Summary: In July, fund managers' had their highest exposure to bonds in 3-1/2 years. In other words, they expected yields to keep falling. Instead, yields reversed higher and have since risen so sharply that several smart money managers now say that a new secular uptrend in yields is taking place. That is a big call, given that the foregoing secular downtrend has lasted more than 35 years.

Over the past 18 months, investors' money has been flowing consistently out of equity funds. Where has that money gone? Mostly to bond funds. Money usually follows performance, so it's a good guess that fund flows might soon begin to favor equities. If past is prologue, then equities should gain and bond yields should continue to rise. Whether that will constitute the start to a new secular uptrend for yields it is far too early to say.

Perhaps the most prevalent storyline in the markets over the past several years has been the long term secular decline in interest rates. Not just in the United States, but worldwide, low economic growth and persistently weak inflation has contributed to falling sovereign yields.

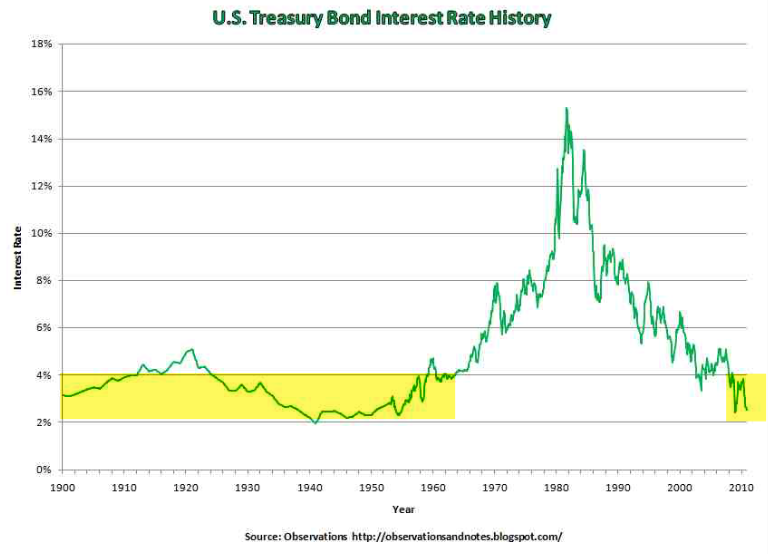

Interest rates have historically moved in cycles. On a relative basis, yields were as low as they are now for most of the period between 1900 and 1960 (the 10 year is currently 2.2%). Rates rose for 20 years until 1920 and then fell for 30 years into the 1950s. Then came a long secular rise in rates until 1980. That 30 year period has been followed by one even longer, as rates have cycled down over the past 4 decades.

Over the past several weeks (and especially since last week's election), some smart money managers have declared that the secular decline in yields is now over and that rates are beginning a long term move higher. Read Ray Dalio's views here.

They might be right. It is, objectively, too early to say.

In the chart above, notice that the change from a secular decline to a secular rise in rates 60 years ago did not take place overnight. For some 15 years in the 1940s and 1950s, rates oscillated between 2-3% before finally moving sustainably higher.

If you're thinking "but that was 60 years ago", you have just put your finger on the main problem with trying to pin point a secular change. By definition, they don't take place very often, during which time the world has massively changed.

We'll know in hindsight, but if yields are now in a secular uptrend, the change in direction will probably once again take time to unfold. Right now, it suddenly looks like higher yields are a one-way bet. It's probably a better bet that "the market" will obscure the change in the long-term trend through fluctuations in the short-term trend.

How so?

30 year yields are very much in a falling channel. In July, yields bottomed at 2.1%; they're now almost 3%. They could rise further to 4% and still be in a declining secular pattern. If a nearly 200 basis point change seems like a lot, recall that yields fell by that amount (from 4% to 2.2%) during calendar 2014.

It's also important to realize that the 1200 basis point rise in rates between 1960 and 1980 was extreme. Again, the secular rise in rates between 1900 and 1920 was a relatively minor 200 basis points. A secular rise now might be similarly minor. Overtime, it might just look like rates are moving within the yellow shaded band (first chart above).

