Regular readers are aware of our research showing that the Knowledge Effect is really a “super factor” (aka. one that outperforms considerably more consistently than more commonly recognized simple factors such as value, size, momentum, quality, or minimum volatility). Now, we take a look at what has worked best for equity investors over the last year– and how dramatically that leadership has changed in the last several months.

Each of the tables below divides all developed market companies into deciles based on their ranking for each factor (indicated in the top left) and calculates the performance of each decile group. The bottom row is the r-squared between the deciles and the performance.

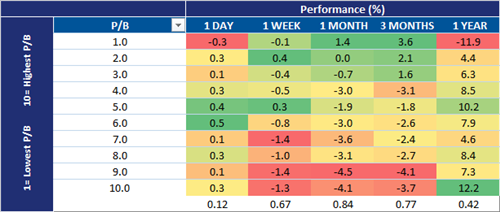

Over the last year, companies with the highest price-to-book value (P/B) outperformed those with the lowest book value by more than 24%, with an r-squared of 42%. Over the last one- and three-month periods, however, those companies with the highest P/B underperformed those in the lowest decile by 5-7% with higher r-squared values of 85% and 77%, respectively.

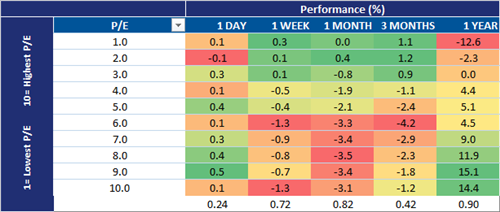

We see a similar trend for price-to-earnings (P/E).

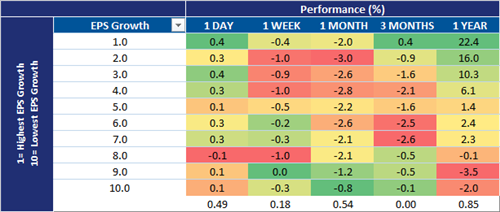

With respect to earnings growth, companies in the top decile outperformed the lowest decile by nearly 25% over the last year (with an r-squared of 85%). More recently, those companies with the highest earnings growth have underperformed those with the lowest earnings growth (with an r-squared of 54%).

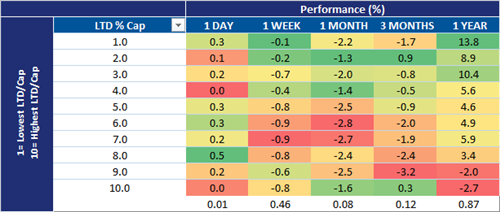

Companies with the least amount of debt on their balance sheets have outperformed those more highly levered by 16.5% since a year ago, with an r-squared of 87%. In the last quarter, companies with more debt have outperformed by a slim margin (2%) with an r-squared of just 12%.

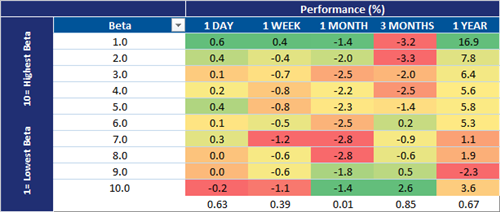

Outperformance of lower beta companies versus the highest beta companies has exceeded 20% over the last year, with an r-squared of 67%. In the last three months, higher beta companies have outperformed by nearly 6% with an r-squared of 85%.

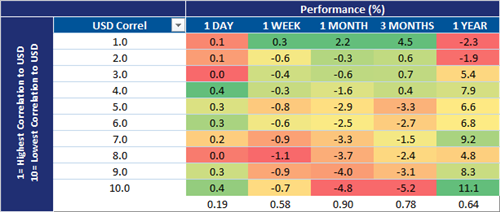

Companies with a higher correlation to the U.S. dollar underperformed those with a lower correlation by more than 13% over the last year, with an r-squared of 64%. That trend has flip-flopped, with those more correlated to the USD outperforming the lowest decile by 7-10% over the last one- to three-months (with r-squared of 90% and 78%, respectively).

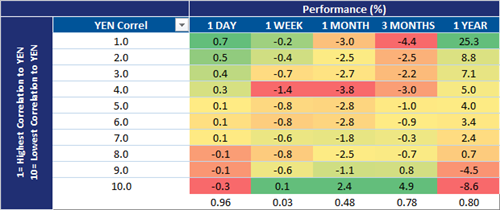

We see a similar trend with respect to equities’ correlation to the Japanese Yen. Those with a higher correlation have tended to outperform over the last year (with an 80% r-squared) while those with a lower correlation to the JPY have outperformed over the last one- and three-month periods.

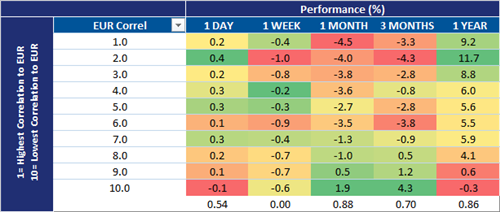

The opposite is true when it comes to correlations with the euro, as companies with the highest correlations outperformed ~10% over the last year (r-squared 86%) but have underperformed over the last one- and three-months (6.4%, 88% r-squared; 7.6%, 70% r-squared, respectively).

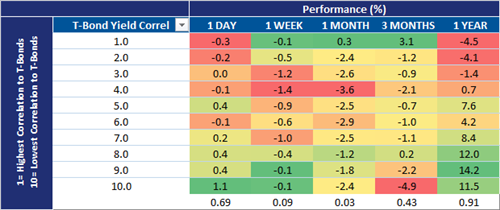

Companies less correlated to U.S. Treasury bond yields have outperformed by some 16% over the last year (r-squared 91%) but have underperformed by 8% versus the most correlated decile of companies over the last three months (r-squared 43%).

To sum up, we have seen a shift from the outperformance of high valuation, high earnings growth, low debt, low beta companies that are more correlated to USD and JPY than they are to EUR and UST yields to an environment over the last few months that is characterized by outperformance of companies with lower valuations, lower eps growth, higher debt, and higher beta with lower correlations to the USD and JPY and higher correlations to the EUR and UST yields. Translation? Investor preference has shifted from growth to value and from higher quality to lower quality companies. At the same time, investor appetite has shifted to higher beta companies that are more correlated to the EUR and U.S. government bond yields.

© GaveKal Capital

Read more commentaries by GaveKal Capital