KEY TAKEAWAYS

- We reflect on last week’s surprising stock market reaction to Donald Trump’s unexpected election victory.

- The S&P 500 gained 3.8% last week, its best since October of 2014. The Dow Industrials and small cap Russell 2000 delivered their best weeks since December of 2011.

- The outlooks for financials, healthcare, and industrials appear to have brightened, while the impacts on energy and small caps are more mixed.

- The near term may be more volatile for emerging markets (EM), although we continue to view the asset class as a potential intermediate-to-long-term opportunity.

This week we reflect on Donald Trump’s surprising victory and the stock market reaction. With Election Day behind us and the benefit of several days to digest the news, we reflect back on what was quite a week for the stock market. Here we offer some perspective on the trading week and share our views on some of the most politically sensitive asset classes and sectors.

STOCKS SURPRISE

There were two big surprises this week for investors: one was of course an election outcome few predicted, and the other was the market’s reaction to it. We are not surprised that stocks recovered; but rather how swiftly. Not even the market’s surprisingly fast recovery from the unexpected Brexit “leave” vote in the U.K. back in June of 2016 prepared us for this. After Dow futures were down over 800 points after the result became clear late on election night, the blue chips reversed course the next day (November 9) to end more than 250 points higher, before adding another 218 points on Thursday and 40 points on Friday. The Dow was down all five days the prior week before rising each day last week; a wild ride to say the least.

By week’s end, the S&P 500 had produced a five-day gain of 3.8%, the best week for the index since October 2014. The 5.4% and 10.2% gains for the blue chip Dow Industrials and small cap Russell 2000, respectively, were the best since December of 2011.

We believe several factors are behind the rebound:

· The certainty of an outcome. A prolonged legal battle to determine our next president would have damaged investor confidence. Some cash on the sidelines was likely waiting for a definitive outcome.

· Optimism regarding a peaceful transition. President-elect Trump seemed to strike the right tone for markets in his acceptance speech and appears willing to work with Republicans and Democrats to get things done, an encouraging development for markets.

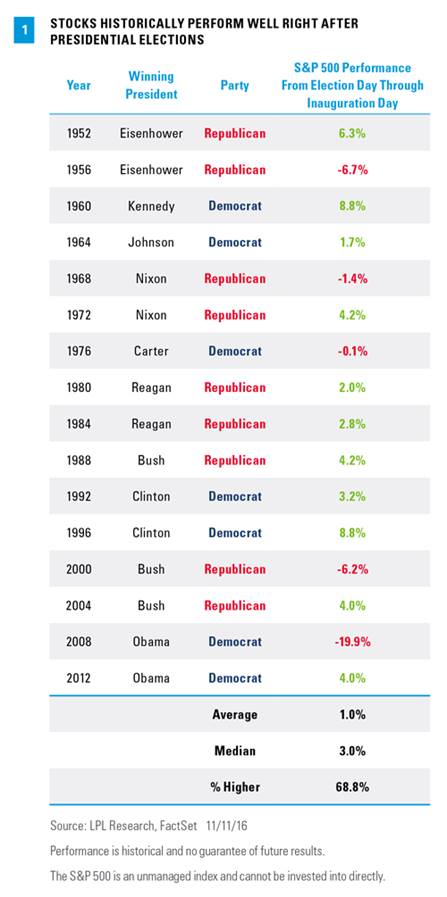

· Favorable election year pattern. Stocks have tended to do well late in election years due in part to the policy clarity provided by a winner. Since 1952, the S&P 500 is up by a median of 3% between Election Day and Inauguration Day (the average, at 1%, is skewed by sharp drops in 2000 and 2008), with gains 69% of the time [Figure 1]. Though policy uncertainty remains high, the likely path is becoming clearer each day.

· Anticipation of market friendly policies. The odds that many of President-elect Trump’s market-friendly policies are implemented following the Republican sweep are high and include tax reform, infrastructure spending, and rolling back regulations in areas such as financial services and healthcare.

· Negative sentiment. Heading into the election, sentiment readings based on derivatives were among the most negative that we have seen in two decades. Equity flows have also been decidedly negative this year. Most recently, the S&P 500 had just ended a nine-day losing streak (on November 7, 2016), the day before the election. That bearishness set up some buying on the news.

KEY MARKET IMPLICATIONS

The strength in the broad stock market indexes this week was notable, but the dispersion in the sectors also stood out. Sectors and industries expected to benefit from President-elect Trump, such as healthcare, financials, and infrastructure, all soared, while those that may be hurt by Trump’s policies sold off, including emerging markets and interest rate sensitive sectors such as utilities.