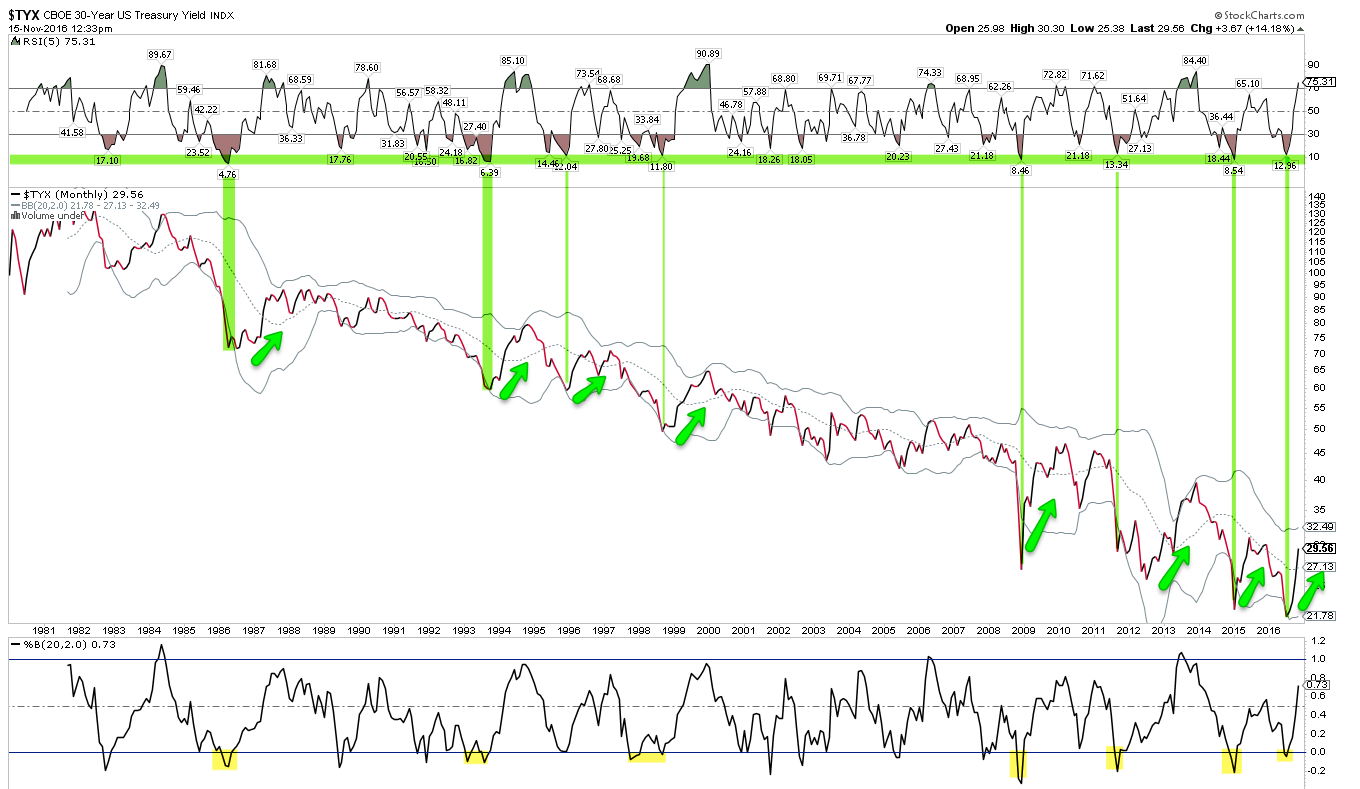

The current rise in yields began this summer from the bottom of a 35 year declining channel (chart above). At that point, the momentum of decline had reached an extreme that had previously been close to a low in yields at least 7 other times in the past (in the chart below, top panel and green line). Like now, yields rebounded higher each time (arrows).

Objectively, yields could now just be reacting to an "oversold low" as they have many times before. It's too early to say otherwise.

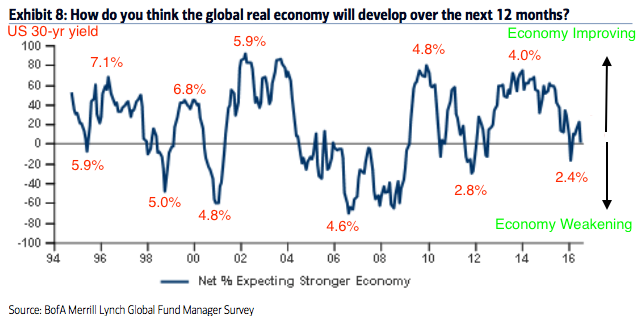

It's worth pointing out the importance of investor psychology in the movement of rates over the short term (measured in months). Right now, the prevailing opinion is that a secular low occurred this summer. Well, what did money managers think about this at the time of that low? In short, they didn't believe it at all.

