You might not think a movie about robbing banks illuminates some of the fundamentals of value investing, but then again, you might not have seen Hell or High Water. The movie tells the story of two brothers who traveled around rural Texas robbing small town banks early in the morning to keep their family property out of foreclosure. It's not about the intricacies of their heist, it's the simplicity of the smaller banks they robbed. It's only when they got greedy, going after a bigger bank, that they got caught.

We think of Charlie Munger, the Vice-Chairman of Berkshire Hathaway, who taught us that "competition is the enemy of competence." You see, while the brothers successfully found no competition in the smaller rural banks, they ran into trouble when attempting to rob a busy bank later in the day with customers who all had their own guns. They had lost their gun-powered moat.

There is a very important investing lesson in these bank robbing efforts. When the brothers were the only holders of a weapon in the early bank robberies, their enterprise was lucrative. You might say they were in “High Water.” When they attempted to rob a larger and busier bank later in the day, their fire power was overwhelmed by weapons in the hands of law abiding citizens. Charlie Munger would say their “Hell” came from too much competition as their competence disappeared.

Do profitable businesses exist today which face little or no competition?

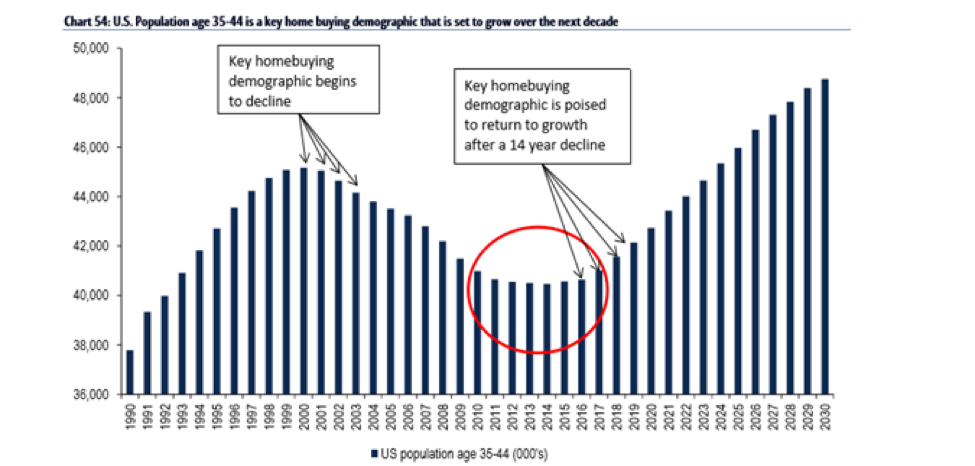

Aflac (AFL) is the largest seller of supplemental health insurance in the U.S. As Yogi Berra said at the barbershop in an Aflac commercial, “If you get hurt and miss work, you won’t be sick because you missed work.” Typically, folks aren’t attracted to supplemental health insurance until they have their first child. We believe the demographics shown below scream for a great market in health insurance sales for Aflac over the next fifteen years1:

We have owned the stock for many years and we have yet to meet another investor who could name their number two competitor. Aflac has raised its dividend for 33 consecutive years. This means that they are in “High Water” and are waving the biggest gun in their industry. Aflac also owns one of the most successful life insurance businesses in Japan, selling cancer insurance to people who eat a low-fat diet and die of cancer much less often per capita than Americans do. They manage a greater than $100 billion bond portfolio, laden with U.S. debt, and would see their income production enhanced by higher interest rates in the U.S.

Express Scripts (ESRX) is one of the largest pharmacy benefits managers (PBM) in North America. It provides retail drug card programs, specialty disease management and prescription drugs through its retail network. It is the interface between the healthcare providers and the makers of medicines, treatments, vaccines and cures. They filed 1.3 billion prescription claims last year. They have 3,000 healthcare organizations as clients and 85 million end customers. To say they have a big gun in their industry would be a huge understatement.

Investors have been concerned about the loss of a large client, Anthem, which is 15% of their revenue. Anthem is unhappy with a contract they made with Express Scripts which runs out in 2019. Anthem is having a difficult time merging with Cigna, the latter of which owns a PBM. Warren Buffett likes to say, “You pay a dear price for a cheery consensus.” Despite their big gun, ESRX stock is priced at a small gun and non-dear price.

While some people consider these circumstances “Hell,” Express Scripts is creating massive free-cash flow. The consensus estimates call for free-cash flow (FCF) that will exceed $7.00 per share in 2016, meaning the stock is trading for around ten times FCF. For most of the last twenty years, this has been a glamour growth stock. It is very difficult to get your gun into this industry and even if you did, your gun would be tiny compared to ESRX.

We seek companies which are waving their gun in an industry where guns are rare and have produced high sustainable profitability. You might say that they sit in “High Water.” Companies which have created great wealth in the past can have great success later in their career despite stumbling. This can be true if they have the balance sheet strength and free cash flow to make it through the difficulties. Who knows, they just might win an academy award, like Jeff Bridges, if they can avoid too much competition.

Warm Regards,

William Smead

1Past performance is no guarantee of future results. Source: BofA Merrill Lynch “Tracking the U.S. Consumer, September 16, 2016.

The information contained in this missive represents Smead Capital Management's opinions, and should not be construed as personalized or individualized investment advice and are subject to change. Past performance is no guarantee of future results. Bill Smead, CIO and CEO, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. Portfolio composition is subject to change at any time and references to specific securities, industries and sectors in this letter are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. In preparing this document, SCM has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources. A list of all recommendations made by Smead Capital Management within the past twelve-month period is available upon request.

© 2016 Smead Capital Management, Inc. All rights reserved.

This Missive and others are available at www.smeadcap.com

Follow us on Twitter @SmeadCap