Inflation can be understood as the destruction of a currency’s purchasing power. To combat this, investors, central banks and families have historically stored a portion of their wealth in gold. I call this the Fear Trade.

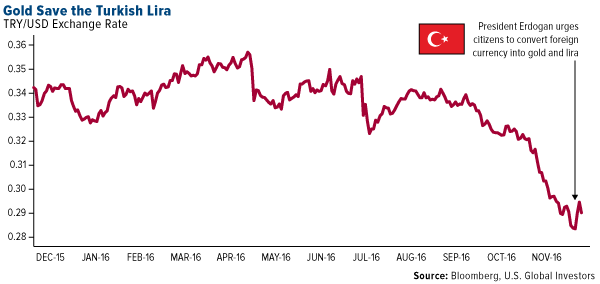

The Fear Trade continues to be a rational strategy. Since President-elect Donald Trump’s surprise win a month ago, the Turkish lira has plunged against the strengthening U.S. dollar, prompting President Recep Erdogan to urge businesses, citizens and institutions to convert all foreign exchange into either the lira or gold. Most obliged out of patriotism, including the Borsa Istanbul, Turkey’s stock exchange, and the move has helped support the currency from falling further.

Venezuela, meanwhile, has dire inflationary problems of its own. Out-of-control socialism has led to an extreme case of “demand-pull inflation,” economists’ term for when demand far outpaces supply. Indeed, the South American country’s food and medicine crisis has only worsened since Hugo Chavez’s autocratic regime and the collapse in oil prices. The bolivar is now so worthless; many shopkeepers don’t even bother counting it, as Bloomberg reports. Instead, they literally weigh bricks of bolivar notes on scales.

“I feel like Pablo Escobar,” one Venezuelan bakery owner joked, referring to the notorious Colombian drug lord, as he surveyed his trash bags brimming with worthless paper money.

Because hyperinflation has destroyed the bolivar, the ailing South American country sold as much as 25 percent of its gold reserves in the first half of 2016 just to make its debt payments. Venezuela’s official holdings now stand at a record low of $7.5 billion.

Trump-Carrier Deal a Case Study in U.S. Inflation

|

The U.S. is not likely to experience out-of-control hyperinflation anytime soon, as the dollar continues to surge on bets that Trump’s proposals of lower taxes, streamlined regulations and infrastructure spending will boost economic growth. But I do believe the market is underestimating inflationary pressures here in the U.S. starting next year.

As I explained to Scarlet Fu and Julie Hyman on Bloomberg TV today, inflation we might soon see is largely caused by rising production costs, which is different from the situation in Turkey and Venezuela.

Nevertheless, it still serves as a positive gold catalyst for 2017.

Consider Trump’s recent Carrier deal—the one that saved, by his own estimate, 1,100 jobs from being shipped to Mexico. We should applaud Trump and Vice President-elect Mike Pence for looking out for American workers, but it’s important to acknowledge the effect such interventionist efforts will have on consumer prices.

|

As I see it, the Carrier deal is indicative of the sort of trade protectionism that could spur inflation to levels unseen in more than 30 years. The Indiana-based air conditioner manufacturer has already announced it will likely need to raise prices as much as 5 percent to offset what it would have saved by moving south of the border.

We can expect the same price inflation for all consumer goods, from iPhones to Nikes, if production is brought back home. That’s just the reality of it. Prices will go up, especially if Trump succeeds at levying a 35 percent tariff on American goods that are built overseas but imported back into the U.S. The extra cost will simply be passed on to consumers.

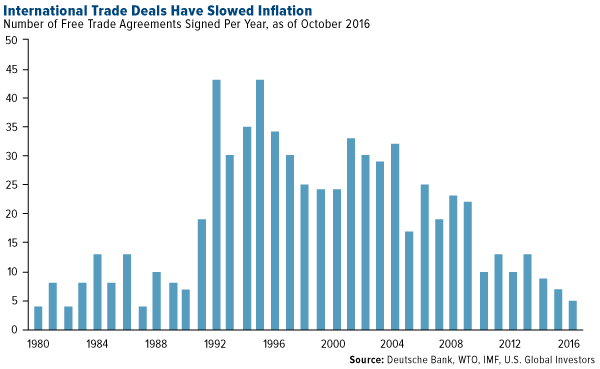

What’s more, Trump has been very critical of free trade agreements, threatening to tear them up after blaming them—NAFTA, specifically—for the loss of American jobs and stagnant wage growth. There’s some truth to this. But trade agreements have also helped restrain inflation over the past three decades. This is what has allowed prices for flat-screen, plasma TVs to come down so dramatically and become affordable for most Americans.

