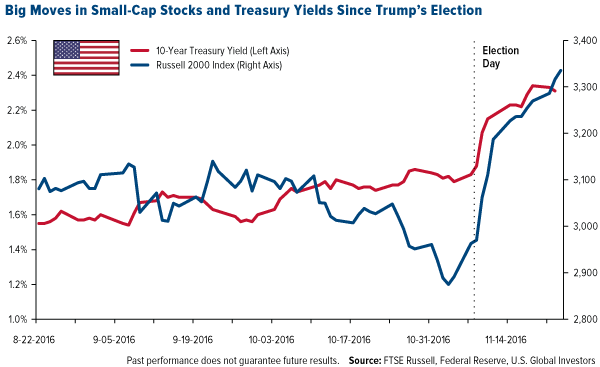

In a Frank Talk this week, I discussed the surge in small-cap stocks since Donald Trump’s election. A bet on smaller domestic stocks, I wrote, is a bet that Trump will deliver on his promise to “make America great again.” He plans to lower taxes, streamline regulations and spend big on infrastructure—all of which has led to a rally in the small-cap Russell 2000 Index and the 10-Year Treasury yield.

The ramifications of government policy change under Trump, especially fiscal policy, have the potential to be huge. Since Election Day, we’ve seen the strong U.S. dollar hurt gold, while the Canadian dollar and Chinese renminbi have dropped.

The question now is whether Federal Reserve Chair Janet Yellen will put the brakes on the so-called Trump rally. She asserts that Fed policy is not politically motivated, but I wonder how many people actually believe that. She’s already criticized Trump’s plans to tear up or at least significantly weaken Dodd-Frank Wall Street Reform.

Both former Fed Chair Alan Greenspan and billionaire investor Warren Buffett have recently suggested Dodd-Frank needs to go, with Greenspan telling CNBC that he’d love to see the 2010 law “disappear.” Buffett, meanwhile, commented in an interview this month that the U.S. is “less well equipped to handle a financial crisis today than we were in 2008. Dodd-Frank has taken away the Federal Reserve’s ability to act in a crisis.”

|

Since the election, banks have seen strong inflows, as investors are betting that the financial industry could be one of the largest beneficiaries of Trump’s administration.

According to Evercore ISI analyst Glenn Schorr, “Animal spirits and higher confidence have returned, and investors are now expecting a better revenue, expense, tax, capital and regulatory profile for financials.” In addition, “we might have just flipped from feeling pretty late cycle right back to early cycle depending on how much we want to buy into Trump’s pro-growth agenda.”

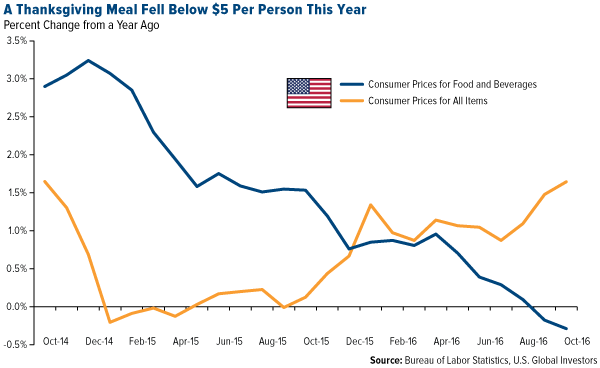

Americans Take Advantage of Low Inflation

Last year, lower gas prices helped American households save $700 on average. Although savings aren’t likely to be as much this year, Americans managed to save in other ways—namely, food and beverages.

According to the American Farm Bureau Federation (AFBF), the cost of a typical Thanksgiving meal for 10—consisting of a turkey, stuffing, sweet potatoes, cranberries, a pumpkin pie and other traditional sides—fell 24 cents from last year’s average to $49.87. That translates to a per-person cost of just under $5, confirming that “U.S. consumers benefit from an abundant high-quality and affordable food supply,” says AFBF Director of Market Intelligence Dr. John Newton.

As I’ve said multiple times before, the U.S. shale oil boom helped deliver an “oil peace dividend” to the world, which drove transportation costs and, therefore, food and beverage costs down over the past two years.

Low fuel costs have also encouraged a huge number of families to hit the highway this Thanksgiving weekend. According to AAA, roughly 50 million people—about 1 million more than last year—will journey 50 or more miles from their homes, the most since 2007.

