False Security? Passive “Protection” in Emerging Markets

Investors are increasingly using passive portfolios to boost exposure to emerging markets and keep volatility under control. We see better ways to reduce the risks while sourcing returns from across the developing world.

Emerging stocks and bonds have strongly outperformed this year, as return-starved investors fled the bleaker prospects on offer in developed markets. Flows are also showing signs of life. Brightening EM economic conditions, rebounding earnings growth and attractive valuations suggest that the EM equity rally has more room to run.

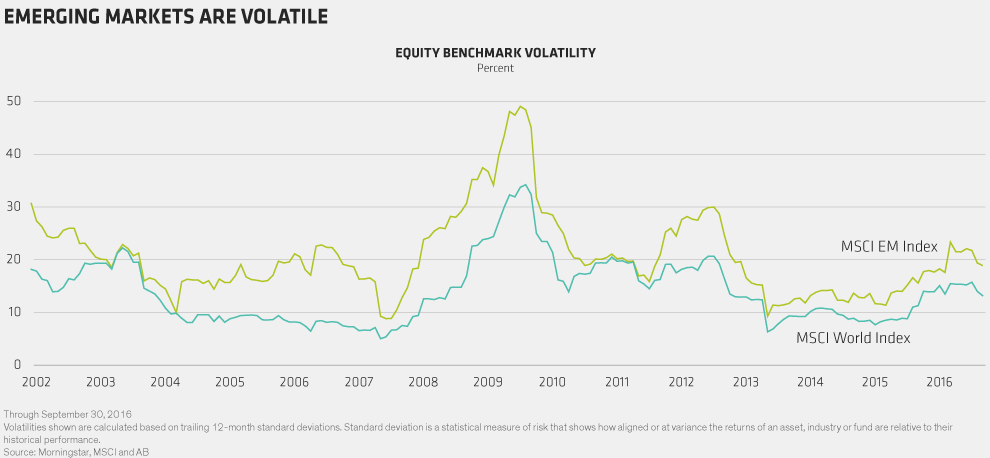

In developing markets, however, greater opportunity comes with greater risks. Though volatility across global stock markets has diminished since 2012, the EM equity market is nearly six percentage points more erratic than its developed counterpart (Display). It’s critical to stay attentive to risks that could derail performance.

THE PASSIVE SLIPPERY SLOPE

Investors manage EM volatility in several ways. Many of them have gone the passive route. Investor interest in low-volatility strategies reached a fever pitch earlier this year. Flows into the dominant low-volatility EM exchange-traded fund (ETF) surged nearly 70% to US$4.4 billion through September, twice the pickup of flows into the MSCI Emerging Markets ETF for the same period.

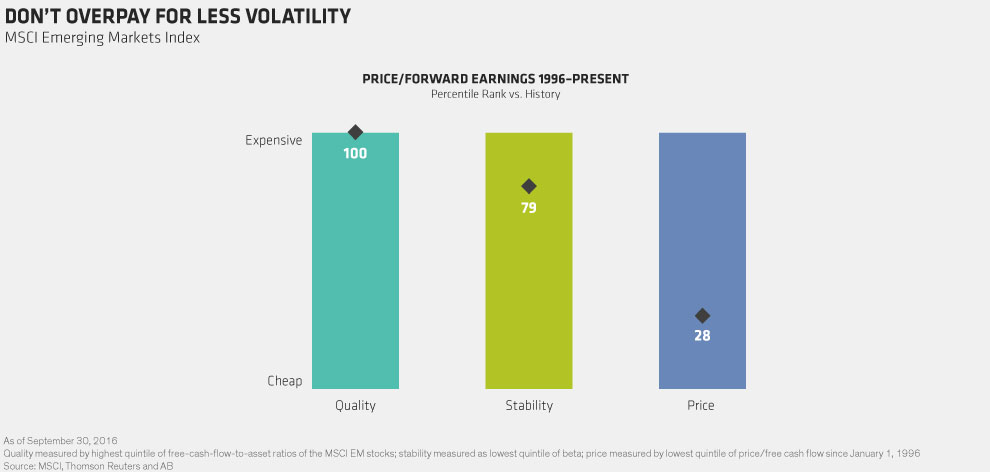

But, by tethering themselves to a low-volatility index, investors are also tethering themselves to risky concentrations in certain pricey sectors. Telecom, consumer staples and utilities stocks have massively outperformed for the past several years as investors gravitated to bond proxies offering stable earnings and high dividends. These stocks now make up one-third of the MSCI EM Minimum Volatility Index, or double their share of the MSCI EM Index, and trade at some of their highest valuations of the past 20 years (Display). They are also highly interest-rate sensitive. Because low-volatility indexes are constructed largely based on historical patterns, they can’t adapt when conditions diverge from the past. This may leave passive investors especially vulnerable to a major about-face in rates, risk sentiment or the macro climate.

Indeed, we’ve seen these vulnerabilities play out in the painful unwinding of low-volatility strategies and so-called “safe haven” stocks that began in August amid a sharp turn in risk appetites. The crowding appears to have amplified the sell-off.