Call it Brexit 2.0: American Edition.

Like their British counterparts, who voted in June to cut ties with the European Union (EU), American voters resoundingly rejected globalism this week, calling into question the United States’ involvement in military alliances such as the North Atlantic Treaty Organization (NATO)—which is 72 percent funded by U.S. tax dollars--and international trade deals, from the North American Free Trade Agreement (NAFTA) to the Trans-Pacific Partnership (TPP). Over the course of his campaign, Donald Trump sharply criticized such groups, vowing either to renegotiate the terms or pull out of them altogether. The future of the Paris climate agreement, ratified by over 100 countries as of this month, has also been thrown into uncertainty.

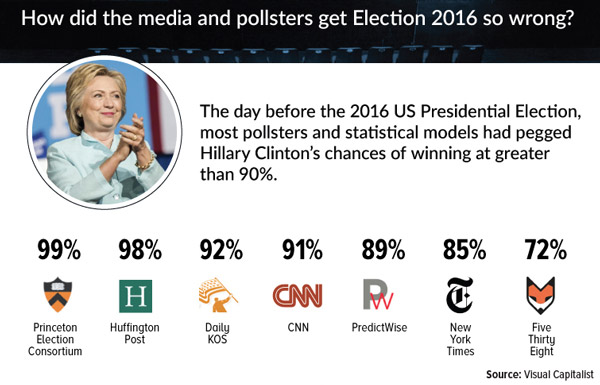

We all remember how Brexit was inaccurately predicted, with polls saying the referendum would fail. In a modern-day equivalent of “Dewey Defeats Truman,” U.S. polls also got the presidential election spectacularly wrong, missing the forest for the trees. Many polls, including CNN, Huffington Post and the Princeton Election Consortium, had Clinton’s chances of winning above 90 percent.

But in a reverse example of the so-called “Bradley effect,” which I shared with you before, people told pollsters one thing but did the exact opposite in the privacy of the voting booth.

U.S. voters largely repudiated political correctness, the Washington establishment and a biased media. They demanded sweeping, fundamental changes, and yet another Clinton or Bush just wasn’t the person for the job.

Zero Hedge quoted Nassim Taleb, scholar and author of “Black Swan: The Impact of the Highly Improbable” who put into words this frustration:

What we have been seeing worldwide, from India to the UK to the US, is the rebellion against the inner circle of no-skin-in-the-game policymaking “clerks” and journalists-insiders, that class of paternalistic semi-intellectual experts with some Ivy league, Oxford-Cambridge, or similar label-driven education who are telling the rest of us 1) what to do, 2) what to eat, 3) how to speak, 4) how to think… and 5) who to vote for.

In an interview on NPR, Alfonso Aguilar of the Latino Partnership for Conservative Principles spoke about the somewhat surprising election results, particularly among Latino voters, who were expected to hinder Trump’s chances of winning, especially with Trump’s comments about Mexican immigrants and immigration proposals. However, Aguilar commented that the reason 29 percent of the Latino vote went to Trump was because of the same issues cited by other American voters, namely jobs and the economy.

Congratualtions, Readers

|

National polls and financial publications might not have gotten it right, but you did. In an October 31 Frank Talk poll, I asked who you predicted would win the election. A third of you said Hillary Clinton, the other two thirds, Donald Trump. Our readers joined some neural network models and Jeffrey Gundlach, the DoubleLine Capital CEO and a Ph.D. mathematician, as some of the few who accurately predicted the outcome, beating the mega media channels.

World markets appeared to have wagered Clinton would win, judging from the selloff that ensued after it became clear Trump could pull off an upset. The one notable exception was Russia, as hopes improved that the U.S.—led by Trump, who has expressed admiration of Vladimir Putin—would lift economic sanctions against the Eastern European country.

Domestic stocks, however, were pointing to a Trump win all along, echoing the presidential election cycle that I’ve written about many times. In the three months ended October 31, the S&P 500 Index fell about 2 percent, and even more recently, the S&P 500 closed down for eight days in a row, the longest losing streak since October eight years ago. Historically, any loss during this period has foreshadowed a victory by the non-incumbent party candidate.

