Key Points

- U.S. stocks, especially small caps, have surged since the election.

- Investor sentiment and sector performance show a remarkable shift in a short period.

- The secular bull market lives on, but some of next year’s performance may get pulled into this year.

Since the pre-election low on November 4, the S&P 500 is up 4.7%, while the Russell 2000 (small caps) is up a whopping 13.8%—rallies which have confounded many investors given the pre-election consensus that stocks would fall on the uncertainty associated with a Trump victory. We did not move into the bearish camp pre-election; but did expect to see a bit more volatility than what has ensued so far.

The rally has had an extreme U.S. bias as well. Global equities, as measured by the MSCI All Country World Index ex. United States, are -1.87% in the past two weeks, while the Wilshire 5000 (the broadest index of U.S. stocks) is +5.61%. That is a spread of 748 basis points in only 10 trading sessions. Cornerstone Macro highlighted this rare occurrence (more than 700 basis points of spread)—it’s happened only 13 other times going back to 1987, when data for the MSCI index was created. Following these occurrences, U.S. stocks had a tendency to give back some of their gains relative to international stocks’ performance and the spread tended to narrow.

Bears morphing into bulls

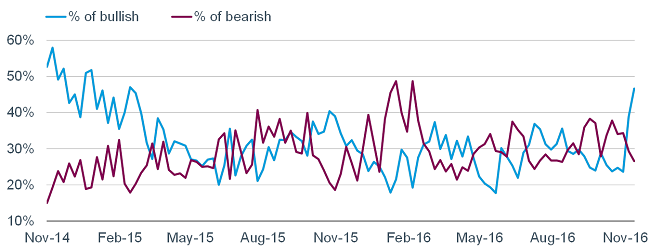

Investors sentiment has certainly shifted swiftly back to optimism. Two sentiment indexes on which I keep a close eye are from the American Association of Individual Investors (AAII) and SentimenTrader (ST). The former, seen below, shows a significant spike in bullishness—back to the highest level in nearly two years.

Source: American Association of Individual Investors (AAII) Sentiment Survey, FactSet, as of November 18, 2016.

ST has a more behavior-oriented measure of confidence as it looks at what two investor cohorts are actually doing and doesn’t involve opinions. Generally, you want to follow the Smart Money (SM) traders when they reach an extreme in either direction. Examples of some SM indicators include the OEX put/call and open interest ratios, commercial hedger positions in the equity index futures, and the current relationship between stocks and bonds. Generally, you want to do the opposite of what the Dumb Money (DM) is doing at extremes. Examples of some DM indicators include the equity-only put/call ratio, the flow into and out of the Rydex series of index mutual funds, and small speculators in equity index futures contracts.

Source: SentimenTrader, as of November 18, 2016.

As you can see, for now, both SM and DM confidence has been rising recently, which is not the normal pattern. If the market’s gains persist, I would expect DM confidence to keep accelerating; while SM confidence would more likely roll over. Either way, for now, this pair of measures is not signaling an extreme.

Institutional survey

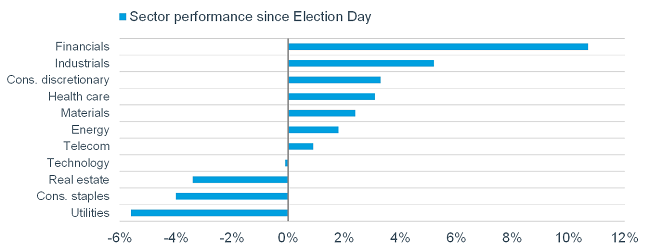

Strategas Research Partners recently conducted a snap survey of institutional investor sentiment; with more than 650 of their clients responding. The question was simple: Does the outcome of the election make you more bullish or less bullish on stocks? More than 83% responded that they’re more bullish. And in keeping with the strong outperformance of the financial sector (on which Schwab has an overweight recommendation), nearly 57% believe financials will be the “biggest beneficiary as a result of the election.” On the other hand, over 40% believe utilities (on which Schwab has an underweight recommendation) will be the “biggest loser.” The utilities’ dour sentiment no doubt reflects the significant back-up in longer-term Treasury yields.

You can see a chart of sector performance since the election below. We’ve witnessed one of the largest sector rotations in the modern market era—in this case from more defensive sectors to those seen as potential beneficiaries of the perceived pro-growth policies of a Trump administration. But performance has been somewhat narrow as financials and industrials are the only two sectors outperforming the S&P 500 by more than one percentage point.

Source: Strategas Research Partners, as of November 18, 2016.

Another behavioral measure of investor sentiment is fund flows. More than $30 billion flowed into U.S. equity funds in the week up to November 16—a record weekly haul, according to data from EPFR. And correlations have been coming down—a potential support for the beleaguered active style vs. passive style of investing.

Animal spirits

Has the market gone too far too fast? Perhaps in the short-term, but animal spirits—assuming they’ve awoken—can fuel rallies for an extended period. There is much about this rally so far to behold—and much which is also unique. According to data from Bespoke Investment Group (BIG), performance since the election has been inversely correlated to market cap (as highlighted above with the dramatic outperformance by small caps).

Stocks with the most attractive valuations have rallied the most, which is unique relative to what is normally seen in big rallies. I think it reflects an environment with improving economic growth prospects. When economic growth is harder to come by, stocks with better growth prospects tend to outperform. But when growth is less dear and more amply distributed among companies, investors tend to shift their focus to finding companies trading at reasonable valuations.

And in keeping with sentiment being a contrarian indicator, since the election stocks with the lowest short interest are up just 2.2%; while stocks with the highest short interest are up over 8%. This trend is also illustrated by the performance of stocks with the best (2%) and worst (4.6%) Wall Street analyst ratings.

Finally, with the dollar up sharply, stocks of companies with the lowest exposure to international markets are up about three times the performance of stocks of companies with the highest exposure to international markets.

Recent economic releases have also provided support for the rally, suggesting that some of the lift in the economy was already happening, and isn’t just a hope for next year under a Trump administration. Of the 20 reports released last week, nine were better than expected—including retail sales, housing starts/permits and unemployment claims. Four were in line with expectations and seven were weaker—including industrial production and capacity utilization. Reflecting the better economic data and higher inflation, the Federal Open Market Committee (FOMC) is likely to raise rates at its December meeting.

Secular bull should live to see its eighth birthday

The net is that my view has not changed that we remain in a secular bull market, which is set to celebrate its eighth birthday this coming March. But we may be pulling some of next year’s performance into the final weeks of this year. I continue to expect some bouts of volatility as we move from speculating about Trump’s policies to actually facing their reality next year; especially if protectionism moves up the priority ranking of policies. As mentioned, animal spirits have been suppressed for some time, and appear to be lighting up. This is the strongest support for both the economy and stock market looking ahead. But there are risks, including the aforementioned spikes in optimistic sentiment (a contrarian indicator) and the U.S. dollar (which is causing a tightening of financial conditions). Stay long, but stay strong in terms of your discipline around diversification and rebalancing.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

(1116-R2XH)

© Charles Schwab

© Charles Schwab

Read more commentaries by Charles Schwab