KEY TAKEAWAYS

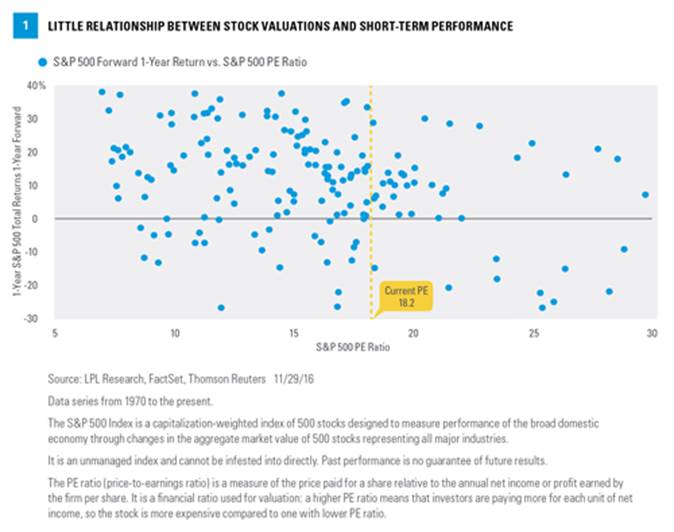

- Valuations are elevated, but there is very little relationship between stock valuations and performance in the short term.

- Consumer confidence breaking out to new post-recession highs confirms the bull market in equities.

- December has been a very strong month historically for equities and could bode well for continued near-term gains.

Twenty years ago today, Federal Reserve (Fed) Chairman Alan Greenspan gave his now-famous “Irrational Exuberance” speech at a dinner hosted by the American Enterprise Institute.The phrase was meant to be a warning about stretched valuations of equities during the 1990s bull market. Although his warning was three years early, the market factors Greenspan highlighted eventually did contribute to the dot-com bubble bursting, leading to the first 10-year decline (from 1999–2008) in the S&P 500, including dividends, since the 1930s, which was exacerbated by the early-2000s recession.

With equity markets making new highs and the bull market close to turning eight-years old, are we entering another period of irrational exuberance? This week we will examine this question by taking a closer look at the three components of our methodology: valuations, fundamentals, and technicals.

VALUATIONS STRETCHED, BUT NOT EXTREME

Traditional market cap weighted valuations are high—the current price-to-earnings ratio (PE)* (trailing four quarters) of roughly 17 is above the average of 15 going back to 1950, and the post-1980 average of 16. But it is nowhere near the euphoric levels of the late 1990s, when PE multiples were consistently in the upper 20s. Even then, it was hard to tell when to sell stocks because they can stay overvalued for long periods. At the end of the bubble, the one-year return for the S&P 500 from March 31, 2000 and a PE of 28.2, was -21.7%, so valuations were a good reason to sell then. But the stock market’s PE was high well before that, suggesting that even at extremes, forecasting market direction using valuations can be an inexact science. In fact, the three years after Greenspan’s speech, the S&P 500 gained another 93% in the face of high PEs.

*Price-to-earnings ratio (PE) is for S&P 500 companies.

PEs have not been good indicators of stock market performance over the subsequent one year as shown in Figure 1. If the dots in Figure 1 formed something resembling a straight line, it would suggest lower returns were to be expected at higher PE ratios. The correlation between the S&P 500’s PE and the index’s return over the following year, at -0.3, is relatively low and suggests a fairly weak relationship. We would be more worried about high valuations in a scenario in which the market begins to, or actually does, price in a recession.

CONSUMER CONFIDENCE BREAKS OUT

The fundamental backdrop continues to suggest very little chance for a recession in 2017, as just last week Q3 2016 gross domestic product (GDP) was revised up to 3.2% from 2.9%—spurred by strong consumer spending. Additionally, U.S. manufacturing, as measured by the Institute for Supply Management, improved as the U.S. manufacturing index rose to 53.2 in November 2016, thanks to higher construction spending. A reading over 50 suggests economic expansion. This all comes on the heels of the end of the year-long earnings recession, and although we are mid-stage in this economic cycle, fundamentals continue to be on firm footing, if not outright improving.

