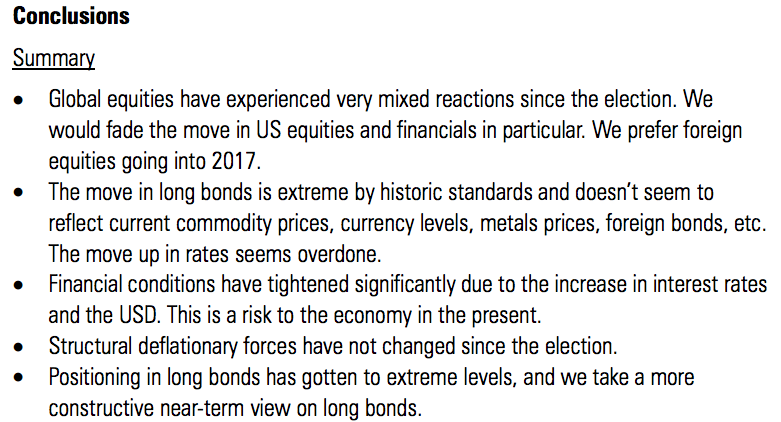

Post-Election Special Analysis

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

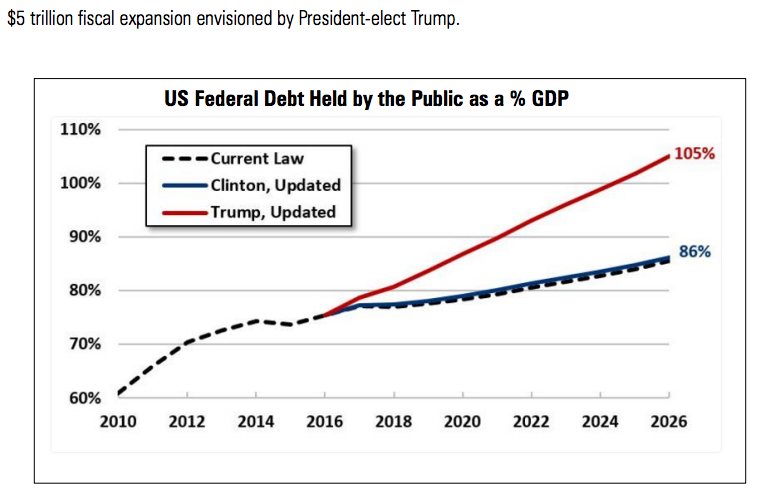

Source: Center for Responsible Federal Budget

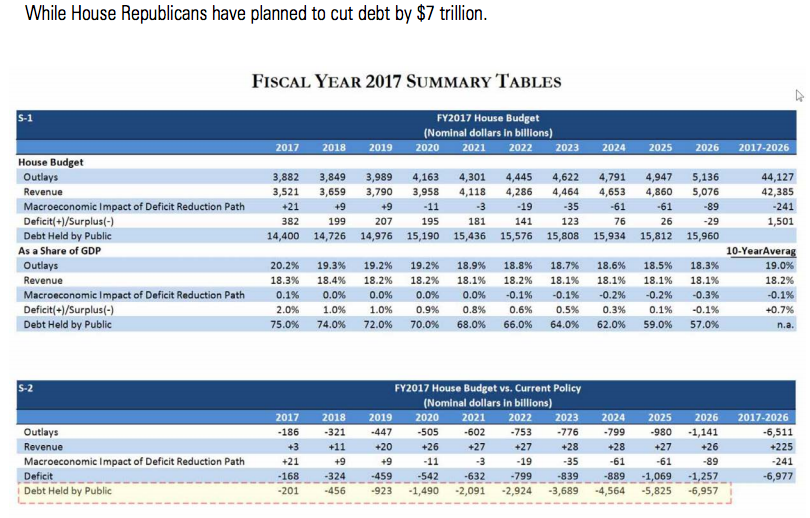

Source: House Republican Budget Blueprint.

