With the US stock market roaring ahead to close 2016 on a high note, the question for many investors is whether the momentum can be sustained. Here, Franklin Equity Group’s Grant Bowers and Matt Moberg share their view of US economic fundamentals and potential market opportunities given many uncertainties in the year ahead. They see the health care sector—which saw some turbulence in 2016—as an area holding long-term potential for growth-oriented investors.

We believe US economic fundamentals remain strong. Factors such as improved employment metrics, wage growth, productivity and housing starts continue to support a slow-but-durable expansion in the United States, in our view. Additionally, with the uncertainty of the US election now behind us, we are looking ahead to the potential implications of a new administration in concert with corporate and consumer fundamentals. Based on President-elect Donald Trump’s public commentary, the path toward corporate tax reform in the United States—which has the highest corporate tax burden in the developed world—seems clearer, especially alongside a Republican-controlled Congress. Tax reform could potentially be a major positive for the earnings prospects of equities generally and for our growth-oriented strategies. On the other hand, Trump’s trade agenda could alter the path to growth for multi-national corporations. Our role as active managers is to discern how these issues may present risks or opportunities in the marketplace.

Positioning Beyond US Election Results

We feel comfortable for now with our current positioning and do not expect to make major thematic changes to our growth strategies as a result of Donald Trump’s election victory. We seek to benefit from multi-year secular growth themes beyond near-term election results or even the tenure of a single US president. Information technology and health care will likely continue to be areas of focus for us in both 2017 and beyond. Innovation and a changing landscape are creating compelling opportunities for investment, in our view. For instance, the entire consumer landscape is evolving, with hyper-connected customers using smart devices to engage with businesses on an ongoing and personalized basis. On-demand taxi-hailing, online robo-advisors and Internet shopping are disrupting the transportation, financial advice and retail industries, respectively.

With e-commerce, a growing tide of consumer information requires artificial intelligence technology to make sense of the data. These secular shifts are stoking demand for payments infrastructure and cloud computing, which have been amplifying opportunities even for legacy industries, such as software within the information technology sector. We believe consumer-oriented companies that want to stay relevant will need to make software investments in order to make their customer experiences more seamless. In this regard, we see tech spending and investment as being much less discretionary than one might think, giving tech a resiliency factor not typically associated with the sector. We are also tracking the trajectory of the semiconductor industry and a possible positive inflection point: Self-driving cars may require a threefold increase in chip content per vehicle.

Health Care: Short-Term Uncertainties, Long-Term Opportunities

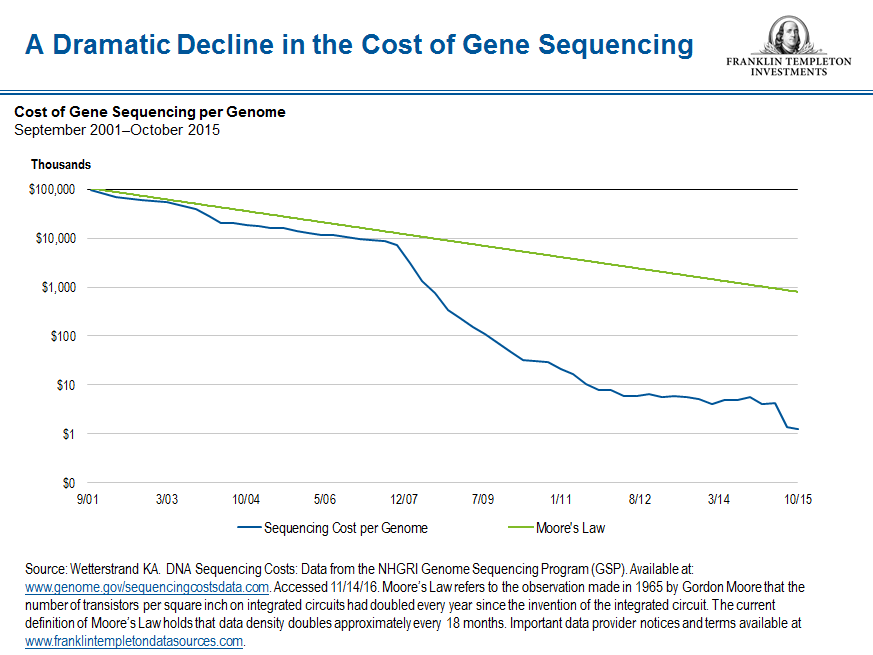

Within health care, it remains to be seen whether the Republican Party’s call for a repeal of the Affordable Care Act will gain traction, which may reduce public access to health care services and, in turn, have potentially negative implications for some health care providers and medical device manufacturers. On the other hand, many drug companies have been under pressure in recent months due to market concerns that a Clinton administration would enact legislation to rationalize drug pricing, which would negatively affect pharmaceutical and biotechnology companies. Trump’s victory may improve the outlook for top-line growth in that arena. Our investment process is to assess each opportunity and its long-term growth prospects on a case-by-case basis. Regardless, we believe there may be greater potential for growth for pharmaceutical and biotech companies with narrow competencies, such as gene-sequencing, hepatitis C cures and so-called orphan drugs, the latter of which target niche populations.

We believe the health care industry overall may benefit from myriad factors. An aging population globally and a swelling middle class in emerging markets could both drive increased consumption of routine health care services and demand for ever-more sophisticated treatments and cures. This demographic tailwind is fueling innovation in drug development and medical technology, and thus improving the prospects at select companies for robust sales and earnings. Future earnings power may be further boosted by innovation and technology-driven reductions in research expenses: For example, the cost of gene sequencing, which enables preventative screening and personalized medical treatment, has fallen faster than reasonably imagined just a few years ago.