A Lesson in Microeconomics - How to Get the Economy Going Again

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits“There is a delusion that macroeconomics is both viable and useful - a delusion encouraged by its extensive use of mathematics, which must always impress politicians lacking any mathematical education, and which is really the nearest thing to the practice of magic that occurs among professional economists.”

F.A. Hayek

Closing the loop on last month’s Absolute Return Letter

“Will you marry me?” The young man, not yet past the pimple stage, could hardly contain his excitement. “Yes, if you make me two promises”, the girl said. “Don’t ever ride a motorbike and promise me never to go into politics.” “I promise”, he said, and the rest is history.

The conversation took place in 1984, but I remember it as if it was yesterday. The young man was obviously me, and the girl was my wife-to-be. I bring it up now, because the recent US elections taught me (and my wife) an important lesson. Not only should I have promised never to enter politics. I should also have undertaken never to engage in politics of any kind – not even write about it.

The amount of offended US readers last month, when I made fun of Trump, made me realise that while I obviously cannot avoid commenting on politics altogether, as it has always had, and always will have, a major impact on financial markets, I can certainly stay away from commenting on individuals. Lesson learned.

The stagnation conundrum

Now to something more productive – a different way to look at how we get the economy going again. I apologise if this month’s Absolute Return Letter is a tad theoretical in places, but there is no way around it, and I hope you can follow my thinking. Our long-standing economic consultant Woody Brock visited us only a few days after the U.S. elections, and he inspired me to write this month’s Absolute Return Letter.

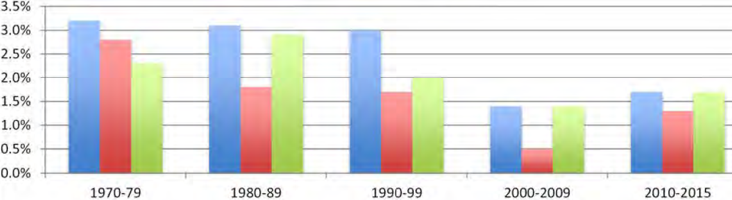

Charts 1a-d below tell a story of stagnation along several dimensions in some of the world’s leading – and most open - economies (the US, Germany and the UK). The picture is not 100% consistent. Germany, for example, went through a period of dismal productivity growth in the 1970s and 1980s, followed by a period of exceptionally high productivity growth in the 1990s post-reunification, but the trend line is consistent enough that it warrants further work and commentary.

Nominal as well as real GDP growth is in a multi-decade decline. Productivity gains have lost momentum for many, many years, and inflation is lower than ever. One could certainly be forgiven for asking the question - what on earth is going on?

Chart 1a: Nominal GDP growth by decade (CAGR)

Chart 1b: Real GDP growth by decade (CAGR)

Chart 1c: GDP per hour worked (productivity) by decade (CAGR)

Chart 1d: Average annual inflation by decade (CPI)

Sources: Strategic Economic Decisions, OECD, BEA, World Bank, WDI, August 2016

Why the stagnation conundrum?

Economists – both those in academia and those in the ‘real’ world – have spent endless amounts of time looking for an explanation. Going into detail on every suggestion that has been put forward over the years would be overkill, but it would probably be fair to say that the following six reasons cover the vast majority of suggestions made when commentators have looked for a reason why ‘everything’ appears to be stagnating:

- A statistical mirage.

Argument: There really isn’t a problem. Smartphones replacing cameras, etc., underestimate actual economic growth.

- A hangover from the Global Financial Crisis.

Argument: Severe financial crises make recovery from a downturn all the more difficult.

- Secular stagnation.

Argument: Reduced population and workforce growth, lower prices for capital goods, and the nature of recent innovations (e.g. online shopping replacing brick and mortar shops) all hold back economic growth.

- Slower innovation.

Argument: The pace of innovation has declined; almost everyone now benefits from the things that matter the most to productivity – e.g. electricity, cars, etc., and recent innovations are more marginal in nature in terms of benefit.

- Policy Missteps.