With gas prices at the second lowest in a decade, driving remains the most popular mode of transportation. But as I shared with you last week, flying has also become more and more affordable for many Americans. This week, an estimated 27 million passengers flew on U.S. airlines, an increase of 2.5 percent over last year.

Black Friday Is the New Cyber Monday

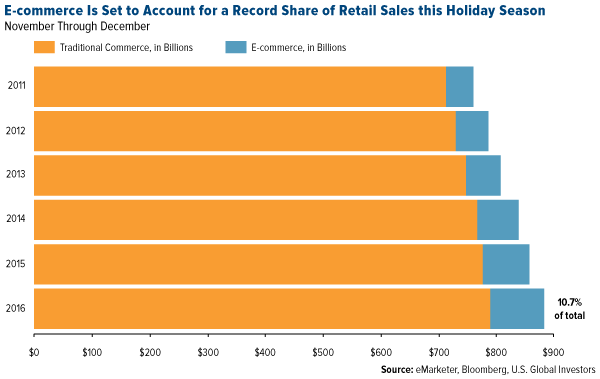

It isn’t just travel that’s back to pre-recession levels. This year, it appears more Americans than ever before—enjoying low inflation and rising wages—will be spending their savings on gifts for friends and family, if estimates from the National Retail Federation (NRF) are accurate.

According to the retail trade association, as many as 137.4 million consumers plan to shop this Thanksgiving weekend, up a whopping 60 percent from last year’s 135.8 million people. This includes both in-store shopping as well as online shopping, which, as you might have noticed, is becoming a huge deal.

Black Friday remains the busiest shopping day, with 74 percent of consumers telling the NRF they plan to venture out into the crowds to take advantage of gotta-have-it bargains.

But e-commerce is quickly catching up, with the internet-only Cyber Monday second in sales to Black Friday. For the first time this holiday season, online purchases are expected to account for more than 10 percent of all retail sales, according to consumer research firm eMarketer. “Online sales,” reports Bloomberg, “are likely to climb to $94.7 billion, representing almost 11 percent of total sales in November and December, an all-time high.”

The growing popularity of online shopping has prompted more and more brick-and-mortar retailers to push their e-commerce sales earlier to Black Friday and even Thanksgiving Day. In years past, retailers waited until Cyber Monday to post digital discounts, but today they risk losing market share among shoppers who increasingly prefer making purchases off their laptop and smartphone.

One of these retailers is Walmart, which will start offering online sales two days in advance, in a bid to stay ahead of competitor Amazon. In a press release, the Arkansas-based behemoth announced it has tripled its assortment of online products, from 8 million last year to more than 23 million today.

Another Record Year for Packages Delivered

The rise in e-commerce has had the inevitable effect of giving more business to ground and air delivery companies such as FedEx and United Parcel Service (UPS). It’s expected that, with online sales jumping 17 percent this year, the number of packages handled and shipped will jump to a record high.

According to Business Insider, UPS—the world’s largest delivery company—projects it will ship a record-setting 700 million packages between Thanksgiving and Christmas, or 70 million more than the same time last year. FedEx hopes it can ship 10 percent more than the 325 million it delivered last year.

Meanwhile, Amazon’s plans to establish its own in-house transportation network have hit a setback. About 250 pilots contracted with Amazon partners Air Transport Service Group and Atlas Air Worldwide Holdings went on strike Tuesday over a “longstanding labor dispute.” The Jeff Bezos-run retailer has been determined to deliver its own products after bad weather in 2013 delayed millions of Christmas deliveries, but it appears these efforts are off to a rough start.

Wishing You Health, Wealth and Happiness!

I wish to conclude by giving thanks to our loyal Investor Alert readers as well as investors. Visit us on Facebook or Twitter and let us know what you’re thankful for this season!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 1.51 percent. The S&P 500 Stock Index rose 1.44 percent, while the Nasdaq Composite climbed 1.45 percent. The Russell 2000 small capitalization index gained 2.40 percent this week.

- The Hang Seng Composite gained 1.57 percent this week; while Taiwan was up 1.67 percent and the KOSPI fell 0.01 percent.

- The 10-year Treasury bond yield fell slightly to 2.35 percent.

