Well I am older now but still running, running against the wind.

“Against The Wind” lyrics by Bob Seger

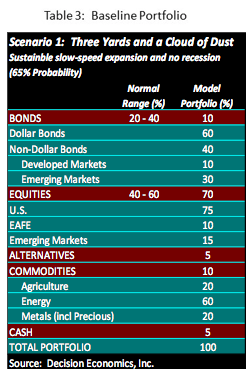

Scenario 1: Three Yards and a Cloud of Dust

The most likely investment scenario in the period ahead takes a leaf out of the playbook of Woody Hayes, the famous football coach at Ohio State University. Instead of having his quarterbacks throw long passes and gain many yards at a time, he preferred to have them keep the ball close to the ground and move it in small increments.

In the view of Decision Economics, Inc. (DE), the odds (65%) favor a grinding world economy that gains ground incrementally supported by strengthening demand, the chronological longevity of the current expansion notwithstanding. And as the old saw goes, business cycles do not die of old age, but they do fall victims to shocks, policy errors, bubbles and imbalances. Political uncertainty, especially the cliffhanger that overshadows the U.S. Presidential Election just around the corner, is always an issue whose investment implications cannot be readily quantified. Then, there is Italy’s constitutional referendum in early December, ongoing questions about fallout from Brexit, and general elections in Germany and France in 2017. Against this backdrop, policy paralysis is usually the best assumption until the dust settles.

Despite a chorus of analysts pointing to some elevated asset prices in part due to ZIRP and QE policies by central banks, presently, there appear to be no visible bubbles about to burst. (Bubbles are usually hard to quantify until they pop.) Similarly, geopolitical shocks and “Black Swans” are frequently mentioned as possible dangers to the outlook, but, they too, can only be assumed away. More importantly, the lethargic tempo of the global economy appears void of the sort of overwhelming imbalances that could lead to recessions.

Catching a “Second Wind”

Though additional evidence would be necessary to confirm it, in DE’s view the world economy, led by a cyclical rebound in the U.S. now underway is starting to catch a second wind. In the U.S., the 2.9% rebound in real GDP growth in 3Q16 represents the start of this second wind.

The bounce up is expected to stretch into 2017 and possibly beyond, sustained by the confluence of three forces. First, aggregate consumption showed some softness in 3Q2016, but is projected to rebound in 4Q16 and beyond on the back of strong consumer fundamentals, including substantial gains in employment and wage growth, and improved household balance sheets. The latter show the best financial position for the household sector ever this far along in an expansion. Second, business capital spending is expected to pick up speed as manufacturing activity rebounds and the energy sector emerges from depression. Third, federal government spending is expected to get a boost, reflecting an emerging consensus among policymakers that monetary policy has reached its limits in pumping up the economy. Fiscal stimulus seems baked- in-the-cake post-Election no matter who is elected and irrespective of the composition of Congress.

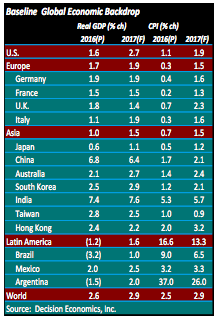

The tilt toward more fiscal stimulus is becoming contagious abroad, as well. The rise in populism in Europe has dented fiscal austerity as shown by a greater willingness to bust government budgets. Safeguarding against any adverse consequences following the Brexit vote is another reason for expanding government spending. Meanwhile in Japan, the recently announced massive fiscal stimulus program amounting to nearly 6% of real GDP is getting underway. Similarly, China is already full steam ahead with fiscal stimulus and Canada is planning on a large boost in government spending. The economic backdrop for Scenario 1, calling for a measured world economic expansion ahead is shown in Table 1.