Argument: An increase in government spending combined with tax hikes (which is a policy pursued by many governments in recent years) has had a strong negative impact on private investment spending.

- Increased ‘rent-seeking’ behaviour.

Argument: Abuse of market power, monopoly profits, etc., have contributed to the slowdown in wages and output (think Apple vs. the EU).

In fact, not a single one of those six suggestions provide a satisfactory explanation for the stagnation conundrum. They have all played a role – some more than others – but not a single one deserves to be credited as the main reason.

The weakest is probably the second one. How can something that materialised around 2007-08 explain a trend that began in earnest in the 1980s? My professor at university was fond of telling us students that, however intricate the question is, as an economist you are expected to always provide an answer, but I am afraid I have to pass on this one.

So, are we heading back to the drawing board? Could years of hard work possibly be wasted? Should I ask for a refund on my tuition fees? No, fortunately, it isn’t that bad, but you’ll have to put your macroeconomic wisdom to one side for a while and instead tune in to something most investors spend little time on these days - microeconomics. Let’s get started.

A new microeconomic way to interpret GDP growth

So that we can make the appropriate comparisons, let's start from first principles and define GDP in a very orthodox (macroeconomic) way. Just about every civilized country on planet earth defines GDP as the sum of consumer spending, corporate investments, government spending and net exports (defined as exports minus imports), or:

GDP = C+ I + G + (X-M)

That formula was one of the very first I learned when I started to read economics back in the early 1980s, and it was presented to us still-wet-behind-the-ears students as the holy grail, but there is another way.

Think microeconomics. Assume there are n companies in the private sector, and think of GDP as the sum of the value-added created by those n companies. The value-added can be defined as total revenues (r) less the cost of generating those revenues ©. All one would have to do to arrive at the same number for GDP as above would be to add government spending (G). That said, the private sector GDP can thus be expressed as follows:

GDP Private Sector = ∑(rn – cn)

Under reasonable assumptions, ∆GDP Private Sector = ∑∆rn and r=pÍq (revenues equal price multiplied by quantity), i.e.:

∆GDP Private Sector = ∑∆(pnÍ qn)

In microeconomics, the price and quantity that a company can achieve on its goods and services is a function of where demand (D) meets supply (S) which, in geometric terms, is where the two lines cross each other in chart 2. The equilibrium (A) is precisely where S meets D, and the shaded area under A equals price multiplied by quantity (pxq).

Chart 2: Geometric interpretation of GDP growth

Sources: Strategic Economic Decisions, August 2016

Now, assume both S and D move out as the economy grows, but that S moves out faster than D (for reasons I will come back to later). The shaded area under the new equilibrium (B) is the new pÍq, and the difference between the two shaded area equals ∆GDP in the private sector.

This is very important. It effectively means that the real reason the economy has ground to a near halt in recent years is that we have allowed S to move out much faster than D, and that we could accelerate economic growth again, if we could somehow find a way to push D out faster than S.

According to microeconomic theory, the change in economic growth is essentially a function of the S-curve and the D-curve. I do not want to over-complicate matters so have assumed that both the S- and the D-curve are linear but, in reality, they won’t necessarily be. Mathematically, we can now express the change in economic growth the following way:

∆GDP = f(∆Sn,∆Dn)

Explaining the stagnation in economic growth in this microeconomic way is new thinking in economic circles and, if the theory is correct, addressing mediocre economic growth shall require a different policy approach than the one favoured by policy makers in recent years (i.e. through QE). How it could be implemented in practice, I will come back to.

It could get even worse

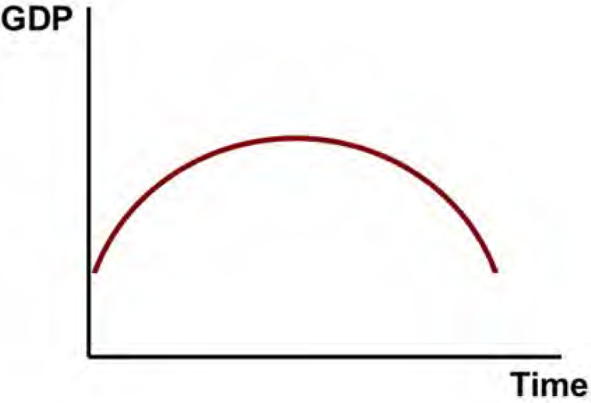

However, before I propose solutions, let me share some bad news with you. If we do nothing, D will most likely continue to shift out more slowly than S, prices will fall more broadly, and ∆GDP will ultimately turn negative. Why is that?