In July when the 30 year dropped to 2.1%, fund managers surveyed by BAML had their highest exposure to bonds in more than 3-1/2 years. Just 2% believed that the global economy would improve over the next 12-months (chart below). In other words, they were convinced that yields would continue to move lower. Instead, they reversed much higher. That pattern of swinging investor psychology has played out consistently over the past decade and at each inflection point, yields have reversed (numbers in red are US 30-year yields). Read more about this in a post from July here.

Momentum has room to run higher, carrying yields higher. Momentum is just starting to reach an extreme now (red line and top panel). This has sometimes been the top for yields but yields have just as often continued higher. In the past 35 years, most of the move higher in yields has taken place by the time momentum reaches current levels. In mid-2013, yields moved 40 basis points higher over the next 6 months before turning lower. In other words, don't count on a quick resolution to the debate about a secular low.

Investor positioning and sentiment suggests the change in the relative performance of bonds (down) versus equities (up) should continue longer.

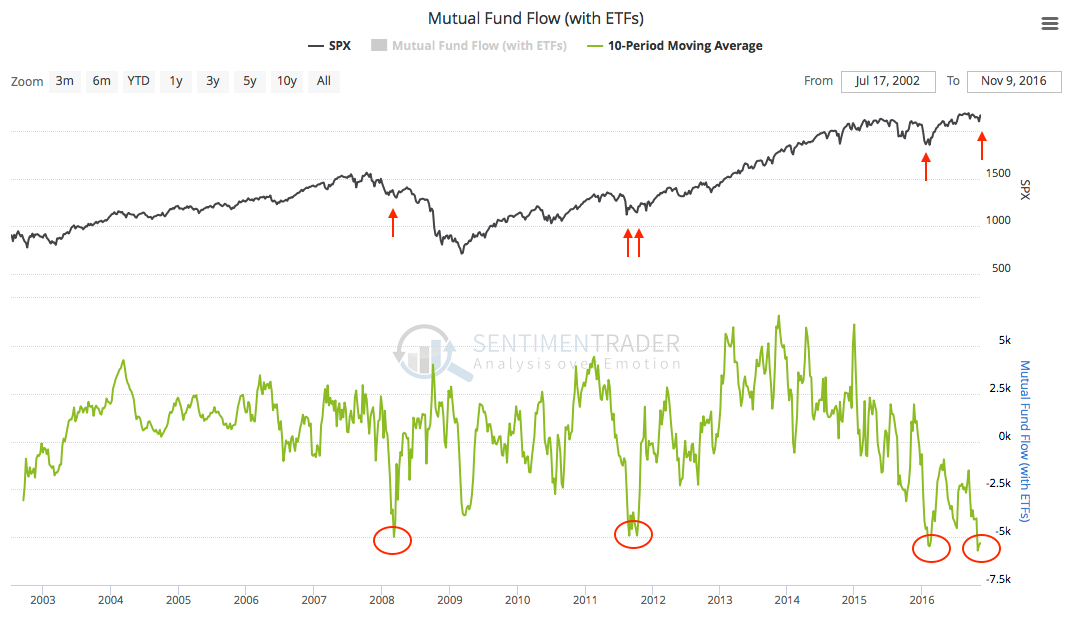

Over the past 18 months, investors' money has been flowing consistently out of equity funds. On a net basis, about $130b has left domestic equity mutual funds and ETFs. You can track that data every week

here (chart below uses data from ICI).

The dates on the chart have been meaningful for SPX. The equity index fell about 17% in the 6 months following the April 2011 peak in equity flows. The index then rose about 50% from the November 2012 low in equity flows to the March 2015 high. Since March 2015, equity flows have been negative and the equity index has been oscillating near 2100, making little net progress.

Those fund outflows have recently become extreme. The 10-week moving average is the lowest ever. It's a small sample, but after similar cases, SPX has always moved higher (arrows). The first arrow might look like it preceded a tiny rally, but SPX moved more than 8% higher in two months. A similar move now would put the index near 2275 (data from Lipper; chart from Sentimentrader).