Social Media: The Great Disruptor

America just endured its first presidential election in which the majority of the electorate got its news from social media, says AdAge.

|

Those worried about the bias of mainstream media need not worry, as it seems a majority of voters were paying more attention to discussions being had, and news being posted, on non-unionized social media. Both candidates utilized social platforms. Trump’s Twitter account in particular gave a no-frills view of his personal thoughts throughout the entire campaign…to all of his 14 million followers.

A Reuters article explains the cost effectiveness of social media on the campaign trail, saying Trump’s win has “upended prevailing concepts about the influence of money in American politics and raised question of whether a lean, media-savvy campaign can become the new model for winning office in the United States.” In fact, Trump is approaching, or may have passed, $100 million from donors who have given “small” donations of $200 or less, reports Politco.com. This surpasses the small donations made throughout the campaigns of many Democrats before him – the most memorable, perhaps, being Barack Obama’s.

The Winners and Losers

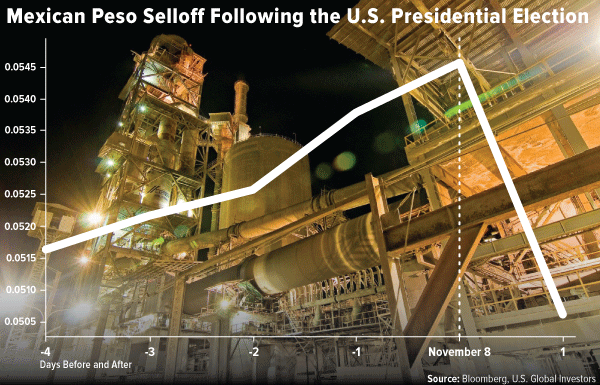

Like the British pound following Brexit, the Mexican peso tumbled dramatically, dipping to a record low on the heightened possibility that Trump, with the cooperation of a Republican-controlled Congress, would tear up NAFTA and make good on his promise to build a “big, beautiful” wall along the nearly 2,000-mile U.S.-Mexico border. Such a wall is estimated to cost between $15 billion and $25 billion.

Infrastructure names such as Vulcan Materials and Caterpillar rallied Wednesday morning. Other winners included drug makers and pharmaceuticals, driven by the apparent relief that price controls would not be imposed under a Clinton administration. Private prison stocks such as Corrections Corp. and GEO Group also surged, as did global defense firms Northrop Grumman, Lockheed Martin and Raytheon.

A Trump presidency could be good news for the financial industry. Back in August, Trump announced that, if elected, he would place a “temporary moratorium” on new financial regulations, such as the Labor Department’s fiduciary rule, which regulates how financial advisors service clients. In fact, as laid out in Trump's first 100-day plan, he wants to implement a rule that eliminates two regulations for every one new regulation. As I’ve written about previously, this is very similar to what former Canadian Prime Minister Stephen Harper proposed – Canada’s “One-for-One Rule” introduced in April 2012.

If Trump has his way, taxpayers will be winners also. Many economists agree that cutting taxes will be good for corporate earnings, and by extension, the investing public. As Deutsche Bank points out, the Republicans want to “lower the effective corporate tax rate and try to stimulate growth and hopefully this causes the tax cut to pay for itself over time.”

Going forward, losers could include multinational technology firms that manufacture some or all of their products in China (Apple and Microsoft, for instance) and retailers that mostly sell Chinese-made goods (Walmart). The new president-elect has expressed interest in levying tariffs on Chinese imports, which, I was surprised to learn, he could very well do through the Office of the United States Trade Representative (USTR) and Commerce Department.

This would certainly push inflation up—raising prices on everything from TVs to iPhones to shoes to houseware—which in turn could light a fire under the Fear Trade.

Gold Swings on Trump Victory

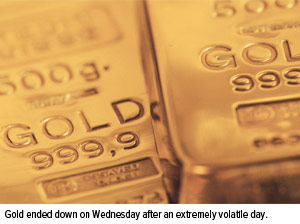

Gold had a phenomenally volatile day Wednesday, the biggest since Brexit. It rose as much as $60, breaching $1,300 an ounce, before ending the day down after U.S. equities rose and the dollar strengthened.

|

Now that the initial shock of Trump’s win is over, the next big test for the yellow metal’s movement is the possibility of a December rate hike. Although gold continues to find support from low to negative government bond yields, we can likely expect the metal to remain relatively flat, at least until we know what the Federal Reserve’s next move will be.