Domestic Equity Market

Strengths

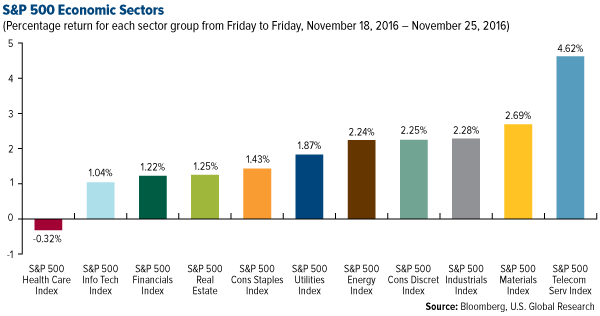

- Telecommunications was the best performing sector for the week, increasing by 4.62 percent, compared to an overall increase of 1.4 percent for the S&P 500 Index.

- Freeport-McMoRan was the best performing stock for the week, increasing 16.53 percent.

- Deere & Co’s stock skyrocketed after the company forecasted 2017 profit that exceeds analysts’ estimates, buoyed by cost cuts amid the longest slump for farmer incomes in decades.

Weaknesses

- Health care was the worst performing sector for the week, falling by 0.32 percent, compared to an overall increase of 1.4 percent for the S&P 500.

- Patterson was the worst performing stock for the week, falling 16.0 percent.

- Tyson Foods tumbled after whiffing on earnings. The stock fell 14.5 percent in trading on Monday after the company posted earnings of $0.96 per share. Analysts had projected earnings of $1.16 per share. Additionally, the firm announced that CEO Donnie Smith would be succeeded by Tom Hayes at the end of the year.

Opportunities

- Amazon is in talks to start streaming sports on Prime. Amazon is in talks with several organizations, including the NFL, NBA and MLB, to start a "premium" sports package that will be streamed on Prime, The Wall Street Journal reports.

- Symantec is buying security firm LifeLock for $2.3 billion. The deal will be funded by cash and new debt. Symantec also bought internet security firm Blue Coat for $4.7 billion in June.

- Facebook is buying back stock. The social media giant announced a $6 billion share buyback program that will begin in the first quarter of 2017 and is consistent with what the company says is its "capital allocation strategy of prioritizing investment to grow the business over the long term."

Threats

- Analysts are starting to worry about Apple's future profitability. Apple's gross margin on the iPhone has slid from 57.7 percent in 2009 to 41 percent today, and it is expected to fall to 39 percent in 2018, according to Toni Sacconaghi at Bernstein Research.

- U.S. dollar strength, weakening emerging market demand and declining capital expenditures have prompted BCA’s U.S. equity strategists to move the S&P industrials sector to their high-conviction underweight list.

- Amazon faces potential holiday shipping disaster as pilots go on strike. A pilot strike is threatening to ground flights carrying cargo for Amazon during the busy holiday season. About 250 pilots employed by ABX Air, a subsidiary of Air Transport Services Group, went on strike Tuesday morning to protest what they say are staffing shortages. Now Amazon and shipping company DHL Worldwide Express, which are both customers of ABX, will have to pay the price. This could cause major disruptions and delays for some Amazon customers during the busy holiday season, according to the union representing the pilots.

![[thumb]](/images/content_image/data/35/35a3c716373dbda5bfbf606dadac97dd.jpg)

November 23, 2016Small-Cap Investors See Big League Growth Under Trump |

![[thumb]](/images/content_image/data/00/003dfe71a8a5a29ba886aba23f739510.jpg)

November 21, 2016Surprise! Buffett Books a Flight on Airline Stocks |

![[thumb]](/images/content_image/data/dd/dd67d57c7d2a93f38d7f6ad8fc60cc5f.jpg)

November 16, 2016Muni Bonds a Key to Making America Great Again |

The Economy and Bond Market

Strengths

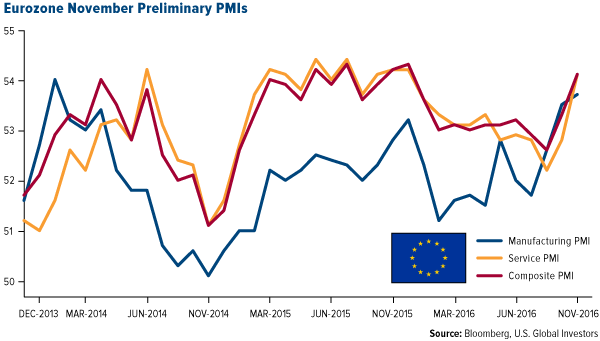

- The preliminary Markit U.S. Manufacturing purchasing managers’ index (PMI) for November came in at 53.9 versus the expected 53.5. That anticipates strength in manufacturing over the next months.