In its 2014 assessment of NAFTA, the Peterson Institute for International Economics (PIIE) calculated that for every job that could be linked to free trade, “the gains to the U.S. economy were about $450,000, owing to enhanced productivity of the workforce, a broader range of goods and services, and lower prices at the checkout counter for households.”

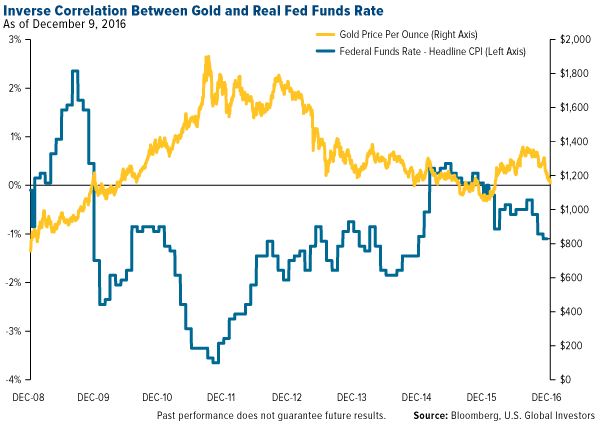

Additional tariffs and the inability to import cheaper goods are inflationary pressures that could result in a deeper negative real rate environment. And as I’ve pointed out many times before, negative real rates have a real positive effect on gold, as the two are inversely correlated.

Macquarie research shows that last year, ahead of the December rate hike, gold retreated about 18 percent from its year-to-date high. Afterward, it gained 26 percent in the first half of 2016. The decline so far this year has been about 15 percent from its year-to-date high. Gold, according to Macquarie, is setting up for another rally in a fashion similar to last year.

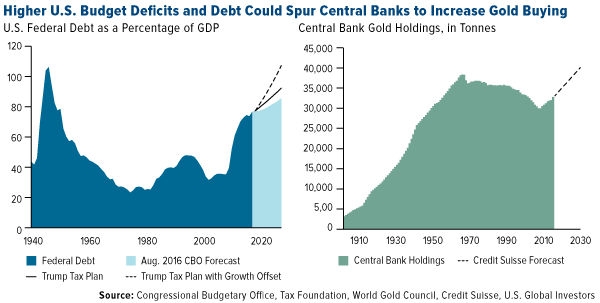

Central Bank Demand Could Accelerate on Growing Federal Debt

The U.S. government is currently saddled with $19.9 trillion in public debt. Since 2008, federal debt growth has exceeded gross domestic product (GDP) growth. And according to a Credit Suisse report this week, Trump’s tax proposal, coupled with deficit spending, could cause federal debt to grow even faster than under current policy.

After analyzing projections from a number of agencies and think tanks, Credit Suisse “estimates a federal debt-to-GDP of 92 percent by 2026, including a GDP growth offset from the lower tax tailwind, and 107 percent excluding the GDP growth offset.”

The U.S. dollar accounts for about 64 percent of central banks’ foreign exchange reserves. With the potential for higher U.S. budget deficits and debt risking dollar strength, central banks around the globe could be motivated to increase their gold holdings, says Credit Suisse.

Waiting for Mean Reversion

As I mentioned last week, gold is looking oversold in the short term and long term, down more than two standard deviations over the last 20 trading days. Statistically, when gold has done this, a return to the mean has often followed. This has been an attractive entry point for investors seeking the sort of diversification benefits gold and gold stocks have offered.

In a note to investors this week, ETF Securities highlighted these diversification benefits, writing that a gold allocation has “historically increased portfolio efficiency—lowering risk while increasing return—compared to a diversified portfolio without an allocation to precious metals.”

As always, I recommend a 10 percent weighting: 5 percent in gold bullion, 5 percent in gold stocks, then rebalance every year.

