India Is a Standout Among Emerging Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsINDIA HIGHLIGHTS

- Population of over 1.3 billion people is among the youngest in the world.

- Domestic consumer demand is being driven by India’s growing middle class, increasing urbanization and rapid household formation.

- Under-penetration of consumer products and services, health care and banking provides growth potential that’s attractive to investors like Wasatch.

- India is a democratic republic that embraces capitalism and the rule of law, and the country has a strong regulatory framework led by the Reserve Bank of India.

- Prime Minister Narendra Modi’s new initiatives, bureaucratic reforms, tax simplification, improved labor laws and streamlining of the bankruptcy process are designed to further the country’s growth and development.

- Low sector correlations provide diversification and potentially lower the risk of investing in India compared to Brazil, China and emerging markets overall.

- Compared to other emerging-market companies, Indian companies often exhibit more of the quality metrics we favor.

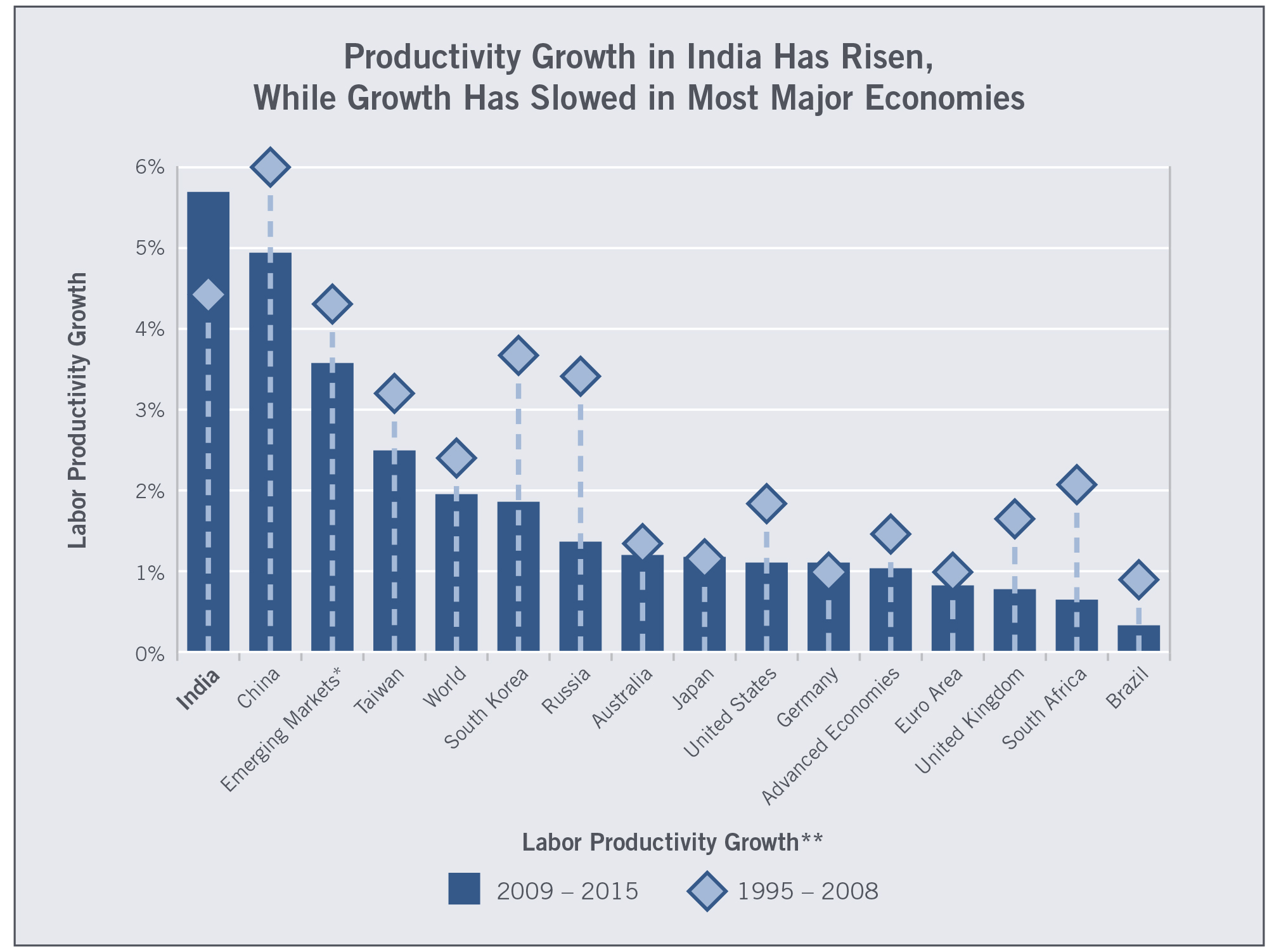

- Productivity growth is rising in India, while it has been slowing in most major economies.

- Wasatch has well over a decade of experience investing in India.

INDIA: AN EXCELLENT SOURCE OF HIGH-QUALITY COMPANIES UNDERPINNED BY A SUPPORTIVE ENVIRONMENT

Wasatch Advisors has been investing in India for well over a decade. We hope this paper will illuminate why we remain excited about the investment opportunities there. For starters, the universe of high-quality Indian companies is broader and deeper than what we’ve found in many other emerging markets. In China, for example, very few companies measure up to our strict criteria, and government meddling often clouds the whole investment picture. By contrast, our on-the-ground research in India continues to provide us with a wealth of strong, well-managed companies with significant growth potential.