- Preliminary durable goods orders for October posted 4.8 percent growth, much higher than the expected 1.7 percent. That is a positive sign for the manufacturing sector.

- The University of Michigan Sentiment Survey for November came in at 93.8, above the expected 91.6, reflecting consumer confidence in the economy.

Weaknesses

- The past week has been brutal for bond funds. Investors ditched bonds at the fastest weekly rate since 2013, according to analysts from Deutsche Bank, on fears high interest rates and inflation will make a return.

- New home sales for October disappointed, coming in at 563,000 versus the expected 590,000.

- Dollar strength makes U.S. companies less competitive, but they will also be selling into weaker demand growth abroad. Just under half of S&P 500 sales come from abroad.

Opportunities

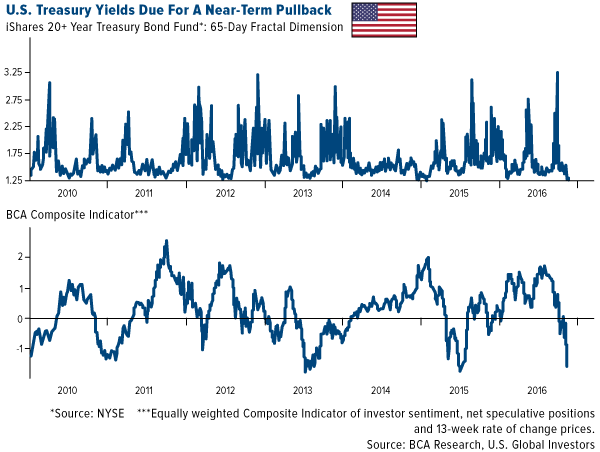

- BCA’s bond strategist believes it is likely that Treasury yields will at least level-off, and perhaps decline a bit, during the next month. First, technical measures and positioning data suggest that the rapid rise in yields is due for a pause. The fractal dimension for long-maturity Treasuries, a measure of groupthink currently sits at 1.25, a level at which a trend reversal - even if only a temporary one - tends to emerge. Additionally, BCA’s composite sentiment indicator, based on the 13-week rate of change in prices, investor sentiment, and net speculative positions, is deeply oversold, highlighting the risk of a near-term reversal.

- In the wake of Donald Trump’s victory, much has been made about the stunning selloff in the U.S. bond market. There’s always a silver lining though. Pension funds, which for years have struggled to keep up with their obligations as yields plumbed to new lows, are now in line for a reprieve as interest rates increase. Savers may finally see the interest they get from Treasuries rise after more than a decade of declines. And for banks, higher yields could also mean billions in extra income.

- The Wall Street Journal called Rhode Island “An Island of Rationality in Blue-State New England” in a recent article. According to the article, “the reforms Governor Raimondo championed in 2011 were, and still are, revolutionary. They shifted future as well as current workers to hybrid retirement plans with a defined-benefit component. The retirement age was increased while cost-of-living adjustments were suspended, slashing the state’s unfunded liability by nearly half.” More states with huge unfunded pensions should take notice.

Threats

- According to Business Insider’s Josh Barro, there’s a problem with the conventional wisdom you’re hearing about a Trump economic stimulus. The American economy is approaching full employment. Interest rates remain low, but they have risen sharply since Trump's election: The 10-year Treasury bond yield has gone from 1.86 percent on Election Day to over 2.30 percent recently. Because of limited slack in the economy, a large fiscal stimulus today could actually have the effects that conservatives incorrectly warned of in 2009: higher government borrowing costs, a crowding out of useful private-sector projects due to higher interest rates, and inflation.

- Paul Krugman, the Nobel-winning economist and New York Times columnist, once again expressed his discontent with the future Donald Trump administration. Krugman decried the possibility of corruption within the Trump administration, particularly in regard to Trump's massive proposed infrastructure plan and foreign policy. He stated, “We’re about to enter, or may already have entered, an era of corrupt governance unprecedented in U.S. history.”

- The housing market is suddenly losing one of its biggest drivers. Mortgage rates have recently surged. A recent report from the Mortgage Bankers Association showed that purchase and refinancing applications fell to the lowest level since January. The index that measures this activity fell 9.2 percent in the week ended November 11. Low mortgage rates after the 2008 housing crash made the dream of owning a home a reality for many. But if the trend of the last two weeks continues, higher rates could have ripple effects across the housing market.