Learn Why Warren Buffett Changed His Mind

When I visited New York in the spring, the media was negative on airlines because Warren Buffett didn’t like the industry. Now, the Oracle of Omaha has changed his mind about airlines, having invested $1.3 billion in the big four American carriers—but the media’s still down on the group. I’ve been in New York all week, and they say airlines have gone up too much.

I’m afraid they’re missing a great opportunity here. Today, the industry is surrounded by what Buffett calls a “moat,” meaning the barrier to entry is too high and restrictive for new competitors. President-elect Trump’s victory means that industry regulations could be streamlined and the Federal Aviation Administration (FAA) brought into the 21st century. Since the group bottomed in late June, it’s rallied a phenomenal 46 percent.

If you’re getting your market news from the mainstream media, you could be at risk of missing out on this opportunity as well. I urge you to learn the real story about the airline industry by registering today for our webcast event, to take place next Thursday, December 15. I’ll be discussing how airlines have reversed their fortunes from near-bankruptcy to record profitability, and where they might go from here.

I hope you’ll join us!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 3.06 percent. The S&P 500 Stock Index rose 3.08 percent, while the Nasdaq Composite climbed 3.59 percent. The Russell 2000 small capitalization index gained 5.62 percent this week.

- The Hang Seng Composite rose 0.68 percent this week; while Taiwan was up 2.21 percent and the KOSPI rose 2.74 percent.

- The 10-year Treasury bond yield rose 8 basis points to 2.46 percent.

Domestic Equity Market

Strengths

- Financials was the best-performing sector for the week, increasing by 4.82 percent vs an overall increase of 3.08 percent for the S&P 500.

- Under Armour was the best performing stock for the week, increasing 16.31 percent.

- Goldman Sachs is up about 30 percent since the election. Shares of the investment bank hit a post-financial crisis high on Thursday as traders continued to price in the impact of a Trump presidency. Goldman is about 2.5 percent below its record high set in 2007.

Weaknesses

- Health care was the worst-performing sector for the week, increasing by 0.65 percent vs an overall increase of 3.08 percent for the S&P 500.

- Universal Health Services was the worst-performing stock for the week, falling -10.09 percent.

- Restoration Hardware slashed its outlook. The high-end furniture retailer expects full-year adjusted earnings per share of $1.19 to $1.29, down from $1.60 to $1.80 as slow holiday sales weigh. Shares were down as much as 19 percent in after-hours trading.

Opportunities

- Amazon unveiled Amazon Go, a grocery-store concept that will automatically add shoppers’ products to a digital cart so they can walk out without waiting in a checkout line. The first store is set to open in downtown Seattle in 2017.

- Samsung is going to supply semiconductor chips to Tesla. A report from South Korea’s Electronic Times says Samsung will make the chips for the self-driving features in Tesla vehicles.

- Lululemon beat and raised its guidance. The yoga clothing maker earned an adjusted $0.47 per share on revenue of $544.4 million, both ahead of estimates. Lululemon expects to earn $0.96 to $1.01 per share during the fourth quarter on revenue of $765 million to $785 million. Shares of Lululemon were up as much as 12 percent in after-hours trading.

Threats

- Sears is planning to close more stores as the company's sales losses widen. "We expect to end up with a smaller but meaningfully-sized store base," Sears Chief Financial Officer Jason Hollar said. The company reported a fifth-straight quarterly loss.

- Express Scripts, a pharmacy benefits manager, fell 7 percent after short-selling firm Citron Research tweeted that it might be targeted by President-elect Donald Trump. "When @realdonaldtrump tells $ESRX 'you’re fired' heads will roll," founder Andrew Left said, calling it the "culprit behind pharmaceutical price gouging."

- Donald Trump's tweets continue to move markets. The iShares Nasdaq Biotech Index exchange-traded fund fell after the president-elect said in a Time magazine interview that "I’m going to bring down drug prices. I don’t like what’s happened with drug prices."

The Economy and Bond Market

Strengths

- Job openings rose slightly more than expected. There were 5.534 million job openings in the U.S. in October, as shown in the monthly Job Openings and Labor Turnover Survey (JOLTS report) released on Wednesday. Economists had forecast 5.5 million job openings, according to the Bloomberg consensus.

