KEY TAKEAWAYS

- The National Retail Federation, a trade organization for retailers that tallies up holiday shopping totals each year, forecasts a 3.6% increase in holiday shopping this year.

- We see several reasons to expect consumers to potentially open up their wallets this holiday season, including low financial obligations, steady job and wage gains, and high consumer confidence.

- Back-to-school shopping increases and solid stock market performance in 2016 also bode well for the holiday shopping season to deliver some cheer.

This week we preview the holiday shopping season. Although the market’s attention has been squarely on the election for the past several months, we should not forget how important this time of year is for the U.S. economy—consumer spending represents about two-thirds of the U.S. economy and roughly 30% of retail sales occur during the holiday season. Here we discuss prospects for holiday shopping, which we expect to deliver some holiday cheer.

HOLIDAY SALES OUTLOOK

The National Retail Federation (NRF), a trade organization for retailers that tallies up holiday shopping totals each year, forecasts a 3.6% increase in holiday shopping this year (excluding restaurants, autos, and gasoline). That compares with 3.2% growth in holiday sales in 2015 versus 2014. Included in these figures are online sales, expected to increase by between 7% and 10% year over year to roughly 9% of total retail sales, according to the NRF.

We see several reasons to expect consumers to potentially open up their wallets this holiday season, suggesting this target may be achievable:

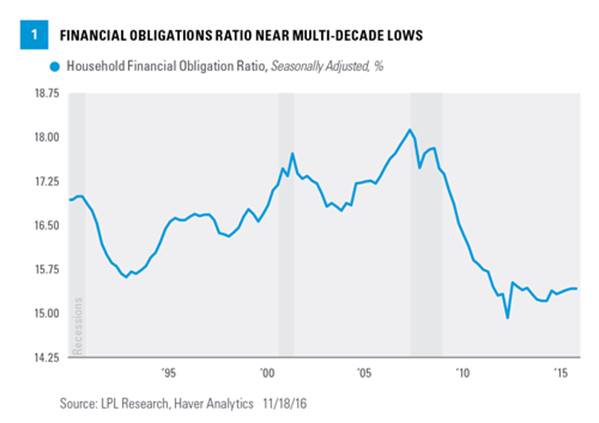

· Consumers’ finances are in good shape. One of our favorite indicators for consumers’ spending power is the financial obligations ratio [Figure 1]. This ratio measures consumer obligations (such as mortgage and property tax payments, rents, consumer debt, car lease payments, etc.) relative to their ability to afford those obligations as measured by disposable income (income remaining after financial obligations are met). As Figure 1 shows, this measure is near its lowest levels in several decades and suggests consumers have the ability to spend.

· Job gains have been steady. Although the pace of job gains has slowed, the U.S. economy continues to add nearly 200 thousand jobs per month and has produced job gains for a record 73 straight months (as of October 2016). Filings for jobless claims are at their lowest levels since the 1970s. And wages, based on average hourly earnings, are growing nicely, rising 2.8% year over year in October 2016, up from 2.7% in September and the strongest since June of 2009.

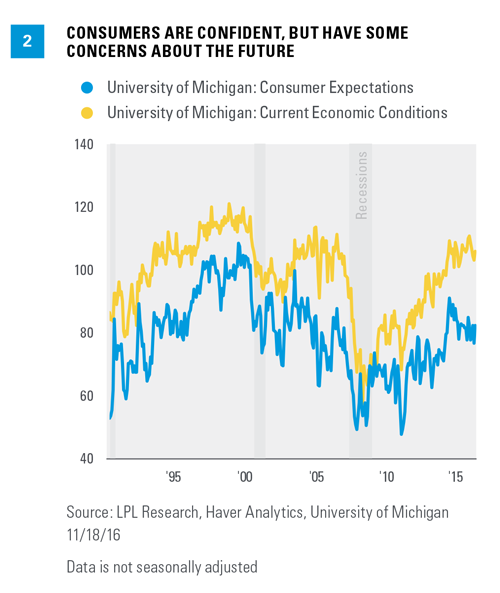

· Consumers are confident.* Consumer sentiment as measured by the University of Michigan sentiment indexes shows consumers are relatively confident about the economy and their financial health [Figure 2]. The gap between expectations and current conditions likely reflects election uncertainty (the latest reading was taken before the election results were known) and may close after the policy path out of Washington becomes clearer. Favorable prospects for a tax cut for individuals in 2017 may help sentiment.*The Consumer Sentiment report refers to a report published by the University of Michigan, in which the University’s Consumer Survey Center questions 500 households each month on their financial conditions and attitudes about the economy. Consumer sentiment is important because it is directly related to the strength of consumer spending. Preliminary estimates for a month are released at mid-month. Final estimates for a month are released near the end of the month.