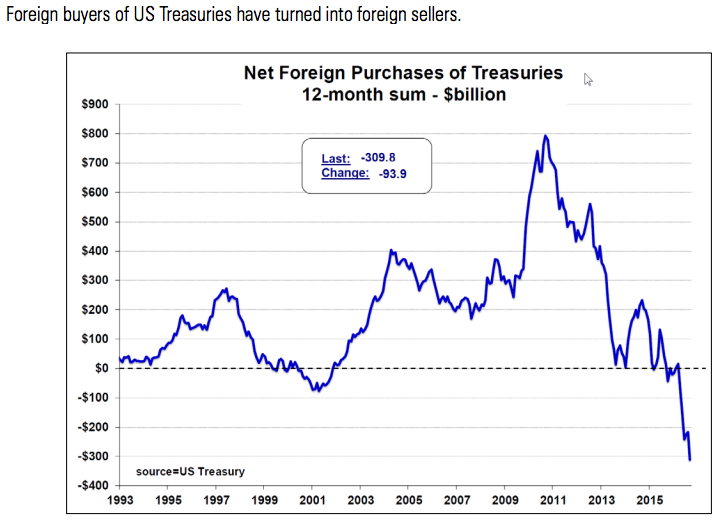

Source: MacroMavens. Data as of 11/15/16

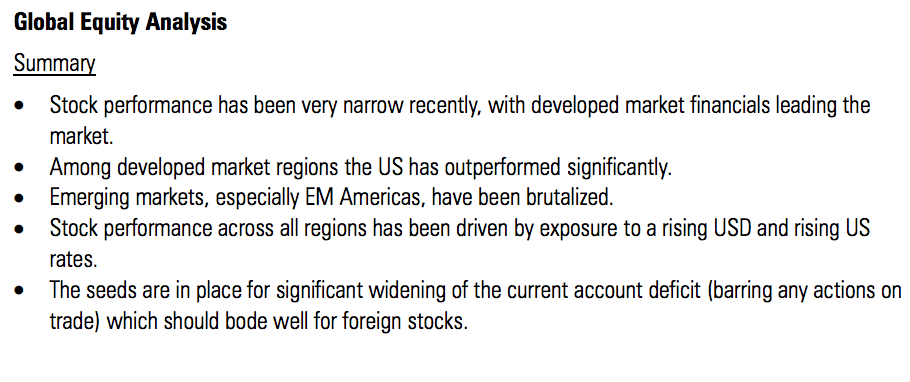

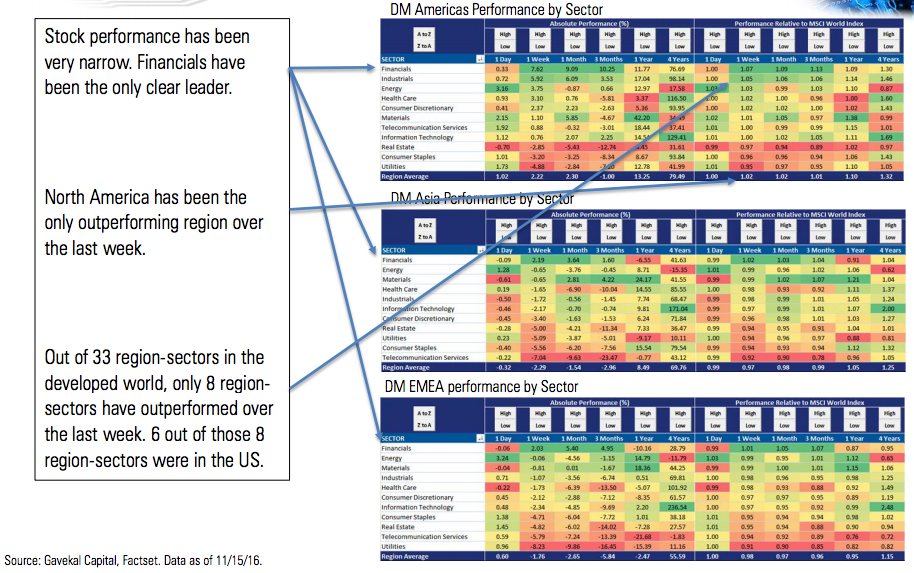

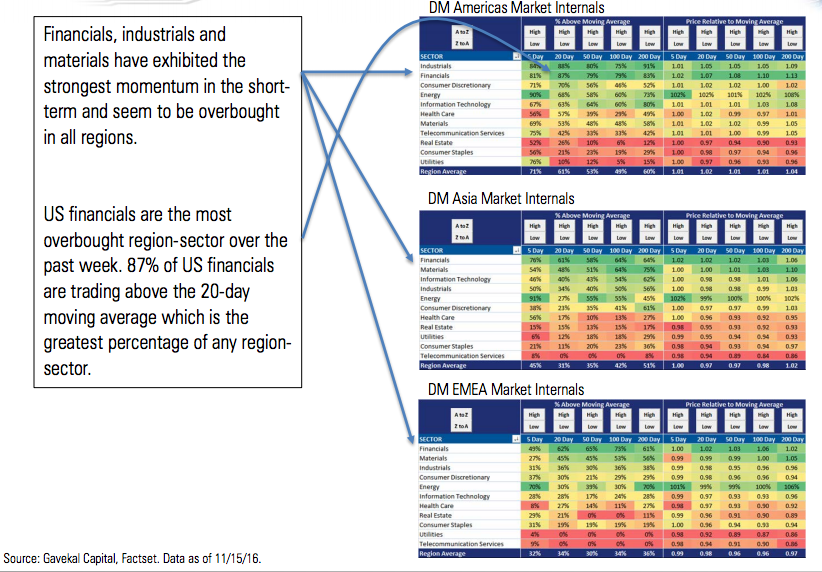

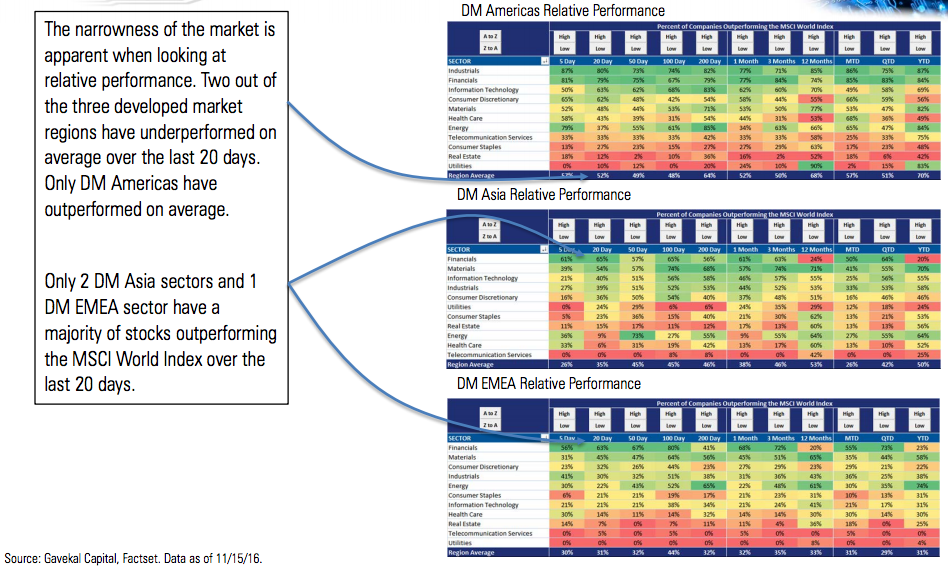

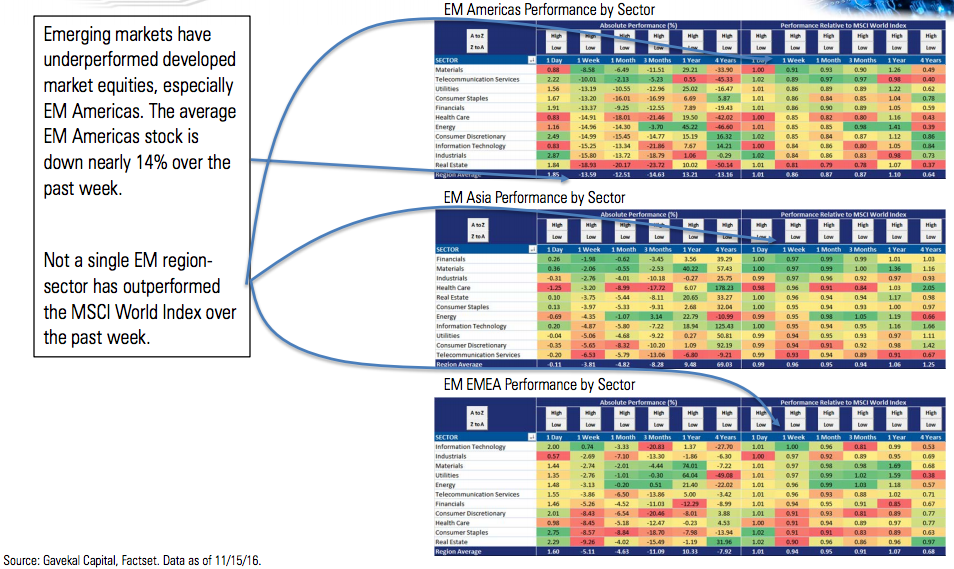

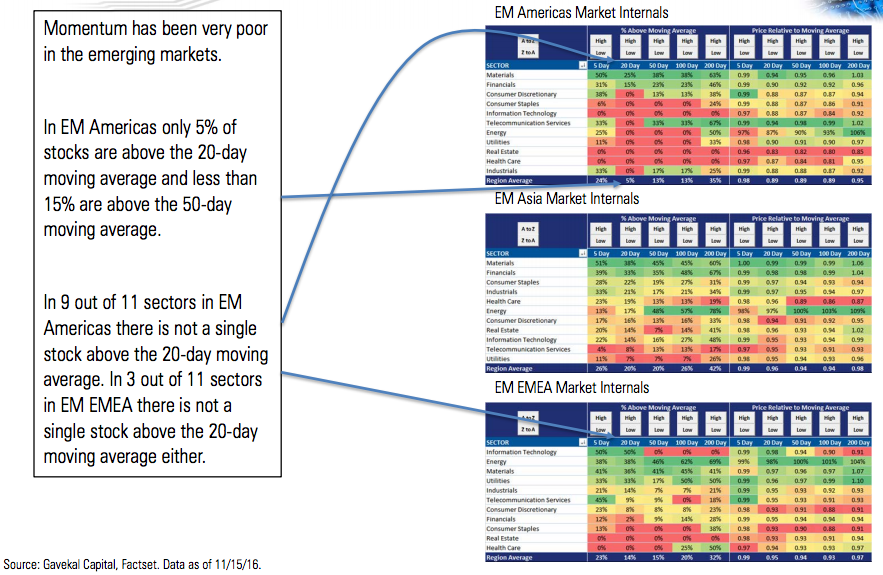

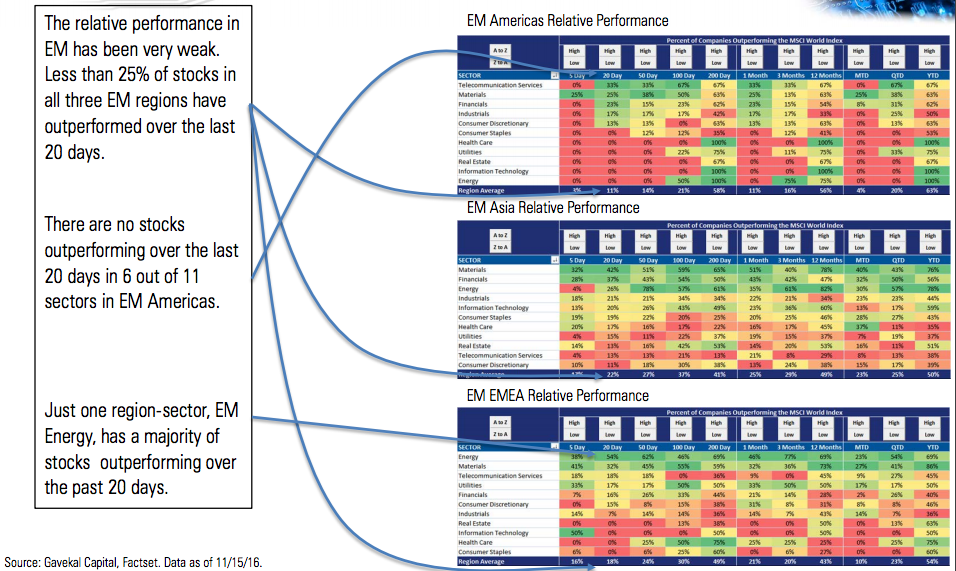

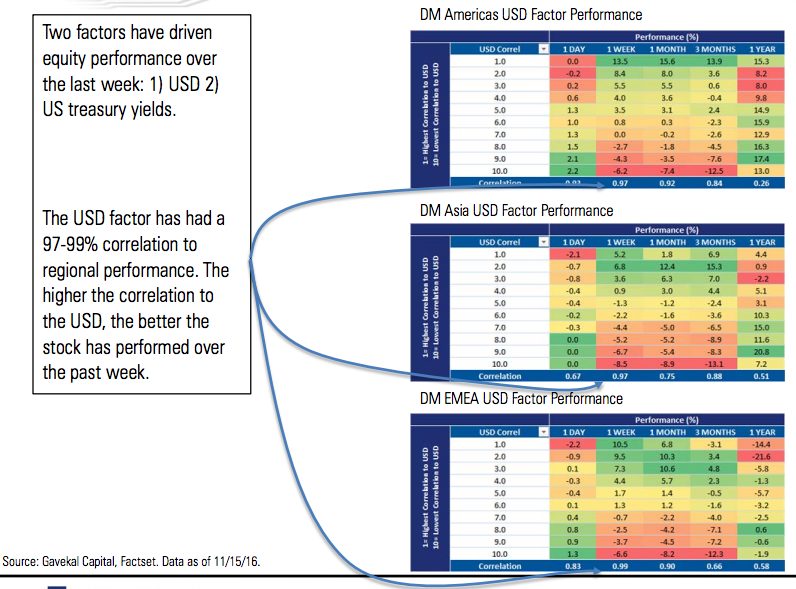

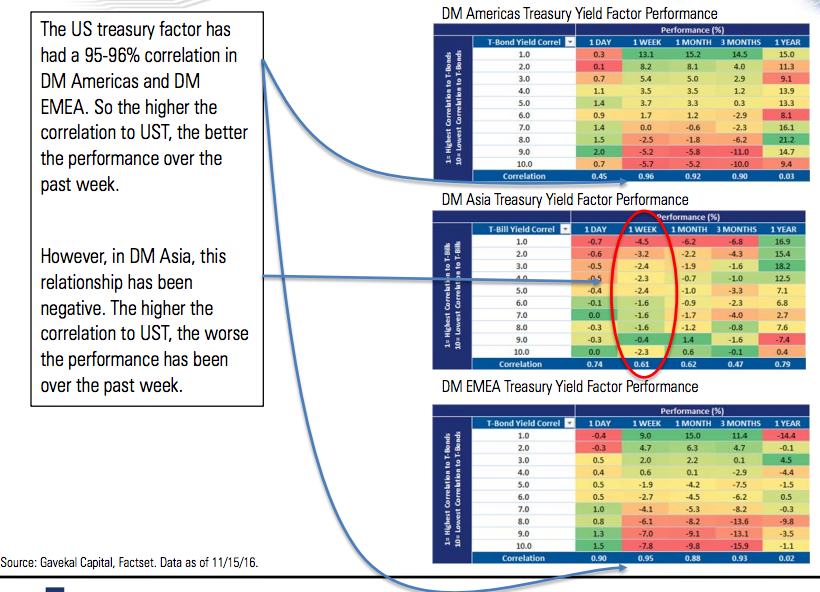

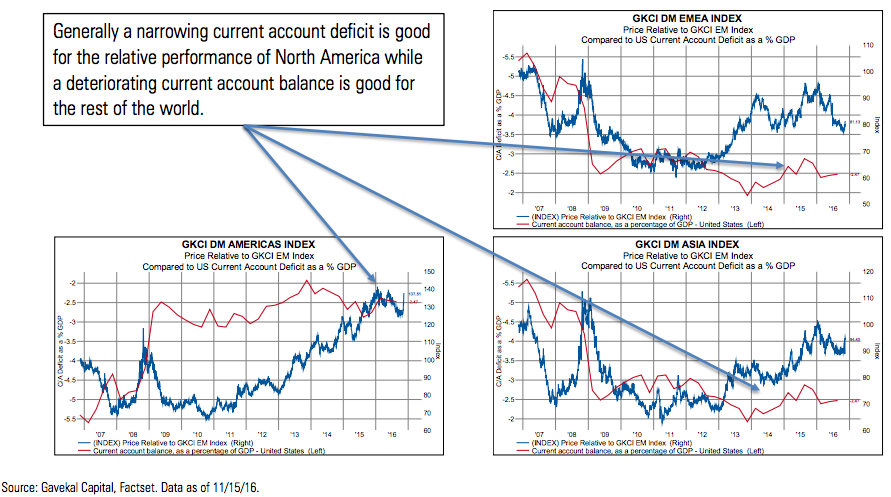

Source: Gavekal Capital, Factset

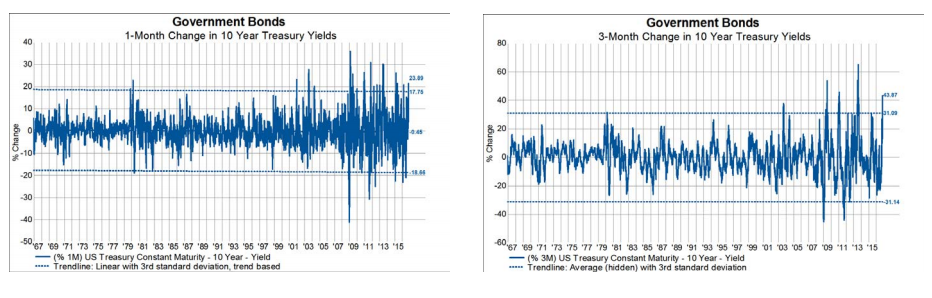