- New orders for U.S. factory goods recorded their biggest increase in nearly one-and-a-half years in October, further evidence that the manufacturing sector is gradually recovering after a prolonged downturn. Factory orders rose 2.7 percent after an upwardly revised 0.6 percent gain in September.

- U.S. service providers in November recorded the fastest pace of new-work growth in a year, according to Markit Economics. The overall purchasing manager's index came in at 54.6 (54.8 forecast.) The Institute of Supply Management's index was 57.2, a 13-month high.

Weaknesses

- Barely half of 30-year-olds earn more than their parents did at a similar age, a research team found, an enormous decline from the early 1970s when the incomes of nearly all offspring outpaced their parents. Even rapid economic growth won’t do much to reverse the trend, according to the report. Economists and sociologists from Stanford, Harvard and the University of California set out to measure the strength of what they define as the American Dream, and found the dream was fading.

- The share of compensation costs paid by state and local governments for defined-benefit plans reached 10 percent, the highest on record, in September 2016, according to a report this week from the Labor Department. That’s up from 9.5 percent in 2015, and 6.3 percent in the same quarter a decade ago. There are two main factors that have gotten state and local governments in trouble. One is declining returns: Pensions’ expected rate of return has fallen from above 8 percent in 2001 to about 7.6 percent in 2015, according to a brief from the Center for Retirement Research. Another is that following the financial crisis, many governments didn’t pay in the full amount required to keep their pensions fully funded.

- Italian voters rejected a referendum on constitutional reform early last week, prompting Prime Minister Matteo Renzi to resign. The result continues the anti-establishment trend in the United States and Europe. Renzi agreed to remain in office until the Italian Senate passes a 2017 budget. Moody's cut Italy's sovereign rating outlook to negative from stable after the vote.

Opportunities

- Municipal bonds are trading at the most attractive levels to benchmark securities in more than a year as President-elect Donald Trump’s pro-growth and anti-tax comments raise uncertainty in fixed-income markets. The current yield on the 10-year municipal benchmark is about 106 percent of Treasuries, up from as little as 90 percent on November 10. Traditionally, anything over 100 percent on the muni-Treasury ratio is a buy signal.

- The Federal Open Market Committee (FOMC) is widely expected to hike rates next Tuesday. Investors will be watching to see if the Fed adjusts its “dot plot” for the expected path of the Fed funds rate.

- Recent U.S. economic data support the view that the economy is picking up steam, even before any fiscal stimulus is enacted by the new Congress. The U.S. economic backdrop should thus remain positive for risk assets heading into 2017, although Fed rate hikes and dollar strength will remain a headwind.

Threats

- BCA’s fixed-income strategists believe that U.S. high-yield bonds are still too overvalued to justify an overweight position.

- There's an unintended consequence of the Trump-Carrier jobs deal. Greg Hayes, the CEO of United Technologies, Carrier's parent company, says the deal that has been hailed as a win for President-elect Trump will lead to automation and fewer jobs.

- Pulling off a renaissance in U.S. manufacturing employment will be extraordinarily tough. After hitting a record of nearly 20 million in 1979, the number of American factory workers has plunged during each of the last five recessions and each time has never recovered. Today, 12.3 million people are employed in U.S. factories, a loss of nearly 8 million jobs. Forecasters in The Wall Street Journal’s monthly survey of economists doubt the numbers of bygone years can be restored. They estimate the U.S. will add about 7,000 manufacturing jobs by the end of 2017, about 40,000 by the end of 2018 and about 50,000 by the end of 2019, according to the average forecast—moving upward in coming years, but at a pace far too slow to replace what has been lost.

