Needless to say, the surprise victory of Donald Trump in the U.S. presidential election has changed the economic outlook on many fronts. With detailed policy proposals still in the early stages of formulation, the precise impact remains a matter of speculation. Nonetheless, we can formulate broad conjecture about the probable course of the economy. Our comments of last week touched on these likely developments.

Expectations about fiscal policy have taken center stage. Some version of the president-elect’s expansionary fiscal policy program, consisting of tax reductions and large scale infrastructure spending, should earn Congressional support. The consequent increase in demand, given that the output gap (actual – potential GDP) currently is small, implies higher inflation. But the impact of the fiscal plan and other policy changes will be evident only much later in 2017.

In the meantime, post-election market reaction to these expectations is visible in higher equity prices, bond yields and inflation expectations. In response, we have made important updates to our inflation and interest rate forecasts. Other economic data remained in the background as elections took the limelight. Incoming reports remain favorable, on the whole.

Key Elements of the Forecast

- Consumer spending in the fourth quarter is predicted to slightly exceed the third quarter’s performance. Auto sales during October recorded the highest mark since November 2015. October retail sales are expected to show gains across most major components. The personal savings rate has edged down in the last six months after holding around 6.0%.

- The housing sector data show improvements. Single-family housing starts rose in September to 783,000 units and erased the losses seen in the previous six months. Permits extended for both single- and multi-family units increased in September, as did sales of new single-family homes which are close to post-crisis highs. Sales of existing single-family homes also increased in September. The Pending Home Sales Index, which leads actual home sales by one to two months, moved up in September and bodes well for sales in the months ahead.

- The increase in the structures component of business spending reflects a pickup in activity in the oil and gas industry. But business equipment outlays have been weak during each of the last four quarters. The recent gain in durable goods orders and the positive monthly factory survey data suggest a likely increase in capital equipment spending in the fourth quarter.

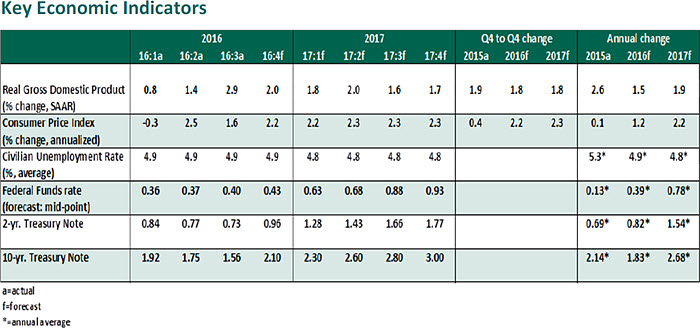

- The unemployment rate dropped to 4.9% in October, and the broad U-6 jobless rate also declined (9.5% versus 9.7% in September – the lowest since 2008). Payrolls increased 161,000, putting the year-to-date average at 188,000. The 2.8% increase in hourly earnings was a new high for the current expansion. The Employment Cost Index increased 2.3% from third quarter 2015, and is at the high end of what we’ve seen in the current expansion. These numbers suggest that labor market conditions are tightening.

- Inflation measures are moving higher. The 1.3% year-to-year change in the personal consumption expenditure price index in September represents a nearly 35 basis points increase since June. The core price gauge, which excludes food and energy, stands at 1.7%. Inflation expectations increased a little more than 20 basis points in the last week.

- The 10-year Treasury note yield is around 2.2%, which is a significant post-election increase. This is the largest gain since June 2013, when yields shot up following the Fed’s decision to taper asset purchases. The key question now is whether bond yields can stage a calm upward movement without causing setbacks to a leveraged corporate sector.

- The dollar has moved up, which spells trouble for emerging markets. The current experience may be more difficult than the 2013 “taper tantrum” because President-elect Trump’s threat of tariffs could hurt growth in emerging markets and jeopardize their ability to service dollar-denominated debt. Presidential authority allows for imposition of tariffs without Congressional approval. Markets will pay close attention to the actual institution of tariffs.

- The Federal Open Market Committee left the policy rate unchanged at the November 1-2 meeting, and the policy statement suggested the Fed’s preference for a higher policy rate at the December gathering. Markets point to a strong likelihood of this happening.

© Northern Trust

© Northern Trust

Read more commentaries by Northern Trust