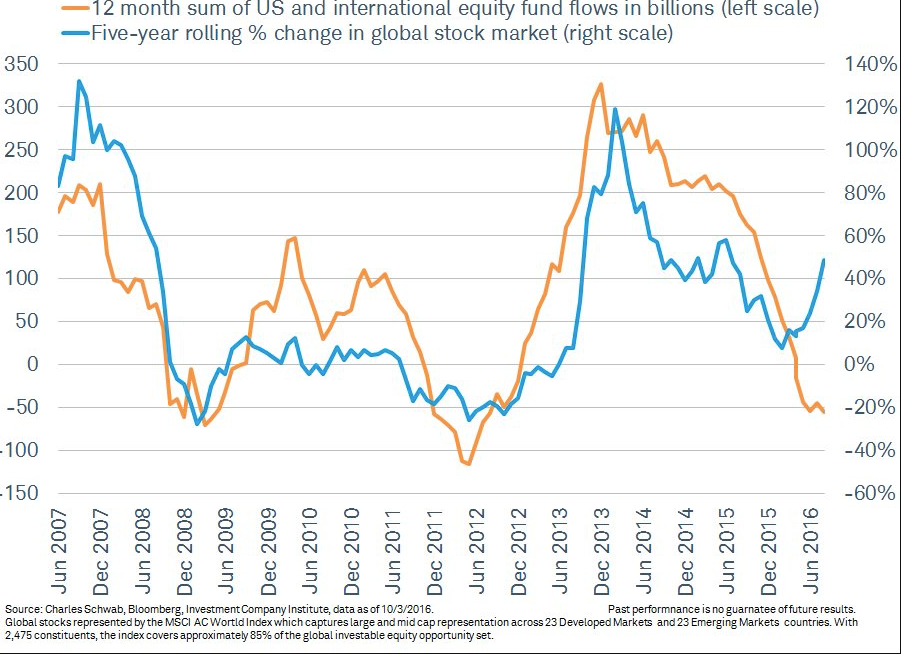

Schwab looks at the same equity fund flow data but over a trailing 12 month basis (orange line). Again, the sample size is small but their view is that this correlates well with the next 5 year change in equity prices (blue line).

As an aside, the evidence suggests that equity outflows have been mostly due to retail investors exiting. Fund flows for institutional investors has been mostly flat since early 2015 (data from the Fed).

Where has the money that has left equity funds gone? Mostly to bond funds.

In the past 45 weeks, during which equity funds have seen outflows 82% of the time, bond funds have seen inflows 71% of the time. The data is even more skewed than that because in many of those weeks, equity inflows and bond outflows were tiny.

Until July/August, favoring bonds over stocks made sense as bonds had been outperforming since early 2015. Recall, the 30-year yield marked its low in July. But since then, equities have outperformed, and since the election, bonds have been routed.

Money usually follows performance. It's a good guess that fund flows might soon begin to favor equities. If past is prologue, then equities should continue to gain and bonds should continue to sell.

The most recent data on fund managers' investment allocations agrees with the fund flow data. Last month, allocations to equities relative to bonds, commodities and cash were near the lows formed in mid-2010, 2011 and 2012. Equities moved higher and bonds moved lower (yields moved higher) at those junctures. Read more on this here (data from BAML).

One final word on equity fund flows. We will know in hindsight, but it seems unlikely the recent equity fund outflows are due to demographics. Boomers reached retirement age starting in 2011 but there was a large increase in retirement age Americans starting already in 2005. We should have seen equity outflows start earlier if demographic forces were predominant. More on demographic shifts in a new post here (data from Doug Short).

To summarize: In July, fund managers' had their highest exposure to bonds in 3-1/2 years. In other words, they expected yields to keep falling. Instead, yields reversed higher and have since risen so sharply that several smart money managers now say that a new secular uptrend in yields is taking place. That is a big call, given that the foregoing secular downtrend has lasted more than 35 years.

Over the past 18 months, investors' money has been flowing consistently out of equity funds. Where has that money gone? Mostly to bond funds. Money usually follows performance, so it's a good guess that fund flows might soon begin to favor equities. If past is prologue, then equities should gain and bond yields should continue to rise. Whether that will constitute the start to a new secular uptrend for yields it is far too early to say.

© The Fat Pitch

Read more commentaries by The Fat Pitch