly surprised if the Italian banking crisis were to create bigger problems for the Eurozone than Greece ever did. My alter ego (the more sinister side) would even assign a meaningful probability to the entire euro currency system collapsing, with the member countries forced to re-introduce their original currencies. This would require for the Italian banking crisis to escalate further, and for either the Netherlands, France or Germany to exit the Eurozone. It is certainly not my core scenario, but it is not as far-fetched as some investors believe it is.

Brexit could also cause considerable damage to the European economy in 2017. Cocky British newspaper editors have left people with the impression that Brexit means nothing; it was all a storm in a teacup, they say[1], conveniently ignoring the fact that the ramifications of Brexit are yet to be felt. A hard Brexit will certainly be bad for the British economy, but little will change until people begin to lose their jobs.

That said, a hard Brexit is likely to be even worse for the rest of the EU than it will be for the UK (as the EU is a net exporter of goods and services to the UK). I am not entirely convinced, though, that the full impact will be felt in 2017. These negotiations could take a long time – certainly longer than the couple of years that appears to be the consensus.

Rising leverage across emerging markets

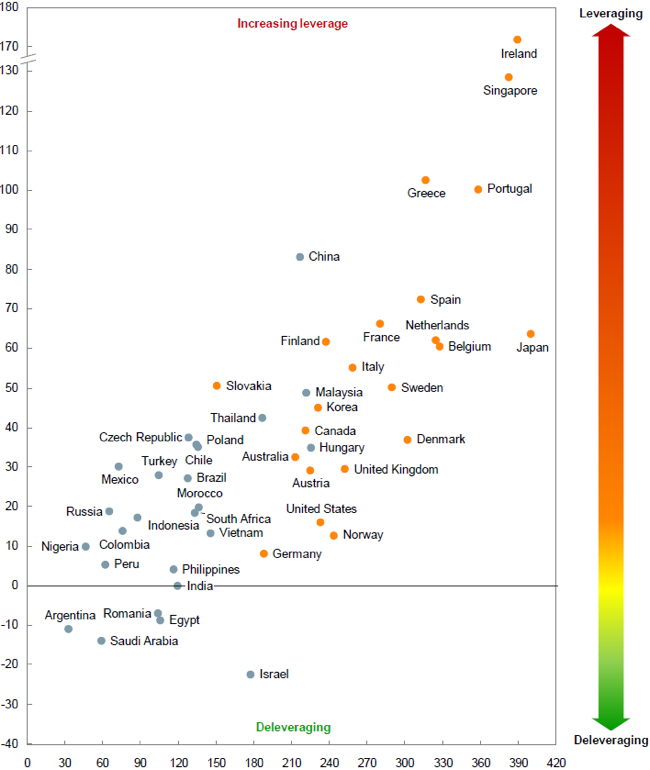

My next worry is the rising indebtedness across emerging markets combined with weak EM currencies. Overall debt levels, in developed market (‘DM’) countries as well as in EM countries, are much higher today than they were when the GFC nearly took us all down in 2007-08 (chart 5). Although I am also worried about debt levels in DM countries, I think the risks associated with excessive debt are higher in EM countries than they are in DM countries, and that has to do with the implications of FX movements.

EM non-financial corporates have continued to accumulate debt as if there is no tomorrow (chart 6). As DM interest rates continued to fall, those corporates increasingly switched to borrowing in US dollars. Given the recent strength of the US dollar - in particular when measured against EM currencies - that decision has been a spectacular own goal. What appeared to be very cheap borrowing costs turned out to be anything but. USD 890 billion of EM bonds and syndicated loans (an all-time high) are coming due in 2017 with almost 30% of that denominated in US dollars[2].

Chart 5: Change in debt-to-GDP, 2007-14

Source: McKinsey & Co, February 2015. Debt-to-GDP 2Q14, %

Chart 6: Indebtedness in emerging markets by sector (% of GDP)

Source: Institute of International Finance, March 2016.