Gold Market

This week spot gold closed at $1,159.28, down $17.97 per ounce, or 1.53 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week lower by 2.98 percent. Junior miners outperformed seniors for the week, as the S&P/TSX Venture Index slipped just 0.08 percent. The U.S. Trade-Weighted Dollar Index continued higher this week with a gain of 0.81 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

|

Dec-6 |

U.S. Durable Goods Orders |

3.4% |

4.6% |

4.8% |

|

Dec-8 |

ECB Main Refinancing Rate |

0.000% |

0.000% |

0.000% |

|

Dec-8 |

U.S. Initial Jobless Claims |

255k |

258k |

268k |

|

Dec-12 |

China Retail Sales |

10.2% |

-- |

10.0% |

|

Dec-13 |

Germany CPI YoY |

0.8% |

-- |

0.8% |

|

Dec-13 |

Germany ZEW Survey Current Situation |

59.0 |

-- |

58.8 |

|

Dec-13 |

Germany ZEW Survey Expectations |

14.0 |

-- |

13.8 |

|

Dec-14 |

U.S. PPI Final Demand YoY |

0.9% |

-- |

0.8% |

|

Dec-14 |

FOMC Rate Decision |

0.75% |

-- |

0.50% |

|

Dec-15 |

U.S. CPI YoY |

1.7% |

-- |

1.6% |

|

Dec-15 |

U.S. Initial Jobless Claims |

256k |

-- |

258k |

|

Dec-16 |

Eurozone CPI Core YoY |

0.8% |

-- |

0.8% |

|

Dec-16 |

U.S. Housing Starts |

1230k |

-- |

1323k |

Strengths

- The best performing precious metal this week was silver with a gain 0.76 percent. Electronic chat documents released by Deutsche Bank show that UBS and Deutsche Bank, along with others, regularly conspired trades with one another to trigger stop-loss orders, coining the name “STOP BUSTERS” for themselves, according to court documents. Plaintiffs contend that the records show these banks conspired to fix the spread on silver offered to customers and used illegal strategies to rig prices.

- BullionVault’s Gold Investor Index, which measures the balance of client buyers against sellers, jumped to its highest in five years, reports Bloomberg. The gauge of gold buying rose to 59.3 in November from 56.8 in October, while the silver gauge retreated.

- Gold premiums in China soared to a three-year high following the news of reported gold import curbs in the country along with limited supply of the precious metal, reports ZeroHedge. The import curbs may be part of China’s efforts to limit outflows of the yuan after the currency’s slide to its weakest in more than eight weeks, the article continues. Coin sales from the U.S. Mint have also risen, for a fourth straight month in fact, following the U.S. election. The 2016 American Eagle gold coin in one-ounce, quarter-ounce and tenth-ounce sizes are sold out, reports Dave Harper with The Buzz.

Weaknesses

- The worst performing precious metal this week was palladium, down 1.77 percent. Commerzbank AG believes that palladium, the best-performing precious metal in the second half of 2016, could be heading for a “price correction” early in the year, reports Bloomberg. Commerzbank also noted that gold, having the worst returns over this same period, could benefit from still-low interest rates and “ultra-low” monetary policy in 2017.

- Platinum miners, on the other hand, are contending with a 50-percent drop in prices for the metal since 2011. In addition, Sibanye Gold has agreed to pay more than its market value for Stillwater Mining Co. for $2.2 billion, giving it charge of the world’s highest-grade deposit of PGMs, reports Bloomberg.

- Exchange-traded funds backed by precious metals saw a net outflow of $6.24 billion over the past month, as gold prices tumbled to a 10-month low, reports Bloomberg. Overseas, China reported that its gold reserves remain unchanged in November from a month earlier, at 59.24 million troy ounces. According to Bloomberg, this marks only the second time the country has paused monthly buying after disclosing a 57 percent increase in holdings since 2009, as of June 2015.

Opportunities

- According to a report from Credit Suisse, higher gold prices are needed for supply to meet demand growth. “The total delineated gold reserves at current prices are unlikely to keep pace with demand over the long term,” states the report. Operating mines have only around 1 billion ounces of reserves left, or around 10 years of mine life. In relation to the chart below, the Credit Suisse explains that significantly higher gold prices are likely needed to increase recycled gold supply above recent levels.

- New Shariah-compliant rules approved on November 19 for trading gold, now allow the precious metal to be accepted as an investment in Islamic finance. The Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) developed the standards with the help of the World Gold Council, which has said the new rules could spur demand for “hundreds of tons” of gold, reports Bloomberg. According to Mohd Daud Bakar, a Shariah scholar, the SPDR Gold Trust (the biggest bullion-backed ETF) will probably qualify, and the standard may open new demand to central banks.

