Risk is one of my all-time favorite board games. It’s among the very few that’s equal parts strategy and luck, and the stakes can’t get much higher than total world domination. It wasn’t uncommon for games between my friends and me to last for hours, sometimes deep into the night.

Today a real-life game of Risk is unfolding on the world stage, with major players moving their pieces into place.

As you probably recall, President-elect Donald Trump recently took a call from Taiwanese President Tsai Ing-wen, a decision that flies in the face of 40 years’ worth of U.S.-China diplomacy. Since 1978, the U.S. has had no diplomatic relations with Taiwan after acknowledging the “One China” policy—a policy Trump says the U.S. is not necessarily bound to.

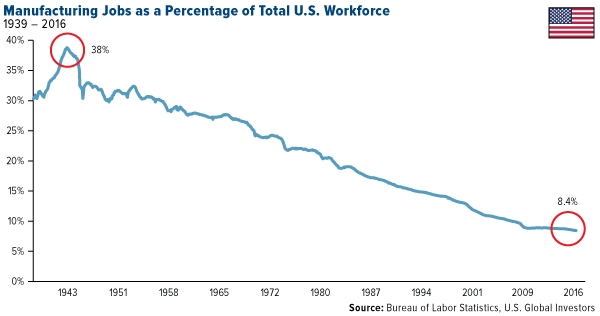

His phone call and comment follow tough talk on the campaign trail about China manipulating its currency and stealing American manufacturing jobs—though bringing them back might be hard, as we’ve steadily been losing such jobs since the Second World War.

Trump has also threatened to impose an unrealistically high 45 percent tariff on Chinese imports, prompting U.S. companies operating in the Asian country to fear “retribution.”

For their part, the Chinese say they have “serious concerns” about Trump’s position on Taiwan and international trade, with one state-run newspaper describing the president-elect as “ignorant as a child” in the field of diplomacy.

China’s “retribution” could be coming sooner than we expect. This week, a top Chinese official visited Mexico to strengthen ties with the Latin American country, which has also frequently found itself caught in Trump’s crosshairs. Both countries—our number two and number three trading partners, after Canada—have expressed interest in lessening their dependency on the U.S., especially given the strong possibility that Trump could raise certain trade restrictions.

In the fight for American jobs, we could be “risking” a trade war with China right on our southern doorstep. Though the stakes might not be as high as total global domination, they come pretty close. With rates moving up and the world resetting to less quantitative easing, inflation might accelerate. To avoid a global recession, Trump will need to make streamlining regulations a top priority.

Gold Sidelined as Trump Rally Continues and Yields Surge

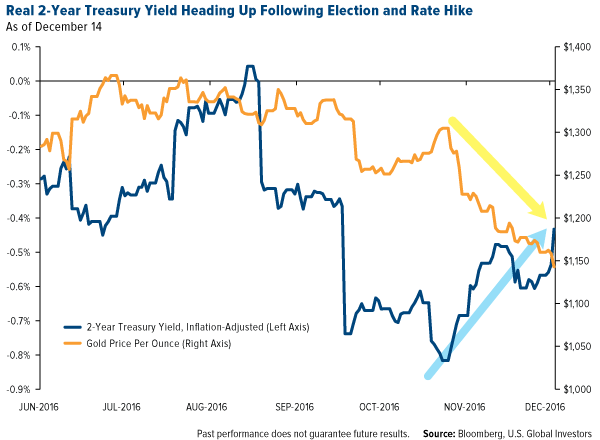

For only the second time since 2008, the Federal Reserve raised interest rates this week, surprising no one. Although the 25 basis point lift was in line with expectations, markets took some time to digest the news that three rate hikes—not two, as was earlier expected—were likely to happen in 2017. Major averages hit the pause button for the first time since last month’s presidential election, but the Trump rally quickly resumed Thursday morning.

The two-year Treasury yield immediately jumped to a nominal 1.27 percent after averaging 0.80 percent for most of 2016, an increase of 58 percent. In real, or inflation-adjusted, terms, the yield is still in negative territory, but it’s clearly heading up following the U.S. election and rate hike. Thirty-year mortgage rates, meanwhile, hit a two-year high.

Gold retreated to a 10-month low. As I’ve explained many times before, gold has historically had an inverse relationship with bond yields, performing best when they’re moving south.

