Corporate Beige Book: Better Tone, Little Election Talk

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKEY TAKEAWAYS

- Our analysis of third quarter earnings conference call transcripts indicates sentiment among corporate executives improved.

- For all of the media attention on the U.S. election, corporate executives spent surprisingly little time on the topic during earnings conference calls.

- Actual third quarter results and improved management tone support our expectation for mid-to-high single digit earnings growth in 2017.

Corporate sentiment improved during the third quarter based on our analysis of earnings conference call transcripts for third quarter 2016 earnings season. We saw greater use of strong and positive words, whereas talk of recession was again virtually non-existent and the election surprisingly garnered relatively little attention. Brexit-related commentary and fewer currency mentions suggest stability in the U.K., while oil and China continued to garner significant attention.

CORPORATE BAROMETER SHOWS SLIGHTLY BETTER TONE

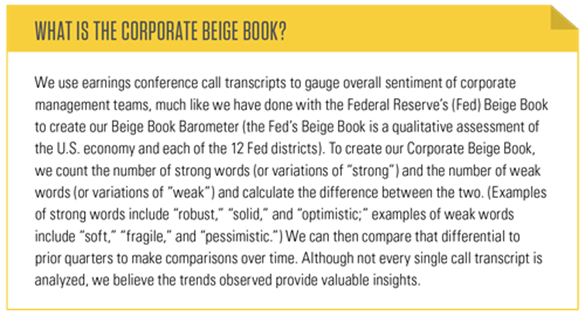

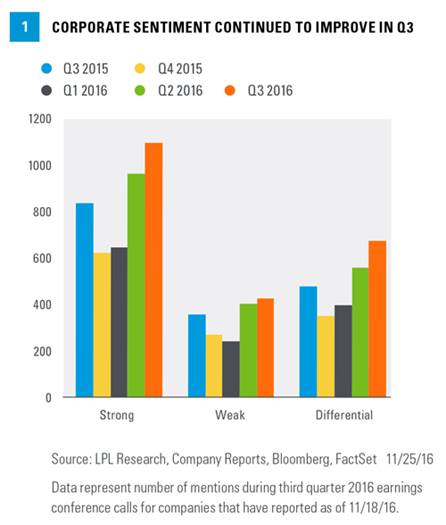

When we count positive and negative words from earnings call transcripts, we see that sentiment among corporate executives improved during the third quarter. More strong and positive words (e.g., strong, robust, solid, improving, good) were counted in the call transcripts sampled [Figure 1]. The word “good” in particular saw a big jump from the second quarter (from 153 to 227). Meanwhile, the weak words (e.g., weak, soft, difficult, and challenging) only increased marginally, pushing the differential and ratio of strong to weak words both higher. The differential between strong and weak words rose 20% to 672 in the third quarter from the second quarter, whereas the ratio of strong to weak words rose from 2.4 to 2.6 [Figure 2].

We observed an increase in the overall use of these strong and weak words for the third straight quarter. Last quarter, we speculated this increase reflected more subtle optimism. It may also be attributed to increased macroeconomic uncertainty, which may have led to increasingly emotional comments from executives.

We are encouraged that this analysis generally reflects the improved conditions in corporate America that we have observed in the economic data and reported earnings and revenue numbers.

SURPRISINGLY LITTLE ELECTION TALK

For all the media attention on the U.S. presidential election, corporate executives spent surprisingly little time on the topic during third quarter conference calls. We found just 31 mentions of the election in the call transcripts we examined for Q3. A search for “Trump” and “Clinton” revealed even fewer mentions. We believe the lack of attention to politics reflects the uncertainty around the outcome and the desire to appear apolitical, especially during this particularly divisive campaign.

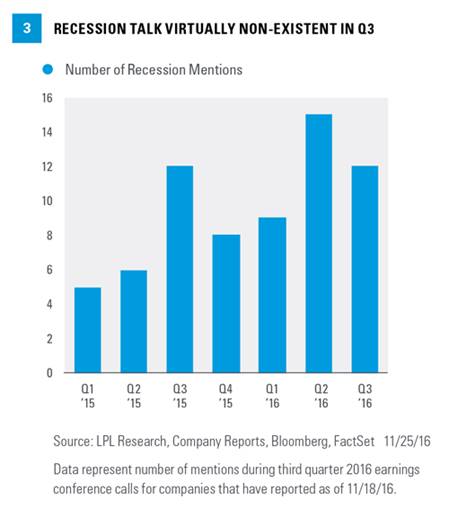

TALK OF U.S. RECESSION NON-EXISTENT

Corporate executives generally try to stay away from the “R” word (recession) when talking with investors, confirmed by the drop in the number of mentions to 12 in the third quarter from 15 in the second quarter. The average number of times the word recession was uttered during the conference calls aggregated over the past seven quarters at less than 10 is surprisingly low, and several of those were related to overseas economies, including the U.K., Brazil, and Russia. We think this bodes well for the near-term economic outlook. [Figure 3]

As we noted in our Outlook 2017 Executive Summary, we believe the odds of recession in 2017 are low based on leading economic data. However, recession risk related to a policy mistake out of Washington, D.C., has risen as 2017 approaches.