- London-based manager of the Old Mutual Gold & Silver Fund says that gold will strengthen as the Fed fails to increase interest rates fast enough to keep up with inflation. Commerzbank is also positive on the metal, forecasting it to climb next year each quarter to an average of $1,300 an ounce in the fourth quarter and extend its gains in 2018 to $1,400 an ounce by the third quarter of that year. “The headwind from U.S. dollar appreciation and the rise of bond yields should abate,” the bank says. Similarly, Citi says that mining companies are changing their behavior, which could lead to value creation in the coming years, reports Bloomberg.

Threats

- Barnabas Gan, an economist with Oversea-Chinese Banking Corp (and one of the most accurate bullion forecasters tracked by Bloomberg), believes gold will be on the retreat in 2017 “on rosier global economic growth and tighter policy from the Federal Reserve,” reports Bloomberg. Gan say that bullion will be at $1,175 an ounce in the first quarter, $1,150 between April and June, $1,125 in the third period and $1,100 by the fourth.

- Bank of America Merrill Lynch forecasts gold to trade around $1,200 an ounce by mid-2017, implying limited upside near-term. Just five months ago the bank called for gold to hit $1,500 an ounce, a much different tone than this new forecast. After prices hit a 13-month high following Brexit, the bank increased its 2017 outlook in July. Now that prices are low, they are forecasting lower. Costanzian Theory would suggest investors do the opposite of the bank’s recommendation.

- JP Morgan cited in a recent report that a tail risk for the market could be realized if the U.S. dollar continues to strengthen, yields rise and global central banks turn more hawkish. “This combination would increase the risk of recession,” the report states. In this situation we could see monetary policy reverse and the application of aggressive monetary and fiscal easing. “In these circumstances, it would not be unreasonable for safe haven, inflation sensitive assets such as gold to reach all-time highs.” The bank advocates a barbell approach – long stocks, long gold as a means to balance the threat of an equity correction.

Energy and Natural Resources Market

Strengths

- A surge in Chinese imports sent iron ore prices to a 27-month high. Despite bearish predictions amongst analysts, iron ore prices have doubled from their 2015 lows. Chinese imports climbed the most in two years on the back of strong demand for iron ore and other base metals.

- The best performing sector for the week was the Bloomberg Americas Auto Parts & Equipment Index. The index rose 8.7 percent following upgrades by major bank analysts, and the disclosure of increases in buybacks for some specific names.

- Rosneft PJSC, the world’s largest publically traded petroleum company by output and the leader of Russia’s petroleum industry, was the best performing stock this week finishing up 11.3 percent. The stock rallied following the announcement of a 19.5 percent stake to the Qatar Sovereign Wealth Fund and Glencore PLC.

Weaknesses

- Platinum was the worst performing commodity this week falling 2.3 percent. French bank Natixis issued a warning for the metal stating that in Europe, where vehicles tend to rely on platinum, consumers are slowly shifting to models using more palladium.

- The worst performing sector this week was the S&P/TSX Diversified Metals & Mining Index. The index of Canadian miners fell 5.4 percent dragged down by Teck Resources and weaker thermal and met coal prices.

- The worst performing stock for the week was Sibanye Gold Ltd. The South African gold miner dropped 16.1 percent after offering to buy U.S.-based Stillwater Mining, which operates the highest grade platinum deposit in the U.S.

Opportunities

- Gold may see increased buying out of the Middle East after the Accounting and Auditing Organization for Islamic Financial Institutions designated gold investments as Shariah-law compliant. Considering the size of Islamic Finance participants, the interest may be high, and should prove bullish for gold prices.

- Natural gas prices could rally as meteorologists forecast a deepening cold front over the next three weeks. Implications for natural gas are very positive as analysts suggest December withdrawals could be as high as 500 billion cubic feet (bcf) versus last year’s 200 bcf.

- The debt markets appear to have reopened for oil and gas producers. Chesapeake Energy Corp, one of the world’s largest exploration and production companies, tapped the debt market for the first time in two years suggesting banks and debt investors feel more confidence that the oil glut may be over. This should prove positive for other companies in the space looking to raise debt capital.

