KEY TAKEAWAYS

- The U.S. economic landscape is still running under its long-term potential and could benefit from policies designed to boost the economy’s productivity and its potential growth rate.

- Based on the LEI, the economy President-elect Trump is inheriting from President Obama is most like the one former President Kennedy inherited from President Eisenhower in 1961; unlike Kennedy, Trump is not inheriting an economy that is in a recession.

In a key speech last week (November 14 - 18, 2016), Janet Yellen, Chair of the Federal Reserve (Fed) testified before the Joint Economic Committee (JEC) of Congress, further preparing markets for a Fed rate hike as soon as the next Federal Open Market Committee (FOMC) meeting in mid-December.

In Yellen’s prepared remarks, she noted that “The U.S. economy has made further progress this year toward the Federal Reserve’s dual-mandate objectives of maximum employment and price stability.” During the Q&A with members of Congress, Yellen also provided some advice to Congress and the incoming Trump Administration’s transition team as they prepare to potentially propose and pass a fiscal stimulus package.

Yellen opined that the economy here in late 2016 is close to full employment, especially compared with early 2009, as Congress and the incoming Obama Administration were preparing a fiscal stimulus package to combat the impact of the Great Recession. Additionally, Yellen noted that policies that enhance productivity should be given consideration, especially given weak productivity growth in recent years. Yellen’s remarks last week were echoed by Fed Vice Chair Stanley Fischer as this report was being prepared for publication on Monday, November 21, 2016. We took a high level look at the fiscal policies under consideration by President-elect Trump in last week’s Weekly Economic Commentary, “Evaluating the Economics of the President-Elect” and discussed the recent lackluster performance of productivity in the U.S. economy in the Weekly Economic Commentary: “Building Blocks” from May 16, 2016.

This week, we will examine the economic conditions faced by President-elect Donald Trump compared with other new incoming administrations in the past 50 years or so. First, let’s define terms. By new incoming presidential administrations, we mean presidents starting their first terms in office:

· Kennedy 1961

· Johnson 1963

· Nixon 1969

· Ford 1974

· Carter 1977

· Reagan 1981

· Bush 1989

· Clinton 1993

· Bush II 2001

· Obama 2009

Although the health of the economy can be measured in many ways, we’ll use the output gap (how close actual gross domestic product [GDP] is to potential GDP) as a proxy for Yellen’s comment about full employment and the Leading Economic Indicators (LEI), which is one of LPL Research’s Five Forecasters. We’ll start with the LEI.

The Five Forecasters

There is no magic formula for predicting recessions and bear markets -- every cycle is different. But we believe the Five Forecasters cover a variety of perspectives and help capture a more complete view of the economic and market environment. They are meant to be considered collectively, not individually. For more on the Five Forecasters and other components we’re watching, please see the latest Recession Watch Dashboard.

These five data series that make up the Five Forecasters have a significant historical record of providing a caution signal that we are transitioning into the late stage of the economic cycle and that recessionary pressures are mounting. Specifically, we monitor: the Market (using the treasury yield curve), Fundamentals (using the Index of Leading Economic Indicators, or LEI), Valuations, using the S&P 500 trailing price-to-earnings ratio, Technicals, using market breadth, and Sentiment, using the Institute for Supply Management’s Purchasing Managers’ Index, PMI.

THE LEI IN TRANSITION

The latest reading on the LEI, based on October 2016 data, revealed that the index rose 0.1% between September and October 2016, and climbed only 1.1% since October 2015. At 1.1%, the year-over-year reading on the LEI puts the odds of recession at under 7% within the next year. The October 2016 reading is right in the middle of the pack compared with the year-over-year gains in the LEI faced by the 10 presidents to assume the office over the past 50+ years [Figure 1].

Based on the LEI, the prospects for the economies facing former Presidents Reagan, Ford, Bush (George W.), and Obama were all materially worse than those faced by Trump, while the prospects for the economy inherited by former Presidents Johnson, Nixon, Carter, and Clinton were materially better than Trump’s. The U.S. economy was in a recession when Kennedy took over in early 1961, when Ford replaced Nixon in 1974, and when Obama replaced Bush in 2009. The U.S. economy was between the “double dip” recessions of January - June 1980 and July 1981 - November 1982, when Reagan took over from Carter in early 1981.

Based on the LEI, the economy Trump is inheriting from President Obama is most like the one Kennedy inherited from Eisenhower in 1961, but unlike Kennedy, Trump is not inheriting an economy that is actually in a recession.

OUTPUT GAP AND FISCAL POLICY IN TRANSITION

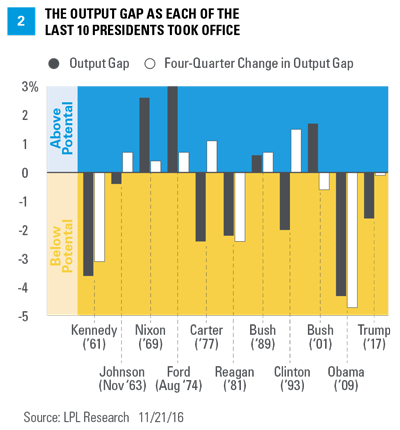

Figure 2 shows the output gap -- the difference between potential GDP and actual GDP as a percent of potential GDP -- at the start of the new terms of each of the past 10 presidential administrations. Although not a precise measure, the output gap is a decent proxy for how close to “full employment” an economy is. Figure 2 also lists the four-quarter change in the output gap, which is a measure of how much slack was taken up (or created) in the economy in the four quarters prior to the start of a term.

Today, the output gap stands at -1.6%, indicating the economy still has some slack. Over the past four quarters, there has been little change in the output gap. Back in late 2008 as President Obama was preparing to take office, the output gap stood at -4.3% and had dropped 4.7 percentage points over the prior four quarters. This move took the economy from full employment to a very wide output gap in just one year. Presidents Kennedy and Reagan faced a similar backdrop to President Obama; an economy that was growing well below potential and one that had deteriorated sharply over the prior four quarters. All three presidents enacted fiscal policies (i.e., tax cuts or spending increases or both) to help boost growth. In contrast, Presidents Johnson, Nixon, Bush, and Bush (George W.) inherited economies that were running at or above potential. As it relates to fiscal policy, President Lyndon Johnson’s policies are worth a mention. Johnson enacted his Great Society legislation in the mid-1960s, in an economy that was already running at or above its full potential, providing some of the impetus for the prolonged upswing in inflation in the late 1960s through the early 1980s.

Although the output gap over the past four quarters hasn’t changed much, Presidents Johnson, Nixon, Ford, Carter, and Bush inherited economies where the output gap was shrinking significantly, suggesting that any fiscal policies enacted by those administrations took effect as the economy was already moving rapidly toward the elusive “full employment.”

Thus, although the economic landscape that Trump is facing is far better than that faced by former Presidents Kennedy, Reagan, and Obama as they prepared to take office, it is still running below its long-term potential, and as Yellen noted, could benefit from policies designed to boost the economy’s productivity, and in turn, its potential growth rate in the coming years.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments, and exports less imports that occur within a defined territory.

INDEX DESCRIPTIONS

The Conference Board Leading Economic Index (LEI) is a measure of economic variables, such as private sector wages, that tends to show the direction of future economic activity.

© LPL Financial

Read more commentaries by LPL Financial