As I shared with you in last week’s Investor Alert, HSBC analysts predict a Trump win will be extremely bullish for gold. According to analyst James Steel, Trump’s “protectionist” policies could have a negative impact on global trade and increase federal deficits, which would be supportive of gold. The bank sees gold rising to as high as $1,500 an ounce by year-end.

In events reminiscent of 1997 and 2006, we are seeing an unwinding of the carry trade, which is putting pressure on gold. Investors have been buying Japanese debt at 0 percent interest rates, to buy gold and emerging markets. But now Japan is calling in its debts, causing investors to sell their gold and emerging markets investments.

In this environment, investors can keep in mind that short- term municipal bonds have been much more stable than two-year and five-year government bond yields, especially with the probability that the Fed will raise rates next month.

I invite you to join our upcoming webcast on gold, taking place next Thursday, November 17, at 3:30pm CT. I hope to share further insight into the world of gold and how the landscape is evolving – from the presidential election, to political events around the world, to the rise of complex algorithms influencing our daily lives. We believe that gold remains attractive for investors worldwide and hope that you’ll join in.

Recognizing Other Leaders

This week, while I was in Melbourne to present a keynote address during the International Mining and Resources Conference, I also had the pleasure of presenting Mines and Money’s 2016 Legend in Mining award to Jake Klein, Executive Chairman of Evolution Mining. Jake, who formerly worked in the commodities division of Macquarie Group, got his start in the mining industry after making several visits to mines and smelters in China. He and two of his colleagues started the company called Sino Mining in 1995, where he was president and CEO. The company grew and was later sold for more than AU$2 billion. After this, he joined Conquest Mining, a small Australian company, which later became Evolution Mining, one of Australia’s rapidly growing gold mining companies.

Jake was nominated by previous winners of the award as well as by members of the Australian investment community. Congratulations again!

It has indeed been an eventful week. Today, however, is an important time to reflect not only on our country’s future but also on how we got here. Today we honor our military veterans, the men and women who have served this country, fighting for our rights, perhaps the most important being the right to vote. We thank you for your service and celebrate the patriotism each and every one of you have displayed for the people of this nation.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 5.36 percent. The S&P 500 Stock Index rose 3.80 percent], while the Nasdaq Composite climbed 3.78 percent. The Russell 2000 small capitalization index gained 10.22 percent this week.

- The Hang Seng Composite gained 0.09 percent this week; while Taiwan was down 1.22 percent and the KOSPI rose 0.12 percent.

- The 10-year Treasury bond yield rose 37 basis points to 2.15 percent.

Domestic Equity Market

Strengths

- Financials was the best performing sector for the week, increasing by 11.33 percent vs an overall increase of 3.77 percent for the S&P 500.

- Nvidia was the best-performing stock for the week, increasing 30.19 percent. The maker of graphics chips used by computer gamers soared to a record high after giving a fourth-quarter sales forecast that shows continued strong demand for its signature products and gains in new markets such as data centers.

- Nordstrom had a great quarterly report. The retailer beat on the top and bottom lines, earning an adjusted $0.84 a share on revenue of $3.54 billion. The results capped off a strong week for the retail space as Kohl's, Macy's, and Ralph Lauren also topped estimates.

Weaknesses

- Utilities was the worst-performing sector for the week, falling by 4.08 percent vs an overall increase of 3.77 percent for the S&P 500.

- TripAdvisor was the worst-performing stock for the week, falling 19.85 percent. More than the earnings miss, TripAdvisor’s warnings over future margins led to the stock’s free fall on its results day.

- Mylan had an awful quarter. The maker of the EpiPen announced a net loss of $119.8 million for the third quarter because of a proposed $465 million settlement with the U.S. Department of Justice and other government agencies.

Opportunities

- Trump said he will roll back regulation on banks and other businesses. That would be a boon for bank stocks.

- Priceline beat on its earnings report. The travel-booking site earned an adjusted $31.18 a share as revenue jumped 19 percent to $3.69 billion.

- Economists comment that Trump is not a supporter of net neutrality. Republicans seem to oppose any effort to establish a competitive market for broadband. Presumably, large wired broadband providers such as AT&T could prosper under such a regime.

Threats

- Yahoo warned that Verizon may back out of their deal because of the massive data breach. In the "risk factors" portion of its quarterly filing disclosed on Wednesday, Yahoo said, "Verizon may assert, or threaten to assert, rights or claims with respect to the Stock Purchase Agreement as a result of facts relating to the Security Incident and may seek to terminate the Stock Purchase Agreement or renegotiate the terms of the Sale transaction on that basis."