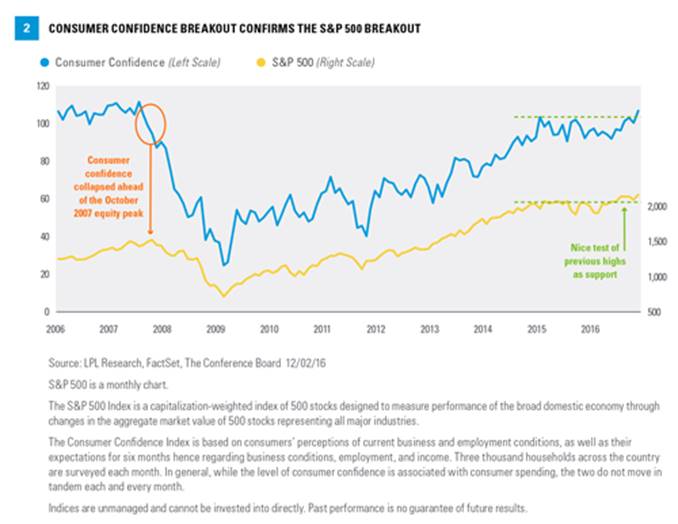

The other big positive last week (November 28-December 2, 2016) was that the Conference Board’s Consumer Confidence Index in November rose to 107.1, the highest since July 2007. In the late 1990s, consumer confidence was in a steady uptrend, and the index eventually peaked near 145 in early 2000. In other words, not that we are forecasting a return to those lofty levels, but there is plenty of room for this to move higher before there is a major excess of confidence.

As Figure 2 shows, this breakout also coincides with the breakout in the S&P 500. Historically, consumer confidence has confirmed moves in the equity market, and these new highs show no major warnings or divergences. For example, at the October 2007 equity peak, consumer confidence had already broken down, suggesting a major warning under the surface for equities. Fortunately, this isn’t the case currently with both at new highs.

TECHNICALS CONTINUE TO LOOK STRONG, BUT BULLISH SENTIMENT IS RISING

Taking another look at Figure 2, the S&P 500 on a monthly chart clearly found support at the peak in 2015. In technical analysis, finding support at previous resistance levels is important. Should the 2015 peak have been violated, that would have suggested the bull move was in danger. The current technical backdrop looks constructive and the U.S. equities bull market appears to be alive and well.

Sentiment is another important part of technicals. A month ago, the Dow leaked lower for nine consecutive days, the longest daily losing streak in 35 years, although it only lost 1.8%, and many sentiment polls were flashing similar amounts of fear seen right before the Brexit vote in late June 2016. Once the election was over and the worst fears didn’t materialize, the S&P 500 gained 3.4% for the best November in seven years, setting new all-time highs along the way. Now we are seeing a much different sentiment backdrop, as new highs have forced some of the bulls out of hibernation.

The American Association of Individual Investors (AAII) Sentiment Survey had gone a record 54 consecutive weeks without the bulls above 40%. After the election, the bulls finally spiked up to nearly 50%, the highest reading in nearly two years.

Additionally, active managers are now exposed to equities near historic levels. The National Association of Active Managers (NAAIM) Exposure Index came in at 98 last week, one of the highest readings during the 10-year history of the survey, in the top 2% of all the readings. This suggests active managers are nearly fully exposed to equities, which has historically served as a contrarian warning sign.

The big question though is, Are these signs of irrational exuberance? We would rate the overall sentiment backdrop as a near-term concern, but by no means are we seeing the over-the-top type of euphoria seen at major peaks. For instance, the AAII poll had a record of 75% bulls in early 2000, well above current levels. Additionally, according to data from Bloomberg, U.S. domestic equity funds still haven’t seen a weekly inflow since the election. In fact, there have been outflows for 39 consecutive weeks, a clear sign most investors are still wary of things.

WILL SANTA COME IN DECEMBER?

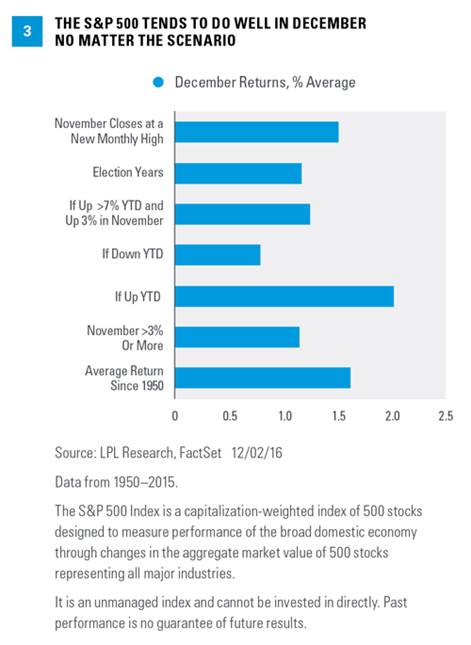

Seasonality is another branch of technicals and it is important to note that December has been a strong month historically for equity gains.

