With the S&P 500 down eight consecutive days for the first time since October 2008, many are wondering what this could mean for the rest of the year. Election jitters are pulling equities lower, and the big question is: could we see a big sell-off after the election?

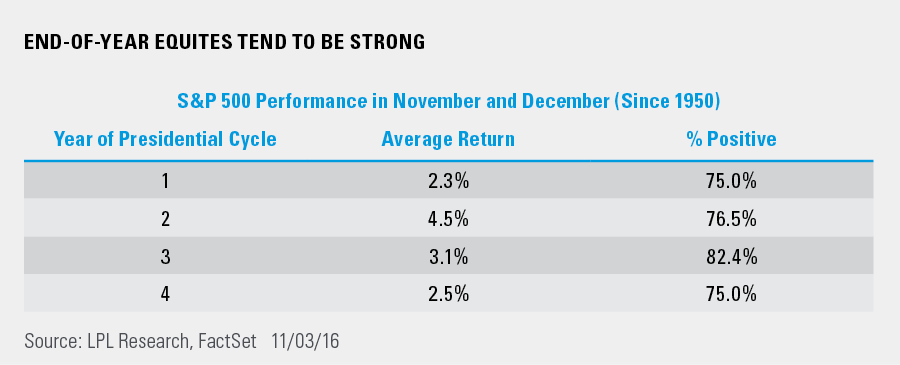

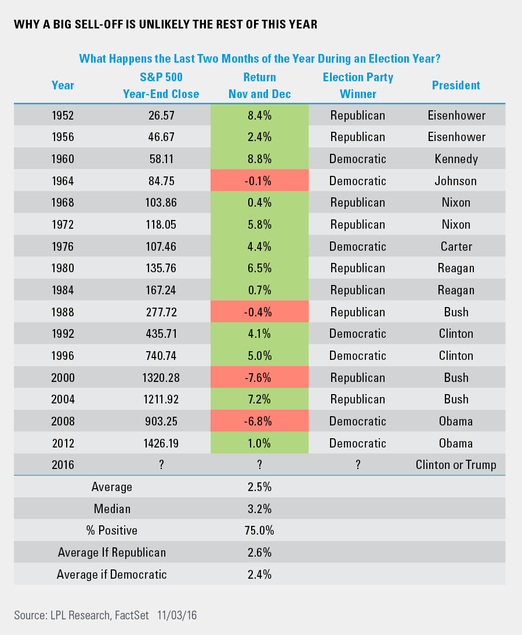

For starters, November and December are historically two of the strongest months, and this plays out in an election year as well. Going back to 1950, the last two months of the year during an election year have averaged +2.5% and been higher 75% of the time.

End-Of-The Year Equities Tend To Be Strong

Breaking it down by the party in power shows that Republicans have returned 2.6%, whereas Democrats have returned 2.4% the last two months of the year during an election year. In other words, there is very little difference in performance depending on which party wins the election. What appears to matter more is how the economy is doing. The two largest declines below were in 2000 and 2008. In late 2000, the economy was months away from a recession, while in late 2008, it was in the midst of a recession. With the economy on firm footing now, this is another positive for the rest of 2016.

Why A Big Sell-Off Is Unlikely The Rest Of This Year

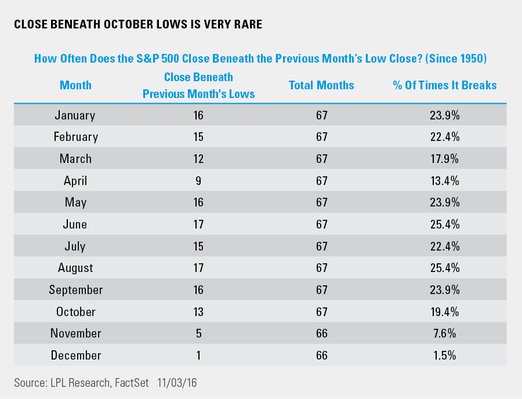

Here’s another way to look at things. The S&P 500 is currently beneath the low daily close in October (2126.15 on October 31); how often will it close the month of November beneath this level? In other words, make a “lower low.” Looking back at history, a close beneath the October low is very rare. In fact, only five times (2007, 2000, 1991, 1973, and 1950) has that ever happened. Incredibly, looking out to December, only once has the month of December closed out the month beneath the low close for the month of November—and that was in 1969. In other words, we could see some volatility, but a big drop from here is simply rather rare.

Close Beneath October Lows Is Very Rare

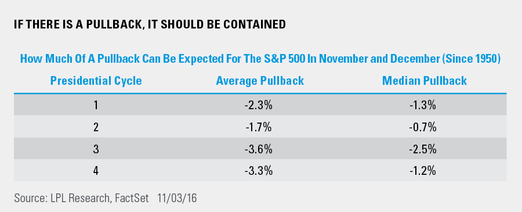

Last, should there be a pullback, how big of a pullback could we see? Again going back to 1950* and breaking it down by presidential cycle, election years see a 3.3% average drop from the end of October until the end of the year. This though is greatly skewed by a 22% drop in 2008 and an 11% drop in 2000. Turning to the median returns, an election year sees a median pullback of only 1.2%. Be aware that after three days in 2016 though, November has already pulled back 1.8%.

If There Is A Pullback, It Should Be Contained

According to Ryan Detrick, Senior Market Strategist, “Election anxieties have many on edge and questioning if we could see a big drop in equities during the rest of this year, given the recent eight-day losing streak. Well, the good news is history would say no. In fact, the only time we’ve seen large drops in the final two months of the year during an election year going clear back to the election in 1952 were in 2000 and 2008. Both of those times, the economy was a larger factor in the weakness than the election. With the earnings recession finally ending and the best gross domestic product (GDP) print in two years in the third quarter, the economy is fortunately on improving footing as we head into 2017.”

IMPORTANT DISCLOSURES

Past performance is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The opinions voiced in this material are for general information only and are not intended to provide or be construed as providing specific investment advice or recommendations for any individual security.

The economic forecasts set forth in the presentation may not develop as predicted.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal and potential illiquidity of the investment in a falling market.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

* Any data prior to March 4, 1957 is back-tested, as published by the index’s parent company, S&P DOW Jones Indices. All information for an index prior to its Launch Date is back-tested, based on the methodology that was in effect on the Launch Date. Back-tested performance, which is hypothetical and not actual performance, is subject to inherent limitations because it reflects application of an Index methodology and selection of index constituents in hindsight. No theoretical approach can take into account all of the factors in the markets in general and the impact of decisions that might have been made during the actual operation of an index. Actual returns may differ from, and be lower than, back-tested returns.

This research material has been prepared by LPL Financial LLC.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial LLC is not an affiliate of and makes no representation with respect to such entity.

Not FDIC/NCUA Insured | Not Bank/Credit Union Guaranteed | May Lose Value | Not Guaranteed by any Government Agency | Not a Bank/Credit Union Deposit

Securities and Advisory services offered through LPL Financial LLC, a Registered Investment Advisor Member FINRA/SIPC

Tracking # 1-552476 (Exp. 11/17)

© LPL Financial

Read more commentaries by LPL Financial