KEY TAKEAWAYS

- In our election playbook, we discuss some investments that could possibly receive an election boost.

- Some areas that may fare better under Clinton include: alternative energy, emerging markets, and healthcare services.

- Some areas that could potentially get a boost from a Trump presidency include: biotech/pharmaceuticals, energy, and financials.

- An increase in stock market volatility around the election is still possible, but we are encouraged by the market’s historical tendency for late election year rallies.

With the election fast approaching, we present our election playbook. With Election Day just 15 days away, and the three presidential debates behind us, investors want to know what the upcoming change in power in Washington might mean for their portfolios. Here we offer our election playbook, including some potential investments that could possibly receive an election boost.

This commentary is not intended to promote short-term trading. Election-related policy impacts are just one part of a sound investment decision.

THE PLAYBOOK

We offer the following advice for stock market investors who may be either worried about the election or simply looking for opportunities to profit from it:

· Campaign rhetoric is mainly just that—rhetoric. Priorities for the candidates do not necessarily match the amount of time they spend discussing various issues on the campaign trail. For example, should Donald Trump win the election, we would not expect him to immediately slap big tariffs on imported goods and potentially start a trade war. Similarly, we would not expect Hillary Clinton to actually break up the big banks even if she could do so unilaterally

· Checks and balances. Many campaign promises will not get through Congress to be implemented even if they are a top priority for a newly elected president. For example, significant subsidies for college tuition that Hillary Clinton supports may sound great in theory but are unlikely to get through Congress (Republicans would likely filibuster this proposal if they did not have a majority in the House). Also keep in mind that newly elected presidents tend not to have as much political capital as they think they will; one of the reasons they are typically unable to get all of their top priorities accomplished.

· Corporate America is adaptable. Corporate America has operated under many different political regimes over time. Over the past 80 years, many disruptive policies have come and gone — as have recessions, periods of high inflation, interest rate spikes, Federal Reserve rate-hike cycles, wars, terrorist attacks, etc. Through it all, S&P 500 companies have grown profits by an average of 8 percent annually.

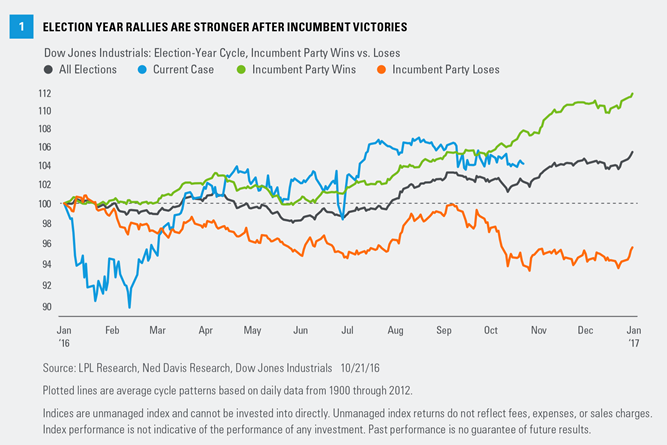

· Stocks like clarity. Stocks tend to do well late in election years regardless of the winner as uncertainty (and in some cases divisiveness) subside. On average, the S&P 500 gains nearly 4% during the fourth quarter of election years.* As shown in Figure 1, stocks often start to rally around Election Day, particularly when the candidate from the incumbent party wins, as the polls currently suggest is the likely outcome.

We are not particularly worried about the stock market under either candidate based on our assessment of the macroeconomic environment; stocks historically have finished election years strong regardless of the political dynamics.

*Average S&P 500 change during 4th quarters of election years since 1950 is 3.6% (excluding 2008), with gains 87% of the time.

LIKELY CLINTON BENEFICIARIES

Here are some investments that may potentially get a boost from a Trump victory:

· Alternative energy. Clinton has made investing in clean energy and reduced reliance on fossil fuels a key part of her environmental platform. As a result, companies focused on alternative energy, such as solar or wind power, or clean energy infrastructure may perform better under a Clinton administration.