Gold Market

This week spot gold closed at $1,184.24, down $23.69 per ounce, or 1.96 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week down by 2.51 percent. Junior miners outperformed seniors for the week, as the S&P/TSX Venture Index fell 1.83 percent. The U.S. Trade-Weighted Dollar Index gained 0.22 percent for the week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Nov-23 | U.S. Durable Goods Orders | 1.7% | 4.8% | 0.4% |

| Nov-23 | U.S. Initial Jobless Claims | 250k | 251k | 233k |

| Nov-23 | U.S. New Home Sales | 590k | 563k | 574k |

| Nov-24 | H.K. Exports YoY | 1.8% | -1.8% | 3.6% |

| Nov-29 | Germany CPI YoY | 0.8% | -- | 0.8% |

| Nov-29 | U.S. GDP QoQ | 3.0% | -- | 2.9% |

| Nov-29 | U.S. Consumer Confidence Index | 101.3 | -- | 98.6 |

| Nov-30 | Eurozone CPI Core YoY | 0.8% | -- | 0.8% |

| Nov-30 | U.S. ADP Employment Change | 160k | -- | 147k |

| Nov-30 | Caixin China PMI Mfg | 50.8 | -- | 51.2 |

| Dec-1 | U.S. Initial Jobless Claims | 253k | -- | 251k |

| Dec-1 | U.S. ISM Manufacturing | 52.1 | -- | 51.9 |

| Dec-2 | U.S. Change in Nonfarm Payrolls | 175k | -- | 161k |

Strengths

- The best performing precious metal for the week was palladium, up 2.83 percent. China boasted imports of silver, platinum and palladium in October. In addition, vehicle sales in Europe are up 4.7 percent through October in 2016 versus a year ago. Global auto sales are tracking at over 3 percent, recovering from sub-2 percent growth in 2015.

- With worries over a supply shortage due to Beijing’s efforts to restrict import licenses, gold premiums in China jumped to their highest in nearly three years this week, reports the Business Standard. One analyst with GFMS, Zhirui Ji, says potential restrictions on gold imports may have to do with limiting the outflows of the Chinese yuan, which touched an eight-and-a-half year low this week.

- Swiss gold exports rose to 162.6 tons in October, reports Bloomberg, up from 147.4 tons in September. Shipments to India and Hong Kong also rose, while exports to China fell during the month. In Russia, October gold buying has reached the largest in a millennium, reports Zero Hedge. Commerzbank explains this humongous gold purchase as follows: “Clearly the central bank was taking advantage of the stronger ruble—which has made gold cheaper in local currency—to buy more gold.

Weaknesses

- The worst performing precious metal for the week was gold. Through Friday, Bloomberg reports that investors pulled out more than $1 billion from the biggest ETF backed by gold since the end of October. Holdings in ETFs are heading for the biggest monthly drop in nearly three years as the Federal Reserve prepares to hike interest rates. While gold has collapsed in November, “cheaper haven silver entered a bear market,” writes Bloomberg, as investors embrace risk on the back of Donald Trump’s pledge to increase infrastructure spending.

- Credit Suisse’s Andrew Garthwaite says investors should consider a long-short play, being overweight Japan and underweight gold. Calls like this present a headwind for gold as some hedge funds will use shorting gold as a source to go long other assets.

- UBS says the downside for gold from here should now be “relatively contained,” noting that with the Thanksgiving holidays, it’s difficult to read too much into price action. Further pressure still exists, however, especially with ETF liquidations persisting and December’s Federal Open Market Committee (FOMC) meeting right around the corner.

Opportunities

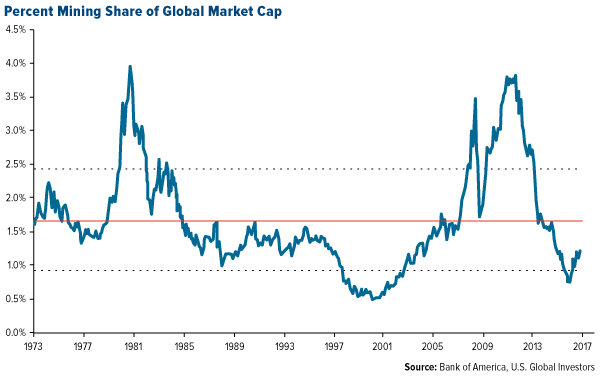

- Macquarie Research elevated Rye Patch Gold to “Top Pick” status, after the company provided a positive construction update with key de-risking data points related to the re-start of its flagship Florida Canyon Mine (FCM) in Nevada, reports Macquarie. Rye Patch is set to be a new 70,000 ounce producer in 2017 via open-put head leach and trades at around 0.3 times price to net asset value (NAV)—a 60 percent discount to peer producers. Macquarie has a 12-month target of C$0.65, which implies close to a potential 200 percent gain in the coming year. While some may say the bull market in mining stock is over, the chart below shows that mining shares as a percent of global market cap is still fairly depressed.