The recent volatile bond sell off is a pretty rare occurrence. The 10 Year UST has just experienced a 3 standard deviation 1 & 3 month move. There have only been 20 other times in the last 50 years that the 10 Year UST experienced a 3-standard deviation move over the past month. The 3-month change has been an even more rare occurrence. Over the past 50 years, a 3 standard deviation move has only occurred six times.

Source: Gavekal Capital, Factset. Data as of 11/15/16

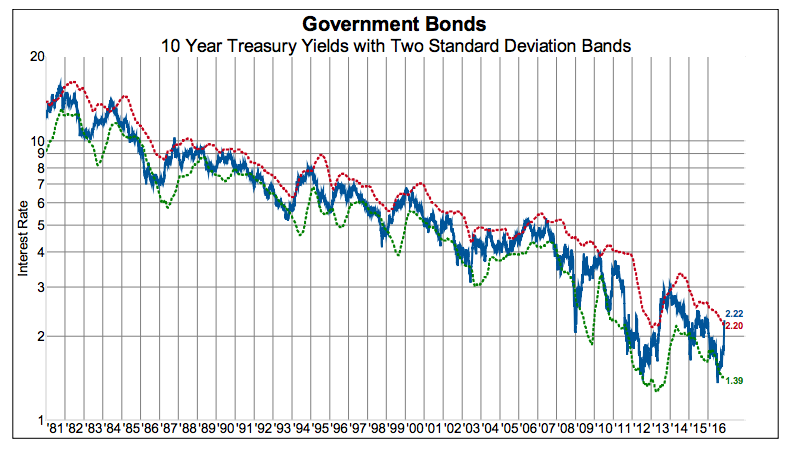

10 year yields have backed up to the 2 standard deviation band around the 1 year moving average.

