New president, same DOL rule for now

Now that Donald Trump has been elected as the next President of the United States, the financial services industry wants to know, among other things, what the incoming administration plans to do with the much-maligned DOL Fiduciary Standard Rule. But given that many financial services companies will already be in the process of implementing the rule, it’s unlikely that many of them will revert back to the old system even if the rule is eventually repealed.

Designed to protect retirement investors, the DOL fiduciary rule stipulates that anyone who advises or makes recommendations to retirement plans, plan participants, or IRA owners, is now considered a fiduciary. At 923 pages long, the rule is expansive and complex, yet if there’s one overarching theme throughout, it's that of risk management. In short, the rule seeks to minimize risk to retirement investors while transferring new fiduciary duties to financial advisors.

Financial advisors are going to have to take a much more comprehensive approach to risk management that starts at the practice level before moving onto client retirement portfolios. This includes a thorough review of advisory operations and determining exactly who in your practice—front as well as back-office—is considered a fiduciary. The review of your business should also encompass all marketing materials—including web content, investor kits and advertising—which have to be scrubbed to make sure they’re DOL rule compliant.

As an alternative, many advisors are considering the Best Interest Contract Exemption (BICE), but this comes with its own issues. The most daunting aspect of BICE, however, is the threat of class-action lawsuits from IRA investors, who can sue advisors if they believe their interests haven't come first. And not only is there a litigation threat, but the burden of proving compliance with BICE provisions falls to the institution claiming the exemption, not the class of investors bringing suit.

Battered by transition risk

The risks to financial advisory practices are directly linked with those of their clients. Once risks have been identified, minimized and eliminated where possible at the advisory level, it’s time to take closer look at the risk embedded at the portfolio level. Among the chief concerns here should be transition risk, which is the risk of transitioning from the accumulation phase of retirement investing to the income phase under unfavorable market conditions.

For a stark example, think back to October 2008—the height of the financial crisis—when asset classes across the board fell in unison. US equities alone, as measured by the S&P 500 Index, returned -17% for the month. This was a rude awakening for those retiring towards year-end, who encountered much higher transition risk, and consequently much lower portfolio values, than those retiring earlier in the year.

After being battered by transition risk, those 2008 year-end investors then had to contend with drawdown risk, which is essentially the risk of outliving one’s retirement savings as account balances dwindle ever downward. Essentially, heightened transition risk leads to heightened drawdown risk as the actual amount to drawdown in retirement may be much lower than anticipated.

In managing client portfolio risks, advisors may believe that passive investments alone are the way to go because their risks are more readily quantifiable and understood by both advisor and client. But this is precisely the kind of thinking that may lead to heighted transition and drawdown risk as the client is at the mercy of the market. The smart alternative here may be active investment portfolios that seek to manage risk just as much as they do return.

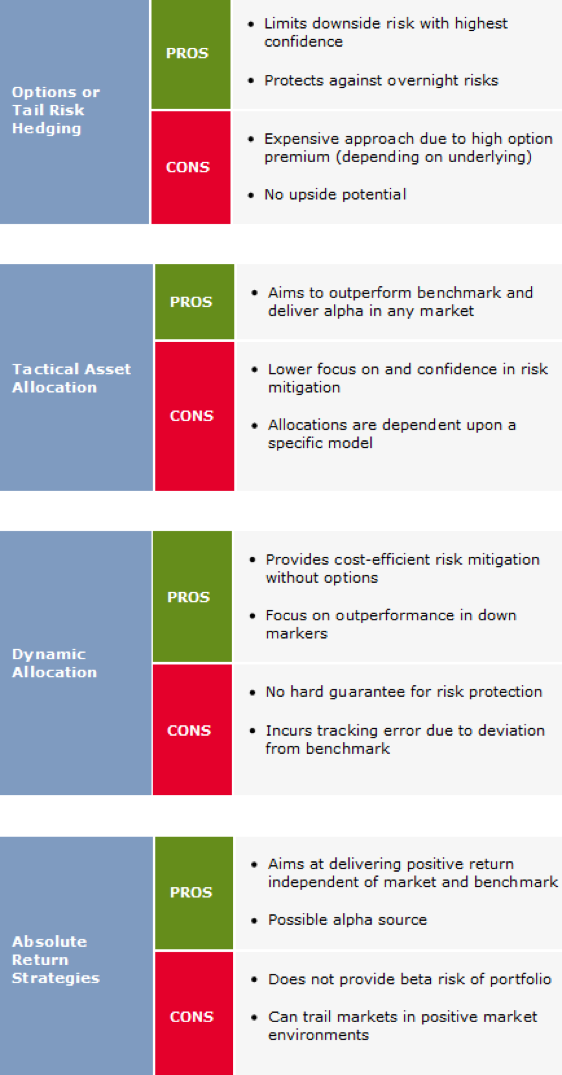

Actively managing risk

Managing for return is one thing, and managing risk is quite another. Here are four investment strategies that place equal importance on both for a more holistic approach to market uncertainty:

Subscribe Today

Dialed In to Retirement is available as a subscription for financial professionals only. New issues will be delivered via email every month. Your email address must be in our records for your subscription to take effect.

About the Author

Glenn Dial is Head of Retirement Strategy in the US with Allianz Global Investors, which he joined in 2011. He has 23 years of defined contribution experience. Mr. Dial is a co-inventor of the method and system for evaluating target-date funds, and is also credited with developing the target-date fund category system known as “to vs. through.”

Important Information

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Allianz Global Investors Distributors LLC, 1633 Broadway, New York, NY 10019-7585, us.allianzgi.com, 1-800-926-4456.

85785