Here are our updated views on some of these areas following the election:

1. Emerging markets. Perhaps nowhere is the impact of Trump’s election felt more acutely than in overseas markets and currencies. Look no further than the Mexican peso, which has come under heavy pressure since the election, falling more than 10%. Emerging market (EM) stocks have been hurt by Trump’s skepticism on foreign trade, with promises to terminate or renegotiate trade agreements and add import tariffs. But changing policies can take some time, and changing economic realities can take even longer. And many of the things that we import from emerging markets are simply not produced in the U.S., including certain commodities and relatively low value-added manufactured goods, suggesting less near-term impact than feared.

Rising interest rates are another concern. The post-election spike in interest rates has made funding overseas investments with U.S. dollars more expensive, on top of the U.S. dollar appreciation that has eroded overseas returns for U.S.-based investors.

Going forward, EM assets are caught between two tensions. A more robust U.S. economy, especially one driven in part by increased infrastructure spending, may benefit EM. However, concerns over U.S. trade policy have created uncertainty regarding whether these benefits would actually flow through to EM economies and companies. We think near-term caution is prudent, with policy uncertainty high, but over the intermediate-to-longer term, we see the potential for improving earnings, attractive valuations, and better-than-feared trade relationships (compared with what was priced in immediately following the election) to support solid performance for EM equities.

2. Energy. Trump is likely to be positive for fossil fuels. He has promised less regulation on drilling, along with expansion of drilling areas. Should oil and natural gas prices hold up, some pipelines may get built that would not have under Hillary Clinton’s leadership. Refiners may see easing ethanol requirements, and the segment of the industrials sector that services the energy sector may also benefit.

The risk is that increased production sends oil prices down and hampers sector performance, although master limited partnerships may be less sensitive to that risk than the oil and gas producers.

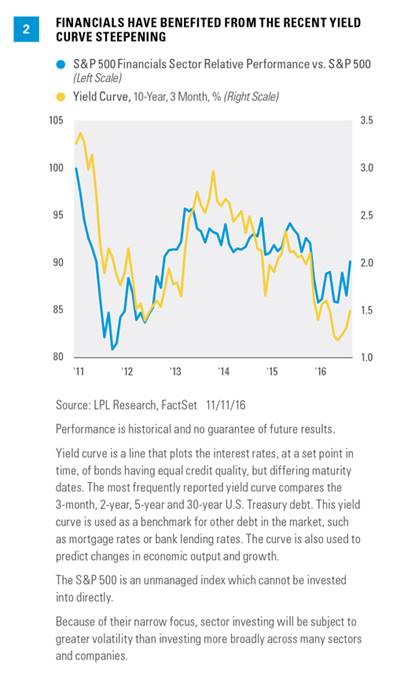

3. Financials. The election outcome has put upward pressure on interest rates and steepened the yield curve (difference between short- and long-term interest rates), which is good for bank profitability [Figure 2]. The Trump administration has stated its desire to roll back financial regulations, including the Dodd-Frank financial reforms created to reduce risk in the financial system following the financial crisis. Implementation of the Department of Labor’s fiduciary standard for retirement investment accounts, slated for April of 2017, could now be delayed, which could benefit the asset managers and mutual fund and annuity distributors. Finally, de-regulation and infrastructure spending could lead to increased bank lending.

One risk, though unlikely, is that Trump would bring back Glass-Steagall, as he alluded to during his campaign. The law would separate traditional banking from investment banking, something that has populist appeal.

4. Healthcare. Trump has stated his desire to repeal and replace the Affordable Care Act (ACA), which would negatively impact segments of healthcare that rely most heavily on those insured under the ACA. However, lowering drug prices through regulatory actions is unlikely to be a priority for President Trump, as it would have been under Clinton’s leadership. As a result, we expect a Trump Administration to be friendly to pharmaceuticals and biotech stocks. Managed care, which has been experiencing widely reported profit pressures through the ACA exchanges, may also benefit under an overhaul.

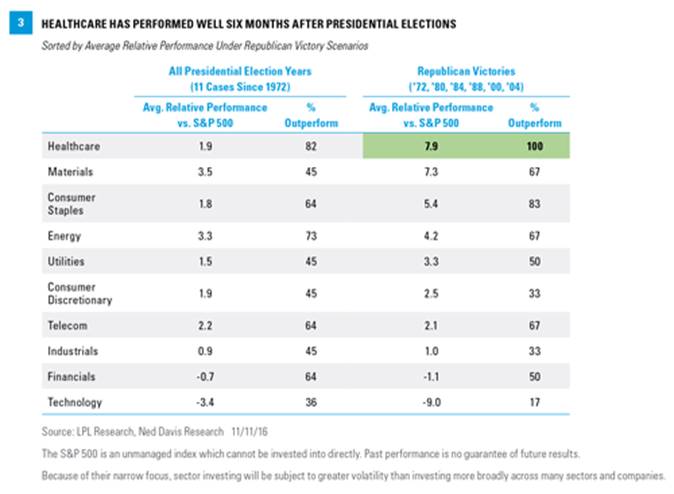

We think healthcare stocks may have overreacted to perceived policy risk prior to the election, suggesting the group could still play some catchup even after last week’s outperformance. The healthcare sector gained 5.9% last week, ahead of the S&P 500’s 3.8% advance, continuing its historical pattern of strong post-election performance [Figure 3].