Make the following assumptions. Assume that (i) the D-curve is always downward sloping (as it is), (ii) the S-curve is always upward sloping (as it is), (iii) S shifts out faster than D over time (as it has done for a number of years), and (iv) both the S-curve and the D-curve are linear (as they are most of the time).

Based on those assumptions (none of which are far from the real world), it can be proven mathematically that GDP growth will conform to a downward-opening parabola (see chart 3), and that it will ultimately turn negative. In other words, it is not entirely unrealistic that, if we choose to sit on our hands and do nothing (and, in this context, QE and other means of monetary policy is akin to doing nothing), not only could the stagnation of recent years continue for a long time to come, but it may actually get even worse.

Prices could start to decline more broadly, and economic growth could turn negative. What I have characterised as good deflation in previous Absolute Return Letters could quite possibly turn into bad deflation – very much like in the 1930s.

Chart 3: GDP growth when S shifts out faster than D

Sources: Strategic Economic Decisions, August 2016

Why the S-curve has shifted out faster than the D-curve

Before I suggest some practical solutions to this conundrum, let me offer at least a couple of reasons why the S-curve has actually shifted out faster than the D-curve since the 1980s.

The question you need to ask yourself is the following – did anything fundamentally change around that time? Has anything been fundamentally different since the early 1980s compared to what is was like before then?

It is certainly not demographics, as they were largely positive throughout the 1980s and 1990s, so what could it be? Think national income, and remember how national income is divided between capital and labour in the national accounts. Then look at the growth in labour income, which has been miserable for the past 30-35 years.

If you combine that with the knowledge that 95% of all salary earners in the US (and a little, but not dramatically, less elsewhere) spend virtually every penny they earn every month, poor growth in earned income for the vast majority of the population has had the effect of cutting back spending power and thus affected the D-curve negatively.

At the same time, the S-curve has shifted out relatively fast, partly because of a bigger share of national income going to capital (which has had a profound effect on companies’ ability to invest in new and better technology), and partly because of globalisation.

Solutions

If you go back to the formulas presented above – the microeconomic way of measuring ∆GDP – there is effectively only one way to re-accelerate economic growth in the private sector, and that is to establish conditions for D to shift out faster than S. If one were to combine microeconomics with the traditional macroeconomic way of looking at things, one could also create more economic growth by increasing government spending (G). Both of those initiatives would affect ∆GDP positively.

Going back to the policy makers’ choice of policy in recent years – monetary policy – it is important that a regime shift takes place. Policy makers need to realise once and for all that monetary policy has no meaningful impact on the D-curve. If anything, access to cheap growth capital has probably allowed the S-curve to shift out more rapidly than the D-curve.

Monetary policy – and QE in particular - served an important purpose in the immediate aftermath of the financial crisis, but central bankers have allowed it to become a quasi-permanent feature, and that is a mistake. Our political leadership should instead turn its attention to fiscal policy.

∆G can be affected in many ways, but the only responsible way to spend more public money would be to do it in a way that affects productivity positively, and that means more infrastructure spending. The UK and the US could certainly do with a better infrastructure, and they are not the only two countries.

Now the trickier one – how do you ensure that the D-curve shifts out faster than the S-curve? Are there ways you can enhance the spending power of the broad public without turning it into a socialist economy? The answer is yes - think helicopter money, but certainly not Zimbabwe-style helicopter money, which was an absolute disaster. Think of it instead as helicopter money achieved through fiscal means and designed to increase the spending power of the poorest 95% of income earners.