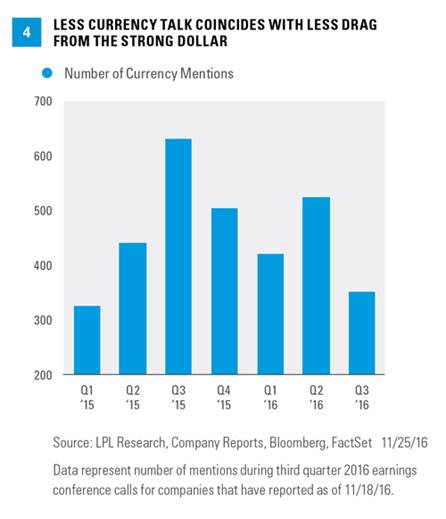

CURRENCY IMPACT CONTINUES TO FADE

Stability in the U.S. dollar was a big part of ending the earnings recession, although recent strength in the greenback has rekindled fears of currency-driven earnings weakness. During third quarter earnings season, currency mentions dropped quite a bit, from more than 500 in the second quarter to around 350 in the third quarter [Figure 4]. We attribute less attention on the dollar to its lessening impact on earnings. The average annual increase in the dollar in 2015 was 17%, compared with flat in 2016 (assuming the dollar stays at November 25, 2016, levels through year-end).

Should the U.S. Dollar Index stay where it closed on November 25, 2016, for the rest of the year, the dollar would represent a 2% headwind in fourth quarter 2016. At that same level, the dollar would represent an average headwind of 5% in 2017. In the Outlook 2017 Executive Summary, we noted that we expect further gains in the dollar to be contained, but that currency is one of the bigger risks to earnings in 2017.

Companies continued to experience some negative currency impacts to earnings during the quarter. As these comments suggest, most of the currency impacts came from the British pound:

“Unfavorable foreign currency reduced sales by about 2% due to primarily the significant year-over-year declines in the Mexican peso and the British pound.” (Materials)

“The weakening of the British pound that has occurred since the Brexit vote at the end of June has been a drag on our reported billings and revenues. But from an earnings perspective, as you'll recall, we are relatively hedged naturally against the pound as the U.K. serves as the headquarters for many of our international operations.” (Financials)

“The strength in the dollar relative to the pound has been challenging. It's probably hurt us by about $0.12 to $0.15.” (Cruise ship operator)

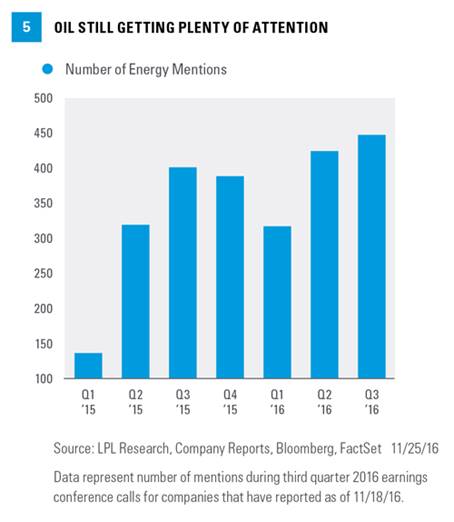

OIL STILL IN THE PICTURE

Oil’s rise from the February 2016 lows in the mid-$20s to its current price in the mid-$40s has eased concerns about the negative impact of low prices on energy companies and energy-sensitive companies, but that does not mean corporate executives have stopped talking about it. As shown in Figure 5, the topic has not stopped getting airtime on conference calls. Should oil stay at current levels, crude prices would average a 12% year-over-year gain in the fourth quarter and a whopping 37% increase in first quarter 2017.

Comments from companies tied to oil and gas reflect a more stable oil price environment:

“All of this means that the period of oversupply and inventory build is over, and that market sentiments should soon change, paving the way for an increase in oil prices and, subsequently, E&P investments.” (Oil services provider)

“Importantly, we see oil prices stabilizing in the $50 range. Generally, activity is picking up across the globe, including in China, and some projects that had been delayed or stalled are now resuming.”(Industrial)

“A recent rally in energy prices has crude oil over $50 a barrel and natural gas over $3 per million BTU, which are both encouraging for our coal and shale-related businesses.” (Railroad operator)

“Over the past few quarters, exposures in our oil and gas [business] that were causing industry concerns for commercial losses have improved and charge-offs have receded.” (Diversified financial services)

