Summary

• Individual commodities trade on their own fundamentals.

• Near-term pressure on gold and silver to give way as inflation rises faster than interest rates.

• Oil to continue range bound trading in first half until visible signs of production cut-backs emerge.

• Short-term correction in industrial metals to precede gains, while La Niña to place pressure on agricultural prices

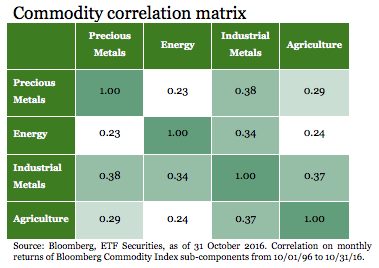

Commodities to trade on own fundamentals

While many group commodities as one asset class, in reality each commodity trades on its own fundamentals. Historic correlation between commodities has been relatively low. In this outlook we will provide an overview of our views on major commodities within each sub-category.

Gold and silver: near term pressure, medium term strength

We believe the US Federal Reserve (Fed) is still on track to raise rates in December 2016. Although there was a degree of political uncertainty in the run-up to the Presidential election, Trump’s progrowth policies are likely to be inflationary. In the short-term, gold and silver prices are likely to come under pressure as we approach the rate hike. However, we believe that the Fed will remain behind the curve and inflation will rise faster than the central bank will raise rates, keeping real rates very low. According to the Fed’s latest ‘dot-plot’ of its committee member’s assessment of appropriate policy settings, the Fed is only likely to raise rates twice in 2017. Low real rates are gold price positive. We believe that gold’s fair value is between the $1400-1450/ounce range.

Silver has a close correlation with gold and hence we expect silver prices to rise. In contrast to gold, which trades like a currency, the physical supply and demand for silver also drives the silver price. Factoring in the decline in mining investment and rising industrial activity, we estimate silver’s fair value in the $22-24/ounce range.

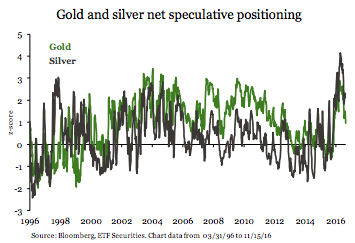

Speculative positioning in gold and silver has retreated from highs reached in July, but they remain elevated as investors seek a hedge against geopolitical risk. The Italian constitutional referendum, the French Presidential election and the German parliamentary elections are some of the items on the calendar for the coming year. When and if the United Kingdom (UK) will start the process of leaving the European Union (EU) has still not been resolved. Rising populism poses a threat to stability and investors will look to hedge this risk.

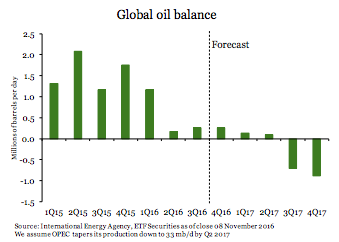

Oil market still on path to balance

We believe that oil will continue to trade in the $40-55/bbl (barrel) range until visible signs of a production cut-back emerge. The market is coming closer toward a supply-demand balance, but the path will be bumpy. Close to $1 trillion of investment cuts in the oil and gas industry since the start of the oil price crash that began in November 2014 will start to bite into supply in 2017.

OPEC (Organization of Petroleum Exporting Countries) has also agreed to cut production back to 32.5-33 million barrels (mb) per day of production, down from 33.4mb of production in September 2016. However, OPEC’s commitment is contingent on the participation of non-OPEC countries. Preliminary meetings between OPEC and several non-OPEC members have not shown any progress toward yielding a positive result. Large non-OPEC members such as Russia, Brazil and Kazakhstan are seeing new production come online as a result of investment put in many years ago. There are also a large number of OPEC countries looking for exemptions from participating in production cuts, placing the burden on countries like Saudi Arabia and other Gulf Cooperation Council members.

Notwithstanding these difficulties, should OPEC manage to agree on how to apportion the cut at its November 30th meeting and stick to the quota thereafter, we could see the market come to balance as early as Q1 2017. But we believe that it will take until Q2 2017 for OPEC to taper production down to 33mb and the market will balance in Q3 2017.

The US will continue to be price responsive. With short-term breakeven prices for shale oil at around $40/bbl we expect to see expansion in US production, which will limit upside on prices to $55/bbl in the first half of the year. President Elect Trump’s pledge to pursue energy independence could see US oil production rise. However, it is a 6-year goal and the necessary policy changes to increase production this year may not emerge.

When we see sustained cuts to production in the second half of 2017 and production deficits eat into elevated inventories, oil prices are likely to trade above $55/bbl.

Industrial metal correction before next rally

Industrial metals have had a strong rally in 2016 as supply deficits have become more widely recognized. Even copper, which had a lackluster first half of the year, has been rising sharply in recent weeks. Since not a lot has changed for the metals from a fundamental perspective, we fear that part of the gains reflects a speculative frenzy originating from China that could correct in the short-term. Ahead of the 19th National Congress of the Communist Party of China to be held in Autumn 2017, Chinese authorities will seek political stability. That could mean that the reform agenda could take a back-seat and over-production of several metals could persist in China.