- Rental car company Hertz collapsed after abysmal earnings. The firm posted earnings per share of $1.50 per share against analyst estimates of $2.73. The stock fell nearly 50 percent to start the day after reporting, but ended down only 25 percent.

- CVS tanked after poor earnings. The pharmacy and retailer dropped over 11 percent in trading on Tuesday after lowering its earnings forecast and posting net revenue below expectations. CEO Larry Merlo cited "slowing prescription growth" as the reason for the lower guidance.

The Economy and Bond Market

Strengths

- Job openings rose in line with expectations and layoffs are at a record low. The Job Openings and Labor Turnover Survey (JOLTS) report showed job openings in the U.S. rose to 5.486 million and layoffs and discharges as a percentage of total employment fell to 1.1 percent, the lowest since 2001.

- The University of Michigan Sentiment preliminary survey for November came in at 91.6, higher than the expected 87.9.

- Initial jobless claims fell more than expected. Claims, which count people applying for unemployment insurance for the first time, dropped to 254,000 last week. The current level is near the lowest since the 1970s, and marks 88 consecutive weeks of claims below 300,000.

Weaknesses

- Treasuries got slammed this week. The U.S. 10-year Treasury yield went from 1.77 to 2.15 on the back of deficit spending expectations during the new Trump administration.

- In the latest Bureau of Labor Statistics, the labor force participation rate, or the share of Americans working or actively looking for work, declined slightly to 62.8 percent. Further, the employment-population ratio, defined as the share of the population working, was just 59.7 percent -- down from 63.3 percent 10 years ago.

- There is a lot of uncertainty given the lack of clarity about Trump’s policies.

Opportunities

- October CPI will be reported on Thursday. The expectation of 0.4 percent, higher than the previous 0.3 percent, would be a confirmation that inflation is indeed picking up, something long sought after by the Fed.

- Municipal bonds have historically weathered periods of economic uncertainty with much less volatility than treasuries. Given the uncertainty around the Trump administration’s policies, municipal bonds may offer a safe haven.

- Industrial production is expected to come in at 0.2 percent, ahead of the previous 0.1 percent. That would provide economic momentum going into year-end.

Threats

- BCA Research’s U.S. 10-year Treasury fair value model, based on a linear regression of the 10-year Treasury yield on global growth, global growth divergences, and economic uncertainty, places fair value at 2.26 percent. As such, BCA recommends remaining short duration.

- Trump's election has Wall Street questioning the future of the Federal Reserve. Jefferies economist Sean Darby said that in terms of possible problems for the economy, going forward the "main risk is monetary policy uncertainty."

- HSBC says a U.S. recession is coming. Kevin Logan, the bank's chief U.S. economist, says that while Trump's tax cuts might help in the short run, "the combined supply shock from a contraction in the labor force and from a disruption to international trade would likely put the economy into a recession after a year or two."

Gold Market

This week spot gold closed at $1,226.35, down $78.25 per ounce, or 6.00 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week down by 15.12 percent. Junior miners outperformed seniors for the week, as the S&P/TSX Venture Index fell just 5.08 percent. The U.S. Trade-Weighted Dollar Index finished the week down 1.99 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Nov-10 |

U.S. Initial Jobless Claims |

260k | 254k | 265k |

| Nov-11 |

Germany CPI YoY |

0.8% | 0.8% | 0.8% |

| Nov-13 |

China Retail Sales YoY |

10.7% | -- | 10.7% |

| Nov-15 |

Germany ZEW Survey Current Situation |

61.6 | -- | 59.5 |

| Nov-15 |

Germany ZEW Survey Expectations |

8.1 | -- | 6.2 |

| Nov-16 |

U.S. PPI Final Demand YoY |

1.2% | -- | 0.7% |

| Nov-17 |

Eurozone CPI Core YoY |

0.8% | -- | 0.8% |

| Nov-17 |

U.S. Housing Starts |

1155k | -- | 1047k |

| Nov-17 |

U.S. Initial Jobless Claims |

256k | -- | 254k |

| Nov-17 |

U.S. CPI YoY |

1.6% | -- | 1.5% |

Strengths

- The best-performing precious metal for the week was palladium, up 7.56 percent. The strength in palladium is seen as an indicator of improving manufacturing and automobile demand, since its primary use is in catalytic converters.

