Introduction

This piece brings together all the Private Wealth Management research teams on a topic of common interest and current importance. The following report stems from a roundtable discussion held earlier this month on the topic of Interest Rates. First, the Fixed Income team talks about the ins and outs of the global interest rate situation. Then three other teams go into detail on how the interest rate environment is impacting the position of their products.

Fixed Income

Bond yields have fallen dramatically since the beginning of the year, despite predictions that they would rise. Yield curves have flattened out, only rising for bonds with terms of three-months or shorter that saw the benefit of the 25 basis point rise in the Federal Funds rate at the end of 2015. The Federal Open Market Committee (FOMC) had suggested it would make as many as four more 25-bp rate hikes in 2016, and so far this year there hasn’t been one.

On the longer end of the interest rate curve, rates have been driven to low levels because of an expectation of a “low and slow” trajectory of short-term yields driven by the monetary policy of the Fed and other countries’ central banks, low inflation expectations, and low growth expectations.

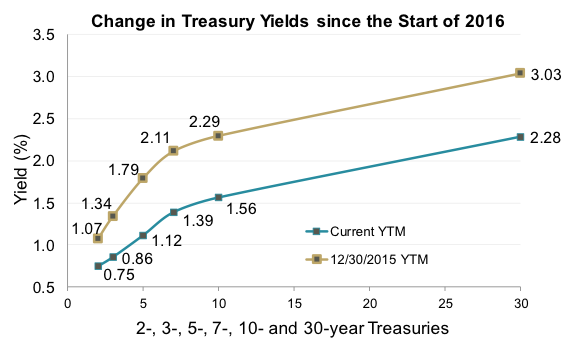

This chart shows how far current yields (teal) have come down since the beginning of the year (tan). (Source: Bloomberg)

Negative interest rates have spread across several countries’ sovereign debt, with Japan, Germany, France and Italy being the leaders in negative yields. The total amount sunk into negative yields is $10 trillion (down recently from $11 trillion, since central banks seem to have indicated they are reaching the end of their appetite for quantitative easing measures).

Foreign money flowing into the 10-year Treasury yield has helped to push yields down to 1.56%, which is 73 basis points below where the 10-year started 2016. Sustained low yields in U.S. government bonds have contributed to normally risk-averse investors entering the equity market. Some dividend-paying stocks, especially in the Utilities, Telecom, and REIT sectors, are seen as “bond-equivalents” because of the income they provide. The result is that investors are paying less attention to fundamentals, and taking on more risk than they were previously comfortable with in an attempt to maintain income levels they once expected from the fixed income market.

Following the Fed’s failure to act in September, a December hike looks more likely, if there will be one in 2016. But if the Fed raises the overnight Fed Funds rate, that doesn’t necessarily mean that rates will go up for longer-term bonds. In fact, historically, the long end has been kept attenuated because raising the Fed Funds rates decreases inflation risk and decreases the potential that short-term rates will go up in the future. However, with yields so low for such an extended period of time, the risk of them rising is high for other reasons than the Fed raising overnight rates.

Recommended Funds (PWM Asset Manager Research)

Over the past several years, net flows into passively managed investments have largely outpaced active management due to low interest rates and a fee-driven investor. With that, there are a number of inherent risks that investors may not be aware of. While market volatility will likely pick up as Fed accommodations come to an end, diminished dealer inventories have reduced trading volume, putting a strain on traditional liquidity. Traditional passive investments are weighted and positioned based on issue-size or market cap. A byproduct of that weighting in passive fixed income products is an overweight to securities of the largest debtors, in particular U.S. Treasuries and other government-related securities. This can skew the “broad market” index funds into taking more interest rate risk than an investor might be willing to incur. Low interest rates have also made it difficult to maintain a truly diversified portfolio. As the Fed has kept interest rates at low levels, many asset classes that have historically had low correlation to one another have been more likely to move in sync, reducing the benefits of traditional diversification. So how do we prudently invest given the low interest rate environment and the risks investor are exposed to?