Weakening EM currencies vs. USD has been akin to a significant rise in interest rates for EM borrowers, and the possibility of a high profile accident or two should not be disregarded. I am not close enough to the EM corporate sector to tell you exactly how bad it is, but I am told it is pretty bad out there.

The high price of low interest rates

I have written extensively already about the consequences of very low interest rates for insurance companies, pension funds, local authorities, and therefore ultimately governments and shall not repeat myself. Suffice to say that, should rates stay this low, it is only a question of time before somebody noteworthy blows up right in front of us.

So far, all these very exposed entities have been able to extend and pretend, but it won’t last. As long-term readers of the Absolute Return Letter will know, I expect interest rates to stay low for a very long time to come – particularly in Europe. It is possible that US interest rates will go through a cyclical upswing over the next year or two, but the longer term (structural) trend is still down – unless our political leaders take drastic action (see what could be done in the December Absolute Return Letter here).

Consequently, somebody will almost certainly default. It is only a question of who and when. Obviously there are the explicit defaults, and there are the implicit ones. Increasing the retirement age meaningfully, and implementing a mandatory conversion from defined benefit plans to defined contribution plans with a built-in haircut would translate into an implicit default, but before the unions bark too loudly, they’d better realise what the alternative is.

Local authorities in the US are at the very front of the bankruptcy queue. Take the state of Illinois with over $200 billion of pension liabilities, much of which is unfunded. I am not saying that the state of Illinois will go bankrupt. If I went through the books of every single US state, I am sure I could find a few that are in an even worse condition. That said, the 1% rise in municipal bond yields since July (chart 7) could turn out to be not the buying opportunity that many argue it is, but still a great shorting opportunity despite the recent rise in yields, should the situation be as bad as I suspect it is.

Chart 7: S&P Illinois municipal bond index yield

Source: The Daily Shot, December 2016

Other possible hiccups

I think I will stop here. I could list quite a few other candidates for hiccup of the year 2017, but those that I have mentioned above are the ones I believe are most likely to do meaningful damage in the year to come, should they unfold.

I haven’t mentioned the fact that the current economic cycle is getting very long in the tooth. The last recession ended in early 2009 and the next one will undoubtedly commence not too long from now. Could it possibly happen in 2017? I don’t know, and I don’t think anybody else does either, despite the fact that about ½ million commentators claim they do.

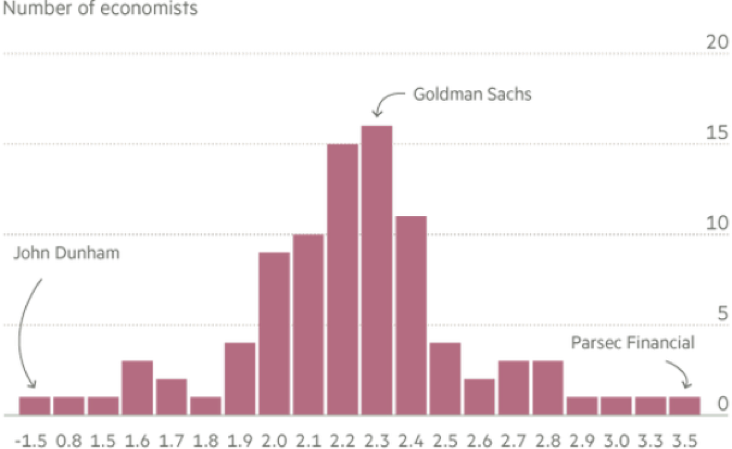

GDP growth projections for 2017 follow an almost perfect normal distribution, suggesting to me that few economists have a very clear idea what sort of conditions 2017 is likely to bring (chart 8). If I were a betting man I would bet against a recession in 2017, though, as almost everyone does in chart 8. There seems to be a great deal of momentum in both the US and the EU economy at present, and I see nothing to change that in the short term.

