THIS IS BIG NEWS!

Headline in the Wall Street Journal: “Game Over for Broker Commissions”

“Wall Street’s days of taking commissions appear numbered…. The latest move to limit commission-based accounts came this past week, when Bank of America Corp’s Merrill Lynch unit said it would do away with individual retirement accounts that charge investors for each transaction.”

This means that IRA accounts are moving into the universe of fiduciary advice. Just remember, for now traditional taxable brokerage accounts remain caveat emptor.

DEPRESSING!

According to the American Council of Trustees

(https://www.goacta.org/images/download/A_Crisis_in_Civic_Education.pdf), 10% of college grads thought Judge Judy was on the U.S. Supreme Court.

WORDS OF WISDOM

From my friend Judy…

From Little Children:

• No matter how hard you try, you can’t baptize cats.

• When your Mom is mad at your Dad, don’t let her brush your hair.

• You can’t trust dogs to watch your food.

From Adults: • Raising teenagers is like nailing Jell-O to a tree.

• Families are like fudge... mostly sweet, with a few nuts.

• Middle age is when you choose your cereal for the fiber, not for the toy.

About Growing Old:

• Growing old is mandatory; growing up is optional.

• Forget the health food; I need all the preservatives I can get.

• When you fall down, you wonder what else you can do while you’re down there.

• You’re getting old when you get the same sensation from a rocking chair that you once got from a roller coaster.

• Time may be a great healer, but it’s a lousy beautician.

• Wisdom comes with age, but sometimes age comes alone.

WORDS FAIL ME

From the WSJ… “Wells Fargo & Co. was slapped with a $185 million fine Thursday for ‘widespread illegal’ sales practices that included opening as many as two million deposit and credit-card accounts without customers’ knowledge, federal and local authorities said… In detailing the widespread nature of the bank’s alleged missteps, CFPB said Wells Fargo has ‘terminated roughly 5,300 employees for engaging in improper sales practices.’”

The good news is that management was innocent; it was just the 5,300 employees. “Wells Fargo CEO Defends Bank Culture, Lays Blame with Bad Employees.”

AND MORE

It seems Wells Fargo’s problems just won’t end. The firm is now defending a 401(k) class action suit by an employee that claims “[t]he company’s ‘criminal epidemic’ caused its stock price to tumble, leading to hundreds of millions in losses that 401(k) fiduciaries didn’t try to prevent.”

However the court rules, the real lesson in this story is the risk of concentrating your investments in the stock of your employer. In this case, approximately 34% of assets in the company 401(k), a massive $36 billion plan with more than 360,000 participants, are invested in Wells Fargo common stock, according to BrightScope Inc., a 401(k) ratings provider.

I wonder how many of the 5,300 employees who lost their job also suffered significant losses in their 401(k) savings. I thought the word was out that no one should concentrate their personal investments in the stock of their employer, but with 34% doing so at Wells Fargo, I was obviously wrong. If you face a similar choice, don’t make the same mistake. http://www.investmentnews.com/article/20161012/FREE/161019973/wells-fargo-embroiledin-401-k-lawsuit-over-cross-selling-scandal?utm_source=Morning- 20161013&utm_medium=email&utm_campaign=investmentnews&utm_visit=43405

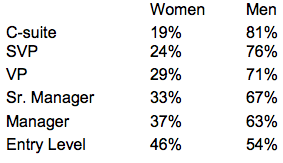

NOT GOOD

From USA Today:

That Glass Ceiling is alive and well. Percentage of employees by level:

MORE DOIN’ GOOD

My #1 Son David and Grandson Nicholas representing E&K in supporting St. Alban’s, a wonderful community endeavor with the mission to provide courteous, convenient, comprehensive, quality child care and family services. The program provides for the child’s physical, emotional, intellectually healthy development. The Coconut Grove Center currently serves 110 preschool children and 30 infants and toddlers. I am mighty proud of these two terrific young men.

CASH, PIZZA, OR ’ATTA BOY!

Dan Ariely, one of the leading lights in the field of Behavioral Finance, conducted an experiment in which three-quarters of employees were given one of three email messages at the start of the workweek. One quarter was offered a cash bonus if they met their production quota for the day, one quarter were promised a pizza, one quarter were promised a rare compliment from their boss, and the remainder did not receive an email. After the first day, the pizza offer increased production by 6.7% and the compliment group increased 6.6%, while the cash bonus only increased production by 4.9%. The real surprise was that by the second day those offered the bonus performed 13.2% worse than those receiving no email. For the week overall, the cash bonus group had a 6.5% drop in productivity. The moral is that extrinsic motivators such as cash bonuses may not actually succeed while the “sense that other people appreciate what you do sticks with you.” http://nymag.com/scienceofus/2016/08/how-to-motivate-employeesgive-them-compliments-and-pizza.html

A BIT MORE BRAGGING

I am proud of my Alma Mater:

WHILE I’M BRAGGING…

Recently Deena was invited to introduce the keynote speaker at the Schwab Impact Conference (the largest annual industry meeting). Here’s a picture. The real Deena is the little dot in the middle of the stage.

