So here we are, 11 days before America picks its poison, with most national polls showing a win for Hillary Clinton. If she pulls it off, she’ll become not only the first woman and first first lady to rise to the country’s highest office but also the first Democrat to succeed another two-term Democrat since Martin Van Buren succeeded Andrew Jackson in 1837.

She’ll also become the first to be under FBI investigation. Today we learned that the bureau is reopening her email case, mere days after WikiLeaks released even more damning files on the nominee. I find it interesting that back in July, eccentric internet entrepreneur Kim Dotcom predicted that WikiLeaks founder Julian Assange would turn out to be Hillary’s “worst nightmare”—a prediction that has largely come true.

Meanwhile, if Donald Trump manages an upset, he will become the oldest person ever to take the oath of office and the first to transition directly from the business world to the presidency without any past experience as a high-ranking government official (like William Howard Taft and Herbert Hoover) or military officer (like Zachary Taylor, Ulysses S. Grant and Dwight D. Eisenhower).

To Trump’s supporters and many others, of course, this is one of his main assets.

But back to the polls. In the end, they can often be misleading. I can point to several previous polls that said one thing but in the end turned out to be inaccurate, starting with those that suggested Brexit wouldn’t happen. As you know, they were way off.

In a now-classic example, California polls gave L.A. mayor Tom Bradley a wide lead in the days leading up to the 1982 gubernatorial election, and yet he was roundly defeated. Known today as the “Bradley effect,” the accepted theory is that voters told pollsters they supported Bradley, an African-American, so as not to appear racist. But in the privacy of the voting booth, those same voters pulled the lever for his opponent.

Many now wonder if a reverse Bradley effect could be taking shape in the current presidential election, with voters not wanting to admit their support for Trump—the least-liked person ever to run in U.S. history, followed closely by Hillary—but casting their ballot for him anyway.

Will this Election Buck the Trend?

I’ve written before about the presidential election cycle theory, developed several decades ago by Yale Hirsch, whose son Jeffrey serves as editor of the indispensable Stock Trader’s Almanac, now in its 50th edition. But because this year’s election breaks the mold in a number of important ways, it raises the question of how closely it will hew to past elections, at least where market reaction is concerned.

One of the most significant factors to keep in mind this year is that no incumbent’s name appears on the ballot. This is rarer than you might initially think. Since 1947, when the number of terms was limited to two, only five people have been elected twice and completed two full terms.

This two-term presidential cycle can often have a measurable effect on markets, as I wrote about in-depth in “Managing Expectations.” A president who’s up for reelection has a huge incentive to enact policies that support the economy and labor market, which investors like.

|

By the end of his second term, however, markets are faced with the reality that someone new will be occupying the Oval Office soon, complete with a new cabinet, new agenda, new governing style and new policies. This uncertainty has historically given investors the jitters—even when they’re in favor of the incoming president. (Even the most ardent Trump supporter must admit he’s more volatile and higher-risk than Hillary, who would likely maintain the status quo. But like a high-risk stock, Trump could also potentially deliver much higher returns.)

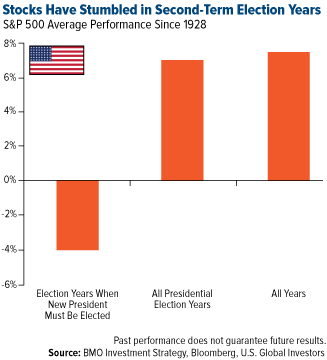

In second-term election years, then, equities dipped an average 4 percent, compared to an average increase of 7 percent during all election years.

Will we see a repeat of this in 2016? There’s no way to say for sure. But as of October 27, stocks are up more than 6 percent year-to-date. Although slightly below the average, this is much higher than returns in the last two election cycles when a new president had to be selected: In 2008, the market plunged nearly 40 percent; in 2000, it ended down 9 percent.