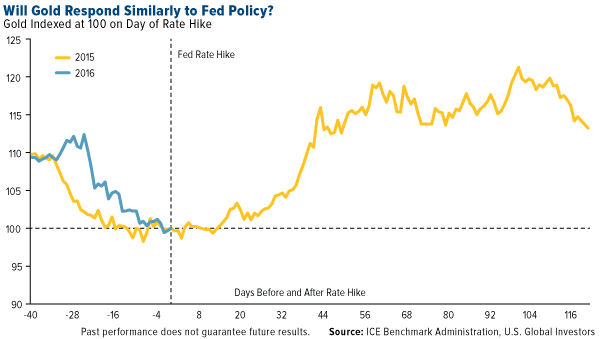

It’s worth pointing out that the most recent gold bull market, which carried the yellow metal up 28 percent in the first six months of 2016, was triggered last December when the Fed hiked rates.

Again, as many as three rate hikes are expected in 2017—unlike the one this year—with Fed Chair Janet Yellen commenting that economic conditions have improved well enough to warrant a more aggressive policy. If true, this should accelerate upward momentum of Treasury yields and the U.S. dollar—currently at a 14-year high—which could dampen gold’s chances of repeating the rally we saw in the first half of this year.

|

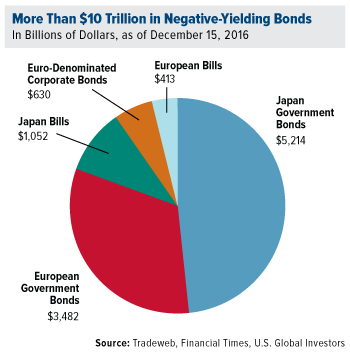

Other gold drivers still remain in place, though, including negative-yielding government bonds elsewhere around the world. The value of such debt has dropped considerably since the election of Donald Trump, but it still stands at more than $10 trillion, supporting the investment case for the yellow metal. And as I mentioned last week, many of Trump’s protectionist policies—opposition to free trade agreements, imposition of tariffs on Chinese-made goods—are expected to heat up inflationary pressures in the U.S., which could serve as a gold catalyst.

What’s more, gold is looking oversold, down two standard deviations for the 60-day period, which has historically signaled a good buying opportunity. With prices off close to 12 percent since Election Day, I believe this is an attractive time to rebalance your gold position. I’ve always recommended a 10 percent weighting, with 5 percent in gold stocks and the other 5 percent in bullion, coins and jewelry.

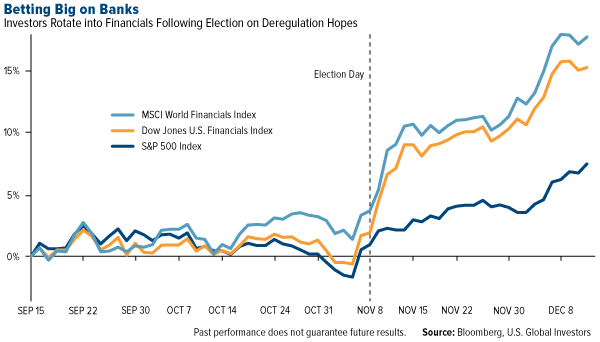

Will Trump Tear Up Dodd-Frank? The Market Is Betting on It

The top beneficiary of the Trump rally so far has been the banking industry, with bets driven by the potential for higher lending rates and stronger economic growth in the coming months, not to mention the president-elect’s pledge to reject any new financial regulations.

I wouldn’t call this rally “irrational exuberance” just yet, but according to Bank of America Merrill Lynch’s monthly survey, fund managers have built up the largest overweight position ever in bank stocks—31 percent above their benchmarks on average.

This phenomenal run-up implies investors have confidence Trump can make good on his promise to unleash the U.S. economy and dismantle Wall Street regulations.

As I’ve made clear in previous commentaries, regulations are usually created with the best of intentions, and they’re sometimes necessary to establish a level playing field. But all too often, they end up impeding financial growth, hurting not just businesses but also consumers.