- Pollsters weren’t the only ones to get the election outcome wrong, as demonstrated by the uncertainty and volatility in the gold market this week. Hedge funds last week betted that the metal would rally for the second-straight week, and Citigroup Inc. analysts predicted that a Trump victory would push gold to $1,400, while a Clinton victory would send prices down to $1,250. However, as the results were posted early Wednesday, gold had its heaviest-ever trading day, surpassing the volume on June 24, after Britain decided to leave the European Union. Gold surged at the start of the day, and gold dealer Sharps Pixley Ltd. reported running out of bars and coins. As the day closed, gold sold off, ending the day down slightly.

- Gold Road Resources has entered into a project acquisition deal with Gold Fields for the Gruyere project. Gold Road has chosen the “best risk-adjusted path to finance Gruyere for its shareholders,” writes RBC Capital Markets.

Weaknesses

- The worst-performing precious metal for the week was silver, down 6.05 percent, with gold following closely behind, down 6.00 percent.

- The World Gold Council (WGC) reported that Middle East gold jewelry demand plunged 24 percent in the third quarter. The WGC cited high gold prices and low crude prices as the chief causes for the decline. The WGC also stated that the high gold prices and the Indian government’s push for more disclosure will cut the country’s demand to the lowest level in seven years in 2016. The negative news went on as the WGC stated that jewelry demand dropped 21 percent in the third quarter, and central banks bought almost half as much gold as a year earlier.

- Goldman Sachs analysts joined the chorus of predictions that Hillary Clinton would win the election, and based their forecast of gold at $1,280 over the next three to six months based on this view. But Bloomberg noted that the surprising Trump victory was not “enough to convince skeptics that the gold rally can be sustained,” as gold closed down for the day on Wednesday.

Opportunities

- “The state of the world is one of constant flux and uncertainty,” said Cobus Loots, CEO of Pan African Resources Plc, as he noted why investors need gold. Randy Smallwood, CEO of Silver Wheaton Corp, echoed this sentiment, as investors see gold as a store of value and will likely continue to use the metal as a hedge against global uncertainty and a potentially weaker dollar.

- BlackRock sees higher expectations for inflation of 1.75 percent, the highest level since the summer of 2015, based on the 10-year Treasury Inflation Protected Securities market. Even though interest rates may rise, the higher inflation level can be supportive of gold.

- Klondex Mines Ltd. announced a new discovery at the Fire Creek Mine. Brian Morris, the vice president of exploration, stated the underground drill results “demonstrate the robust, high-grade nature of the vein system.” Positive drill results would mean resource growth for the company.

Threats

- The Indian government made a surprise announcement to abolish 500- and 1,000-rupee notes as part of an effort to discourage black-money trade. The decision resulted in a sudden rush of gold buying, and shops stayed open until 11:00 at night to accommodate buyers. However, this initial rush is seen as temporary, and the lack of large cash notes could lower gold demand, according to India’s Bullion and Jewellers Association.

- Hedge fund manager Stanley Druckenmiller told CNBC that he sold all of his gold, saying that “All the reasons I owned it for the last couple of years seen to be ending.” Druckenmiller stated that he now has a “large bet on economic growth.”

- For gold miners, the push to cut costs has seen capital expenditure levels take a hit. Global Mining Research notes that some of the cuts may be attributable to lower prices and more efficiencies. However, for those companies that have been too aggressive in cutting costs, this could be a threat to their delivery and production.

Energy and Natural Resources Market

Strengths

- Copper, nickel and zinc all climbed to 52-week highs this week on the back of a strengthening China and the “reflation trade” resulting from the election of Donald Trump as U.S. president. These moves provide a positive indication for base metals producers globally.

- The best-performing sector for the week was the S&P 500 Steel Sub Industry Index. The index of U.S. steel manufacturers rose 17.6 percent largely benefiting from president elect Trump’s infrastructure plans and protectionist policy views.

- Freeport-McMoran Inc., the Phoenix-based copper producer, was the best-performing stock this week, finishing up 26.2 percent on the back of copper’s 11 percent weekly gain, the metal’s single largest weekly advance is 30 years.