Source: Gavekal Capital, Factset. Data as of 11/15/16

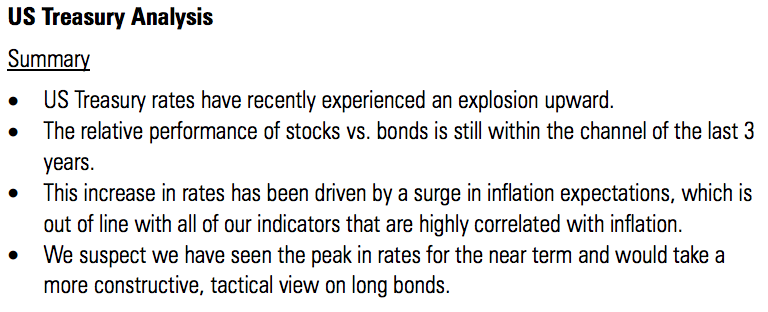

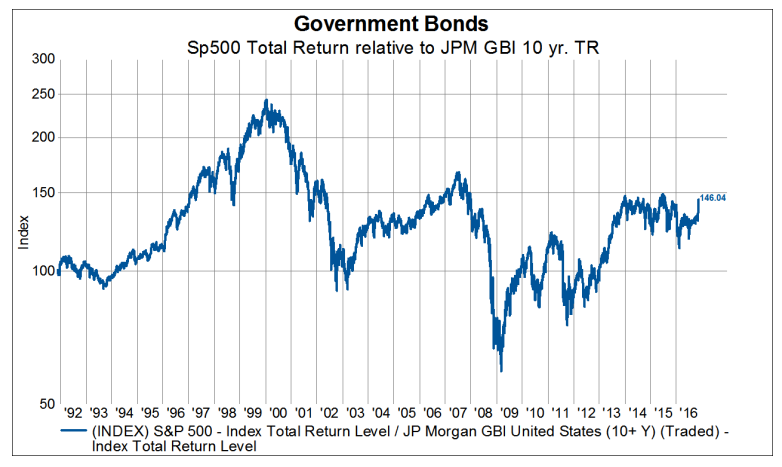

Even with the selloff, stocks have not broken out of their relative performance range compared to long bonds.

Source: Gavekal Capital, Factset. Data as of 11/15/16.

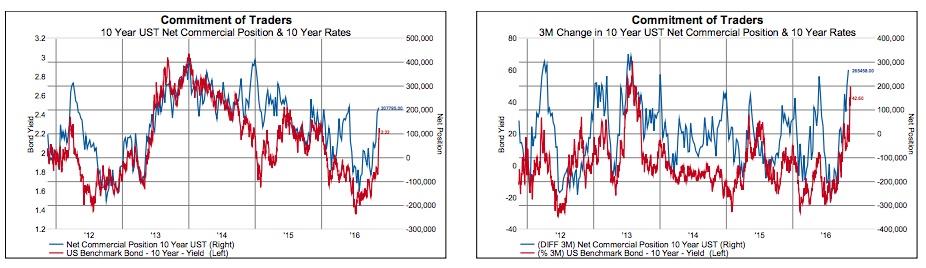

Bond positioning has gotten extreme lately, with commercial traders re-establishing long positions in US bonds. The abrupt change in positioning is reminiscent of the taper tantrum in 2013.

Source: Gavekal Capital, Factset. Data as of 11/15/16.