5. Industrials. Trump has put infrastructure spending at the top of his agenda, throwing out numbers of as much as $1 trillion in additional spending. Within industrials, construction and engineering firms are poised to benefit (as will related materials companies). Industrials are also poised to benefit from increased defense spending, another emphasis of the Trump campaign. On top of that, some of the big global industrial companies have a lot of cash trapped overseas that could come back should tax reform include repatriation of overseas cash, as we expect. In addition, less energy regulation may support the segment of industrials tied to oil and gas infrastructure. Finally, we expect improved global growth from the increased spending to support the sector in the coming year.

The risk to these areas is again restrictive U.S. trade policy, should Trump follow through on his campaign threats to slap tariffs on Chinese and Mexican imports. The industrials and materials sectors are among the most globally focused. The potential for U.S. steelmakers to gain market share against overseas competitors is a potential offset to this risk.

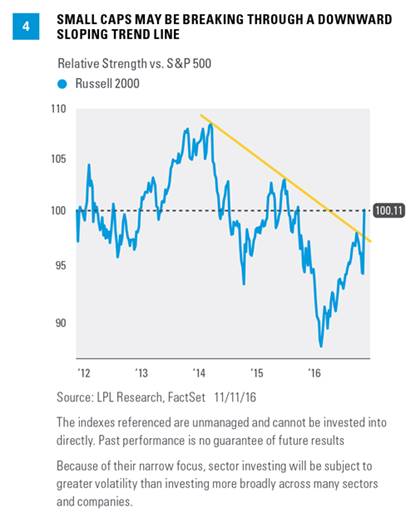

6. Small caps. Policies aimed at bringing manufacturing jobs back to the U.S., a key campaign goal for Mr. Trump, are positive for small cap stocks. More bank lending is also positive because small companies are generally more dependent on bank credit. Technical analysis suggests small caps have the potential for a relative performance run given they broke above a downward sloping trend line [Figure 4].

Conversely, favoring large caps over small is the likelihood of tax repatriation, which benefits larger companies with the most cash parked overseas. Valuations for small caps relative to large are rich, in our view. And although we do not expect a recession as early as 2017, the latter stage of the business cycle tends to be friendlier to larger caps. Bottom line, although small caps may experience a short-term run of outperformance on the election results, the strength may not be sustained beyond the near term.

CONCLUSION

It was quite a week for stocks, with impressive gains and some big moves in some key politically-sensitive areas. The outlook for financials, healthcare, and industrials appear to have brightened meaningfully while the impact on energy and small caps are a bit more mixed; meanwhile, the near term may be more volatile for EM, although we continue to see that asset class as a potential intermediate-to-long-term opportunity. Look for more on potential election impacts in our Outlook 2017, with an Executive Summary due out later this month.

Thank you to Ryan Detrick and Matthew Peterson for their contributions to this report.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

Because of its narrow focus, sector investing will be subject to greater volatility than investing more broadly across many sectors and companies.

International investing involves special risks such as currency fluctuation and political instability and may not be suitable for all investors. These risks are often heightened for investments in emerging markets.

The fast price swings in commodities and currencies will result in significant volatility in an investor’s holdings.

Small cap stocks may be subject to a higher degree of risk than more established companies' securities. The illiquidity of the small cap market may adversely affect the value of these investments.

All investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average Index is comprised of U.S.-listed stocks of companies that produce other (non-transportation and non-utility) goods and services. The Dow Jones industrial averages are maintained by editors of The Wall Street Journal. While the stock selection process is somewhat subjective, a stock typically is added only if the company has an excellent reputation, demonstrates sustained growth, is of interest to a large number of investors, and accurately represents the market sectors covered by the average. The Dow Jones averages are unique in that they are price weighted; therefore, their component weightings are affected only by changes in the stocks’ prices.

The Russell 2000 Index is an unmanaged index generally representative of the 2,000 smallest companies in the Russell 3000 index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

© LPL Financial

Read more commentaries by LPL Financial