- The Commerce Department’s personal consumption expenditures measure (the Fed’s preferred gauge to inflation), hasn’t matched the central bank’s 2 percent goal since April 2012, reports Bloomberg. And while gold has been dropping for two months, other commodities have surged in moves “that may feed through to faster inflation,” the article continues, with copper jumping to its highest level since June 2015. David Lennox, a resource analyst at Fat Prophets in Sydney, notes that the expected rate hike in December and a significant spending program in the U.S. could “create inflation.”

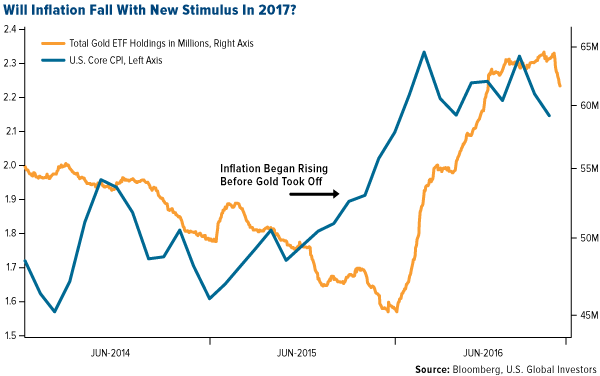

- With new stimulus planned for 2017, the chart below poses a good question, particularly for gold investors: Will inflation recede? One can observe in the chart that investors only started accumulating physical gold via exchange-traded funds about six months after inflation started to lift. With new infrastructure spending plans construction inputs such as copper has jumped, is it likely inflation is going to recede from historic lows? The upcoming interest rate hike may be an opportunity to add to gold and gold stocks going into year end.

Threats

- Dundee Capital Markets reported on its recent attendance of a review of resource estimation, and what red flags to be aware of. One of the key takeaways was that among the 100-plus NI43-101 resource estimates published each year, there are occasionally rare situations of poor practices that can yield economic failures. Another takeaway dealt with accuracy of the resource estimation, which in the context of economics is generally low—one calculated within 10 percent accuracy is considered “good.” Some of the red flags that Dundee noted, which investors should be aware of, include: 1) high capping levels can skew grade upwards, 2) ignoring un-sampled intervals may cause smearing, and 3) utilizing incorrect (or no) boundaries can generate non-representative resources.

- The Indian Bullion & Jewellers Association (IBJA) informed its 2,500 members that the Indian government was hearing proposals on a possible ban on gold imports this week, reports Cryptocoins News. “We hear from certain circles of this possibility, although nothing official is out yet,” Surendra Mehta, national secretary of the IBJA said. The government also wants information held by the nation’s jewelers. “Already, 600 jewelers have received notices from the tax department to disclosure their sales till November 8,” Mehta said. If gold is less available to Indians, this spells good news for India Bitcoin demand. In a parallel vein, Goldcore reported that Citibank will make all Australian branches cashless, and UBS proposes that Australia eliminate $100 and $50 bills.

- According to the Washington Post, giant eagles are terrorizing the surveying work done by an Australian gold mine. An unmanned aerial vehicle (UAV), or drone, is one piece of technology that surveyors at the St. Ives Gold Mine in Australia use as part of the mapping and gold production process. The wedge-tailed eagle has cost mining companies a hefty price. Since the drone program began, the birds have swooped down and taken out nine of their 10 UAVs, each of which costs $9,500, in addition to carrying a $10,000 camera. The birds are not likely anti-mining but may just be trying to defend their territory from other perceived predators. In this video link, you can watch one of the eagles attack a drone as it snaps a picture of a second eagle, perhaps capturing the “first recorded eagle selfie in history.”