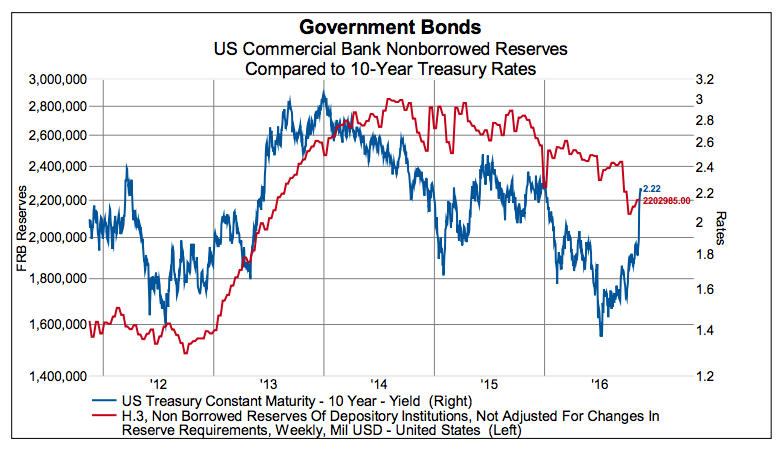

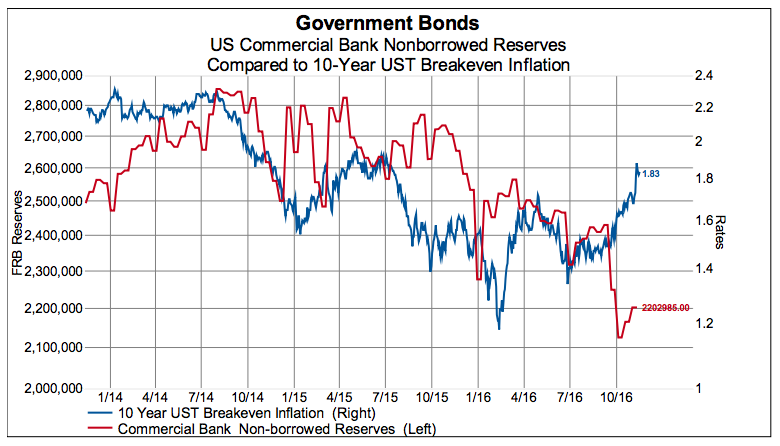

Many banking variable relationships are not confirming the selloff. For example, the correlation between UST bonds and commercial bank liquidity has broken down. Banking liquidity, which will get tighter if the Federal Reserve Bank (FRB) raises rates, should continue down.

Source: Gavekal Capital, Factset. Data as of 11/15/16

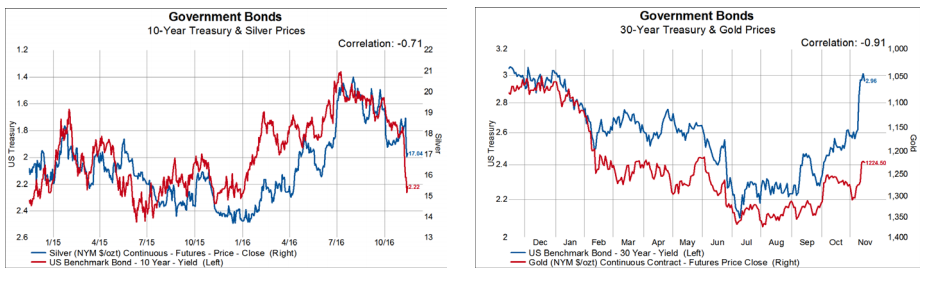

Bond yields compared to gold and silver suggest either we see a further drop in metals prices or UST rates reverse. The move in the 10-year bond suggests another 15% drop in gold prices, and the move in the 30-year bond suggests a 10% further drop in gold prices.

Source: Gavekal Capital, Factset. Data as of 11/15/16.

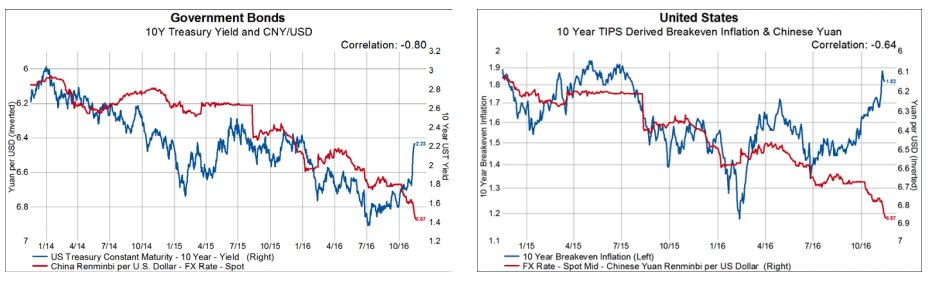

The latest move in UST is also out of sync with a depreciating Yuan. Yuan depreciation usually drives rates lower via falling inflation expectations.

Source: Gavekal Capital, Factset. Data as of 11/15/16.

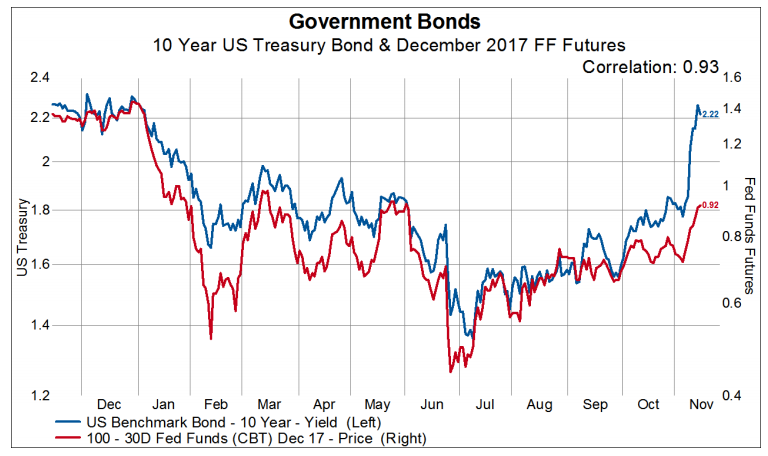

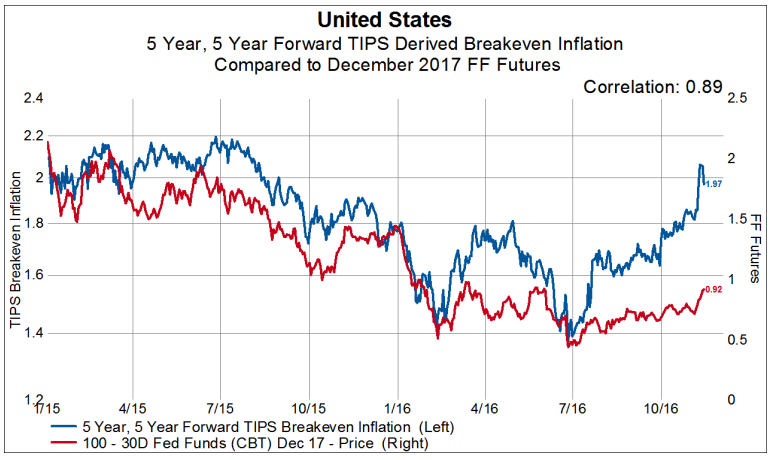

2017 federal funds futures have not matched the move up in long rates.

Source: Gavekal Capital, Factset. Data as of 11/15/16.