Threats

- Crude oil prices might be subject to greater than average volatility in 2017 than expected. Despite an incredible rally last week after OPEC finally reached an agreement to cut supply, crude oil may be at the mercy of hedging activity from U.S. shale producers. This hedging has flattened the futures curve, suggesting price gains may stall in 2017 according to Glencore’s chief Ivan Glasenberg, one of the biggest traders in oil.

- The future of copper’s rally may be in question after Moody’s noted that an overhang in inventories suggests long-term fundamentals are not supportive of the recent short-term price rally. The credit rating agency embarked on a sector wide review of 87 global copper miners and is currently in the process of downgrading many names in this space to junk.

- Brazil, one of the world’s largest exporters of soybeans, is facing a turbulent rain and thunderstorm season. It is still too early to determine what kind of damage will be done to the crops but these developments will be sure to add volatility to soybeans in the short term.

China Region

Strengths

- China’s November readings for imports and exports both beat expectations: imports rose 6.7 percent, well ahead of an expected decline of 1.9 percent, while exports jumped 5.9 percent, also well ahead of an expected decline of 1.0 percent.

- November Caixin China Services purchasing managers’ index (PMI) data came in at 53.1, up from October’s reading of 52.4, and yielding a Composite Caixin China PMI for November that was right in line, at 52.9, with October’s reading.

- Taiwan’s year-over-year exports came in ahead of expectations, up 12.1 percent, better than an anticipated rise of only 9.3 percent.

Weaknesses

- China’s November reading for foreign exchange (FX) reserve levels dropped some $69 billion, more than expected, to $3.052 trillion, down from $3.121 trillion in October.

- The most recent export data for the Philippines (October, released this week) showed a miss, rising only 3.7 percent year-over-year, below expectations for a gain of 7.9 percent.

- Malaysia also missed, on both imports and exports, with year-over-year exports dropping 8.6 percent, below the drop of 5.6 percent that was expected, and imports falling 6.6 percent, well below expectations for a minor drop of only 10 basis points.

Opportunities

- Earlier this week the Shenzhen-Hong Kong Stock Connect program officially kicked off, and while some suspect that Hong Kong-bound inflows may be limited by the current hostility toward mainland outflows, the stock connect should be a long-term positive for China and its liberalization of capital and investment.

- Samsung, which recently moved the auto space with its Harman acquisition, announced this week that it will also be a Tesla supplier after signing a memory chip supply and design agreement. In China, too, we have some interesting news, as auto sales numbers are on their way to finishing out a twenty-sixth straight record year (although some concerns linger about the viability of future sales if expiring tax incentives are not extended).

- While U.S. President-elect Trump has all but killed the Trans-Pacific Partnership, China is moving, along with other regional partners, to create a new trade deal, one to which China would actually be party, if not cornerstone, known as the Regional Comprehensive Economic Partnership (or RCEP). Current talks in Indonesia will be followed by further talks in Japan in February.

Threats

- Following weeks of protests and pushback, South Korea’s beleaguered and increasingly unpopular President Park has been impeached. (If you read this column regularly, this should not be a total surprise.) The precise consequences of the impeachment and of Park’s potential exit (potential because the impeachment must first be ratified by the constitutional court) remain at present uncertain, and although snap elections could come as soon as two months’ time and while we do know that Prime Minister Hwang Kyo-ahn would presumably be acting interim President, it is still unclear whether and to what extent Park may face prosecution (she is currently essentially immune), what potential reform/s may result—if any—etc. Stay tuned for more on South Korea.

- U.S. President-elect Trump continues to keep policy-watchers on their toes, and his protocol-breaching fielding of a call from the democratically-elected President of Taiwan, Tsai Ing-wen, ruffled quite a few feathers in Beijing. The U.S. President-elect’s rhetoric on China and trade has not lessened either. It seems clear that Mr. Trump is keen to convey the message that there is indeed a new sheriff in town, but at the same time, policy questions revolve around the possibility and extent to which Mr. Trump—one obviously familiar with the use of the media—is merely entertaining, as opposed to negotiating, bargaining, or shifting policy in any major ways. (Of course, he may well be at all of the above.)

