KEY TAKEAWAYS

- Many measures of investor sentiment indicate widespread uncertainty about the direction of markets.

- The age of the bull market, U.S. elections, the possibility of a mistake by central banks, U.S. dollar strength, Brexit, and China’s debt problems all seem to have the potential to scare markets.

- Looked at in context, the current “wall of worry” is not unusual, and we believe the bull market will continue into 2017.

It’s Halloween, so what else could we do but write about what might scare the markets? We know from the financial media, measures of investor sentiment, and mutual fund outflows from equities and into bonds that investor nervousness is widespread. Some concerns are related to the presidential election, now just eight days away. Other concerns are related to the age of the bull market, discomfort with central bank actions, Brexit, and China’s debt problems; and there are certainly others. This week, in the spirit of Halloween, we discuss what might scare markets.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal and potential illiquidity of the investment in a falling market.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond and bond mutual fund values and yields will decline as interest rates rise and bonds are subject to availability and change in price.

Investing in mutual funds involves risk, including possible loss of principal.

SCARE #1: AGE OF THE BULL MARKET

The bull market and the current economic expansion are now seven-and-a-half years old, and are as long as any post-WWII cycles besides the 1990s. Some market participants believe this alone means that the U.S. economy will likely head into recession next year, ending the current bull market. But bull markets don’t die of old age; they die of economic excesses. Essentially, the gradual trajectory of the economic recovery from the Great Recession increases the chances that the expansion lasts longer.

We continue to follow a variety of leading economic indicators and are closely watching for signs of overheating in the economy that might suggest a recession is forthcoming. The latest reading on gross domestic product (GDP) for the third quarter of 2016 increases the odds that the expansion continues. The categories of excesses that have ended prior economic expansions and bull markets (overspending, overborrowing, overconfidence) remain contained. Bottom line, based on the indicators we watch, we see a low probability of recession in the next 12 to 18 months (perhaps 20%), although there is always the chance of an exogenous shock or policy mistake.*

*LPL Research is always on recession watch and we use our Five Forecasters as the advance warning system. These five data series have a significant historical record of providing a caution signal that we are transitioning into the late stage of the economic cycle and that recessionary pressures are mounting. Specifically, we monitor: the Market (using the treasury yield curve), Fundamentals (using the Index of Leading Economic Indicators, or LEI), Valuations, using the S&P 500 trailing price-to-earnings ratio, Technicals, using market breadth, and Sentiment, using the Institute for Supply Management’s Purchasing Managers’ Index, PMI.

SCARE #2: THE ELECTION

Although we list the election second, it is probably the first scare that pops into people’s minds when discussing market risks at this point. We noted in last week’s Weekly Market Commentary that there are some investments that might be hurt by a Donald Trump presidency, and others than might be hurt by a Hillary Clinton presidency. There are risks of trade protectionism, higher taxes, political gridlock (which could lead to another debt ceiling debacle), and others. Regardless of the outcome, we do not expect a major election-related market disruption for several reasons: 1) the stock market historically has performed well around elections as policy uncertainty is resolved (with 2008 a notable exception, but the worsening global financial crisis was the prominent force for financial markets in late 2008, not the election); 2) the adaptability of corporate America over time; 3) checks and balances in Washington (we expect split government to continue after the election); and 4) our belief that the U.S. economy is on pretty firm footing.

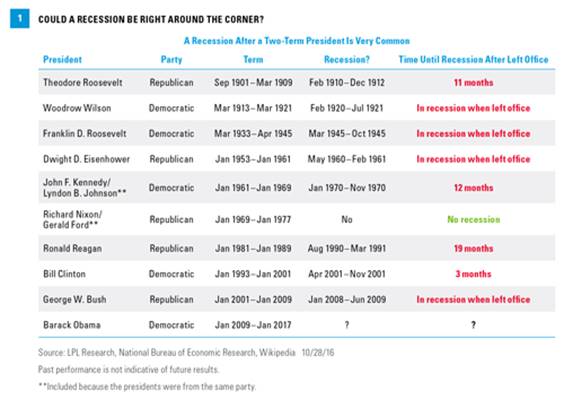

A bearish story that has popped up recently related to the election is that recessions tend to happen after two-term presidents leave office. Going back to 1900 and President Theodore Roosevelt, only twice did the economy not slip into a recession within one year of new leadership after one president was in office for two or more terms. The two exceptions were President Ford (recession came three years later) and President Reagan, who left office 19 months before a recession began in 1990 [Figure 1].

Here’s the good news — as surprising as this might be, we believe this will be the strongest economy a new president will inherit since President Bill Clinton in 1993. The reality is multiple presidents inherited rapidly deteriorating economies or recessions. With the strongest gross domestic product (GDP) reading in two years in the third quarter of 2016 (reported on Friday, October 28, 2016), consumer confidence high, and earnings growth resuming, the macroeconomic picture appears to be in good shape.

SCARE #3: U.S. DOLLAR STRENGTH

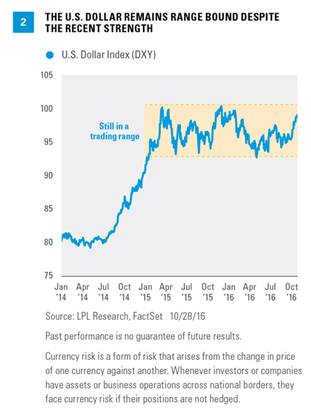

The U.S. dollar has made a big move in October 2016, hitting its highest level since early February 2016 and gaining 3.1% month to date. Improving economic growth and inflation expectations, higher interest rates, and a likely Federal Reserve (Fed) rate hike in December 2016 are among the reasons for the strength. Should dollar strength continue, earnings growth for multinationals may be impaired as it was in 2015, when the dollar rallied to a peak of roughly 20% year-over-year gains, which contributed to the earnings recession.