Looking Past November 8

|

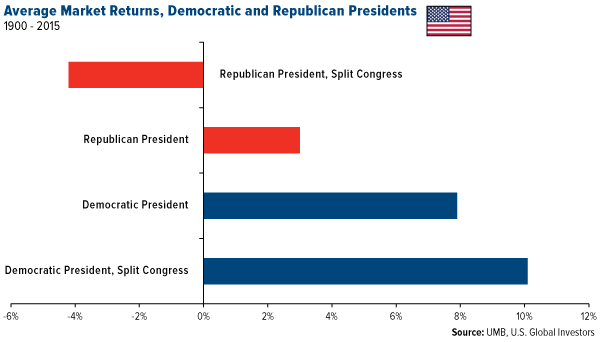

Again, it’s the policies that matter, not necessarily the party. However, there is evidence that stocks have performed slightly better when a Democrat is president, especially when Congress is split, as it was during most of Barack Obama’s administration.

Members of both parties might not like hearing this, but it’s what data mining has uncovered.

By-and-large, though, markets seem to be agnostic as to which party is in control of the White House. So many other factors exert just as much, if not more, influence over market performance, including monetary policy, inflation/deflation and whether the country is at war or peace.

Whichever way you swing, though, it’s becoming more compelling to have some of your portfolio in tax-free municipal bonds, which in the past have provided a certain level of stability in times of uncertainty.

Could Venezuela Become the Next Syria?

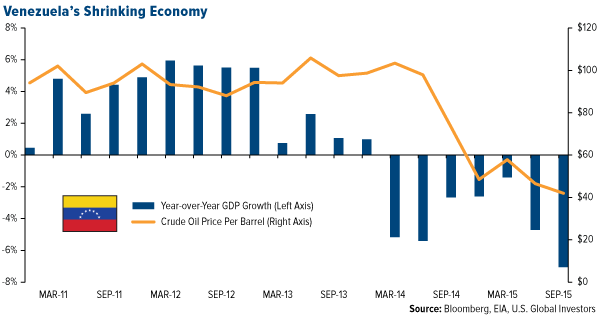

Speaking of poor policymaking, hyperinflation and violence—Venezuela is sliding closer and closer to the brink of collapse, with some sobering consequences.

This was among the topics of conversation this week at the Mining & Investment Latin America Summit in Lima, Peru. While there, I had dinner with a couple of Canadian lawyers who represented a few Latin American oil producers, some of them based in Venezuela.

Things have gone from bad to worse, they informed me. Since 2013, when Nicolás Maduro took power after the death of Hugo Chávez, the socialist country has struggled with skyrocketing inflation, food and medicine shortages, a shrinking economy and rising violence and corruption. (Its capital city of Caracas recently overtook San Pedro Sula, Honduras, for having the world’s highest homicide rate.)

These have only intensified since oil prices fell by half more than two years ago, as oil accounts for 95 percent of Venezuela’s export earnings.

Now, President Maduro has effectively suspended a scheduled recall referendum, backed by the opposition-controlled National Assembly, despite as many as 80 percent of Venezuelans in favor of his removal from office. The suspension has led to widespread protests in the streets, with accusations of a coup being tossed around on both sides.

|

The fear, the lawyers said, is that if Caracas falls, the vacuum it leaves behind would serve as a prime terrorist base of operations—a Latin American Syria, as it were, complete with the world’s largest proven oil reserves to finance it.

We’ve already seen the country cozy up to fellow OPEC member Iran, recognized by the State Department as the world’s leading state sponsor of global terrorism. According to the Gatestone Institute, a New York-based international policy think-tank, Iran is “partnering with Venezuela’s drug traders and creating a foothold” in the Latin American country.

It’s such a travesty that a nation as resource-rich as Venezuela could allow itself to rot from within. Its descent into chaos should serve as just the latest cautionary tale to other countries that are willing to risk stability and prosperity for even more socialism.

Join Me in San Francisco

Next month I will be in beautiful San Francisco, presenting at the Silver & Gold Summit, hosted by Cambridge House. I’ll be joined by many other prestigious figures in the metals and mining industry, from top analysts to mining executives to respected newsletter writers. The conference, which you can register to attend here, will be held November 14 and 15. I hope to see you there!

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average gained 0.09 percent. The S&P 500 Stock Index fell 0.69 percent, while the Nasdaq Composite fell 1.28 percent. The Russell 2000 small capitalization index lost 2.50 percent this week.

- The Hang Seng Composite lost 1.71 percent this week; while Taiwan was flat and the KOSPI fell 0.67 percent.

- The 10-year Treasury bond yield rose 11 basis points to 1.85 percent.