- The yuan rose once more above 6.9 this week and remains something of a threat amid lower FX reserves numbers and more chatter of capital outflow crackdowns.

Emerging Europe

Strengths

- Poland was the best performing country this week, gaining 4.6 percent. S&P unexpectedly raised its outlook on Poland’s rating to stable from negative. The group is no longer worried that the Polish government will try to undermine the independence of the central banks, and believes that weaker growth will not harm public finances.

- The Russian ruble was the best performing currency this week, gaining 1.8 percent against the U.S. dollar. Borrowing in U.S. dollars and investing in ruble assets (a so-called carry trade), returned 26 percent for investors this year. UBS AG expects the ruble to offer substantially higher carry than any other market in Europe, the Middle East and Africa.

- The real estate sector was the best performing sector among eastern European markets this week.

Weaknesses

- Romania was the worst performing country this week, losing 80 basis points. Romania will hold a parliamentary election on December 11. According to the latest polls, the PSD (Social Democrats) are likely to win the election after they promised voters higher wages and lower taxes. Almost 27 years since the revolution that toppled communist dictator Nicolae Ceaușescu, Romania is still the second poorest country in the European Union.

- The Hungarian forint was the worst performing currency this week, losing 1.5 percent against the U.S. dollar. Emerging European currencies declined after the European Central Bank (ECB) announced extension of its quantitative easing (QE) plan, with the Hungarian forint recording the biggest losses.

- The health care sector was the worst performing sector among eastern European markets this week.

Opportunities

- The ECB decided Thursday to extend its asset purchase program by nine months to the end of 2017. However, the monthly purchase value will be reduced to EUR 60 billion from current EUR 80 billion in April of next year. All interest rates were kept unchanged, and the QE program would allow for the purchase of bonds with less than two years in maturity and bonds trading with a yield that sits below the Bank’s deposit rate of -0.4 percent. Germany’s 2-year notes are yielding negative 0.7 percent, and they gained the most in more than two weeks. Mario Draghi commented that the ECB can add to the program in size and duration if the outlook turns less favorable.

- Commodity Trader Glencore Plc and Qatar’s sovereign wealth fund agreed to buy 19.5 percent stake of Rosneft, Russia’s biggest state-owned oil producer, for $11 billion dollars. It is the biggest foreign investment in Russia since the crisis in Ukraine and since sanctions on the country were imposed. Luis Saenz, head of equity sales and trading at BCS Financial Group in London, said that this transaction is a massive positive for Russia moving closer to breaking the sanction/isolation regime.

- December’s preliminary PMI data for the eurozone will be reported next week. Latest readings have shown an increase in manufacturing activity, with November PMI at 53.7, the highest reading since the beginning of 2014. The positive trend may continue.

Threats

- Fitch has revised the Turkish banking sector outlook for 2017 to negative from stable. Political uncertainty is likely to put pressure on Turkey’s long-term performance and bank asset quality. Foreign currency lending makes up about a third of total loans and is at risk as the lira has fallen sharply since 2013 and could fall further.

- The Greek government was hoping to have an agreement on the second review this month, but it is unlikely that it will happen. There are still many uncertainties regarding the medium- and long-term debt measures, the fiscal gaps for 2018 and after, and the primary surpluses for the same time. Greek banking stocks could rally after the short-term Greek debt relief measures have been agreed upon, and short-term correction in the following days is likely.

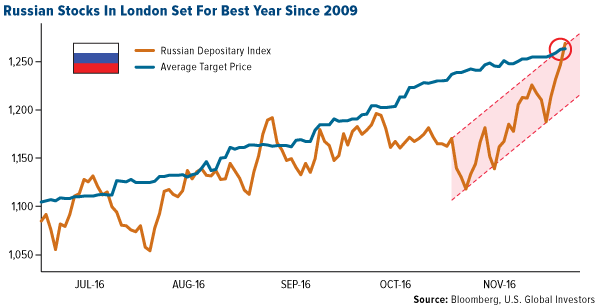

- The Russian ruble advanced 14 percent this year, the most since the collapse of the Soviet Union, and Brent crude oil gained 16 percent during the same period. This has helped Russian stocks listed in London beat analysts’ expectations.

© US Global Investors