At the three-quarter pole, the global economy is muddling through a disappointing 2016. Growth in developed and emerging markets continues, but at a pace that has fallen short of expectations. Populism is spreading across the world electorate, central banks may be giving way to fiscal stimulus, and Brexit is back on the front burner.

Despite these risk factors, the current expansion should continue at a modest pace into next year. Inflation is generally expected to remain range-bound, limiting the reaction of central banks. Several jurisdictions may stress fiscal policy over monetary remedies as a path to better performance. Politics and China’s performance remain at the top of the watch list.

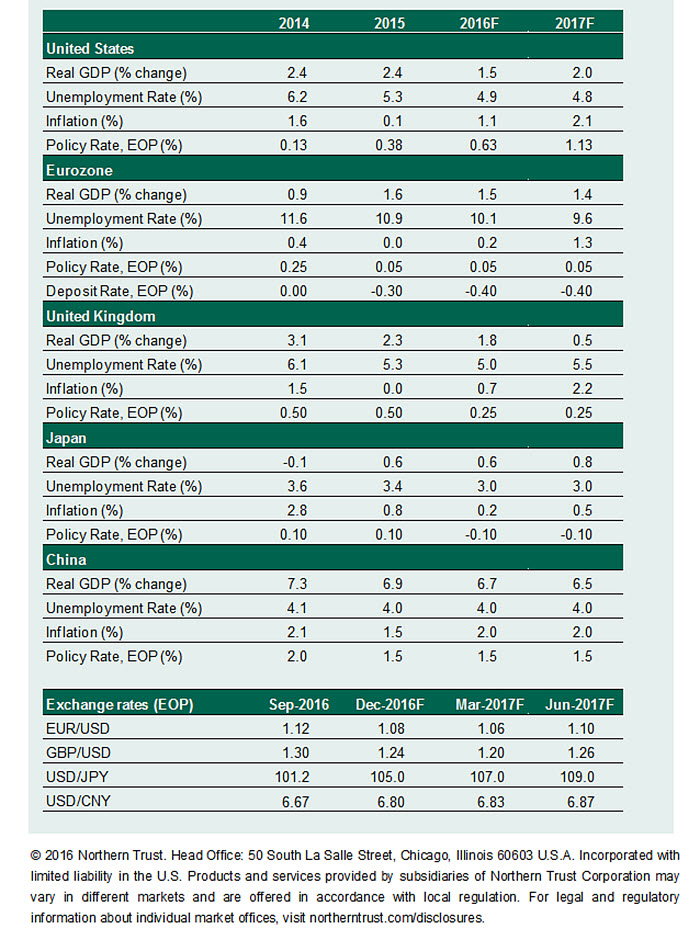

UNITED STATES

Economic growth in the second half of 2016 should exceed the pace of activity seen in the first two quarters. The fundamentals are in place to support continued forward business momentum in 2017. Consumer spending is projected to advance at levels comparable to recent trends. Business spending appears to be stabilizing, following a weak performance in the past three quarters. The housing sector’s soft readings are anticipated to turn around, given favorable employment conditions and low interest rates. With the current solid labor market numbers, the Fed’s full employment mandate is close to be being satisfied.

As the impact of a strong dollar and low energy prices fade, inflation is likely to move closer to the Federal Reserve’s 2.0% target. Oil prices are not, however, expected to rise enough to significantly rekindle drilling activity in the United States.

Ample evidence exists to support a Fed policy rate increase in December, barring adverse global economic developments. But future policy moves will be data dependent and gradual. Long-term interest rates have retraced a large part of the declines seen after the Brexit referendum. The upcoming U.S. election is not expected to result in major changes to economic policy.

EUROZONE Economic activity remains resilient in the eurozone, as indicated by the latest industrial production, retail sales and lending survey figures. Brexit has had little negative impact on the continent, and we believe Europe likely will start benefitting from the relocation of businesses, especially financial services, as early as next year.

Nevertheless, we expect the ongoing woes of peripheral debt and the troubled financial sector, along with elevated political uncertainty from a number of upcoming elections, will weigh down growth. Therefore, we expect gross domestic product (GDP) growth to decline marginally to 1.4% in 2017 from 1.5% in 2016. Several member states may require special financial attention in the months ahead, with Greece and Portugal heading the list.

