People are mostly insane.

For evidence, look no further than sales of bottled water in the first world. Our ancestors spent hundreds of billions of dollars developing the infrastructure to deliver potable water to every home, yet we spend billions each year to purchase bottled versions of what we can get for free almost anywhere. Boom – I just blew up the very foundation of economics.

Takeaways:

1. Investors pay too much for traditional active management

2. The market itself does most of the heavy lifting for most mutual funds and ‘smart \beta’ products

3. Where mutual funds do add value in excess of market returns, most of this value is consumed in fees and costs

4. Many GTAA strategies produce returns with low systematic market exposure

5. These strategies produce a much higher proportion of active value.

This irrational behaviour also extends to how we pay for financial products. Consider that most financial products are benchmarked to an index that one can easily track with ultra-cheap ETFs or index funds. Want exposure to U.S. equities? Vanguard’s VTI ETF provides exposure to every U.S. listed stock for just 0.05% per year. That’s basically free. Want international bond exposure? Vanguard’s BNDX gives you diversified international bond exposure for just 0.15%. Again – free.

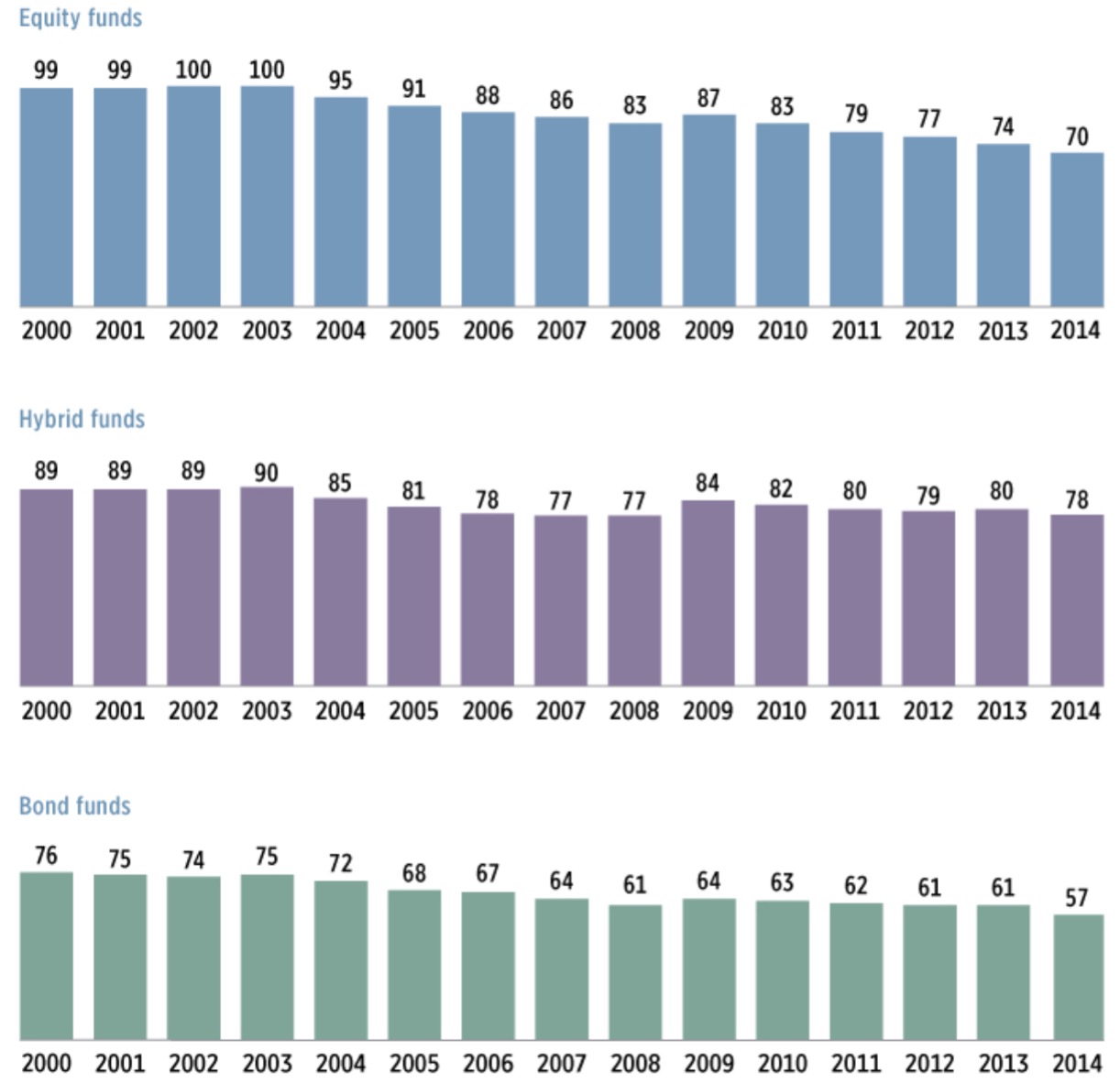

Yet according to a recent Blackrock report, active mutual funds still dominate about 2/3 of investors’ allocations. And according to the Investment Company Institute, the average cost of active mutual funds is currently about 0.70% on an asset-weighted basis, and 1.33% on an equal-weighted basis. Different fund mandates have different expense ratios, per Figure 1.

Figure 1.

Source: Investment Funds Institute

Source: Investment Funds Institute

Presumably, advisors recommend active funds because they expect outperformance relative to an index fund alternative. Let’s set aside for a moment the fact that this outperformance has not materialized for active funds in well over a decade (see SPIVA report here). Instead, let’s play along with the illusion of outperformance and assume an active equity fund delivered a 1% return premium after fees and costs, while an equity index fund produced a 9% return in the same period. Further, assume that the fund has a beta of 1 to the market (this will be explained below).