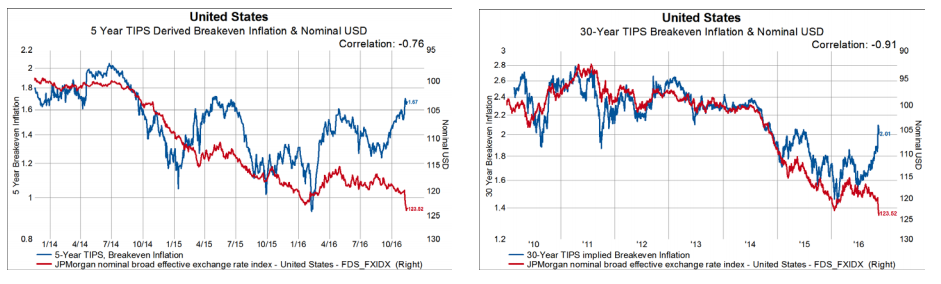

The USD is surging, which is associated with falling inflation expectations. A definitive breakout in the USD would surely put into question the logic behind rising inflation expectations.

Source: Gavekal Capital, Factset. Data as of 11/15/16

Most of the recent move in bond yields has been due to increasing inflation expectations. Falling banking reserves have been highly correlated with falling inflation expectations. If the FRB tightens in December, liquidity will contract even more.

Source: Gavekal Capital, Factset. Data as of 11/15/16.

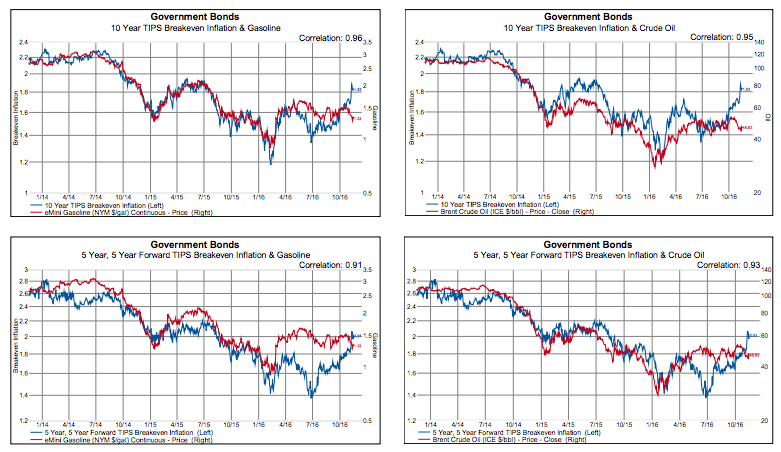

Inflation spreads are most correlated with gasoline, which along with oil, is declining.

Source: Gavekal Capital, Factset. Data as of 11/15/16

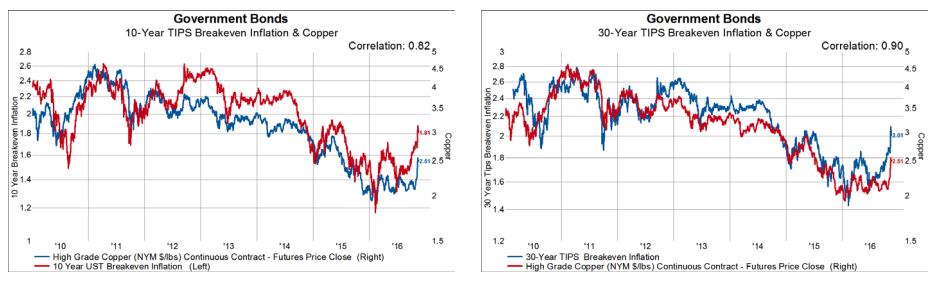

10 and 30-year breakeven inflation spreads suggest copper at $3/lb…. or lower rates.

Source: Gavekal Capital, Factset. Data as of 11/15/16.

The recent increase in inflation expectations would suggest that Fed expectations are around 100bps, too low for next year.

Source: Gavekal Capital, Factset. Data as of 11/15/16.

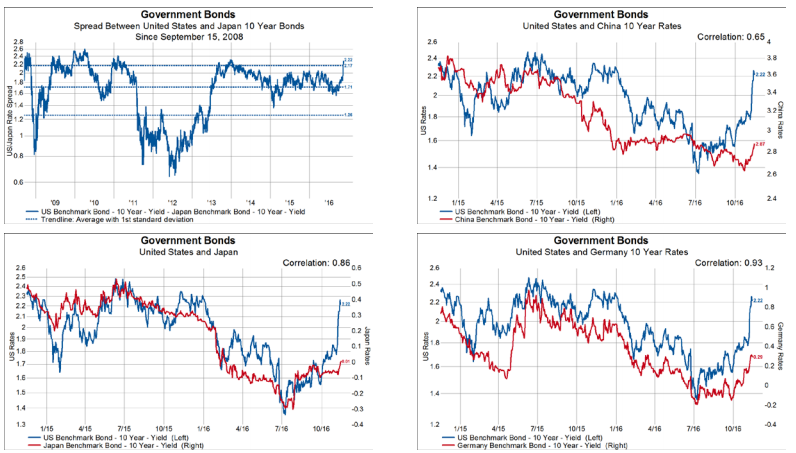

The nominal spreads between different government bonds has widened as well. The nominal spread with Japan is at a 1 standard deviation level. The recent move up in US rates suggest Japanese long rates at 40bps, China at 370bps and Germany at 90bps. Or, the US rates should move back down.

Source: Gavekal Capital, Factset. Data as of 11/15/16.

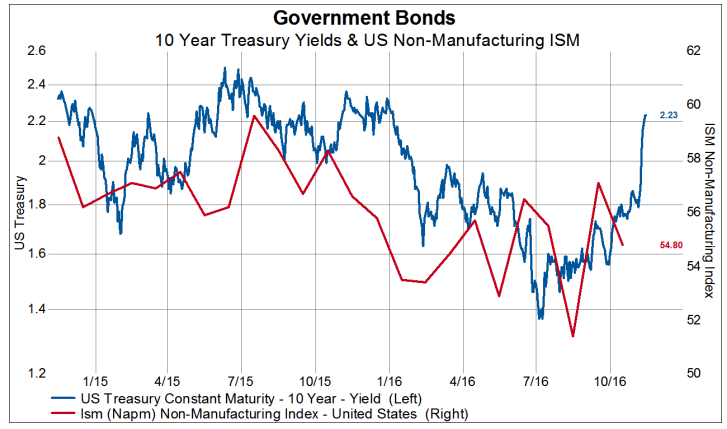

The spike in yields suggests economic data is set to surge…not a year from now, but NOW. The latest monthover-month change for the non-manufacturing ISM is down. The selloff in bonds would suggest that economic statistics increase rapidly in the next several months.