· Prices at the pump are still low. Consumers are spending as small of a percentage of their income on energy, at about 3%, as they have since the late 1990s (based on U.S. Bureau of Economic Analysis data). Although oil and natural gas prices have risen over the past year, they remain low and we expect any increases in the near term—barring a big surprise from OPEC at the end of this month—to be gradual.

BACK-TO-SCHOOL INDICATOR

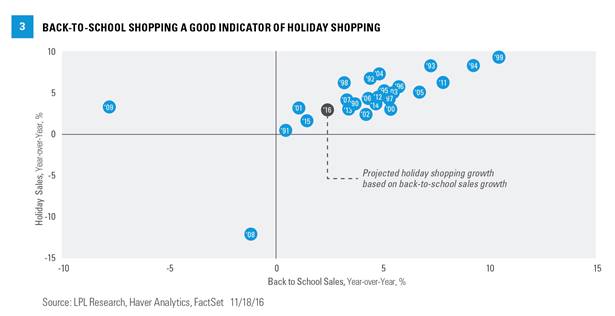

In recent decades, back-to-school shopping has been a good leading indicator for the holiday shopping season [Figure 3]. Historically, when sales during this important part of the retail calendar—in August and September—are good, sales for the holidays are almost invariably solid as well (the farther to the right a data point is on the horizontal axis in the chart, the higher that data point tends to be on the vertical axis, and vice versa).

This year, retail sales during the back-to-school shopping season (August and September 2016) rose 2.4% year over year, compared with last year’s gain of just 1.5%, suggesting slightly better holiday sales than 2015 is possible. However, the relationship between these two data points suggests a 3.1% increase, slightly less than the 3.2% increase in 2015 and below the NRF’s 3.6% forecast for this year.

STOCK MARKET GAINS MAY OFFER SOME HELP

The stock market has historically been a pretty good indicator of the health of holiday shopping season. Figure 4 shows the strong correlation between annual gains in retail sales compared with annual gains in stock prices. Since 1990, when the S&P 500 is up year to date through November 30, the average holiday sales gain is 5.0%. When the S&P 500 is down year to date through November 30, the average holiday sales gain is just 1.4%. The S&P 500 is up more than 6.7% year to date (total return is 8.9%).

MARKET IMPLICATIONS

Although we expect a good holiday shopping season, we see a more mixed outlook for retailers and the consumer discretionary and consumer staples sectors overall. Many traditional retailers continue to struggle with the disruption from the boom in e-commerce, which has contributed to more widespread discounting and resulted in pressure on profit margins as retailers have made costly investments to compete.

Demographics are another headwind for traditional retailers, as many millennials are opting for experiences over things, causing a shift in spending. Finally, technology products (smartphones, tablets, gaming consoles, etc.), have gained wallet share over goods sold at traditional retailers, presenting yet another challenge for many retailers.

These headwinds have shown up in slower earnings growth for the consumer discretionary sector, which along with the mid-to-late stage of the business cycle, support our preference for technology and industrials over the consumer sectors for growth potential.

We do expect the consumer to make a good enough showing that if holiday sales miss forecasts, the shortfall may be small enough so as to not spook the markets. That may not necessarily preclude a stock market correction in the next month or two; we would just be surprised if holiday shopping had much to do with it.

CONCLUSION

Consumers are in pretty good shape, suggesting that this holiday shopping season could potentially be a fairly good one. Low financial obligations, steady job and wage gains, high consumer sentiment measures, retailers’ back-to-school shopping increases, and the solid stock market performance in 2016 all suggest the NRF’s forecast for holiday sales growth of 3.6% compared with 2015 may be doable. We do not necessarily expect these sales gains to translate into outperformance for the consumer sectors, but we suspect they may be good enough to not spook markets.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

Because of its narrow focus, sector investing will be subject to greater volatility than investing more broadly across many sectors and companies.

All investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

© LPL Financial

Read more commentaries by LPL Financial