Domestic Equity Market

Strengths

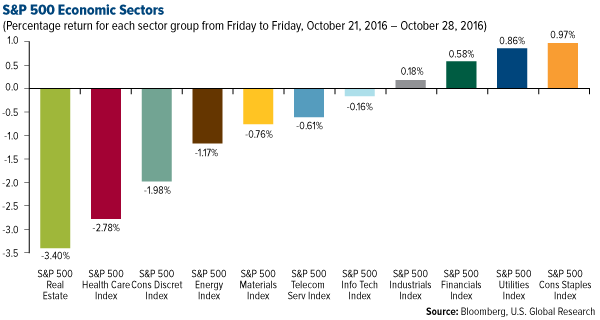

- Consumer staples was the best performing sector for the week, increasing by 0.97 percent vs an overall decrease of-0.69 percent for the S&P 500.

- Akamai Technologies was the best performing stock for the week, increasing 21.22 percent. The stock jumped in the wake of its third-quarter earnings report. The content delivery network specialist posted a 6 percent rise in revenue, with its strongest performance coming from its cloud security solutions business. With the new emphasis across the tech world on cybersecurity protection and having the strongest possible defenses against cyberattacks, Akamai has positioned itself well at exactly the right time.

- Google beat on the top and bottom lines. The search behemoth earned $9.06 per share on revenue of $18.3 billion, and said it would buy back $7 billion worth of stock. Paid clicks rose by 33 percent while cost-per-click fell by 11 percent.

Weaknesses

- Real estate was the worst performing sector for the week, falling by 3.40 percent vs an overall decrease of 0.69 percent for the S&P 500.

- McKesson was the worst performing stock for the week, falling 22.93 percent. The stock plunged after disappointing quarterly results and a downbeat outlook from management that suggested a price war is playing out in the drug distribution industry.

- The biggest initial public offering (IPO) of the year had a brutal start. Chinese package delivery company ZTO Express plunged 15 percent in its New York Stock Exchange debut.

Opportunities

- General Electric said on Thursday it was in discussion with the No. 3 oilfield services provider Baker Hughes Inc. on potential partnerships.

- Qualcomm has agreed to buy NXP Semiconductors, the world’s largest developer of chips for use in automobiles, for $47 billion in an all-cash deal. The deal is the largest in the history of the semiconductor industry. The move is seen as a big bet on the ever-increasing use of technology in cars and would lower Qualcomm’s dependence on the mobile phone market.

- Tesla reported its first quarterly profit since 2013. The electric-car maker earned an adjusted $0.71 a share after changing the way it accounts for some adjustments in its earnings. Wall Street was expecting an adjusted loss of $0.54 a share, according to Bloomberg data.

Threats

- Apple reported its first annual revenue decline in 15 years. The tech giant reported earnings of $1.67 a share as revenue fell 8.9 percent to $46.9 billion amid declining iPhone sales. Additionally, Apple Watch sales are in free fall. An estimate released by IDC shows Apple shipped just 1.1 million Apple Watches in the third quarter of 2016, down a whopping 71.6 percent from the 3.9 million watches that were delivered a year ago.

- Anheuser Busch InBev lowered its revenue forecast. The world's largest brewer had a rough quarter thanks to weakness in its Brazil business and lowered its revenue growth per hectoliter to be in line with inflation after previously suggesting it would outpace inflation.

- Southwest Airlines missed on revenue and gave a bleak outlook for a key industry metric. The revenue generated from each seat flown a mile — Revenue per Available Seat Mile (RASM) — will fall by between 4 percent and 5 percent in the fourth quarter, the company said. Third-quarter revenue and profit fell, as airlines drop ticket prices to better compete.

The Economy and Bond Market

Strengths

- New home sales rose more than expected in September, by 3.1 percent at a seasonally adjusted annual rate of 593,000. Demand for new homes is still robust amid low mortgage rates and healthy job gains. But supply continues to be a problem. Pending home sales grew by 1.5 percent, better than the forecast for a 1 percent increase. The jump brought the pending sales of single family homes, condos and co-ops to their fifth-highest level of the last year, according to the National Association of Realtors.

- Service-sector activity in the U.S. improved at the sharpest rate in nearly a year, according to Markit Economics' preliminary report for October. The flash services purchasing managers' index released Wednesday rose to 54.8 from 52.3 last month. Service providers were the most optimistic about business conditions since August 2015, as their clients became more willing to spend.