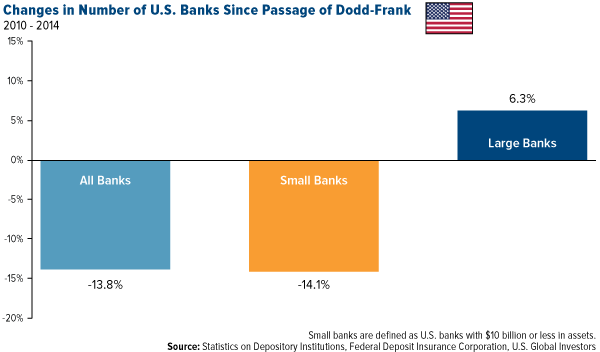

Take Dodd-Frank. What was intended as a set of policies to prevent another financial meltdown has dramatically limited consumer choice, shrunk the number of retirement options and squeezed out smaller banks and credit unions. The 2,300-page act, signed in 2010, places a monumental burden on financial institutions, from banks to brokers to investment firms, which we have felt indirectly. Even former Fed Chair Ben Bernanke had a hard time refinancing his house in 2014, one of Dodd-Frank’s unintended consequences.

Before 2010, about 75 percent of banks offered free checking accounts. Only two years later, that figure had fallen to less than 40 percent. Since the law went into effect, the U.S. has lost one community financial institution a day on average. This hurts credit-seeking small businesses and startups, not to mention consumers in the market to buy a new home or vehicle.

In House Speaker Paul Ryan’s “A Better Way” initiative, several solutions to runaway regulations are proposed. One that stands out is a “regulatory budget,” which would limit the number and dollar amount of rules federal agencies can impose every year. My hope is that Ryan and Trump can set aside their differences to streamline the ever-growing mountain of rules that weighs on American businesses and restricts the flow of capital.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 0.44 percent. The S&P 500 Stock Index fell 0.06 percent, while the Nasdaq Composite fell 0.13 percent. The Russell 2000 small capitalization index lost 1.71 percent this week.

- The Hang Seng Composite lost 3.12 percent this week; while Taiwan was down 0.70 percent and the KOSPI rose 0.87 percent.

- The 10-year Treasury bond yield gained 13 basis points to 2.60 percent.

Domestic Equity Market

Strengths

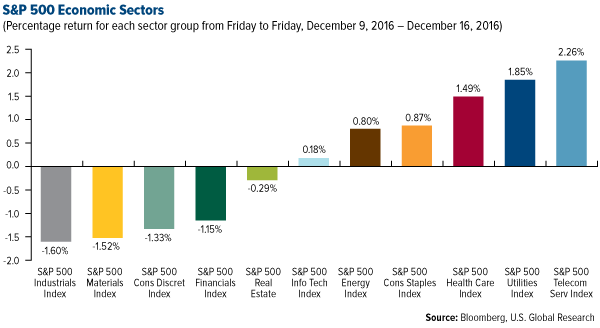

- Telecommunications was the best-performing sector for the week, increasing by 2.26 percent vs an overall decrease of -0.14 percent for the S&P 500.

- Nvidia was the best-performing stock for the week, increasing 9.36 percent.

- Oil companies surged after news of an agreement between OPEC and non-OPEC producers for a production cut. The oil producers jumped between 2 percent and 5 percent after news that the oil cartel and outside countries had agreed on a deal.

Weaknesses

- Industrials was the worst-performing sector for the week, decreasing by 1.60 percent vs an overall decrease of 0.14 percent for the S&P 500.

- Nordstrom was the worst-performing stock for the week, falling 16.91 percent.

- Yahoo revealed another huge hack. In what may be the biggest hack ever, the company says more than 1 billion accounts may have had phone numbers, birth dates, and security questions stolen by hackers during an attack that took place in August 2013.

Opportunities

- Priceline has a new CEO. Glenn Fogel, a 16-year veteran of the firm and current head of strategy and executive vice president of corporate development, has been named CEO.

- SeaWorld is opening a park in Abu Dhabi without whales. This will be the first park without the signature orca attraction. SeaWorld has been slowly moving away from the whales since the release of the documentary “Blackfish.”

- Sony is rated investment grade at Moody's again. Bloomberg reports that Moody's Japan KK raised its rating on the electronics maker Sony by one notch to Baa3, making it investment grade nearly three years after losing the status. Moody's cites the “expectation of further improvement in operating profit, setting aside one-off factors,” as a reason for the upgrade.

Threats

- Jeff Gundlach thinks a stock market sell-off is coming. During Tuesday's webcast titled “Drain the Swamp,” DoubleLine Funds founder Jeff Gundlach said stocks typically rise following an election and then sell off as investors realize the new president can't implement everything he has promised.

- Bonds are flashing a warning sign for stocks. The U.S. 10-year yield ticked above 2.60 percent on Thursday, the level at which Societe Generale's Cross Asset Allocation team says stocks become “rich” to bonds.