The European Central Bank (ECB) kept policy unchanged in its latest meeting and dismissed any speculation about ”tapering” its asset purchases. Given the tepid inflation outlook, we expect the ECB to extend its asset purchase program in December 2016 when more macroeconomic data would be at disposal. Scarcity of bonds eligible for purchase is likely to be solved via relaxation of technical criteria, rather than tapering the size of purchases.

UNITED KINGDOMWhile recent data releases do not show much of an impact from the United Kingdom’s decision to leave the European Union, policy uncertainty, higher import prices and a rethink of business investment will hinder growth. Therefore, we expect U.K. GDP growth for this year to come out at 1.8%, and to decelerate to just 0.5% in 2017.

Strong retail spending has been a source of economic stability, but we expect the fall in the value of the pound to dent consumption in the months ahead. Continued uncertainty over trading and financial relationships with the European Union and the rest of the world would not just keep the pound volatile but also likely depress or delay business investment. It really is difficult to overstate the number of variables that are unknown as the onset of negotiations approaches.

The Bank of England has signaled that it would tolerate the sharply weaker pound and the resultant inflation over-shoot, and continue to keep policy conditions accommodative to support economic activity. Fiscal policy also likely will be more simulative as the government has moved away from the budget-surplus-rule, although a continued rise in gilt yields could pose a constraint on the magnitude. We’re expecting the sterling to find a floor, but to remain near historical lows.

JAPANA moderate spurt in household spending and private investment, especially residential investment, has helped mitigate the impact of declining exports on the Japanese economy. Furthermore, fiscal policy remains supportive of growth and underpins our projection for economic activity in 2017. On the back of the recently announced fiscal stimulus, we expect economic growth to improve very modestly, to 0.8% in 2017 from 0.6% in 2016.

Although the Bank of Japan has spared no effort in keeping monetary conditions ultra-loose, we remain skeptical as to whether that will translate into higher inflation, a weaker yen and more robust economic activity. Thus, even though we expect some price pressure from a narrower output gap and a tighter labor market, Japanese inflation is unlikely to be anyway near the 2% target.

We continue to hold the view that more support is needed from the other two arrows of ”Abenomics” – fiscal policy and structural reforms – for any improvement in Japanese growth prospects. Unfortunately, changes to workplace practices that could deepen the labor pool and raise wages have been progressing very slowly.

CHINA Strong public investment in infrastructure and a real estate boom continue to support economic activity, even as industrial production slows. The latter’s weakness is apparent in the shrinking share of manufacturing, which is now below 40% of Chinese GDP, while services now make up more than half of the GDP. Looking ahead, even as public sector investment is expected to remain strong, we expected authorities to rein in housing prices and that the slowdown in private sector investment will continue. On balance, we expect GDP growth to slow marginally, to 6.5% in 2017 from 6.7% in 2016.

Financial sector stability and real estate prices remain the key sources of concern. In particular, rising leverage, debt and the overall health of the banking sector are worrying. On the housing market, local authorities have recently imposed curbs, such as tougher down-payment requirements and restrictions on foreign buyers, to cool prices.

While the People’s Bank has noted the frothiness of house prices, we expect the response to come via prudential measures to reign in excess credit, rather than policy-rate tightening. China’s monetary policy path likely will remain neutral as it tries to balance rising financial risks with decelerating private activity. Instead, stimulus will largely come from fiscal policy, and from a slightly weaker currency, at the margin.

The Chinese are preparing for a major party congress next spring, which should provide important indications of their economic intent.

The views and opinions expressed are those of the individuals noted herein and are subject to change without notice. This material is provided for informational purposes only and does not constitute an offer or solicitation to purchase or sell any security or commodity or invest in any specific strategy. It is not intended as investment advice and does not take into account each investor’s unique circumstances. Information has been obtained from sources believed to be reliable, but its accuracy, completeness and interpretation cannot be guaranteed. Past performance is no guarantee of future results.

Global Economic Forecast – October 2016

© Northern Trust

© Northern Trust

Read more commentaries by Northern Trust