· Emerging markets. Although both candidates have talked tough on trade, we believe a Clinton victory may be better for emerging market equities and currencies due to the potentially lower probability of soured trade relations with either China or Mexico. The sensitivity of the Mexican peso to election polls, which we discussed in a recent blog, is perhaps the strongest evidence of EM’s preference for Clinton. Remember, the President can act unilaterally on trade in the interest of national security, though it is unclear whether Trump would exercise this authority.

· Healthcare providers. Healthcare companies leveraged to the Affordable Care Act (ACA), such as hospitals, treatment centers, and insurers, are poised to do well in a Clinton victory scenario given her desire to maintain and strengthen the ACA. Lab companies and diagnostic testing equipment makers may also benefit.

· Multinationals. Stocks with the most international exposure have tended to perform better over the past several months when Clinton has fared well in the polls. We believe this is partly a reflection of the greater risk that Trump may impose added trade restrictions.

Investing in foreign and emerging markets securities involves special additional risks. These risks include, but are not limited to, currency risk, geopolitical risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

LIKELY TRUMP BENEFICIARIES

Here are some investments that may potentially get a boost from a Trump victory:

· Biotech and Pharmaceuticals. Although Trump has stated his desire to repeal the ACA and has favored drug re-importation from other countries, controlling drug prices is unlikely to be as high of a priority for him as it would be for Clinton. As a result, biotech and pharmaceutical companies may get a bump in the event of a Trump victory. Even under Clinton, we believe the market may have overreacted to perceived policy risk and we continue to favor the healthcare sector, which has historically performed well after elections.

· Energy. Trump is likely to be better for fossil fuels than Clinton. He has promised less regulation on drilling and expansion of drilling areas. The segment of the industrials sector that services the energy sector may also benefit.

· Financials. Trump is likely to be easier on financial regulation than Clinton, suggesting that the financial sector — and banks in particular — may get a boost under a Trump victory scenario. Trump has indicated he would like to roll back financial regulations, including the Dodd-Frank financial crisis legislation that Clinton has pledged to strengthen. Both candidates have suggested bringing back Glass-Steagall, which would separate traditional banking from investment banking, a move we see as very unlikely regardless of the election outcome.

POTENTIAL WIN-WIN SITUATIONS

· Defense. We are likely to see a boost in defense spending under either candidate. Clinton is likely to be more hawkish on defense than President Obama has been, while Trump has talked repeatedly about building up the military.

· Infrastructure. Both candidates support increased infrastructure spending. Under a Trump administration, while restrictive trade policy may constrain overseas revenue for multinationals, those same companies — many industrial companies — would benefit from increased infrastructure spending. Engineering and construction companies appear particularly well positioned.

· Overseas cash. We believe tax reform stands a fairly good chance of getting done under most election scenarios, including repatriation, which would allow companies to bring cash back to the U.S. from overseas at a discounted tax rate. This move would benefit big technology companies that are holding the most cash. Some of that cash may end up being used to increase dividends which could help the share prices of those companies, although that would not be the ideal outcome for most policymakers. The risk, as with many legislative possibilities, is that a divided Congress and fractured leadership within the parties prevent compromise and potentially lead to more gridlock.

CONCLUSION

An increase in stock market volatility is still possible ahead of or immediately following the election, but we are encouraged by the market’s historical tendency to rally during the fourth quarter of election years. With Clinton the favorite, we might focus on the trades that may get a lift should she win the election. But an “October surprise” is still possible, so ignore the Trump trades in our playbook at your own risk. With Election Day fast approaching, this playbook can be your guide.

Note that LPL Research is non-partisan and individuals including the named authors and others with varying political views contributed to this commentary.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

Because of its narrow focus, sector investing will be subject to greater volatility than investing more broadly across many sectors and companies.

All investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones Industrial Average Index is comprised of U.S.-listed stocks of companies that produce other (non-transportation and non-utility) goods and services. The Dow Jones industrial averages are maintained by editors of The Wall Street Journal. While the stock selection process is somewhat subjective, a stock typically is added only if the company has an excellent reputation, demonstrates sustained growth, is of interest to a large number of investors, and accurately represents the market sectors covered by the average. The Dow Jones averages are unique in that they are price weighted; therefore, their component weightings are affected only by changes in the stocks’ prices.

© LPL Financial

Read more commentaries by LPL Financial