Weaknesses

- Natural gas was a laggard this week, falling 5.1 percent as U.S. inventories rose to an all-time high. Abnormally warm temperatures this fall have not helped the commodity find a floor while the near-term weather forecast calls for unseasonably warm temperatures.

- The worst-performing sector this week was the NYSE Arca Gold Miners Index. The index of gold major miners fell 15.3 percent, stamping its worst week in over a year following the retreat in gold prices post-election.

- The worst-performing stock for the week was Silver Wheaton Corporation. The company fell 24.7 percent on the back of silver prices falling 5.7 percent in conjunction with the negative sentiment within the precious metals universe.

Opportunities

- Mining and metal stocks surged this week after the Trump win. This could be the start of a long-term bullish trend for industrial companies as infrastructure spending is at the forefront of president-elect Donald Trump’s policy plans.

- U.S. crude oil refining margins increased this quarter by 17 percent, beating out analyst expectations. Although the future path for crude oil is uncertain, this is a positive sign for U.S. oil refiners.

- Crop production in corn for the month of October was 1 percent higher than last month’s estimate, and ahead of market expectations. Futures of the commodity have reached their 100-day moving average, potentially reaching an inflection point if near-term releases come in strong.

Threats

- OPEC’s production numbers increased by 240,000 barrels per day for the month of October, posting an unexpected production increase. At a run rate of 33.6 million barrels per day, oil stockpiles will continue to build, creating greater imbalances and downward pressure on oil prices.

- The International Energy Agency warned this week of “relentless” oil supply if OPEC cannot reach an agreement. The agency said the supply overhang could run into a third year in 2017 if OPEC and the industry if the parties fail to implement production caps.

- Coal and base metals prices may fall as China tries to limit market speculation. In an effort to curb commodity price speculation, China launched a series of margin hikes on its three main commodity exchanges this week. Interference from the world’s top consumer of raw materials may result in liquidations of speculative long positions.

China Region

Strengths

- The Shanghai Composite Index rose to official bull market territory, making new multi-month highs this week even as the index briefly surpassed the 3200 mark, bucking the trend of most of other regional indices.

- Alibaba sold more than $1 billion worth of products in the first five minutes of the so-called “Singles Day” sale today. This day for “singles” in China originally aimed to celebrate singleness on the day marked by the maximal number of ones—11/11— and was initially marked by the giving of gift to oneself. The day has since evolved in China to become an occasion for massive, special one-off online sales.

- South Korean unemployment for the October period dropped to 3.7 percent from 4.0 percent, beating expectations for a 4.0 percent print.

Weaknesses

- Markets in Asia tumbled amid volatility in the wake of the U.S. elections. The rising U.S. dollar and implications of the expected U.S. Fed rate-hike in December (currently at 84 percent odds) weighed heavily on emerging markets sentiment.

- New Yuan and Aggregate financing data both came in a little bit lighter than expected. New Yuan Loans were 651.3 billion, versus 672 expected, while Aggregate came in at 896.3 billion yuan versus 1 trillion expected.

- The Chinese yuan itself continues to weaken, rising amid post-election volatility above the 6.8 level for the first time since 2010.

Opportunities

- An interesting development this week was Indian Prime Minister Narendra Modi’s intriguing crackdown on corruption by means of outlawing 500- and 1,000-rupee notes. This move, which obviously prevents the store of value in the higher-denominated banknotes, hypothetically forces transactions and the storage of wealth either into smaller denominations or some other value-storing mechanism, like gold, or—perhaps in line with many of the PM’s reforms and outreach to the rural unbanked—digital technology. It is difficult to predict precise outcomes, but in any case, the government continues to attempt to crack down on corruption.

- While there is and has been much rhetoric about China in this U.S. election cycle, some investors and analysts are expecting a pragmatic relationship between China and the Trump administration, Bloomberg News reports. The language President-elect Trump supposedly employs is seen by some, the argument goes, as “the language of a deal-maker,” perfectly amenable and relatively understandable to China.

- Next week we receive third-quarter GDP data for the fast-growing Philippines, perhaps offering investors insights from one of the earliest economic assessments of the flamboyant and controversial President Rodrigo Duterte’s new administrative policies and potential.

Threats

- The combination of the election of Donald J. Trump to the highest office in the land—with a Republican-controlled Congress to boot—and highly negative campaign rhetoric toward current and recent trade deals, may place the Trans-Pacific Partnership (TPP) at risk.