- Gilead must pay Merck $2.5 billion in royalties. A federal jury has awarded Merck a $2.54 billion reward in a patent verdict against Gilead related to its hepatitis C drugs Sovaldi and Harvoni, Reuters reports.

The Economy and Bond Market

Strengths

- The Federal Reserve hiked its key interest rate by 25 basis points to a range of 0.50 percent to 0.75 percent at Wednesday's meeting and upgraded its forecast to three rate hikes in 2017 versus its prior forecast of two based on the view of a stronger economy.

- CPI inflation came in right in line with expectations. The reading of inflation registered a 0.2 percent gain for the month of November and a 1.7 percent gain from the same month last year. Economists had expected those exact numbers. The core index — which strips out volatile energy and food prices — came in at 0.2 percent growth from the last month and 2.1 percent year-over-year, as economists expected a reading of 0.2 percent month-over-month and 2.2 percent expected.

- Empire manufacturing surged. The New York Federal Reserve's Empire State manufacturing index jumped to 9.0 for the month of December, higher than the 4.0 expected from economists.

Weaknesses

- Bond markets everywhere are getting crushed. Post-Fed selling has run the U.S. 10-year yield up about 20 basis points to 2.62 percent, its highest level since June 2014. Selling in Europe is having the biggest impact on the U.K. 10-year, which traded up 14 basis points to 1.52 percent.

- Gold and silver got smashed in the aftermath of the Fed’s Wednesday decision to raise rates. “Although almost every market participant expected a rate hike, gold has taken a significant hit since yesterday’s move by the Fed,” said RBC Capital Markets commodity strategists in a note on Thursday.

- U.S. mortgage applications remain on a downtrend, dropping another 4 percent last week. The tightening in financial conditions via the rise in bond yields is adversely impacting the housing market.

Opportunities

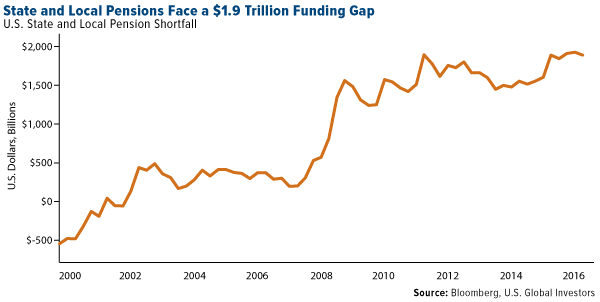

- PIMCO’s municipal bond chief said the company has invested almost all of its municipal portfolio in state and local debt backed by dedicated revenues, arguing they provide higher payouts and better security from pension risk than general-obligation debt. He anticipates investors will demand higher spreads on general-obligation bonds in the coming years as struggling pensions become a bigger driver of credit ratings.

- Next week, an upturn in the leading economic indicator (LEI) would confirm an outlook for better growth in 2017.

- High-profile investors are backing a $1 billion green-energy fund. Bill Gates, Jeff Bezos, and other high-profile investors’ new venture called “Breakthrough Energy Ventures” will invest in “anything that leads to cheap, clean, reliable energy we're open-minded to,” Gates said.

Threats

- The dollar is on fire. The U.S. dollar index is at an almost 14-year high. The index strengthened in the aftermath of the Fed’s decision to raise rates for the second time this decade. A strong dollar makes American exports uncompetitive.

- In the latest U.S. National Federation of Independent Business (NFIB) report, small-business owners reported that they are less optimistic about capital expenditures. Just 24 percent of those surveyed plan to spend on capex in the next 3 to 6 months.

- Given the soft November retail sales report this week, the personal spending/income data next Thursday could further cement concerns that household consumption growth is slowing.

Gold Market

This week spot gold closed at $1,134.84, down $25.17 per ounce, or 2.17 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 8.02 percent. Junior tiered stocks outperformed seniors for the week, as the S&P/TSX Venture Index fell 1.81 percent. The U.S. Trade-Weighted Dollar Index continued higher this week with a gain of 1.34 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