The fixed income funds and managers on our recommended list have taken on a more defensive position in preparation for a rising interest rate environment. They have had a slight bias to higher quality issues and have maintained an underweight or neutral allocation to duration, meaning they are taking on less interest rate risk than their corresponding benchmarks. To combat increasing correlation between asset classes investors should look to provide additional diversification to their asset allocation models by pairing core fixed income strategies with alternative fixed income investments, which may include allocations to global sovereign bonds, bank loans, high yield bonds, and other non-traditional fixed income sectors. The threat of rising interest rates, reduced liquidity and higher correlations should cause investors to be more aware of downside risks and potential loss of capital. We believe the funds and strategies on our recommended list present a viable solution to mitigate those risks and enhance the client’s asset allocation.

Recommended Portfolio (PWM Equity Research)

The Recommended Equity Portfolio has been underweight the most defensive, interest-rate sensitive sectors of the S&P, such as Consumer Staples, Telecom, and Utilities. We continue to be underweight on those sectors, given the premium price-to-earnings multiples they are trading at, along with limited organic growth.

Our defensive exposure has come from Healthcare, with a current overweight exposure. The sector has underperformed the market this year, partly on the back of political rhetoric, but relative valuations appear to be at more reasonable levels. After the presidential election passes we may begin to see some of the political rhetoric fade and the focus come back to the strong operations and defensive qualities of the sector as a whole.

We are overweight in REITs (Real Estate Investment Trusts, previously part of the Financials sector, but recently reclassified as their own sector). REITs have driven solid growth relative to other yield sectors and splitting away from the rest of the Financials sector may drive additional interest to the sector as index funds look to match their benchmarks. We have been underweight the remainder of Financials slightly, especially after bank stocks ran up recently on investors’ hopes for a rate increase.

We have also been underweight Energy and Materials. Increasing interest rates could put upward pressure on the U.S. dollar, which would be negative for commodities. In addition, continued question marks over the rate of recovery in supply and demand, combined with expensive valuation multiples for premium assets continues to make us a bit cautious.

We are overweight Technology and Industrials. The Fed increasing rates would be a sign of confidence in the domestic economy, suggesting upside potential for these cyclicals.

Value Focus Portfolio (PWM Value Equity Research)

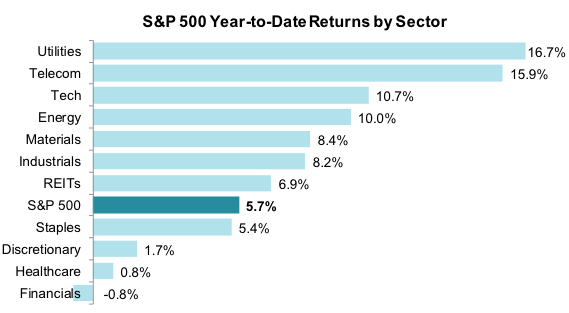

With the Value Focus Portfolio, we take a value-sensitive approach that is often contrarian. We aren’t trying to time interest rate hikes and have added names that we think can outperform over time regardless of Fed policy. However, we are underweight in Telecom, Utility, and REITs—sectors with typically high dividend yields that are sometimes treated as income assets similar to bonds. All three have outperformed the S&P 500 year to date in an environment where low bond yields have pushed investors into chasing dividend yields in the equities markets. We removed our last Utility name from the portfolio in March. The last REIT was removed in July.

This bar graph shows how higher dividend sectors like Utilities and Telecom have outperformed the rest of the S&P 500 year to date. Financials have underperformed. (Source: FactSet)

The Value Focus Portfolio has been overweight Energy all year, as we’ve been positioning for an eventual recovery in the oil markets. We are also overweight Healthcare, one of the worst-performing sectors year to date, along with Consumer Discretionary and Financials. We added a couple of positions in Financials in the last year. That move was based on strong fundamentals in an unloved sector, and took advantage of short-term volatility due to rate expectations. Conventional wisdom is that if the Fed raises interest rates, it will benefit banks—but it could take both a steepening yield curve and a sustained pattern of rising rates to meaningfully boost bank earnings.