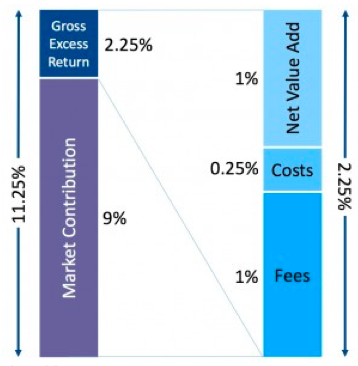

Remember, the market itself is responsible for 9% of the 10% total net return, or 90%, while the manager is responsible for just 10%. To produce this 1% excess return, the active manager charged a 1% fee, and incurred 0.25% in costs. Therefore, the manager actually generated 11.25% in returns (9% from the market, 1% in fees, 0.25% in costs, and 1% in next excess returns). It follows that the manager produced 2.25% in gross excess returns, of which 1% / 2.25% = 56% was consumed in fees and costs, and 1% was distributed to unit holders as excess returns. In other words, the manager himself consumed 56% of the value he created.

Figure 2. Breakdown of value contributions from market and manager for hypothetical equity fund.

Source: ReSolve Asset Management

The investment industry is happy to perpetuate the illusion that the fund consumes 1.25% of the 10% total returns, or 12.5%. But it is clear from the example above that the market itself is responsible for 90% of those returns. The fund manager had nothing whatsoever to do with that. Rather, the manager is responsible exclusively for 2.25% in gross excess returns, of which he consumes over half in fees and costs. So the real cost of active management in this example is 56% of the value, not 12.5%.

Now, it may be appropriate for managers to consume 50% of the profits from their activities. After all, active management is extremely difficult, consumes an enormous amount of time and resources for research and compliance, has a very high attrition rate, and contains many dimensions that are largely out of the manager’s control. As such, it is a very stressful job, and should command relatively high margins.

However, it should be made clear to investors exactly what the compensation arrangement really is. Most of all, investors should understand that, for the vast majority of active funds, the market itself performs the vast majority of the heavy lifting. The active component is at best, a cherry on top (and most of the time the cherry is rotten).