Energy and Natural Resources Market

Strengths

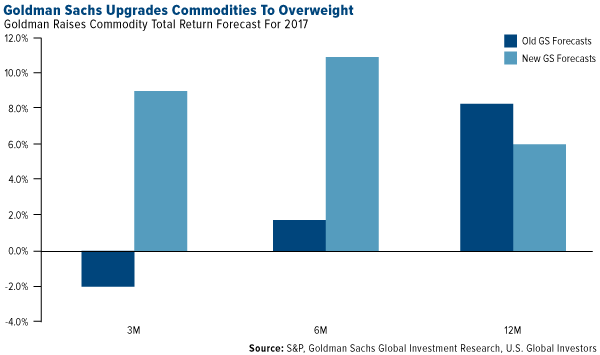

- Goldman Sachs initiates an overweight position on commodities for the first time in over four years. The bank is notoriously bearish toward commodities and has argued that as manufacturing is picking up around the world, investors should be overweight commodities next year. As PMI’s are improving and the prospect of increased infrastructure spending in the U.S. exists, this is a very positive read through for commodity prices as a whole.

- The best performing sector for the week was the S&P/TSX Composite Diversified Metals & Mining Sub Industry Index. The index rose 11.5 percent on the back of rallying base metal prices this week.

- First Quantum Minerals, one of the world’s leading copper producers, was the best performing stock this week finishing up 15.1 percent. The stock rallied on the back of further momentum gained this week in the continuation of copper’s incredible rally.

Weaknesses

- Gold was the worst performing commodity this week falling 3 percent. Risk-off sentiment has subsided across markets as the Trump and reflation trades have gained steam. Combined with the Federal Reserve preparing to raise rates in December, this is a negative read through for the price of gold.

- The worst performing sector this week was the S&P/TSX Composite Gold Sub Industry Index. The index fell 3.02 percent as the U.S. dollar and risk on sentiment continues to hammer the shiny yellow metal.

- The worst performing stock for the week was Newcrest Mining, one of the world’s largest gold mining companies with key assets in Australia. The company fell 4.7 percent on the back of falling gold prices.

Opportunities

- Shares of independent oil refiners gained some momentum this week. President elect Donald Trump’s victory has given some fuel to small independent oil refiners who have been burdened by the excess cost of buying credits from the Energy Independence and Security Act of 2007. A positive read through for independent oil refiners.

- Steel demand in China has improved this month. Macquarie Bank released a very positive report in its monthly Chinese steel survey for the month of November which surveys mills, steel traders, and iron ore traders. The purpose of the survey is to gauge sentiment, orders, sales and production, all of which dramatically improved from the month of October.

- Several hedge funds in China closed their copper short positions on the Shanghai Futures Exchange this week. Discussions with the financial community in Shanghai has led to information that certain key short positions were closed early last week, serving as a catalyst to the upward move in copper this week. A positive read through for copper.

Threats

- Gold broke the $1,200 dollar level this week on the back of a weak data print in U.S. durable goods orders. With the Federal Reserve preparing for its December rate hike and the Trump rally in full effect, heightened volatility in gold continues to persist.

- Home sales for the month of October came in at 558,000, missing expectations of 593,000. This was the weakest new home sales number since June of this year. A negative read through for the building materials sector.

- This week Macquarie Bank released a research note stating the odds of OPEC reaching a deal remain at 60 percent; however, the structure of the deal remains unclear. In the note, the bank gave a range for crude oil to move to the low $50 range if a deal is made, but failure of reaching a deal could lead crude oil to the low $30 range. All eyes will be on OPEC next week.

China Region

Strengths

- The Shanghai Composite rose 2.16 percent for the week.

- Hong Kong-listed miner CITIC Resources Holdings Ltd. (1205 HK) rose just under 24 percent for the week as Temasek made an exit on a share sale.

- The Hong Kong dollar continues to hold up relatively well against a large number of its peers.

Weaknesses

- Industrial Production and export orders in Taiwan both missed respective expectations this week. IP came in up 3.7 percent year-over-year, while expectations were for a 5.3 percent gain; Export orders, on the other hand, rose only 0.3 percent—well short of an anticipated gain of 3.7 percent for the October period.

- Taiwan’s third-quarter GDP print missed, coming in at a 2.03 percent year-over-year pace, just shy of expectations for a 2.10 percent print.

- Thailand’s third-quarter GDP also missed expectations. Expectations for the year-over-year third-quarter print were for 3.4 percent, but came in at only 3.2, while quarter-over-quarter expectations were for a rise of 0.7 percent, but the actual print came in short at a gain of only 0.6 percent.

Opportunities

|

- As the sharing economy in China continues to expand, Airbnb announced it may be seeking to acquire its Chinese home-rental rival Xiaozhu.