Growing populism elsewhere is likely to increase spending on infrastructure which will boost demand for industrial commodities. For example, President Elect Trump has pledged up to a $1 trillion infrastructure spend (financed through a combination of tax credits and private sector borrowing). We believe that this will drive industrial metal prices higher after the short-term correction that we mentioned above takes place.

Other political risks may also impact industrial metal prices. The Philippine’s recent threat of banning ore exports is one of them. However, President Duterte’s relationship with the US is likely to improve under a Trump administration and its new political alignment with China will likely keep ore exports flowing, at least to its largest consumers.

La Niña to provide better agricultural growing conditions

A La Niña weather pattern is expected to emerge which will provide cooler temperatures during the Southern Hemisphere summer and reduce heat damage for Arabica coffee, corn and soybean. Current rains have produced a good flowering of coffee bushes in Brazil, setting up for a good crop this year.

Better snow cover in North America during La Niña could also benefit winter wheat growing. Normal levels of rain in India has refilled resevoirs (following the failed monsoon the previous year). Such beneficial conditions will help reduce the sugar production deficit. The EU’s scrapping of the sugar prodution quota in October 2017 will increase the supply of sugar beet in Europe and reduce the demand for raw cane sugar, which will also weigh on prices.

Important Information

The statements and opinions expressed are those of the author and are as of the date of this report. All information is historical and not indicative of future results and subject to change. Reader should not assume that an investment in any securities and/or precious metals mentioned was or would be profitable in the future. This information is not a recommendation to buy or sell. Past performance does not guarantee future results.

The ETFS Silver Trust, ETFS Gold Trust, ETFS Platinum Trust, ETFS Palladium Trust and Precious Metals Basket Trust are not investment companies registered under the Investment Company Act of 1940 or a commodity pool for purposes of the Commodity Exchange Act. Shares of the Trusts are not subject to the same regulatory requirements as mutual funds. These investments are not suitable for all investors. Trusts focusing on a single commodity generally experience greater volatility.

Commodities generally are volatile and are not suitable for all investors. Trusts focusing on a single commodity generally experience greater volatility. Please refer to the prospectus for complete information regarding all risks associated with the Trusts. Shares in the Trusts are not FDIC insured and may lose value and have no bank guarantee.

The value of the Shares relates directly to the value of the precious metal held by the Trust and fluctuations in the price could materially adversely affect investment in the Shares. Several factors may affect the price of precious metals, including:

• A change in economic conditions, such as a recession, can adversely affect the price of the precious metal held by the Trust. Some metals are used in a wide range of industrial applications, and an economic downturn could have a negative impact on its demand and, consequently, its price and the price of the Shares;

• Investors’ expectations with respect to the rate of inflation;

• Currency exchange rates;

• Interest rates;

• Investment and trading activities of hedge funds and commodity funds; and

• Global or regional political, economic or financial events and situations. Should there be an increase in the level of hedge activity of the precious metal held by the trust or producing companies, it could cause a decline in world precious metal prices, adversely affecting the price of the Shares. Should there be an increase in the level of hedge activity of the precious metal held by the Trusts or producing companies, it could cause a decline in world precious metal prices, adversely affecting the price of the shares.

Also, should the speculative community take a negative view towards the precious metal held by the Trusts, it could cause a decline in prices, negatively impacting the price of the shares. There is a risk that part or all of the Trusts’ physical precious metal could be lost, damaged or stolen. Failure by the Custodian or Sub-Custodian to exercise due care in the safekeeping of the precious metal held by the Trusts could result in a loss to the Trusts.

The Trusts will not insure its precious metals and shareholders cannot be assured that the custodian will maintain adequate insurance or any insurance with respect to the precious metals held by the custodian on behalf of the Trust. Consequently, a loss may be suffered with respect to the Trust’s precious metal that is not covered by insurance.

Commodities generally are volatile and are not suitable for all investors.

Please refer to the prospectus for complete information regarding all risks associated with the Trust.

Investors buy and sell shares on a secondary market (i.e., not directly from Trusts). Only market makers or “authorized participants” may trade directly with the Trusts, typically in blocks of 50k to 100k shares.

Definitions: The Federal Reserve (Fed) is the central banking system of the United States of America. The European Union (EU) is a politico-economic union of 28 member states that are located primarily in Europe. The Organization of Petroleum Exporting Countries (OPEC) is a group consisting of 12 of the world's major oil-exporting nations. La Nina is the cooling of the water in the equatorial Pacific that occurs at irregular intervals and is associated with widespread changes in weather patterns. Correlation is a mutual relationship or connection between two or more variables. A z-score (aka, a standard score) indicates how many standard deviations an element is from the mean.

Commodities generally are volatile and are not suitable for all investors. This material must be accompanied or preceded by the prospectus. Carefully consider each Trust’s investment objectives, risk factors, and fees and expenses before investing. Please click here to view the prospectus.

ALPS Distributors, Inc. is the marketing agent for ETFS Silver Trust, ETFS Gold Trust, ETFS Platinum Trust, ETFS Palladium Trust and ETFS Precious Metals Basket Trust.

Maxwell Gold is a registered representative of ALPS Distributors, Inc.

ETF001069 12/31/17

© ETF Securities

Read more commentaries by ETF Securities