Chart 8: Economist projections for 2017 US GDP growth

Source: The Daily Shot, Financial Times, Bloomberg, January 2017

However, the Fed could quite possibly ignite the next recession, should it be necessary to tighten more in 2017 than they have already indicated. Based solely on US domestic data, they should probably have tightened a great deal more than they actually did in 2016, but weak data elsewhere kept them sitting on their hands – most likely because they didn’t want the US dollar to appreciate too much. That could potentially force them to tighten more than they would like in 2017. An increasingly capacity-constrained US economy could lead to rising inflationary pressures, but that is more likely to be an issue for 2018 than for 2017, I suspect.

Neither have I mentioned China at all, but China could certainly blow up. After all, the credit bubble appears to be bigger in China than anywhere else. How that will all pan out I don’t know, but I have learned over the years that normal rules do not apply in China. Despite what the rulers want us all to believe, it is most definitely not a proper market economy; hence applying normal logic doesn’t work as far as China is concerned. Investing in China is about knowing the right people and little else. In our part of the world you would most likely go to jail if you applied that investment technique, but not in China – at least not so far.

Summing it all up

The combination of Brexit and Trump has generated significant momentum for nationalistic forces worldwide, and one would be foolish to conclude that the worst is over. I certainly expect at least one of the forthcoming elections in Europe to deliver an outcome that will create further problems for project EU, but don’t assume that I am bearish on the euro for that reason.

Yes, low economic growth across the EU will almost certainly lead to further USD appreciation vs. EUR, but a complete collapse of the euro currency system - or at least a reconfiguration (the latter of which I think is the more likely outcome) - will not necessarily cause the euro to weaken. It will all depend on how the crisis is handled.

The timing of the forthcoming weakening of US equities (which I consider a given) will to a substantial degree depend on when the US economy goes into reverse and, as I said earlier, that is more likely to materialise in 2018, but it could certainly happen as early as 2017.

Some sort of emerging market crisis driven by a combination of high USD-denominated debt and weak EM currencies is my prime candidate for hiccup of the year, but it is not entirely clear what the implications will be for developed markets – sort of depends on where it happens and to what degree DM banks are implicated. Generally speaking, though, DM banks are only modestly involved in emerging markets these days; hence an EM crisis doesn’t necessarily imply that we all get sucked in.

What to do in practice

You would be forgiven for thinking that, from an investment point-of-view, the not insignificant risks laid out in front of us makes it virtually impossible to construct a portfolio that is likely to generate an attractive return in 2017, but nothing could be further from the truth.

Firstly, remember what I said earlier. I usually focus on the negative aspects when investing; hence my writing also has a negative bias. That is not the same as saying that I am always bearish, and I am most definitely not particularly bearish going into 2017.

Secondly, given the risk factors mentioned above, I would emphasise alpha risk over beta risk at this (late) point in the economic cycle. There are indeed many ways that can be accomplished, and that is precisely what next month’s Absolute Return Letter will be about. This month’s letter is already too long, so all I will do for now is to wish you a very successful 2017.

Niels C. Jensen

3 January 2017

© Absolute Return Partners LLP 2017. Registered in England No. OC303480. Authorised and Regulated by the Financial Conduct Authority. Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ, UK.

Important Notice

This material has been prepared by Absolute Return Partners LLP (ARP). ARP is authorised and regulated by the Financial Conduct Authority in the United Kingdom. It is provided for information purposes, is intended for your use only and does not constitute an invitation or offer to subscribe for or purchase any of the products or services mentioned. The information provided is not intended to provide a sufficient basis on which to make an investment decision. Information and opinions presented in this material have been obtained or derived from sources believed by ARP to be reliable, but ARP makes no representation as to their accuracy or completeness. ARP accepts no liability for any loss arising from the use of this material. The results referred to in this document are not a guide to the future performance of ARP. The value of investments can go down as well as up and the implementation of the approach described does not guarantee positive performance. Any reference to potential asset allocation and potential returns do not represent and should not be interpreted as projections.

1 What Brexit jitters? See this story.

2 Source: Institute of International Finance