One way to do it would be to lower the tax rate for low income earners or to send them a monthly cheque. Before you object to spending public money on non-productivity enhancing initiatives, think about the trillions of dollars that corporates from all over the world have stashed away in offshore tax havens. Taxing that money at a reasonable rate could easily finance such an initiative, and pushing out the D-curve would benefit the corporate sector anyway.

Investment implications

Infrastructure spending and helicopter money would both have the likely effect of increasing the public deficit, at least temporarily, so rising interest rates would be almost inevitable. That said, if the alternative is a 1930s style depression with bad deflation and negative GDP growth for several years, rising interest rates would be a small price to pay.

Equities could actually perform quite well, assuming only modestly rising interest rates. Historically, the sweet spot for equites is most definitely higher levels of interest rates than current levels, although a dramatic rise would likely be counter-productive. A gradual move away from monetary policy towards fiscal policy would therefore turn me more bullish on equities than I have been in a long time.

In the alternative arena, the obvious game in town is infrastructure, but other investment strategies could also benefit. More on this topic in 2017 - I am running out of time and space.

Concluding remarks

I stated earlier that demographics haven’t had a meaningful impact on f(∆Sn,∆Dn) – at least not in the 1980s and 1990s – but that doesn’t imply that it won’t going forward. Ageing will almost certainly ensure that - ceteris paribus - the D-curve will shift out even more slowly in the years to come, and that is particularly the case in Japan, Korea, and continental Europe, where the demographic outlook is the worst.

As a consequence, those countries would have to take even more drastic action than the US and UK to ensure that D shifts out faster than S, but will they do it? And at what point will bond investors say that enough is enough?

In that context, I believe that bond investors are likely to be far more forgiving, if public money goes towards productivity enhancing infrastructure investments rather than vote-buying transfer incomes.

On that optimistic note, I would like to wish you all a most enjoyable Christmas (if you celebrate it), and may 2017 bring more good news than 2016 did. I will return in early January with my usual annual forecast, which is not at all like what most January forecasts are like, so don’t raise your expectations!

One final note – I am sad to announce that, after almost nine years at Absolute Return Partners, Tricia Ward has decided to move back up North again. Tricia has headed our research team and done some fantastic work along the way, and she will be sadly missed. Good luck with your new life Tricia.

Niels C. Jensen

1 December 2016

©Absolute Return Partners LLP 2016. Registered in England No. OC303480. Authorised and Regulated by the Financial Conduct Authority. Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ, UK.

Important Notice

This material has been prepared by Absolute Return Partners LLP (ARP). ARP is authorised and regulated by the Financial Conduct Authority in the United Kingdom. It is provided for information purposes, is intended for your use only and does not constitute an invitation or offer to subscribe for or purchase any of the products or services mentioned. The information provided is not intended to provide a sufficient basis on which to make an investment decision. Information and opinions presented in this material have been obtained or derived from sources believed by ARP to be reliable, but ARP makes no representation as to their accuracy or completeness. ARP accepts no liability for any loss arising from the use of this material. The results referred to in this document are not a guide to the future performance of ARP. The value of investments can go down as well as up and the implementation of the approach described does not guarantee positive performance. Any reference to potential asset allocation and potential returns do not represent and should not be interpreted as projections.

Absolute Return Partners

Absolute Return Partners LLP is a London based client-driven, alternative investment boutique. We provide independent asset management and investment advisory services globally to institutional investors.

We are a company with a simple mission – delivering superior risk-adjusted returns to our clients. We believe that we can achieve this through a disciplined risk management approach and an investment process based on our open architecture platform.

Our focus is strictly on absolute returns and our thinking, product development, asset allocation and portfolio construction are all driven by a series of long-term macro themes, some of which we express in the Absolute Return Letter.

We have eliminated all conflicts of interest with our transparent business model and we offer flexible solutions, tailored to match specific needs.

We are authorised and regulated by the Financial Conduct Authority in the UK.

Visit www.arpinvestments.com to learn more about us.

©Absolute Return Partners LLP 2016

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits