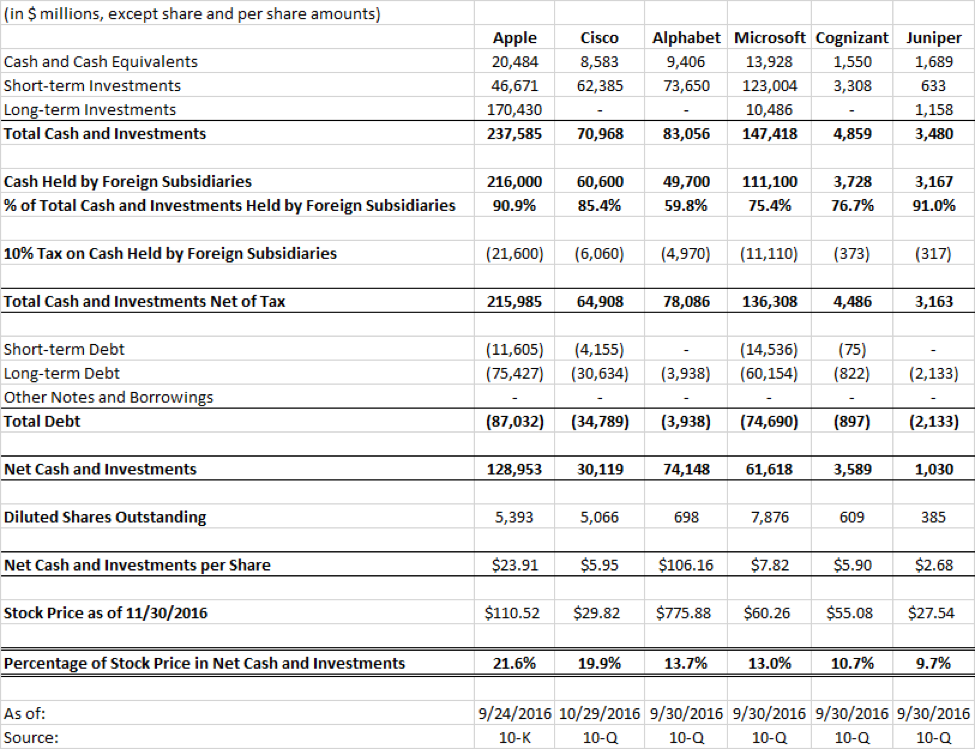

In August 2013, we provided an analysis of excess cash on the balance sheets of four technology holdings: Apple, Inc. (AAPL), Juniper Networks, Inc. (JNPR), Microsoft Corp. (MSFT), and Cisco Systems, Inc. (CSCO)1. Nearly three and a half years later, the balance sheet remains a meaningful source of value at each of the four companies. Additionally, we have initiated investments in Alphabet, Inc. (GOOGL), the parent company of Google, Inc., which has accumulated $83.1 billion of cash and marketable securities, and Cognizant Technology Solutions Corp. (CTSH), a provider of information technology (IT) services, which has accumulated $4.9 billion in cash and short-term investments. While our projections of the future earnings and free cash flow account for the majority of our estimate of the intrinsic value of each business, excess cash may not be fully reflected in current market prices. Revisiting the extent to which cash on the balance sheet represents a source of value at each company may prove timely if President-elect Trump follows through on his plan to lower the rate at which corporations are able to repatriate foreign profits that have not yet been taxed by the United States.

Tax Policy and Repatriation

Under current tax laws, profit recognized outside of the United States is taxed in the foreign jurisdiction immediately, but is not taxed by the U.S. government until the cash is returned to the United States. Because many of the countries in which the profit is recognized have lower corporate tax rates than the U.S., corporations benefit in the short term by paying less income tax. However, when the cash is returned to the U.S., it is taxed at roughly the difference between the 35% U.S. corporate tax rate and the tax rate that was already applied in the country in which the profit was recognized. Reluctant to pay this additional tax, many companies have elected to keep overseas cash in the foreign jurisdictions rather than repatriating the cash to the U.S. and paying the additional tax.

The most recent repatriation holiday, The Homeland Investment Act of 2004, allowed companies to bring profits earned in foreign jurisdictions back to the United States at a 5.25% incremental U.S. tax rate. According to the Internal Revenue Service, 843 companies repatriated a combined $312 billion as a result of that legislation. President-elect Trump’s tax plan2 proposes a one-time 10 percent tax on the repatriation of corporate profits that are currently held outside of the United States. An opportunity to repatriate overseas cash at a favorable repatriation tax rate would likely be viewed positively by many companies in the technology sector, and could result in a significant amount of overseas cash returning to the U.S. Once overseas cash is repatriated, it is reasonable to believe that it could be either invested into the businesses at favorable rates of return, or returned to shareholders via share repurchases or dividends. The table that follows details the extent to which cash, net of debt, represents a source of value at six technology companies that are owned by Diamond Hill. For the purposes of this analysis, a 10 percent tax is applied to cash held by foreign subsidiaries.

Use of Repatriated Cash

While the Homeland Investment Act of 2004 was designed to stimulate domestic investment, employment, and research and development, the repatriated cash may not have increased investment in these areas to the extent that might have been anticipated. A prominent study released by the National Bureau of Economic Research3 found that each dollar of cash that was repatriated was associated with a $0.92 increase in capital returned to shareholders, primarily through share repurchases. This occurred despite the legislation being designed with the intent of preventing the use of repatriated cash for dividends and share repurchases. However, money is fungible, and in practice the availability of additional cash resulted in additional capital being available for dividends and share repurchases. It is possible that future legislation could more effectively prohibit the use of repatriated cash for dividends and share repurchases, but regardless, it would be a positive for companies with large overseas cash balances to have the option to repatriate that cash at a lower tax rate than is typically applicable.