- As the market digests the results of the recent U.S. election and continues to incorporate higher expectations for U.S. rates (and thus perhaps also the U.S. dollar), there are risks of volatility and of unwinding carry trades, risky emerging markets debt, and possible declines in regional equities in Asia.

- The weakening yuan could create more potential outflows of capital from China.

Emerging Europe

Strengths

- Russia was the best-performing country this week, gaining 3.5 percent. Donald Trump’s election victory may improve relations with Russia and help the economy to recover from recession. The president-elect’s proposals to increase infrastructure spending spurred gains in mining and metal companies.

- The Czech koruna was the best relative-performing currency this week, losing 2.6 percent against the dollar. Regardless of the Trump victory, the Czech Republic’s central bank plans to remove the cap on the currency next year, a move that will strengthen the currency.

- The materials sector was the best-performing sector among eastern European markets this week.

Weaknesses

- The Czech Republic was the worst relative-performing country this week, gaining 80 basis points. CEZ, the utility company traded on the Prague exchange was the biggest laggard, losing 7.4 percent after the company reported weak quarterly results.

- The Polish zloty was the worst-performing currency this week, losing 4.6 percent against the dollar. The Czech koruna, Hungarian forint, Russian ruble and Turkish lira lost about 3 percent of their value against the dollar. Expectations that an acceleration of infrastructure spending in the world’s largest economy may lead the Fed to increase the pace of interest rates hikes weighed on developing nations’ bonds and currencies, as an increase in U.S. borrowing cost reduces the appeal of risker assets. Also, BNP Paribas head of FX strategy Daniel Katzive says that an aggressive unwinding of the carry trade is taking place and it has further to run.

- The utilities sector was the worst-performing sector among eastern European markets this week.

Opportunities

- Donald Trump does not support U.S. commitment to NATO and now Britain’s military strength and intelligence capabilities may be more in demand from European Union countries that worry about terrorism and Russian expansionism. The U.K. has the second-largest defense budget in NATO and Trump’s victory may have given Prime Minister Theresa May unexpected leverage in the coming Bexit talks.

- Wood & Company’s research team recommends overweighting Russia. Trump’s positive stance on Russia should lead to easing of sanctions and moving equity market higher, especially those stocks most sensitive to economic growth. When growth returns and fixed-asset-investment picks up, steel demand grows. Russian steel should benefit from this, says Vinay Rupareli, rmerging Europe equity sales analyst at the Wood & Company Brokerage firm.

- The prime minister of Hungary, Victor Orban, said that government must reduce corporate, payroll and personal income taxes to allow a “decisive” increase in wages, which is needed to sustain economic momentum. Budapest’s stock exchange gained 27 percent year to date, supported by the strengthening economy and improving household balance sheets.

Threats

- European leaders officially congratulated Donald Trump on his victory but some expressed reservations with his proposed polices, and scheduled an informal meeting in Brussels Sunday to assess the election’s impact. German foreign minister Frank-Walter Steinmeier said earlier on Wednesday in reaction to the Trump victory that “many things will get more difficult” for America’s allies as a result of the election.

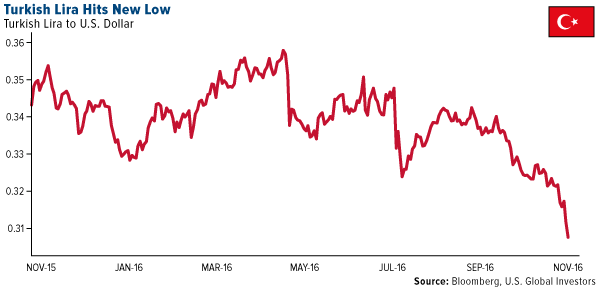

- UniCredit’s research team predicts the Turkish real GDP to contract by close to 1 percent year-over-year in the third quarter, which would be its first year-over-year decline since 2009. A drop in industrial production, along with the collapse in tourism, shrinking retail sale and political noise, weighs on growth and scares foreign investors. The lira reached a new low level.

- General elections are to be held in Romania on December 11. Politicians have been voting in favor of tax cuts and wage increases for state employees. These popular fiscal stimulus measures should have a positive effect on the economy but they are also raising the risk of a widening budget gap that could cross above the 3 percent of GDP limit.

© US Global Investors