Dec-12 |

China Retail Sales |

10.2% |

10.8% |

10.0% |

|

Dec-13 |

Germany CPI YoY |

0.8% |

0.8% |

0.8% |

|

Dec-13 |

Germany ZEW Survey Current Situation |

59.0 |

63.5 |

58.8 |

|

Dec-13 |

Germany ZEW Survey Expectations |

14.0 |

13.8 |

13.8 |

|

Dec-14 |

U.S. PPI Final Demand YoY |

0.9% |

1.3% |

0.8% |

|

Dec-14 |

FOMC Rate Decision |

0.75% |

0.75% |

0.50% |

|

Dec-15 |

U.S. CPI YoY |

1.7% |

1.7% |

1.6% |

|

Dec-15 |

U.S. Initial Jobless Claims |

256k |

254k |

258k |

|

Dec-16 |

Eurozone CPI Core YoY |

0.8% |

0.8% |

0.8% |

|

Dec-16 |

U.S. Housing Starts |

1230k |

1090k |

1340k |

|

Dec-22 |

U.S. GDP Annualized QoQ |

3.3% |

-- |

3.2% |

|

Dec-22 |

U.S. Durable Goods Orders |

-4.5% |

-- |

4.6% |

|

Dec-22 |

U.S. Initial Jobless Claims |

260k |

-- |

254k |

|

Dec-23 |

U.S. New Home Sales |

575k |

-- |

563k |

Strengths

- The best-performing precious metal this week was platinum, up 1.20 percent for the week after surging 3.48 percent on Friday when the December 16 issue of Science published research on a new fuel cell design using an atomically ordered platinum and lead core surrounded by a thick uniform shell of four platinum layers. The new design can undergo 50,000 voltage cycles with a negligible decay in performance and no apparent changes in their structure or elemental composition which has been a weakness in previous fuel cell designs.

- China’s gold withdrawals surged in November, according to the monthly report from the Shanghai Gold Exchange. The increase of 214.72 tonnes was a 40 percent rise over the October figure. This level of demand puts China on track to potentially maintain its position as the world’s largest gold consumer. Kitco also reports that China may be unofficially restricting gold imports. Rumors and reports indicate that international banks are having difficulties with their imports, as the People’s Bank of China is taking longer to approve each importing transactions. The central bank may be trying to unofficially restrict gold imports to curb high capital outflows from China’s investors.

- Bloomberg reports that gold imports by India climbed 10 percent in November, to the highest this year. After pressure on gold demand due to higher prices, an excise tax and anti-corruption measures, overseas purchases rose to 111 metric tons , compared to 101 tons a year earlier. Zerohedge also reports the rush to buy gold in the midst of the disruption has consumers paying as much as a 50 percent premium above official India prices. India’s top gold importer, Axis Bank, has reportedly suspended the bank accounts of some bullion dealers and jewelers after some executives were arrested over money laundering.

Weaknesses

- The worst performing precious metal this week was palladium, down 4.73 percent. Palladium, which is up 23.75 percent this year, seemed to trade more in line with the sentiment towards gold and silver but did not see the Friday bounce the other metals experienced.

- Gold mining company Gold Reserve, Inc. is still owed $300 million for its first installment from Venezuela for the seizure of a mining project. The payment was due on November 30, pushed back from the original date of October 31, but the country requested an extension to December 15. Now that deadline has passed also.

- The Mexican Environmental Authority has denied the environmental impact assessment of Argonaut Gold Inc.’s planned San Antonio project in Baja California Sur, Mexico. The company believes it can provide the needed information to the Mexican agency quickly.

Opportunities

- Macquarie Research has published a positive report on GFG Resources, a new precious metals explorer that holds a 100 percent district-scale interest in the Rattlesnake Hills gold project in Wyoming. Macquarie reports that senior mining companies previously validated their interest prior to the district being consolidated. This project targets an alkaline gold deposit, which is a relatively rare type of deposit, but alkaline-related rocks have historically been associated with giant scale gold deposits.

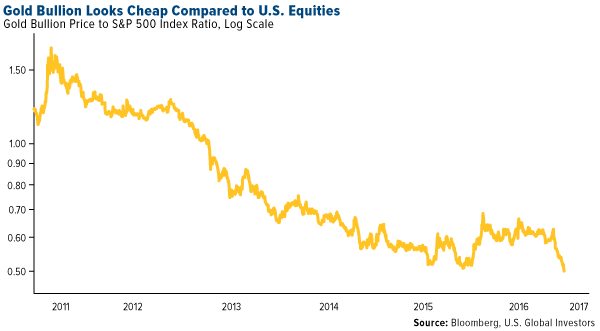

- As the Federal Reserve plans to raise rates three times in 2017, this hinders the recovery in gold, as pointed out in a note from Canaccord Genuity, which sees marginal downside risk to gold and gold equities. The price ratio between gold prices and the S&P 500 has fallen to last Decembe’rs low. “In other words, as an asset class, the bullion has become very cheap relative to U.S. equities,” analyst Martin Roberge notes.