The shift in policy in favor of more government spending is a big theme. It would help to underpin economic growth prospects which in turn would provide a second wind to stock markets. Importantly, DE is calling for a rebound in earnings, starting in 3Q16. Though still preliminary, our models show S&P 500 operating earnings per share jumping +1.2% in 3Q16 from a year earlier. If validated, this rebound would be the first positive quarter in five quarters on a year-over-year basis. DE calls for an acceleration in 4Q16 EPS growth to 3-1/2% year-over-year, followed by 6%-8% rise in 2017. The expected earnings rebound translates into $115.75 earnings estimate for the S&P 500 in 2016 and takes operating earnings to $123 plus in 2017.

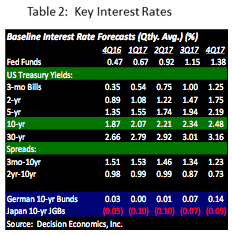

The recovery in earnings will be sufficient to take in stride relatively small increases in interest rates following an expected Federal Reserve hike in December and an uptick in inflation. Nor would the rise in interest rates pose a serious threat to overall economic activity coming from near-historically low levels. A summary of DE’s forecasts of interest rates consistent with the Baseline Scenario 1 is shown in Table 2.

In the face of the projected moderate world economic growth, relatively low inflation, measured Interest rate increases and accommodative monetary policies, DE forecasts global stock market gains led by the U.S. in the period ahead and extending into 2017. In contrast, we anticipate only a mild bear market in bonds. With oil prices stabilizing around $50/b, overall exposure to commodities is raised to 10% from previously 5%. Most of the increase reflects a larger share for energy, while portfolio exposure to agriculture and metals remains largely unchanged. The corresponding Baseline global portfolio is shown in Table 3.

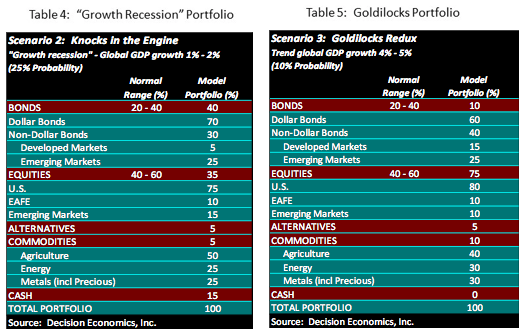

Scenario 2: Knocks in the Engine

Under a “Growth Recession” scenario (25% probability), the world economy fails to build up steam. The list of headwinds thwarting growth includes: 1) lack of response to unprecedented monetary ease as the private sector continues with balance sheet restructuring, while private credit growth remains subdued as tighter regulation and squeezed profitability restrain lending; 2) unwillingness by governments to loosen spending; 3) tepid business spending weighted down by large gaps in capacity usage across many lines of production; 4) a collapse in world trade in the face of anemic demand that undermines large export-based economies like Germany, China, and Japan. Recession, however, is held at bay thanks to loose monetary policies. This environment favors global bonds, especially since inflation expectations remain well anchored, but global equities suffer. Table 4 shows the corresponding global portfolio.

Scenario 3: Goldilocks Redux

Scenario 3 (10% probability) describes a Pollyannaish environment, where all cylinders of the world economy are firing. The revving up is fueled by a manufacturing renaissance and a substantial rise in capital spending, while government spending goes all in with large-scale expenditures in infrastructure and defense, and employment gains new vigor despite the longevity of the expansion. At the same time, interest rates stay relatively low in the face of plentiful credit availability absent any tightening of central bank policies. Inflation, however, accelerates but remains contained as a result of expanding business investment and gains in productivity. Underscored by favorable fundamentals, including a smart rebound in earnings, equities become the asset class of choice, while exposure to bonds falls. The corresponding global portfolio is shown in Table 5.

Disclaimer: This report was prepared by Decision Economics, Inc. (DE), a global macro research firm, which is wholly responsible for its content. It reflects the current opinions of DE. It is confidential and proprietary. It is for information purposes only and is not intended to be used, and may not be used, as an investment or tax advice. No express or implied representation or warranty is being made with respect to its accuracy or completeness. It is based upon sources and data believed to be accurate and reliable. Opinions and forward-looking statements expressed are subject to change without notice.

© Decision Economics, Inc.

Read more commentaries by Decision Economics, Inc.