Satellite / International (PWM Asset Manager Research)

The extended period of low interest rates has caused some deviation from historical correlation expectations. With rates being low for this long, you would have expected a weaker dollar and higher commodity prices, but global macro issues produced the opposite. Gold continues to be strong. There has been more of a negative correlation between gold and stock prices versus tracking what interest rates are doing. If we get a correction in the stock market, we might see money continue to flow into gold.

On the international front, we follow a number of value managers that have been overweight the Financials, believing the banks are in a better capital positon now. The valuations of European banks appear to reflect the fact that they aren’t as strong as U.S. banks as some still trade under book value. There’s been a lot of volatility in those names. The international managers have also struggled with valuations in the high dividend sectors like their domestic counterparts. Exposure to emerging markets, particularly Brazil, has boosted some international performance as EM has posted top equity returns year to date.

Appendix—Important Disclosures

Baird Recommended Mutual Funds: This is a stand-alone list of over 80 mutual funds across a variety of asset classes, which are selected and monitored by the PWM Asset Manager Research team. It is not offered as a managed portfolio. Investors should consider the investment objectives, risks, charges, and expenses of each fund carefully before investing. This and other information is found in the prospectus and summary prospectus, which can be obtained from your financial advisor. Please read the prospectus or summary prospectus carefully before investing.

Baird Recommended Portfolio: The goal of the Recommended Portfolio is to focus on high-quality companies with strong fundamental characteristics and management teams, attractive growth prospects, and reasonable price-appreciation expectations. The Recommended Portfolio is derived using a top-down approach starting with the macroeconomic and market outlooks, and industry sector weightings are taken into account. The Portfolio is intended as a long-term investment strategy. It is managed by the PWM Equity Research team

Baird Value Focus Portfolio: The Value Focus Portfolio is model portfolio of 30 (±5) stocks, built with the intent of helping Baird clients create and preserve wealth over time. The VFP is managed by a team of analysts take a long-term value approach to investing, often with a contrarian, opportunistic bent. The team seeks companies that trade at attractive discounts to their intrinsic value and offer favorable returns relative to the perceived risk of investing in them. The VFP includes companies with a wide range of market capitalizations, but are biased toward companies with mid-to-large capitalization (more than $1 billion). The Portfolio does not match sector weights of benchmark indices and can often be overweight or underweight certain sectors for extended periods of time. It is managed by the PWM Value Equity Research team

The S&P 500 is a stock market index that includes 500 large companies and is intended to be a representative sample of leading companies in leading industries in the U.S. economy.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation, or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make a decision about any investment strategy identified in this report.

Baird is exempt from the requirement to hold an Australian financial services license. Baird is regulated by the United States Securities and Exchange Commission, FINRA, and various other self-regulatory organizations and those laws and regulations may differ from Australian laws. This report has been prepared in accordance with the laws and regulations governing United States broker-dealers and not Australian laws.

Copyright 2016 Robert W. Baird & Co. Incorporated.

UK disclosure requirements for the purpose of distributing this research into the UK and other countries for which Robert W. Baird Limited holds an ISD passport.

This report is for distribution into the United Kingdom only to persons who fall within Article 19 or Article 49(2) of the Financial Services and Markets Act 2000 (financial promotion) order 2001 being persons who are investment professionals and may not be distributed to private clients. Issued in the United Kingdom by Robert W. Baird Limited, which has an office at Finsbury Circus House, 15 Finsbury Circus, London EC2M 7EB, and is a company authorized and regulated by the Financial Conduct Authority. For the purposes of the Financial Conduct Authority requirements, this investment research report is classified as objective.

Robert W. Baird Limited ("RWBL") is exempt from the requirement to hold an Australian financial services license. RWBL is regulated by the Financial Conduct Authority ("FCA") under UK laws and those laws may differ from Australian laws. This document has been prepared in accordance with FCA requirements and not Australian laws.

Read more commentaries by Robert W. Baird