- Bank Credit Analyst (BCA) points out that realistically, it will take time for the incoming Trump administration to draft legislation that deploys fiscal stimulus – at least six months. It will then take time to see if it works. Given this reality, BCA’s team notes that the U.S. dollar and real rates “have moved too far too fast, and likely will correct.” Where BCA differs from consensus is that the rising inflation expectations they measure in the forward markets are probably warranted for 2017. If growth materializes with stimulus, overlaid on a labor market that is close to full employment, the low inflation consensus could shift higher. This could depress real rates and provide a more attractive outlook for gold in 2017.

Threats

- Troy Gayeski, senior portfolio manager at SkyBridge Capital, reflected this sentiment, saying, “The Trump victory has delivered the sum of all fears to gold investors due to the combination of anticipated pro-growth tax reform, a rollback of the hyper-regulation of the Obama administration, and the potential for fiscal stimulus.” He also noted that additional Fed tightening, increase in interest rates and the strong dollar have hampered gold’s appeal. UBS points out that sentiment toward gold is quite negative currently, but there are no signs of panic in the market as selling had been orederly.

- Recent gold selling implies fresh shorting and liquidation, notes HSBC Global Research. The firm notes that selling, while likely to slow, may not yet be exhausted, and gold is nearing the $1,100/ounce support level.

- The Federal Reserve’s announcement that they may raise rates three times in 2017 has put pressure on gold. However, David Doyle of Macquarie Research states that the research firm believes a two-rate hike year is more likely. Doyle points out that some of the more hawkish voting members of the Federal Open Market Committee (FOMC) will change next year and likely will be replaced by doves. Doyle noted six of the FOMC participants favor just one or two hikes in 2017 and Yellen and Dudley are likely in this group.

December 14, 2016These Factors Show Why Buffett Likes Airlines Again |

December 12, 2016Inflationary Expectations in 2017 Keep the Polish on Gold |

December 8, 2016Time to Take Trump Seriously on Infrastructure Spending? |

Energy and Natural Resources Market

Strengths

- Coking coal contract prices settled at $285 per ton, $100 dollars higher than initial estimates. The strength in coking coal prices will translate into upgraded earnings estimates for producers like BHP Billiton and South32, a positive read-through for coal producers.

- The best performing sector for the week was the Bloomberg Global Integrated Oils index. The index rose 2.5 percent as a result of investor positioning following OPEC’s November end agreement.

- Rosneft PJSC, the world’s largest publically traded petroleum company, was the best performing stock this week, finishing up 12.3 percent. The stock rallied on the back of a 2.3 percent gain in Brent oil prices.

Weaknesses

- Lumber was the worst performing commodity this week, falling 2.5 percent. The drop was driven by the expiration of the last softwood lumber agreement in the U.S. and uncertainty related to tariffs among trading partners going forward.

- The worst performing sector this week was the NYSE Arca Gold Miners Index. The index fell 8 percent on the back of falling gold prices as result of the Federal Reserve’s announcement to hike rates, and guiding for as many as three rate hikes in 2017.

- The worst performing stock for the week was Newcrest Mining Limited, the largest Australian producer of gold and silver. The company fell 13.3 percent on the back of falling precious metal prices.

Opportunities

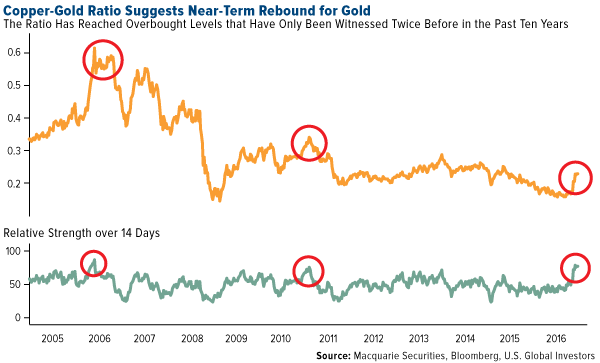

- Gold prices may rebound in the New Year as the U.S. dollar has rallied “too far too fast,” according to BCA Research. After a tumultuous week following the Federal Reserve’s interest rate hike, the copper-to-gold ratio has reached levels that have only been witnessed twice in the past ten years; gold has outperformed in both instances. Additionally, gold is entering a bullish seasonality pattern for the months of January and February, where the price has rallied 7 out of 10 times.