- Markit's flash manufacturing purchasing manager's index for October beat expectations, at 53.2. "Both output and new orders are rising at the fastest rates for a year amid increasingly widespread optimism that demand will pick up again after the presidential election, which has been commonly cited as a key factor that has subdued spending and investment in recent months," said Chris Williamson, chief business economist at IHS Markit.

Weaknesses

- Durable goods orders fell 0.1 percent in September, more than forecast, according to a preliminary release. The headline drop was due to a plunge in orders for defense aircraft and parts. Durable goods orders provide a window into business spending, which has contracted every quarter since the last three months of 2015.

- The Conference Board's consumer confidence index fell to 98.4 in October from 104.1 last month, which was a post-recession high. Consumers were less optimistic about current business and employment conditions.

- Personal consumption for the third quarter was lackluster, coming in at 2.1 percent vs expectations of 2.6 percent.

Opportunities

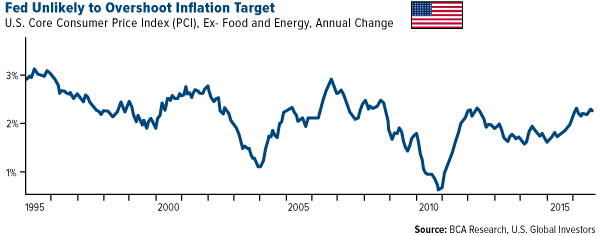

- BCA’s investment strategists believe that while PCE inflation is likely to move above 2 percent, a meaningful overshoot is unlikely. They believe core inflation is likely to drift higher as the labor market tightens and wage growth continues to accelerate. However, deflation in the goods sector will provide somewhat of an offset.

- Robust U.S. payrolls (Friday), manufacturing PMI (Tuesday,) and services PMI (Thursday) figures will be critical to confirm that the economic "soft patch" this year is coming to an end. Meanwhile vehicle sales (Tuesday) will indicate whether U.S. consumer resiliency is continuing.

- The Federal Open Market Committee (FOMC) meeting on Tuesday should provide more clarity on a December rate hike.

Threats

- A rush into higher yielding long-term bonds in recent years has created one of the most crowed trades in financial markets. Investors seeking relief from central banks’ zero interest rate policies have poured into government debt due in a decade or more. Now, according to Bloomberg, money managers overseeing more than $1 trillion say the case for owning longer maturities is crumbling. There’s mounting evidence that inflation is starting to stir, just as some central banks hint that higher long-term interest rates may be the key to boosting growth. That’s troubling because a key bond-market metric known as duration has reached historic levels, and the higher the measure goes, the steeper the losses will be if rates rise.

- Obamacare will get a lot more expensive in 2017. On Monday, the Obama administration warned that premiums for plans under the Affordable Care Act, also known as Obamacare, would soar by an average of 25 percent next year.

- BCA’s bond strategists anticipate a long-run bull market in the U.S. dollar which should act as a major headwind for U.S. dollar-denominated sovereign debt. This is because, when the dollar appreciates, it makes U.S. dollar-denominated debt more expensive to service from the perspective of a foreign issuer, and therefore causes sovereign debt to underperform domestic alternatives.

Gold Market

This week spot gold closed at $1,275.50, up $9.22 per ounce, or 0.73 percent. Gold stocks, however, as measured by the NYSE Arca Gold Miners Index, ended the week down by 3.21 percent. Junior miners outperformed seniors for the week, as the S&P/TSX Venture Index fell just 1.86 percent. The U.S. Trade-Weighted Dollar Index finished the week down 0.36 percent.

| Date | Event | Survey | Actual | Prior |

|

Oct-25 |

U.S. Consumer Confidence Index |

101.5 |

98.6 |

103.5 |

|

Oct-26 |

U.S. New Home Sales |

600k |

593k |

573kk |

|

Oct-27 |

Hong Kong Exports YoY |

-0.4% |

3.6% |

0.8% |

|

Oct-27 |

U.S. Durable Goods Orders |

0.0% |

-0.1% |

0.3% |

|

Oct-27 |

U.S. Initial Jobless Claims |

256k |

258k |

261k |

|

Oct-28 |

Germany CPI YoY |

0.8% |

0.8% |

0.7% |

|

Oct-28 |

U.S. GDP Annualized QoQ |

2.5% |

2.9% |

1.4% |

|

Oct-31 |

Eurozone CPI Core YoY |

0.8% |

-- |

0.8% |

|

Oct-31 |

Caixin China PMI Mfg |

50.1 |

-- |

50.1 |

|

Nov-1 |

U.S. ISM Manufacturing |

51.7 |

-- |

51.5 |

|

Nov-2 |

ADP Employment Change |

165k |

-- |

154k |

|

Nov-2 |

FOMC Rate Decision |

0.50% |

-- |

0.50% |

|

Nov-3 |

U.S. Initial Jobless Claims |

256k |

-- |

258k |

|

Nov-4 |

U.S. Durable Goods Order |

-- |

-- |

-0.1% |

|

Nov-4 |

Change in Nonfarm Payrolls |

175k |

-- |

156k |

Strengths

- The best performing precious metal for the week was platinum with a price surge of 5.09 percent. On Tuesday, South African news reported that plans are underway to manufacture more forklifts powered by hydrogen for local and international markets. Legislation in 2007 created the Hydrogen South Africa Strategy to develop vehicles powered by hydrogen through the utilization of the country’s platinum group metal resources.

- In a drop that could signal a buying opportunity, the net-long position in gold futures and options held by hedge funds and large speculators fell to the smallest level in more than seven months, in the third straight week of contraction. China raised bullion imports from Hong Kong for the first time in four months in September, according to data from the Hong Kong Census and Statistics Department. Investors have sought to diversify their assets while facing a weakening yuan. Net purchases were 44.9 metric tons, compared to 41.9 tons in August.

- This weekend is a key time for gold demand, with the Hindu festival of Diwali and Dhanteras on October 28, which is considered the most auspicious day of the year to buy gold. Goldman Sachs also noted that Chinese demand has potential to rise if the yuan continues to decline. Also supporting the potential for strong demand is the Indian government’s consideration of reducing its import tax on gold to 6 percent from 10 percent. This decision may take place in the third week of November.

Weaknesses

- The worst performing precious metal for the week was palladium, the only precious metal that recorded a loss for the week, with a decline of 0.55 percent. Physical demand could be weakening as it was reported in Canada that automobile and parts dealers sales declined 0.5 percent in August, the third consecutive monthly decline. In addition, S&P Global Ratings noted that in the U.S., subprime borrowers are falling behind on car loan payments at the highest rate in more than six years.

- Gold prices have been stuck in a narrow trading range of less than 3 percent, the tightest range in three years. Although physical demand in India has picked up ahead of festivals and the wedding season, investors are wary of picking up more gold while awaiting the expected interest rate increase by the Federal Reserve. Approaching the end of the month, gold may be headed for the biggest monthly drop since May.

- Gold consumption in India is set to shrink to the smallest level in seven years, at 650 metric tons. This is a significant drop, compared to 864 tons last year, and 1,006 tons in 2010. Marwhan Shakarchi, of MKS (Switzerland) SA, a Geneva-based refiner and trader, said, “In my 33 years in the market, physical demand has never been this dead.” Although gold prices have dropped about 8 percent from the two-year high in July, they are still up 20 percent this year.

Opportunities

- Platinum could get a boost from a new breed of electric vehicle. Toyota has released a new type of electric vehicle the company is calling the Mirai. Its energy is stored in a hydrogen tank rather than a battery, with a refueling time of just five minutes. With a price tag of over $50,000, Toyota expects to sell 1,000 of the vehicles this year and 3,000 in 2017. The key advantage is short refueling time relative to electric vehicles which rely on a battery power source to store energy.

- Goldman has reiterated its view that any sell-off substantially below $1,250 an ounce should be seen as a buying opportunity. Gold demand may be spurred by weakness in China’s currency and concerns over the nation’s property market. In addition, global inflation expectations have risen to the highest level since May 2015. Investors anticipate annual consumer inflation of 1.4 percent. Gold is traditionally used as a hedge against inflation.

- Mark Mobius, executive chairman of Templeton Emerging Markets Group, says he thinks gold will gain as much as 15 percent through 2017, as the Fed increases rates slowly and the dollar remains subdued. “The U.S. dollar is not that strong and may even decline,” said Mobius.

Threats

- The rush into higher-yielding, long-term bonds in recent years has become an extremely crowded trade. Money managers have noted that the prospect of rising inflation, and with high duration levels, investors may be facing steep losses in bonds.

- An ongoing legal dispute between Avocet Mining Plc and former workers from the Burkina Faso-located mine has resulted in $3.4 million of gold being seized from the mine, and the company’s shares have slumped by the most in a year, as much as 24 percent. In related news, Randgold made a $25 million advance payment to the government of Mali in their tax dispute ahead of talks to resolve the issue of alleged back taxes owed to the country.

- Chinese billionaire and Alibaba founder Jack Ma has proposed that Chinese government security should use big data to prevent crime. A draft cybersecurity law would grant the government nearly unlimited access to user data in the name of national security. Anti-terror laws that went into effect on January 1 allow authorities access to bank accounts, telecommunications and a national network of surveillance cameras called Skynet. Hmm, do you think someone did not get the English-Chinese translation of “Skynet” correct when the Terminator movies were imported? Recently, Twitter and Facebook cut off Geofeedia who was marketing aggregated user tweets and posts to provide local intelligence to law enforcement--even parsed down to zip codes or physical locations on its users.

Energy and Natural Resources Market

Strengths

- U.S. GDP hit a two-year high of 2.9 percent for the third quarter, beating expectations of 2.5 percent. This marks the fastest rate of growth in the past two years and will further boost investor confidence in the near future.

- The best performing sector for the week was the FTSE 350 Mining Index. The index rose 2.60 percent, largely benefiting from copper’s spectacular rally this week.

- Archer Daniels Midland, a major global food processing and commodities trading corporation, was the best performing stock in the natural resources space for the week. The stock finished 3 percent higher on news out of Egypt that large orders for wheat have been placed with the company.

Weaknesses

- Gold and other precious metals faced their largest outflows since 2013 out of U.S.-based funds this week in the range of $902 million. With the U.S. dollar maintaining its strength and the December interest rate hike under way, fear for safe-haven assets like gold has surfaced.

- The worst performing sector for the week was the Philadelphia Stock Exchange Oil Service Sector Index. The index dropped 5.95 percent for the week on weak crude oil prices that fell by 3.60 percent this week.

- The worst performing stock for the week in the broader natural resource space was BHP Billiton. The company fell 5.52 percent on the back of bad press. The company faces criminal charges in relation to Samarco and investors fear the liability may be greater than expected after insiders resign.

Opportunities

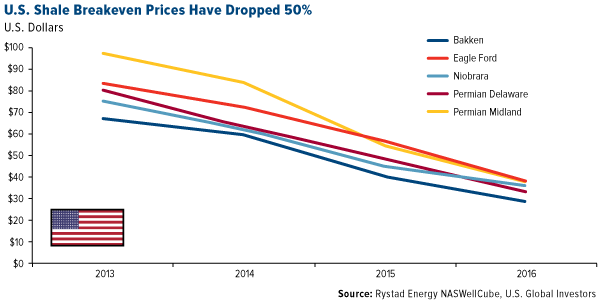

- After a two-year roller coaster ride in downward oil prices, the U.S. shale industry has officially come out on top as the biggest winner. The leaders of the group have successfully cut costs and consolidated operations to create a far more robust industry that will benefit from current and improving prices moving forward.

- The outlook for copper in the coming months is looking positive according to Macquarie’s China copper survey, which interviews smelters, traders and fabricators who are active in China. Fabricators and traders have expressed intentions to dynamically build inventories while smelters are restocking raw materials.

- Natural gas prices might have a great run this winter due to the prospect of a La Niña. Earlier this week, Desjardins Capital Markets published a note in which they outlined their outlook and key drivers for natural gas over the coming winter months. Despite an unusually warm fall in the north so far, the climatologists at the National Oceanic and Atmospheric Administration’s Climate Prediction Center are expecting this to change, which would be very positive for natural gas.

Threats

- Caterpillar continues to deliver disappointing earnings results, with a negative read-through for the resource and construction materials sectors. For the past 46 consecutive months, the company has failed to post a single month of positive retail sales—a negative signal for all natural resources.

- Last week we took a bleak view on the future of coal prices, and our view on coal has turned even more bearish. In the month of September, China consumed 311 million tons less than what was consumed in September 2015. This drop in output equates to a 20 percent decline in domestic output and accounts for a quarter of global coal trade. Neighboring major importers such as South Korea, India and Japan are all sharing a similar picture to China.

- U.S. oil producers are hedging at record levels not seen in over a decade. This is a negative read-through for the current rally in crude oil prices. To add further insult to injury, OPEC members have yet to reach a definitive and actionable agreement on a production cut deal.

China Region

Strengths

- South Korea’s year-over-year third-quarter GDP print came in at 2.7 percent, ahead of analysts’ expectations for a growth rate of only 2.6 percent.

- Once again the Hang Seng Composite’s Properties and Construction sector managed to eke out a small gain for the week—the HSCI’s only sector to do so— rising 0.3 percent even as the broader index declined 1.71 percent.

- Singapore’s unemployment rate beat expectations for a rise to a 2.2 percent print, as the bustling city-state’s actual third-quarter unemployment number came in steady at its still relatively and amazingly low 2.1 percent!

Weaknesses

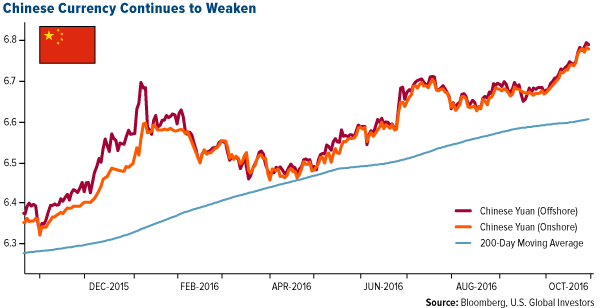

- The Chinese yuan continued to weaken this week. The onshore CNY hit 6.7868 while the offshore CNH touched 6.7987.

- Hong Kong’s troubled PAX Global Technology Ltd., an electronic fund transfer point-of-sale company, reported earnings this week and also named a new CFO—the last one had to resign after throwing an analyst out of a meeting—and still fell nearly 15 percent for the week.

- The Philippines Stock Exchange PSEi Index declined 3.21 percent for the week. President Rodrigo Duterte, who traveled to Beijing last week and collected some 24 billion in funding from China even as he announced a headline-grabbing “separation” from the United States, has since traveled to visit close U.S. ally Japan and simultaneously played down some of his rhetoric. The peso declined for the week as well.

Opportunities

- The Chinese Communist Party’s carefully crafted declaration of Xi Jinping to be its “core” provides President Xi with an elevated status and greater centralized authority, perhaps all the better to aid him in executing various reforms.

- Early next week we get PMI data out of China, as well as most other nations in the region. Official Manufacturing PMI (expectations 50.3; prior print 50.4) and Non-Manufacturing PMI for China come out early Tuesday morning, as does the Caixin China Manufacturing PMI (expectations are for 50.1; previous print also 50.1), while the Caixin China Services PMI comes out early on Thursday.

- Bloomberg News reports that the OECD is urging Indonesian authorities to “communicate clearly” that the current TAS, or Tax Amnesty Scheme, will not be repeated, and bring in even further tax revenue. Indonesia has already brought in almost 100 trillion rupiah in tax penalties through the most generous phase of the amnesty plan, which continues into the spring, and is designed to coax undeclared and offshore assets home to Indonesia while encouraging domestic investment and closing an expected budgetary shortfall.

Threats

- Singapore’s mall vacancies rose to the highest level in the past decade, while office vacancies also rose, to the highest level in four years.

- The weakening yuan continues to loom as a potential driver for capital outflows.

- U.S. monetary policy and interest rate speculation as well as election outcomes may play an outsized role in forthcoming months.

Emerging Europe

Strengths

- Poland was the best-performing country this week, gaining 2.4 percent. Warsaw stock exchange gains were led by Lotos and PKN Orlen. Polish refiners climbed to a new one-year high after reporting strong third-quarter results. Shares of Lotus appreciated 9.6 percent and PKN Orlen gained 7.2 percent.

- The Czech koruna was the best-performing currency this week, gaining 1 percent against the dollar. The Czech Republic economic sentiment (ESI) rose to the second-highest level since 2008.The economy remains strong, driven by rising consumer and service confidence.

- The energy sector was the best-performing sector among eastern European markets this week.

Weaknesses

- Greece was the worst-performing country this week, losing 90 basis points. European Stability Mechanism approved the remaining EUR2.8 billion loan payment to Greece. Greece’s first bailout program review was successfully concluded and the second review is starting, during which the controversial issue of labor reforms will be discussed.

- The Russian ruble was the worst-performing currency this week, losing 90 basis points against the dollar. Brent crude oil corrected this week and the ruble, which is highly correlated with the price of oil, followed its path. Brent lost 4 percent, closing at $49.8 per barrel.

- The consumer staple sector was the worst-performing sector among eastern European markets this week.

Opportunities

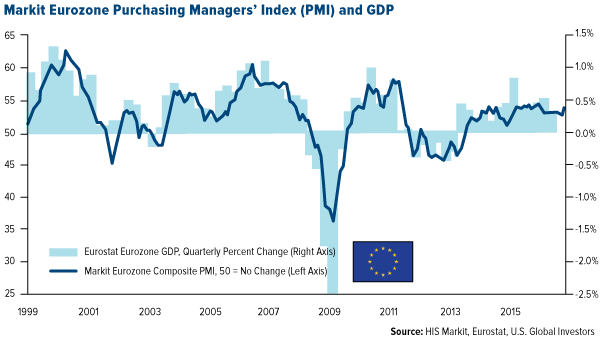

- The flash Eurozone PMI manufacturing index strengthened to 53.3 for October from 52.6 the previous month. This was the strongest reading for 30 months and above expectations of a 52.7 reading, pointing to a stronger gross domestic product. Third quarter GPD data for the eurozone will be reported next week.

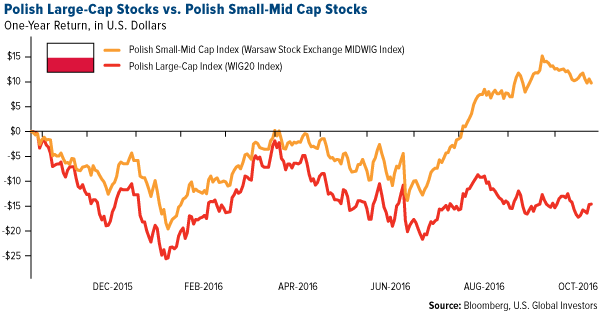

- This week Poland was celebrating the one-year election victory of the right-wing national-conservative Law & Justice (PiS) party. Since PiS came to power currency volatility jumped and the Warsaw main index (WIG20) lost 1 percent while the mid-cap index (MIDWIG) gained almost 10 percent. Mid-cap names started significantly to outperform large-cap names in the summer after the government announced its pension reform supporting smaller domestic companies. Government support for local players most likely will continue.

- European central bank (ECB) president Mario Draghi stressed the central bank’s commitment to keep rates low until the inflation target is met. Despite the ECB’s actions to stimulate economy, inflation has stayed around zero for more than two years. Most investors expect the ECB to extend its quantitative easing program by at least six months during the next policy meeting in early December. The program is currently due to expire in March.

Threats

- Italy, who is among the biggest contributors to EU budget, threatened countries who reject migrant quota with funding cuts. According to Interior Ministry data, Italy has housed around 160,000 asylum seekers from the 460,000 who reached its shore from North Africa since the start of 2014. 39,000 refugees were due to be relocated, but so far only 1,300 have been moved to Eastern members, as Hungary, Poland and Czech Republic protest against accepting new migrants. Earlier this month, 98 percent of Hungarians voted in a referendum to reject any future plans to accept EU quotas. Hungary and Poland are the biggest beneficiaries of EU funding.

- According to Raffaella Tenconi, senior economist at Wood & Company, a Donald Trump victory would cost central emerging Europe from 1.5 to 2 percent lower growth next year, saying his leadership would disrupt trade agreements and increase geopolitical tension. A Hillary Clinton victory would likely be positive for growth in the near term, but her appointment may increase the likelihood of an escalation of tensions close to the Russia - EU border.

- The number of foreign investors arriving in Tukey on September dropped 32.84 percent or 2.86 million people. Tourism adds about $30 billion to gross domestic product but has been hammered by terrorist attacks and geopolitical tension.

© US Global Investors