Source: Gavekal Capital, Factset. Data as of 11/15/16

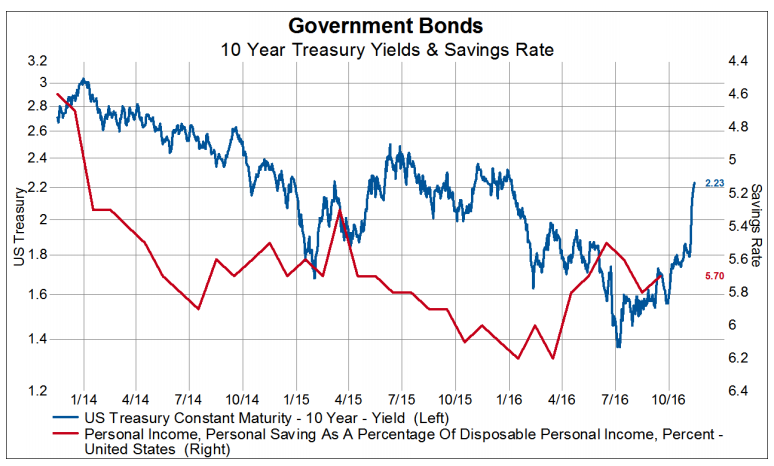

Consumers have been saving more than they did prior to the financial crisis. The spike in rates suggests this trend changes and the savings rate plunges immediately, propelling the economy.

Source: Gavekal Capital, Factset. Data as of 11/15/16.

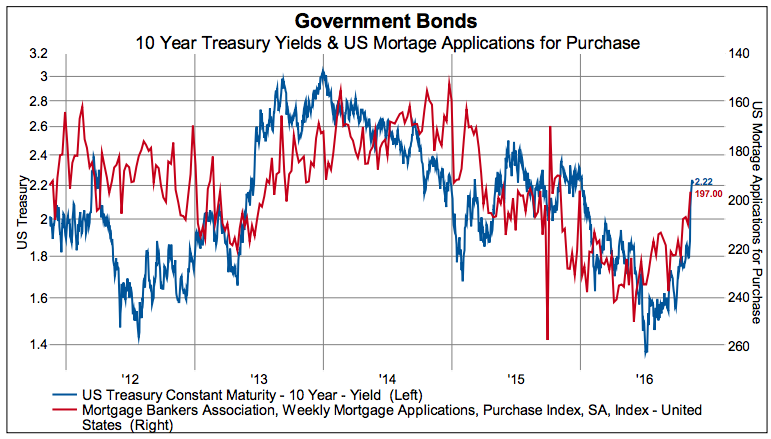

The rapid increase in rates, driven by inflation expectations is a headwind to near-term growth. The housing market should feel the effects of rising rates soon with mortgage applications down 20% since this summer.

Source: Gavekal Capital, Factset. Data as of 11/15/16.

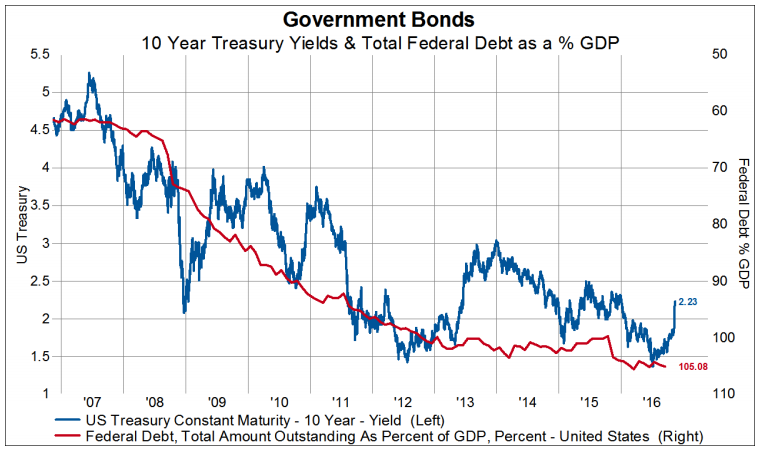

Any significantly larger than expected fiscal/debt expansion should be seen as a factor contributing to interest rate compression.

Source: Gavekal Capital, Factset. Data as of 11/15/16.

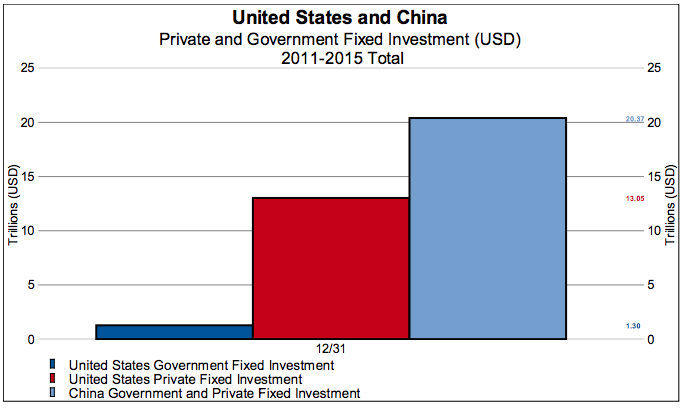

In the big picture, $1 trillion of US infrastructure spending over the next decade is a drop in the bucket compared to China. Over the last 5 years alone China has spent $20 trillion on fixed investment compared to just $1.3 trillion for the US public sector and $13 trillion for the US private sector. China will spend $52 trillion on fixed investment over the next decade even if we assume 0% growth.

Source: Gavekal Capital, Factset. Data as of 12/31/15.

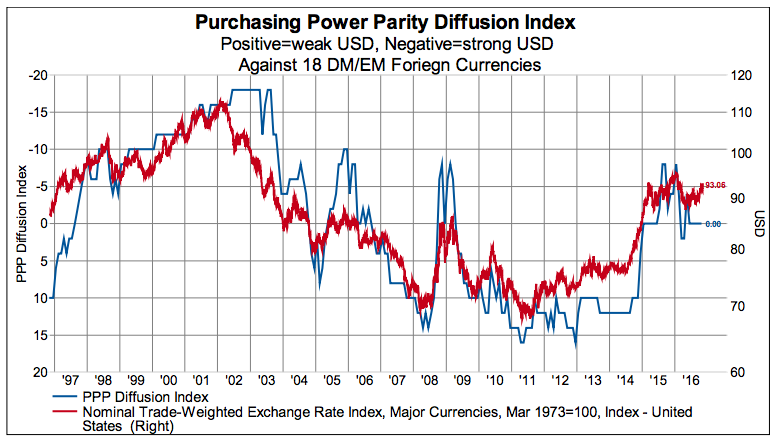

Another economic headwind could be the rising USD, which doesn’t appear over-valued across a large group of currencies.

Source: Gavekal Capital, Factset. Data as of 11/15/16.

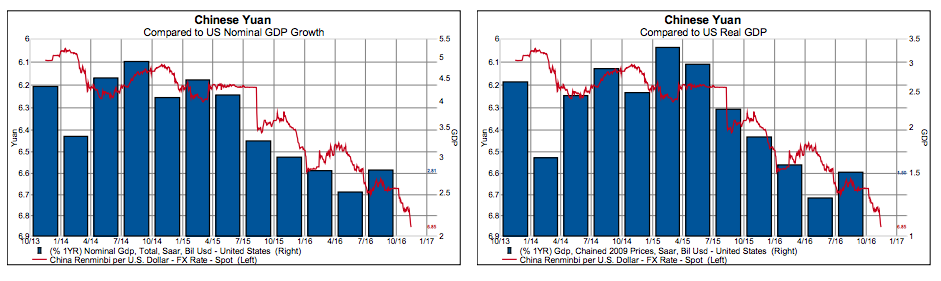

The downside break-out in the Chinese Yuan may cause US GDP growth to drop down to a still slower pace.