· Going back to 1950, no month has sported a better average return than the 1.6% return seen in December.

· Interestingly, returns in December jumped to 2.0% when the S&P 500 was up year to date heading into the month, versus up only 0.8% if down year to date.

· If November has a big gain, does it steal some of Santa’s thunder? It looks like it has done so slightly, as when November gained more than 3% (like 2016), the average return in December dipped to 1.2%.

· When November closed at a monthly new all-time high (like 2016), December gained another 1.5%.

· Lastly, election years have been up 1.2% in December; and when November was up 3% or more and the year-to-date return was more than 7% (like 2016), December still gained 1.3% on average.

As Figure 3 shows, equities usually gain in December under various scenarios, and the worst scenario below (down year to date) doesn’t even count this year.

It is worth pointing out that December monthly return has been negative each of the past two years for the S&P 500, but going all the way back to 1928, it has never been down three consecutive years. That bodes well for 2016, along with these two impressive stats as well:

· December has never closed as the worst month of the year for the S&P 500. It has closed as the 10th or 11th worst month a few times, but never the worst. January was the worst month in 2016 at -5.1%, so even if things are bad this month, history has shown that they probably won’t be worse than the 5.1% drop in January.

· Another sign of how strong December tends to be is only once since 1950 has the S&P 500 closed at the end of December beneath the low close of November. The low close in November was on November 4, at 2085.18 (about 4.6% below current levels), so the chances of December closing beneath that level appear to be very slim based on history.

But what if there is a selloff? As Figure 4 shows, when December is red, it is down by only 2.1% on average, the smallest average loss out of all 12 months. Not to mention when it is green, it is up an average of 7.0%—the best performance out of the 12 months.

CONCLUSION

Greenspan’s speech from 20 years ago is a nice reminder to objectively assess fundamentals, valuations, and technicals to make sure the bull case for equities is still valid. Our take is this bull market may be old, but it still has legs. In fact, we continue to expect mid-single digit returns from stocks in 2017, as we recently discussed in our Outlook 2017 Executive Summary.*

*We expect mid-single-digit returns for the S&P 500 in 2017 consistent with historical mid-to-late economic cycle performance. We expect S&P 500 gains to be driven by: 1) a pickup in U.S. economic growth partially due to fiscal stimulus; 2) mid- to high-single-digit earnings gains as corporate America emerges from its year-long earnings recession; 3) an expansion in bank lending; and 4) a stable price-to-earnings ratio (PE) of 18–19.

Thank you to Jeff Buchbinder for his contributions to this report.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

All investing involves risk including loss of principal.

The P/E ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher P/E ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower P/E ratio.Correlation ranges between -1 and +1. Perfect positive correlation (a correlation co-efficient of +1) implies that as one security moves, either up or down, the other security will move in lockstep, in the same direction. Alternatively, perfect negative correlation means that if one security moves in either direction the security that is perfectly negatively correlated will move in the opposite direction. If the correlation is 0, the movements of the securities are said to have no correlation; they are completely random.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The ISM Manufacturing Index is based on surveys of more than 300 manufacturing firms by the Institute of Supply Management. The ISM Manufacturing Index monitors employment, production, inventories, new orders and supplier deliveries.

The Consumer Confidence Index is based on consumers’ perceptions of current business and employment conditions, as well as their expectations for six months hence regarding business conditions, employment, and income. Three thousand households across the country are surveyed each month. In general, while the level of consumer confidence is associated with consumer spending, the two do not move in tandem each and every month.

American Association of Individual Investors (AAII) Sentiment Survey is an independent survey that compiles responses from individual investors.

The National Association of Active Managers (NAAIM) Exposure Index represents the average exposure to U.S. equity markets reported by its members.

© LPL Financial

Read more commentaries by LPL Financial