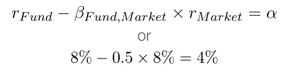

Remember that one of the assumptions in our example above is that the fund in question had a beta of 1 to the market. This means that the fund’s risk was entirely explained by market risk. If the fund took greater than market risk to generate its returns, the excess returns would be less impressive. That’s because anyone could simply lever up exposure to the market to achieve the same return with no excess skill.

Imagine that our star fund had a beta of 1.1 to the market. Then if the market produced a 9% return, we would expect the fund to produce a return of 9% x 1.1 = 9.9%. That’s because any investor who purchased 1.1 units of the market (using 10% leverage), would have achieved a 9.9% return (assume no cost to borrow for simplicity). As a result, adjusted for risk the manager would have actually only produced 10% – 9.9% = 0.1% in excess returns.

Again ignoring the return and/or borrowing cost on cash, expected returns and realized returns are linked to market exposure by this equation:

The equation suggests that the return that should be expected from a fund is equal to the return from the market itself times a scaling factor (beta), which is the fund’s sensitivity to market returns. In addition, the fund may deliver returns in excess of what would be expected based on the fund’s sensitivity to the market. This is the alpha variable in the equation. Alpha is the return that is not explained by a fund’s exposure to the market. It quantifies the true value added by the manager.

You can see that the true value generated by a manager is a function of how much market risk he assumes to generate the returns. Simply inverting this statement leads to the following corollary: there is greater value in returns that are generated with less exposure to markets.

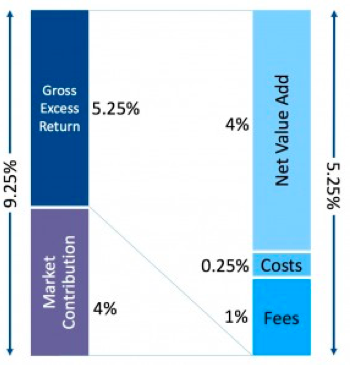

Now consider a typical Global Tactical Asset Allocation (GTAA) fund with a fee of 1% and 0.25% in costs, that delivered an 8% net return with a beta of 0.5 to a global balanced portfolio. Assume the global balanced portfolio produced the same 8% return over the period.

One might at first glance perceive that the GTAA fund added no value, since it delivered the same return as an investor could have achieved from investing in index tracking funds at near zero cost. But this view misses the fact that the return on the balanced portfolio is only responsible for half of the returns to the GTAA fund. Rearranging the equation above we see that the alpha from the GTAA fund is:

Let’s compare the value added by the GTAA manager to the value added by the equity fund manager discussed above. The equity fund manager produced total gross returns of 11.25%, but the stock market itself was responsible for 9% of that, so the manager’s gross value add was 2.25%. Of that 2.25%, fees and costs consume 1.25% or 56% of the value.

On the other hand, the GTAA fund delivered gross returns of 8% + 1.25% in fees and costs = 9.25%. Per the equations above, the fund manager was responsible for (8% – 4% = 4%) of those returns, and the market contributed 4%. Gross of fees, the GTAA fund delivered 4%+1.25% = 5.25% of gross value independent of the market. Of that, fees and costs of 1.25% consumed 1.25%/5.25% = 24% of this value, while 76% of the value accrued to investors in the fund.

Figure 3. Breakdown of value contributions from market and manager for hypothetical GTAA fund.

Source: ReSolve Asset Management

The moral of this (admittedly slightly long) story is that it is not economically valid to think about fees and costs as a percentage of total return because for traditional funds, most of the heavy lifting is done by the market, not the manager. In fact, where a traditional mutual fund manager is able to add value, most of that value is consumed by the fund itself in fees and costs.

At the same time, if a manager is truly generating returns independent of an easily (and cheaply) trackable index portfolio, then the manager may indeed be delivering value, most of which accrues directly to investors.

If you are going to pay for something, make sure you can’t get it for free. ReSolve strategies have a low correlation to global markets and a history of delivering meaningful value. Learn more about how to allocate directly to strategies that do their own heavy lifting using the ReSolve Online Advisor.

© ReSolve Asset Management

Read more commentaries by ReSolve Asset Management

Source: Investment Funds Institute

Source: Investment Funds Institute