A strong dollar and related weaker profit growth do not necessarily mean stocks will fare poorly. During the 1950s and 1980s, huge bull markets were accompanied by a strong dollar. If the dollar goes higher for the right reasons, it can be a positive. Based on our macroeconomic view, should dollar strength continue, we think it would be for the right reasons. Further, we do not currently expect a major move higher with the dollar having been range bound since early 2014 [Figure 2].

SCARE #4: CENTRAL BANK POLICY MISTAKE

Many of the bears out there are concerned that Fed rate hikes will disrupt global markets. We believe the Fed’s transparency will enable the market to successfully digest the next hike, and probably several subsequent hikes, without a significant spike in volatility. The market believes that a rate hike in December is very likely, while a firming growth outlook gives the Fed comfort with the move. Some are worried about the emerging world’s dependence on U.S. dollar funding in a rate hike cycle — a valid concern in previous crises, though less so today given improved trade situations and greater financial flexibility that comes with unpegged currencies for most of these economies.

Also note that historically, stocks have fared well during the early stages of rate hike cycles due to the economy’s progress.* The next hike will only be the second of this cycle and, we believe, will likely be followed by several more (at least) before the next recession. Inflation is picking up gradually, but low interest rates overseas and sub-par global growth continue to cap the move higher in interest rates in the United States.

The Fed could move too fast, certainly a risk to markets (it happened in 1994, and we all remember the “taper tantrum” of 2013). Conversely, the Fed could wait too long, inadvertently allowing inflation to surge. We do not see either of these scenarios as significant risks to markets in the coming months, though they could become worrisome down the road.

Finally, at this point the size of the Fed’s balance sheet, another widespread concern, is not particularly worrisome given the central bank’s ability to hold the bonds until maturity.

*Based on 9.4% as average cumulative return for large caps 18 months after the start of Fed rate hikes over the past three cycles (February 1994–February 1995, June 1999–May 2000, and June 2004–June 2006). Based on Russell 1000.

SCARE #5: BREXIT AND THE EUROZONE

The outlook for international investments changed significantly following the United Kingdom’s June 2016 vote to the leave the European Union. This vote not only created near-term market uncertainty, leading to a 6% pullback in the S&P 500, but has also raised legitimate fears about the future of the European Union and the euro, its primary currency. Two immediate consequences of this vote have been a stronger dollar and increased likelihood of further central bank easing (the Bank of England subsequently lowered its target interest rate). This increased uncertainty and higher than anticipated currency volatility have made investments in the developed international markets less attractive, although the recent resilience of the British economy is encouraging as the weaker British pound has helped drive exports. The health of European banks is a related concern, as capital levels are generally not as strong as U.S. peers.

SCARE #6: CHINA’S DEBT PROBLEM

China’s economic growth since the 1990s was driven in large part by capital investments — building roads, factories, even entire cities. In the process, Chinese government entities, banks, and companies built up large debts. As the global economy slowed, Chinese leaders increased infrastructure investments to maintain employment, adding to the problem.

China’s debt problems are not insurmountable for several reasons. First, most of the debt is owed internally, that is, within China. China’s external debt-to-GDP ratio is under 10%, limiting external pressure and potential contagion. Further, in many instances, the Chinese government owes money to itself, because banks and borrowers are often both state-owned enterprises, making the debt levels more manageable.

The other bit of positive news is the steady growth in household banking deposits in China. The Chinese people save a lot, approximately 30% of their income, providing Chinese companies and government entities with the ability to finance their expansion without looking overseas.

The concern, assuming the debt level is manageable, is that fixing the problem could cause civil unrest. Most of the impact of these changes would be felt within China, and we believe the government would intervene in a way that would limit the global impact. Still, the numbers are scary: Chinese entities, its government, companies, and households now owe approximately $30 trillion.

Investing in foreign and emerging markets securities involves special additional risks. These risks include, but are not limited to, currency risk, geopolitical risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

NOTABLE OMISSIONS

The bears are using other arguments to scare investors to make their case, including elevated stock valuations, high margin debt, wars, terrorism, China’s currency, etc. But stock markets have climbed a wall of worry throughout their history, and we expect them to do so over the rest of 2016 and into 2017.

So don’t be scared off of your long-term plan. Happy Halloween everyone!

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

Because of its narrow focus, sector investing will be subject to greater volatility than investing more broadly across many sectors and companies.

All investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. Additional indexes, such as the S&P 500 Consumer Discretionary Index, represent GIC sector sub-indexes of the S&P, constituted of S&P 500 stocks classed within a particular sector.

The U.S. Dollar Index (DXY) indicates the general international value of the U.S. dollar. The DXY Index does this by averaging the exchange rates between the US dollar and six major world currencies.

The Russell 1000 Index measures the performance of the large cap segment of the U.S. equity universe. It is a subset of the Russell 3000 Index and includes approximately 1000 of the largest securities based on a combination of their market cap and current index membership. The Russell 1000 represents approximately 92% of the U.S. market.

DEFINITIONS

Gross Domestic Product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all of private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

Purchasing Managers Indexes are economic indicators derived from monthly surveys of private sector companies, and are intended to show the economic health of the manufacturing sector. A PMI of more than 50 indicates expansion in the manufacturing sector, a reading below 50 indicates contraction, and a reading of 50 indicates no change. The two principal producers of PMIs are Markit Group, which conducts PMIs for over 30 countries worldwide, and the Institute for Supply Management (ISM), which conducts PMIs for the US.

© LPL Financial

Read more commentaries by LPL Financial