- Zinc’s rally has a strong probability of continuing through 2017. The base metal rallied more than 70 percent this year alone, grounded on strong demand for high quality vehicles from India and China, which are heavy users of rustproof galvanized steel. The rally’s momentum has been supported by the closure of several mines globally, constricting supply and helping the metal flourish.

- Oil producers are forecast to make double digit returns on exploration for the first time since 2012. The downturn in oil prices has helped lower costs and create an environment ripe for gains in risky but promising areas like exploration. With oil prices near 52-week highs, this prompts extra attention towards the exploration and production universe in 2017.

Threats

- The iron and steel rally may be at risk as China property starts slow sharply according to a developer’s sentiment survey by UBS. The slowdown is a result of policies implemented earlier this year to tighten lending and cool a property bubble. Housing accounts for 37 percent of China’s steel consumption, creating negative ramifications for the price of steel.

- The copper rally may fizzle as London copper inventories rose sharply this week to a total inventory of 241,550 tons. Macquarie Bank believes this could be the first of a number of inflows to come, due to a lack of tightness in the physical market. If inventory does continue to build, expect the prices of copper to reverse to the downside.

- OPEC now believes the oil market will not balance until the second half of 2017, as opposed to its earlier expectation that the market could balance in the first half. Despite agreeing to production cuts, the organization has stated in its latest monthly release that the market will remain in surplus by approximately 100,000 barrels per day—a negative read-through for crude oil in the short term.

China Region

Strengths

- Fullshare Holdings rose more than 30 percent for the week as the stock and its acquisition target—China High Speed Transmission Co., up 23 percent for the week—continue to fluctuate amid very little news.

- Year-over-year retail sales in China beat expectations, coming in for the November period at 10.8 percent, ahead of expectations for a gain of only 10.2 percent.

- Retail sales in Singapore also beat, rising 2.2 percent in the most recent period, well ahead of expectations for a gain of 0.3 percent.

Weaknesses

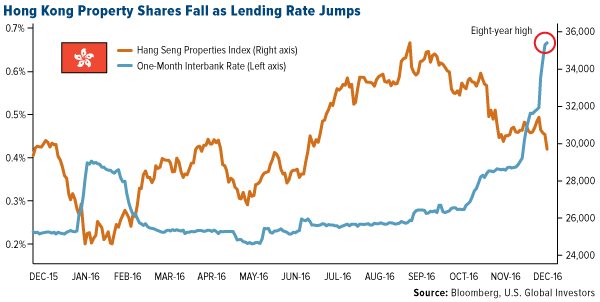

- With rising mortgage costs (measured by HIBOR, or Hong Kong Interbank Overnight Rate) and recently-raised taxes, property shares took a bit of a beating in Hong Kong this week.

- Overseas Workers Remittances to the Philippines missed for October, the most recent period, dropping 3 percent year-over-year versus an anticipated gain of some 10.8 percent.

- Landing International Development, a holding company for businesses heavily tied to property development and operation, fell some 36 percent this week in Hong Kong as the company reported that it is actively exploring raising equity.

Opportunities

- Reuters reports that China may be targeting as much as $290 billion of investments in tourism by 2020 as it seeks to draw in more private investors to capitalize on the fast-growing demographic trend of middle class travel services.

- China issued a red-level pollution alert—the highest level on its pollution scale—highlighting the ongoing smog and air quality issues in the country. But even though this is a problem and threat, such a problem means there are opportunities surrounding treatments and solutions to said problem: Chinese interest in alternatives continues to grow.

- The Bank of Indonesia reports, according to Bloomberg News, that a 4.94 percent year-over-year growth rate for the fourth quarter may well be achievable, ahead of growth assumptions of only 4.8 percent.

Threats

- Several media sources suggest a tit-for-tat interpretation of Chinese actions this week including announcing an investigation into a Chinese auto company linked to U.S. manufacturer GM; the announcement of a strategic deepening of relations with the U.S.’s southern neighbor, Mexico; and later in the week, a headline-grabbing seizure of a U.S. unmanned underwater drone. Are such actions indeed or necessarily indicative of Chinese retribution for Trump’s Taiwan call? Do they represent manifestations of risks to longstanding U.S. “One China” protocol and broader political and economic stability?