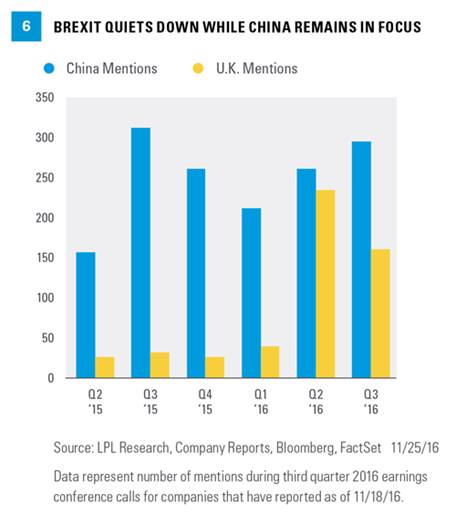

MINIMAL BREXIT DISRUPTION; CHINA STILL A FOCUS

Entering the third quarter, the U.K. was our primary geographic focus following the unexpected vote in favor of Brexit (i.e., the vote for the U.K. to leave the European Union). However, given the U.K. economy’s resilience following the vote and the stock market’s swift bounce back after the initial selloff, management teams seem comfortable with the situation. As shown in Figure 6, U.K. mentions dropped 11% in the third quarter to 119 from 134 in the second quarter.

With regard to Brexit and Europe, the message from most management teams is to acknowledge the risk but remain cautiously optimistic:

“Economic growth in Europe, it's been kind of okay, but we're still concerned about Brexit. And as that draws nearer, the concerns that we have are does it impact economic growth and business confidence and investment.” (Industrial)

“Only Europe slowed due to general economic weakness as well as the impact of the Brexit vote on the euro and the pound.” (Credit card processor)

“In Europe, we have seen a slowdown in construction activity in the U.K., we think as a result of the Brexit vote, but the rest of Europe appears to be improving slowly, more than compensating for the slowdown in the U.K.” (Industrials)

“Post the Brexit vote, we've actually seen very strong results in the UK, benefiting from the currency weakness and increased traction with the local consumer.” (Consumer apparel brand)

Meanwhile, despite relative stability in the data and markets during the third quarter, China continues to get a lot of attention. That attention is expected to increase next quarter given the focus on President-elect Donald Trump’s trade policies. The stability in China mentions is encouraging, but we are surprised they have not fallen further since the market volatility early in 2016.

Comments from executives generally suggest a supportive operating environment in China:

“On China, we actually believe that it’s going to be better than what we saw in the last quarter.” (Metals and mining)

“Volume growth of 4% was driven by increased demand in automotive markets, primarily in China.” (Chemicals)

“We grew volume in every geographic area in the quarter with notable strength in Europe, which was up 9%, and the United States and China, both up 6%.” (Chemicals)

“In China, we continue to see a solid demand, anticipate higher prices in China in the fourth quarter, and encouragingly inventories actually came down a little bit in third quarter versus the second quarter.”(Timber company)

“Our strong year-to-date results were led by record results in North America, sustained strong performance in China, and breakeven results in Europe.” (Automaker)

“Sales in China increased by 37%, as demand for our products continues to outpace end-market growth.” (Industrial)

“On the positive side, construction in China, that's been generally positive this year. And the market there has improved, and that's been good for us.” (Industrial)

CONCLUSION

Our Corporate Beige Book suggests that corporate executives have become more confident in the macroeconomic outlook. The end of the earnings recession, which coincided with drags from oil and the dollar abating, and the market’s calm reception to Brexit likely provided reassurance. We believe third quarter results were strong enough to justify the improved tone and support our expectation for mid-to-high single digit earnings growth in 2017.*

*As noted in our Midyear Outlook 2016 publication, we continue to expect mid-single-digit returns for the S&P 500 in 2016, consistent with historical mid-to-late economic cycle performance. We expect those gains to be derived from mid- to high-single-digit earnings growth over the second half of 2016, supported by steady U.S. economic growth and stability in oil prices and the U.S. dollar. A slight increase in price-to-earnings ratios (PE) above 16.6 is possible as market participants gain greater clarity on the U.S. election and the U.K.’s relationship with Europe.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Third-party quotes given may not be representative of the views of LPL Financial, and are not indicative of future performance or success. Neither LPL Financial nor LPL Financial Advisors can be held responsible for any direct or incidental loss incurred by applying any of the information offered in third-party quotes.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

Because of its narrow focus, sector investing will be subject to greater volatility than investing more broadly across many sectors and companies.

All investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The USD Index measures the performance of the U.S. dollar against a basket of foreign currencies: EUR, JPY, GBP, CAD, CHF and SEK. The U.S. Dollar Index goes up when the dollar gains “strength” compared to other currencies.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All