Source: Gavekal Capital, Factset. Data as of 11/15/16

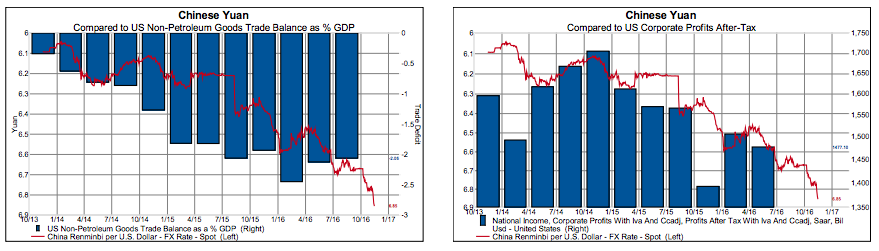

The breakdown in the Yuan could coincide with a widening of the non-oil trade deficit and a drop in corporate profits.

Source: Gavekal Capital, Factset. Data as of 11/15/16

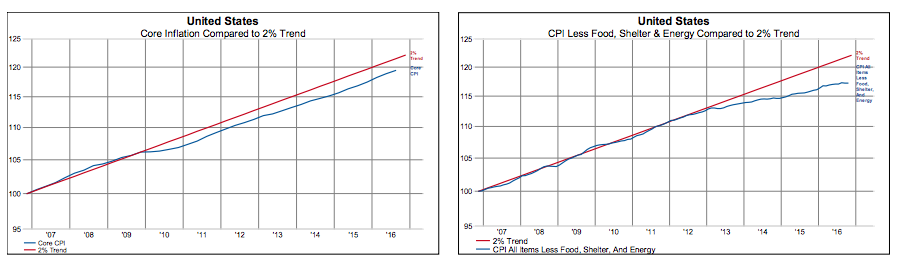

Currently, core inflation is under a 10 year 2% trend, while core inflation with shelter removed is deviating strongly from the 2% trend.

Source: Gavekal Capital, Factset. Data as of 10/31/16.

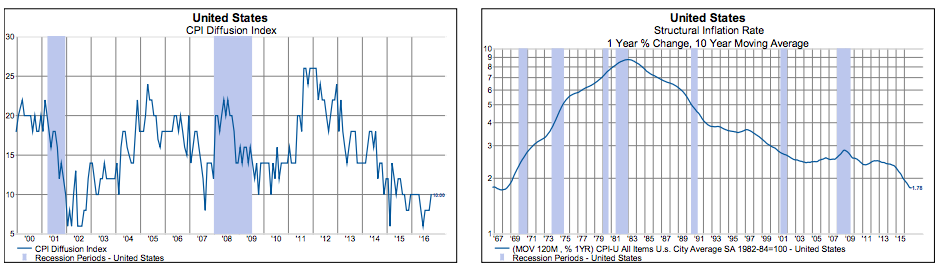

Our diffusion index of the CPI components is near recessionary lows. Our measure of structural inflation is still in a clear downward trend.

Source: Gavekal Capital, Factset. Data as of 10/31/16.

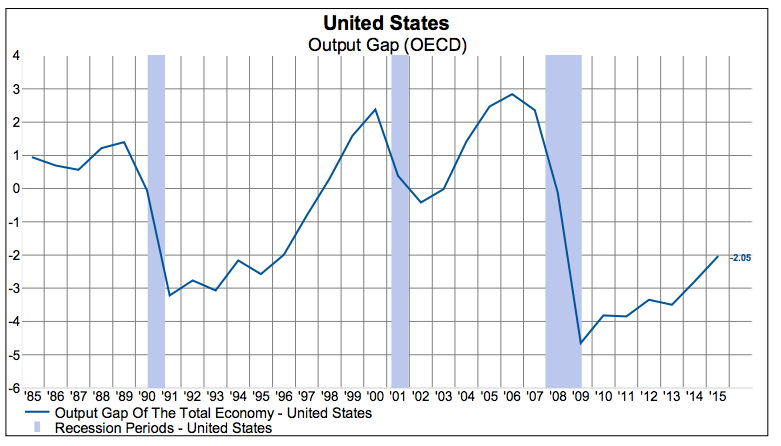

By most measures there is still a measurable output gap in the US, again suggesting inflation is not a here and now problem.

Source: Gavekal Capital, Factset. Data as of 12/31/15

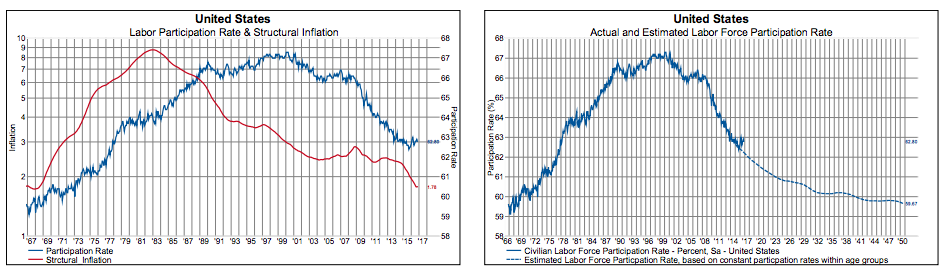

Demographics suggest a powerful deflationary force is in place for the next couple decades.

Source: Gavekal Capital, Factset. Data as of 10/31/16.

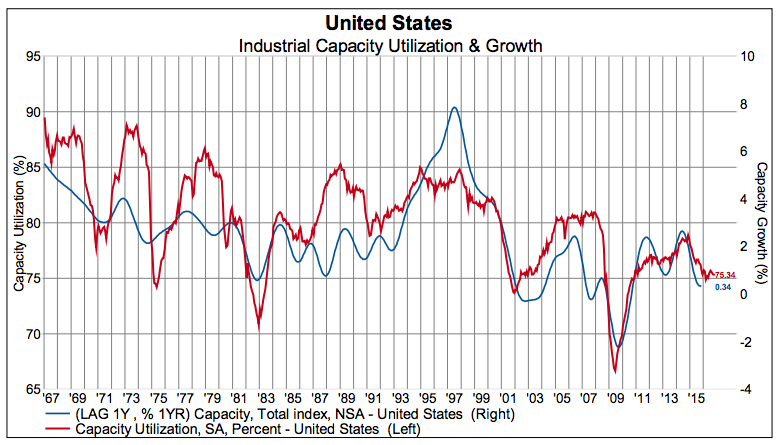

Industrial capacity utilization is 5% below the rate which has historically spurred capacity growth.

Source: Gavekal Capital, Factset. Data as of 10/31/16.

![]()

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits