Markets are once again facing a proverbial wall of worry, built of political uncertainty, populism, and fiscal and monetary policy concerns. Although the market’s ascent is not likely to be straight up (it never is), we are cautiously optimistic that the wall can be surmounted. We believe the U.S. and global economies can maintain a pace of slow expansion over the near term, creating opportunities across asset classes for the active manager.

Over recent months, risk-on sentiment has prevailed (Figure 1), as globally accommodative monetary policy continued to offset near-term global growth challenges. However, we believe investors should be prepared for volatility ahead. We expect the political environment and populist currents will continue to complicate the markets, putting downward pressure on investor sentiment. In addition to U.S. elections, an upcoming constitutional referendum in Italy and national elections in France and Germany in 2017 could have a significant impact on the financial markets and global economic landscape.

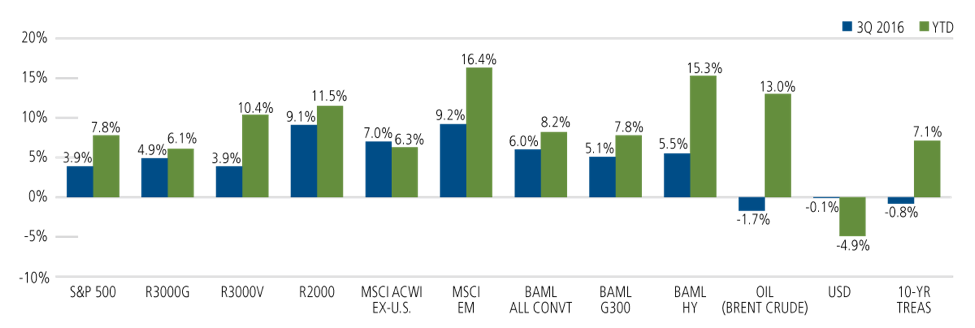

FIGURE 1. GLOBAL ASSET CLASS PERFORMANCE, 3Q16 AND YTD

Small-caps and growth led within the U.S. equity markets during the quarter, while an easing of dollar appreciation and stabilizing commodity prices contributed to a rebound in emerging markets. After lagging the S&P 500 Index during 4Q 2015 and 1Q 2016, the BofA Merrill Lynch All U.S. Convertibles Index has outperformed for the past two quarters and now leads year to date, supported by narrowing spreads and small-cap gains. High yield extended its rally, boosted by a quest for yield and a preliminary agreement by OPEC to cap oil production.

Past performance is no guarantee of future results. Source: Bloomberg.

This material is distributed for informational purposes only. The information contained herein is based on internal research derived from various sources and does not purport to be statements of all material facts relating to the information mentioned, and while not guaranteed as to the accuracy or completeness, has been obtained from sources we believe to be reliable.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

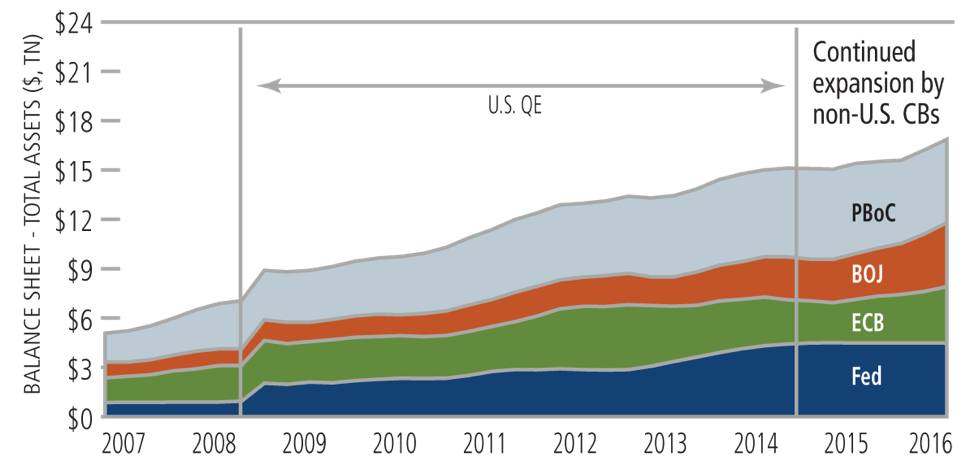

Global liquidity is at an all-time high as the major central banks work to support a weak growth and low inflationary environment (Figure 2). Although rates are likely to stay very accommodative, policy divergence may become more of an issue as the Fed signals a bias for increasing rates modestly. Meanwhile, fiscal policy (or a lack thereof) remains a formidable hurdle for many countries. While monetary policy acts as a short-term fix by supporting asset prices and financial markets, real economic growth requires fiscal policies that encourage private sector growth and entrepreneurship, such as a reasonable regulations and tax reform.

FIGURE 2. MONETARY SUPPORT CONTINUES TO EXPAND

TOTAL ASSETS ON CENTRAL BANK BALANCE SHEETS

Source: Goldman Sachs, Investment Research, Robert D. Boroujerdi, “Framework in Pictures,” September 2016 using Bloomberg and Goldman Sachs Global Investment Research. Balance Sheet Total Assets are as of 2Q16.

While we see many opportunities, security selection remains paramount given the highly consequential events on the horizon. Valuations are elevated in many segments of the market, with the ongoing yield play in dividend-oriented stocks likely to influence the market for the foreseeable future. We believe the risks in traditional fixed income remain formidable, as many investors in this crowded trade are underestimating the downside. In our view, growth-oriented companies remain more attractive than value companies in this environment. However, there are select opportunities among cyclicals, calling for a degree of balance in our positioning. With many historically low volatility stocks trading at high prices, convertible securities and select alternative strategies (such as market neutral income and hedged equity) may provide a more attractive means of addressing downside equity volatility. Finally, we are vigilant to the potential impact of currencies, both on individual companies as well as market performance.

The stock market is likely to remain highly sensitive to economic releases and announcements, as participants seek to make sense both of the data itself as well as how it is likely to influence Fed policy. As the next earnings announcement season commences, guidance is likely to be cautious, especially for currency-sensitive companies. We are devoting particular focus to trends in capex spending, where the impact of euro zone uncertainties is yet to be determined.

U.S. EQUITIES

U.S. economic data has become incrementally choppier since early spring, but we believe an imminent recession remains unlikely. Job growth and housing and manufacturing data may be less robust yet are still positive. While the consumer is in good shape from employment, wage and balance sheet standpoints, we are monitoring the impact of relatively higher energy prices on lower-end consumers and overall sentiment shifts in an uncharted political environment. Corporate earnings are likely to start looking better on a year-over-year basis, but in many cases these improvements are a function of easing U.S. dollar appreciation (a benefit to U.S. exports) and stabilizing commodity prices (a boost to energy and related companies) rather than demand-driven factors. Growth-oriented stocks tend to do well during this stage of the economic cycle, but the quest for yield is not likely to abate in a low-rate environment.

Within the U.S. equity market, we are favoring high-quality, consistent growth companies, while selectively increasing cyclical growth exposure. We have maintained our emphasis on technology, seeking to strike a balance between growth and valuations, favoring companies which are disruptors and market share gainers.

In our growth equity portfolios, our consumer exposure favors dominant companies with sustainable franchise values over “brick and mortar” companies. We have identified select opportunities among biotechnology names, where we believe valuations have become quite attractive. Cyclical exposures are consistent with a positive view on housing, a rebalancing in the energy markets, and defense and post-election infrastructure spending.

In our lower-volatility equity strategies, we have sought stable-to-improving fundamentals and reasonable valuations, and have found those across industries. In addition to a range of technology opportunities, we have identified opportunities within consumer areas. We have also invested in financial companies where we see catalysts other than potential rate increases.

GLOBAL AND INTERNATIONAL

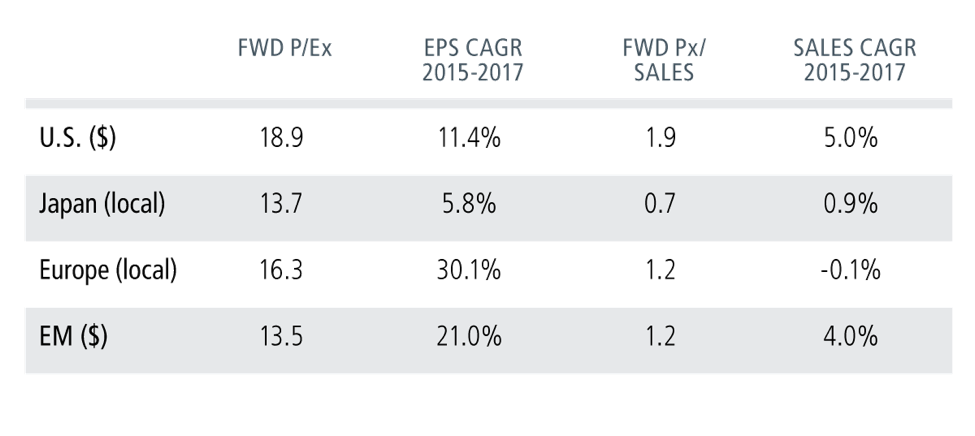

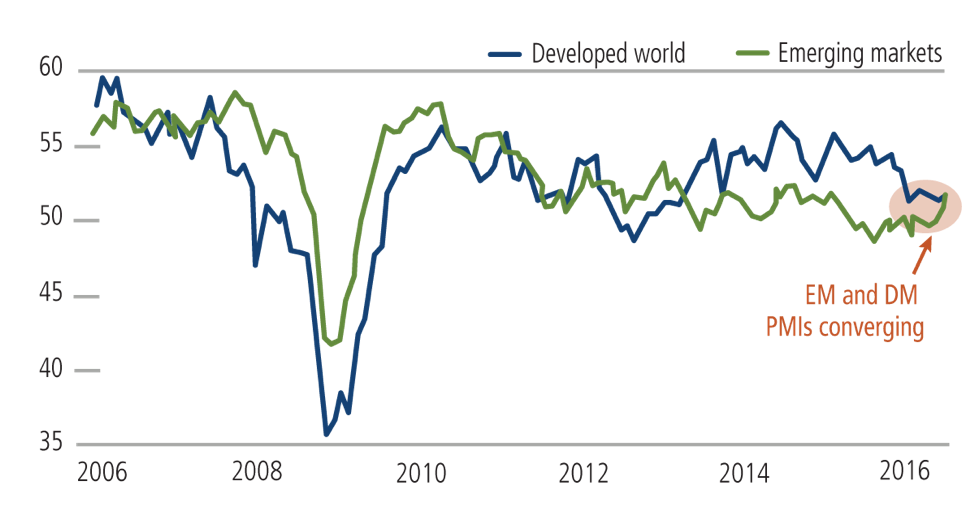

Our view on emerging markets has grown more positive throughout the year. Valuations and growth characteristics are quite favorable on a relative basis versus developed markets (Figure 3). As we discussed in our recent commentary, emerging markets have also benefited from an easing in the appreciation of the dollar and commodity price stabilization. While we do not expect economic growth in emerging markets to accelerate in an environment of muted global expansion, we are seeing signs of a near-term bottoming out in EM economic data. For example, purchasing manager indexes for emerging and developed markets have converged, albeit at a relatively weak absolute level (Figure 4). We have also seen improvements in current account balances, for both commodity importers and exporters.

FIGURE 3. GLOBAL VALUATIONS

AS OF 10/3/16

Source: Bloomberg.

FIGURE 4. DM AND EM: CONVERGENCE OF FORTUNES?

PURCHASING MANAGER INDEXES

Source: IHS Markit, JP Morgan, Nikkei, Caixin.

Overall, our emphasis in emerging markets remains on countries that are embracing economic reforms. We are particularly constructive on India, and are identifying an increased number of opportunities in Indonesia. In the past, we have discussed our positive view of Mexico. We are presently holding our exposure steady rather than increasing it, due to the political uncertainties associated with the U.S. presidential election. In China, economic data looks incrementally better, but we are watching for signs of cooling in housing, which could ripple across other sectors.

Our emphasis remains on companies associated with the “New China” (technology and consumer) over “Old China” (industrials and commodities). We are monitoring risks and opportunities tied to the weak renminbi and its recent official inclusion in the IMF’s Special Drawing Reserve. While we remain underweight in Russia, Brazil and South Africa, we have identified opportunities to boost exposure in more stable companies with higher-quality balance sheets. We have also more broadly increased exposures to emerging market currencies.

In contrast, our stance toward Europe and Japan has become less sanguine. Brexit’s winners and losers will emerge as the exit takes shape next year, with the aforementioned elections potentially altering the landscape further. Meanwhile, Japan continues to struggle with weak inflation. As we see fewer macro tailwinds in Europe and Japan, our positioning in both regions reflects bottom-up ideas that can benefit from the positive liquidity environment. In Europe, we have identified beneficiaries of low debt costs and inflated asset values, such as private equity firms. In Japan, we favor exporters and automation and technology companies that support increased industrial productivity.

CONVERTIBLE SECURITIES

Global convertible security issuance ramped up during the third quarter, with $22.6 billion coming to market. Year-to-date issuance stands at $60.8 billion, now generally on pace with 2015. We expect healthy issuance to continue even in an environment of subdued growth.

With many so-called “safety stocks” and traditional fixed income securities trading at stretched valuations, investors are facing more downside volatility. Because convertibles provide the opportunity for upside equity participation with less exposure to downside volatility, we believe they can offer a compelling alternative to holding more richly valued defensive equities. Active management remains key, given that underlying valuations are bifurcated, with traditional value areas trading at elevated levels versus traditional growth areas.

In our positioning, we continue to emphasize the balanced portion of the convertible market and are more selective regarding the most equity-sensitive and the most speculative issues. From a sector standpoint, we continue to favor technology—valuations are fair, fundamentals are strong, balance sheets are solid, M&A activity is robust, and secular trends provide tailwinds. We are underweight in cyclical areas (industrials, energy, materials) but are monitoring potential OPEC actions that could have positive impacts on the energy sector. The global search for income has resulted in full valuations for many yield-oriented “bond surrogates,” but we have identified opportunities in REITs, long-duration bank-issued convertible preferreds, and utilities.

HIGH YIELD

As we discussed in our monthly high yield commentary, higher energy prices, a patient Federal Reserve and a declining default rate have spurred investor appetite for high yield debt. However, despite strong technical demand, we see increased risks.

The recent surge in issuance suggests the capital markets are open to all but the riskiest issuers. We are concerned the market is pricing these riskier deals at aggressive levels relative to years past. Also, the average coupon for the overall high yield market has dropped over the years, giving investors less cushion when interest rates rise and/or spreads widen.

In this environment, we remain overweight industries that we believe can still generate solid fundamentals absent a robust U.S. economy, and underweight those industries that are more secularly challenged. We are highly selective toward the most speculative credits, choosing instead to focus on “rising stars” (high yield issuers that we believe the rating agencies will upgrade to investment grade in the near term). Historically, pinpointing these opportunities before the agencies has proven to be a significant source of alpha.

CONCLUSION

Brexit and the market response to it remind investors to be prepared for both unexpected events as well as unexpected market reactions. The referendum in favor of leaving the EU took many by surprise, but so too did the short-lived market selloff and rally that followed. Now, eyes are on the U.S. presidential election. We cannot predict with certainty the outcome, the market’s immediate response, or the changes to fiscal policy that will unfold over the months to come.

Moreover, the U.S. elections are only one of many events on the horizon—we also have central bank policy decisions, Brexit and a variety of referendums and elections in Europe. However, history has shown that emotional responses increase the likelihood of being whipsawed. Accordingly, we encourage investors to maintain a disciplined, long-term focus through these next months.

CALAMOS INVESTMENT COMMITTEE

John P. Calamos, Sr.

Founder, Chairman and Global Chief Investment Officer

John Hillenbrand, CPA

Co-CIO, Head of Multi-Asset Strategies and Co-Head of Convertible Strategies, Senior Co-Portfolio Manager

David P. Kalis, CFA

Co-CIO, Head of U.S. Growth Equity Strategies, Senior Co-Portfolio Manager

Nick Niziolek, CFA

Co-CIO, Head of International and Global Strategies, Senior Co-Portfolio Manager

Eli Pars, CFA

Co-CIO, Head of Alternative Strategies and Co-Head of Convertible Strategies, Senior Co-Portfolio Manager

Jeremy Hughes, CFA

Senior Vice President, Co-Portfolio Manager

Indexes are unmanaged, not available for direct investment and do not include fees and expenses. The U.S. Dollar Index measures the value of the U.S. dollar relative to a basket of foreign currencies, including Euro Area, Canada, Japan, United Kingdom, Switzerland, Australia, and Sweden. The Russell 3000 Growth Index and Russell 3000 Value Index measure U.S. growth and value equities, respectively. The Russell 2000 Index measures U.S. small cap stock performance. The S&P 500 Index is considered generally representative of the U.S. equity market. The MSCI All Country ex U.S. Index represents the performance of global equities, excluding the U.S. The MSCI Emerging Markets Index is a measure of the performance of emerging market equities. The BofA Merrill Lynch U.S. High Yield Index is an unmanaged index of U.S. high yield debt securities. The BofA Merrill Lynch All U.S. Convertible Index (VXA0) is a measure of the U.S. convertible market. The BofA Merrill Lynch G300 Index measures the performance of 300 global convertibles. Oil is represented by current pipeline export quality Brent blend. Purchasing Managers Indexes measure manufacturing sector strength. Quantitative easing refers to central bank bond buying activities. Earnings per share (EPS) is a company’s profit divided by its number of common outstanding shares. Price-to-earnings ratio (P/E) is a valuation ratio of a company’s current share price compared to its per-share earnings; forward P/Es are based on forecasted earnings. CAGR, or compounded annual growth rate measures year-over-year growth. Price to sales ratio measures a company’s stock price versus its revenues. REITs, or real estate investment trusts, are securities that invest in real estate or mortgages. Alpha is the measurement of performance on a risk adjusted basis. A positive alpha shows that performance of a portfolio was higher than expected given the risk.

Alternative strategies entail additional risks and may not be suitable for all investors.

Opinions, estimates, forecasts, and statements of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. The views and strategies described may not be suitable for all investors. References to specific securities, asset classes and financial markets are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations.

NOT FDIC INSURED | MAY LOSE VALUE | NO BANK GUARANTEE

© 2016 Calamos Investments LLC. All Rights Reserved.

Calamos® and Calamos Investments® are registered trademarks of Calamos Investments LLC.

OUTLKCOM 18158 0716O C

© Calamos Investments

Read more commentaries by Calamos Investments