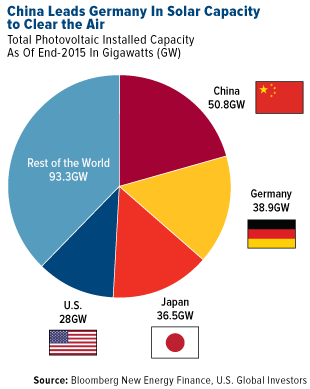

- Chinese growth in renewables continues to expand—a trend that may or may not be reflected in, or affected by, a new Trump administration in the United States—but China has now surpassed even Germany in total photovoltaic installed capacity.

- Stay tuned next week as several countries in the region report November PMI data, including China.

Threats

- While still somewhat unlikely, South Korea’s political scandal involving President Park continues to drag on, with talk of impeachment weighing to some degree upon sentiment, even as some of Park’s own party members have now joined the clamor for her to step down.

- U.S. President-elect Donald Trump continues to proclaim the imminent death of the Trans-Pacific Partnership.

- The weakening yuan—which rose to more than 6.92 this week, once again making new highs (lows) on the year—could force more potential outflows of capital from China.

Emerging Europe

Strengths

- Poland was the best performing country this week, gaining 3.6 percent. The Warsaw stock exchange rebounded with the biggest gains noticed in the utility and consumer discretionary sectors. Wood &Company recommends staying selective in Poland with a focus on high-quality, medium/small-cap names.

- The Polish zloty was the best relative performing currency this week, gaining 60 basis points against the U.S. dollar. The currency gained more ground on Friday after unemployment fell from 6.2 percent in the second quarter to 5.9 percent in the third quarter, the lowest reading since 2010.

- The materials sector was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst performing country this week, losing 1.7 percent. The European Parliament voted in favor of freezing Turkish membership talks with the final decision to be made on December 15. The president of Turkey said that his country should look at other opportunities, such as the Russian-led Shanghai Pact which currently has five members: Russia, China, Kazakhstan, Kyrgyzstan and Tajikistan.

- The Turkish lira was the worst performing currency this week, losing 2.1 percent against the U.S. dollar. Lira weakness continues despite the Central Bank of Turkey hiking the main policy rate by 50 basis points and the overnight borrowing rate by 25 basis points. Domestic and geopolitical events put pressure on the country’s currency.

- The real estate sector was the worst performing sector among eastern European markets this week.

Opportunities

- The November flash PMI data for the eurozone was reported strong, signaling firm Euro--area growth. The composite November reading rose to 54.1 from 53.3, a new high for the year.

- The Athens stock exchange has seen increased trading volumes, mostly due to higher interest in banks. The market remains optimistic about the course of the second program review in Greece. The Greek government wants to wrap up the review by December 5 and push forward with talks on debt relief that could allow the European Central Bank to include Greek bonds in its quantitative easing program.

- At the October OPEC meeting, members failed to reach an agreement on potential oil production cuts on concerns over Iran, but in recent days ministers and officials have said OPEC is moving closer to offer Iran flexibility on production volumes. The final meeting will take place November 30, and if OPEC decides to cut its production, the price of oil will increase. Russia will benefit from higher oil prices as most of the country’s revenue comes from the sale of oil and gas.

Threats

- More than 70 percent of the adult population of Russia belongs to the less wealthy half of the world's population, including a quarter of Russians (among the poorest 20 percent of humanity), Credit Suisse said in a report. During the year, the inequality in Russia has increased. Ten percent of Russians account for almost 90 percent of national wealth. The wealth of an average Russian fell by 14.5 percent in the year to mid-2016, largely due to the depreciation of the rubble, and Russians account for just 0.4 percent of global wealth.

- Federal funds futures for December delivery implied traders briefly priced in a 100 percent chance the Fed would hike rates in December by 25 basis points. Emerging Europe currencies will depreciate against the U.S. dollar in the case of a rate hike in U.S. The lira is JPMorgan’s highest conviction short trade in EMEA Emerging Markets because the currency is highly exposed to a rise in U.S. yields, as the country funds its borrowing needs in U.S. dollars.

- The market was surprised first with the Brexit vote and recently with Donald Trump’s victory in November. Next week, on December 4, Italy will vote in a referendum on whether or not to overhaul its national constitution. If yes camp wins, Prime Minister Matteo Renzi will have more power in his hands and will be able to push forward with the much needed economic reforms. Renzi threatened to resign if he loses and sees the government collapsing.

© US Global Investors