- Credit in China continues to grow (Aggregate CNY Financing in November came in up 1.74 trillion, well ahead of expectations for 1.1 trillion), which, while a positive for growth scenarios, does raise concerns about deleveraging in the country and the extent to which steps like housing curbs are achieving intended effects.

- The yuan climbed once again to new highs, soaring above 6.96 this week after the U.S. Federal Reserve announcement. Capital outflow concerns remain a threat.

Emerging Europe

Strengths

- Hungary was the best-performing country this week, gaining 4.2 percent. Mol, the Hungarian integrated oil and gas company, led the gains on the Budapest stock exchange, rising to nearly a five-year high, and gaining 7 percent in the past five days. The company is in talks to acquire OT Industries, a Budapest-based company specializing in engineering for the energy industry.

- The Russian ruble was the best-performing currency this week, gaining 64 basis points against the dollar. The central bank of Russia left the main rate unchanged at 10 percent, as most economists predicted. A rate easing cycle may resume in the first half of the next year.

- The financial sector was the best-performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst-performing country this week, losing 10 basis points. The European Stability Mechanism (ESM) announced that it will put the short-term debt relief decision for Greece on hold after the Greek government announced, without prior consultation with its creditors, that it will give EUR600 million to low income pensioners and postpone the tax increase for the Northeast Aegean island most severely hit by the refugee crisis. Greece is obligated to notify euro area officials of such changes to its spending plans, but it failed to do so in this case.

- The Romanian leu was the worst-performing currency this week, losing 1.4 percent against the dollar. The Social Democrats (PSD) won the parliamentary election and will be forming its government. A government led my Social Democrats was previously in power from 2012 to 2015, led by Prime Minister Victor Ponta, who resigned at the end of 2015 due to mass protests related to corruption allegations.

- The material sector was the worst-performing sector among eastern European markets this week.

Opportunities

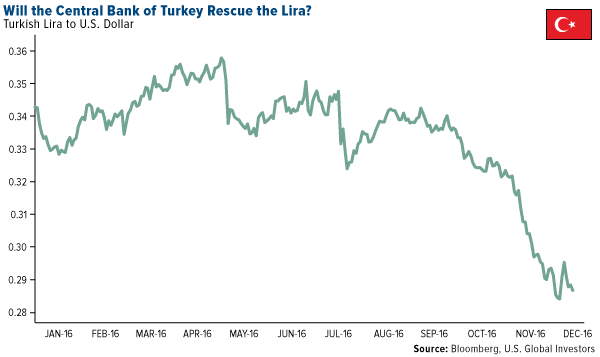

- The central bank of Turkey will meet next week and may decide to hike rates in order to support the lira currency. Berenberg’s research team believes that the rate should increase by at least 250 basis points to hold the falling currency, to lower inflation and to make Turkey investible again. A move by the central bank to raise rates will not be in line with President Recep Erdogan’s recent call to lower the rates in order to boost the country’s growth. The rate decision for Turkey will be announced on December 20.

- Russia overtook China in Bank of America Merrill Lynch’s top emerging markets rankings for the first time since the rankings began in 2009. The rankings are based on financial stability scores for everything from growth and inflation to fiscal vulnerability. Russia’s growth is poor, but current account, fiscal and leverage indicators remain strong. South Korea is ranked first, Russia second and China third.

- Hungary will introduce the European Union’s (EU) lowest corporate tax rate in 2017. Currently companies are taxed at two different rates: 10 percent on profits up to 500 million forints ($1.74 million) and 19 percent above that level. Economists said the measure will mainly benefit midsized Hungarian and foreign-owned companies with more than EUR 2 million in revenue.

Threats

- Emerging market stocks and currencies declined after the U.S. Federal Reserve hiked rates by 25 basis points and forecast a steeper path for borrowing costs in 2017, reducing the appeal of riskier assets.

- EU leaders agreed to rollover economic penalties for six months imposed on Russia over Ukraine, but the EU did not expand sanctions against the Kremlin in response to Russia’s bombing of civilians in Syria. It is clear that the EU is divided over Russia, with some leaders wanting to extend the sanctions and others supporting their removal.

- Turkey’s economy contracted for the first time in seven years during the third quarter. Gross domestic product (GDP) in July through September shrunk by 1.8 percent annually, sinking deeper into negative territory than the 0.4 percent drop forecasted by economists. The economic downturn was driven by a collapse in private domestic consumption, which declined by an annualized 3.2 percent in the third quarter. Further GDP weakness in the fourth quarter may follow.

© US Global Investors