COOL SITES

• Health Care Cost Estimator at fairhealthconsumer.org provides medical and dental cost lookup tools that provide cost estimates of medical and dental services in your area and estimates of how much insurers generally cover when you visit physicians or dentists who are not in your plan’s provider network.

• Medicare.gov lets you “find and compare doctors, hospitals, & other providers”

https://www.medicare.gov/forms-help-and-resources/find-doctors-hospitals-andfacilities/quality-care-finder.html.

• Goodrx.com compares costs for drugs at local and mail-order pharmacies.

Thank you Kiplinger for these leads.

OH MY

From the Wall Street Journal:

“We Put Financial Advisers to the Test — and They Failed”

http://blogs.wsj.com/experts/2016/10/27/we-put-financial-advisers-to-the-test-and-they-failed/

This is one more reason I’m so passionate about the fight for a fiduciary standard.

“Typically, when faced with complex and important decisions we rely on trusted experts for advice. Sick people turn to doctors, those accused of crimes seek the help of lawyers, and the list goes on. These cases all have a common feature: The expert adviser must abide by a strict code of conduct that puts the interest of the client first.

“Surprisingly, the same is not always true for financial experts who advise people on their retirement savings. A majority of these professionals are not registered as financial advisers who have a fiduciary responsibility to their clients, which means putting their clients’ interest first. Instead, they are registered as brokers who only adhere to what is known as a ‘suitability’ standard, which is much vaguer and only asks brokers to make recommendations that are consistent with the client’s interest.

“In addition, the majority of brokers are not paid on the basis of the quality of their advice, but rather on the fee income they generate from their clients. To resort to a medical analogy, this is equivalent to simply prohibiting doctors from recommending drugs that kill you, while not actually requiring they prescribe the best drugs to cure your disease.

“In a study with my co-authors Sendhil Mullainathan at Harvard University and Markus Noeth at Hamburg University, we set out to analyze the quality of financial advice commonly given to clients. We sent ‘mystery shoppers’ to financial advisers in the greater Boston area who impersonated regular customers seeking advice on how to invest their retirement savings outside of their 401(k) plans. The mystery shoppers also represent different levels of bias or misinformation about financial markets. What we learned is highly troubling.

“By and large, the advice our shoppers received did not correct any of their misconceptions. Even more troubling, the advisers seemed to exaggerate the existing misconceptions of clients if it made it easier to sell more expensive and higher fee products…. As a result, we found that advisers appeared willing to make their clients worse off in order to secure financial gain for themselves. This is bad news for savers — including the many baby boomers — seeking to boost their retirement nest egg.

“But our research also suggests that the proposed fiduciary standard can be beneficial. Indeed, we found that advisers who have a fiduciary responsibility toward their clients provided better and less biased advice than those that were merely registered as brokers.”

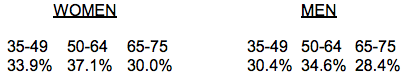

THE SANDWICH GENERATION

From the Wall Street Journal: Percent of families with living parents and adult children who provide time and dollar resources to both generations.

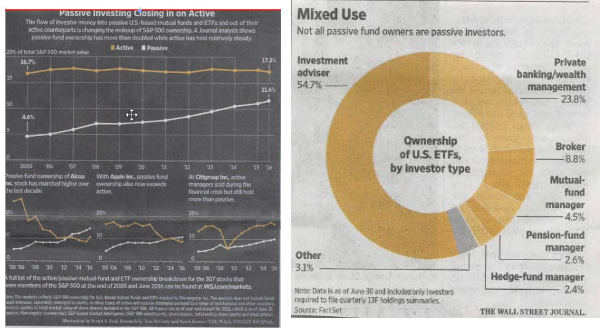

PASSIVE INVESTING ON THE RISE

We are pleased to have been a pioneer in this area.

Hope you enjoyed,

Harold Evensky

Chairman

Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management

© Evensky & Katz / Foldes Financial Wealth Management

Read more commentaries by Evensky & Katz / Foldes Financial Wealth Management