A democratic government underpins India’s investment environment. The strong institutions it has built have helped the country avoid much of the political turmoil, massive borrowing, debt defaults and runaway inflation that have plagued some other emerging-market countries during the last 30 years. We also like India’s growing middle class, young demographics (as indicated in the chart below) and high personal savings rates.

Sources: Global Demographics, Macquarie Research, September 2015.

Moreover, we’ve found that market forces (rather than political patronage) are increasingly having positive effects on India’s national and state policies and on infrastructure development. In India—relative to most other emerging countries—our research has shown that management expertise, financial controls, corporate governance and transparency are remarkably good.

The reasons for these positive conditions include a strong regulatory framework led by the Reserve Bank of India (RBI) and a long history of multinational corporations. In fact, many multinationals have had operations in India for more than 75 years, which has created a robust business culture despite periodic political and economic challenges.

From a company-specific perspective, we’re able to invest across many sectors and industries in India. For example, we hold high-tech and business-processing companies that are beneficiaries of outsourcing from developed nations. In addition, we hold some health-care companies that export generic pharmaceuticals around the world. Interestingly, about 40% of the generic drugs sold in the U.S. are produced by Indian companies.

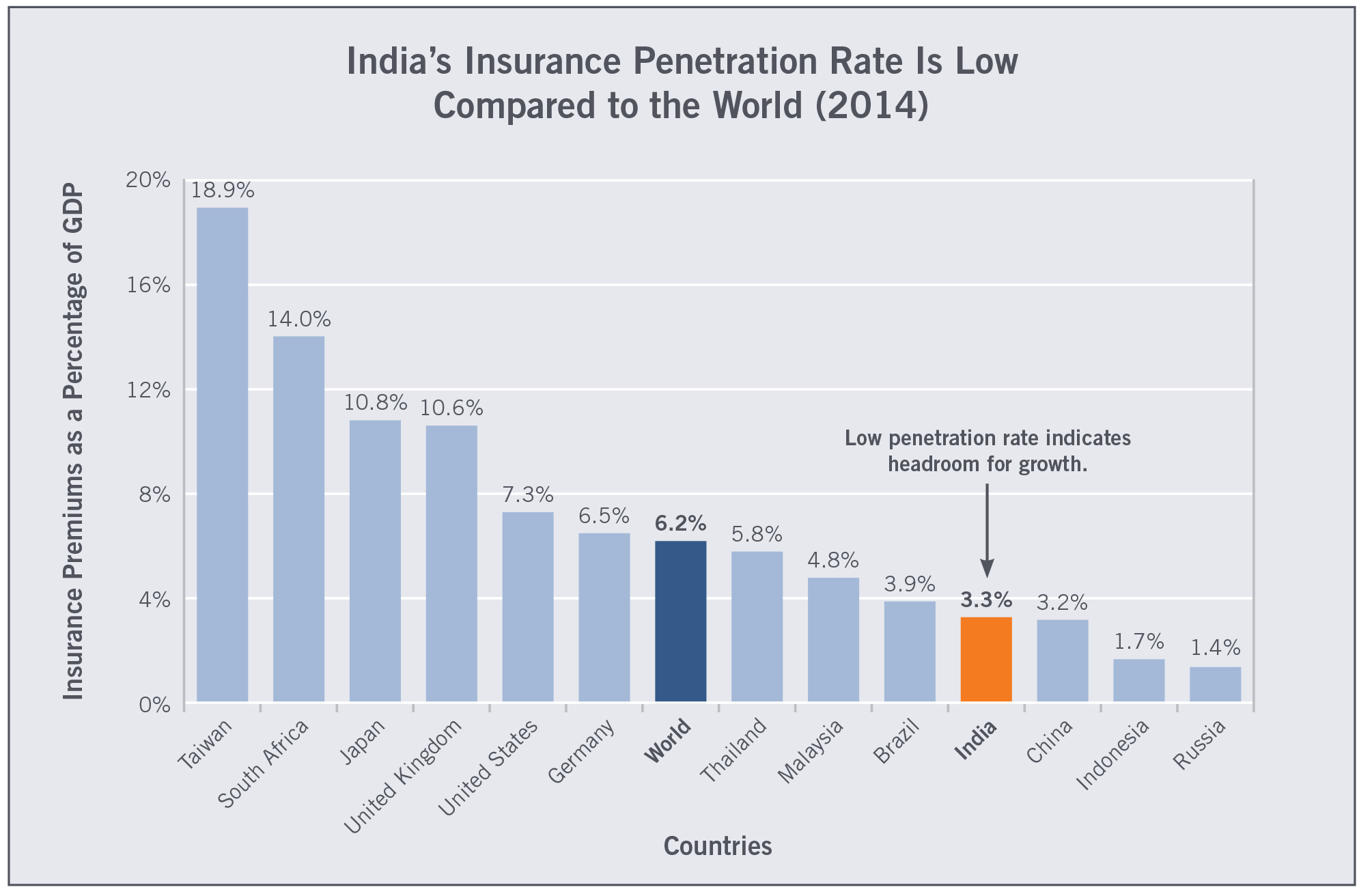

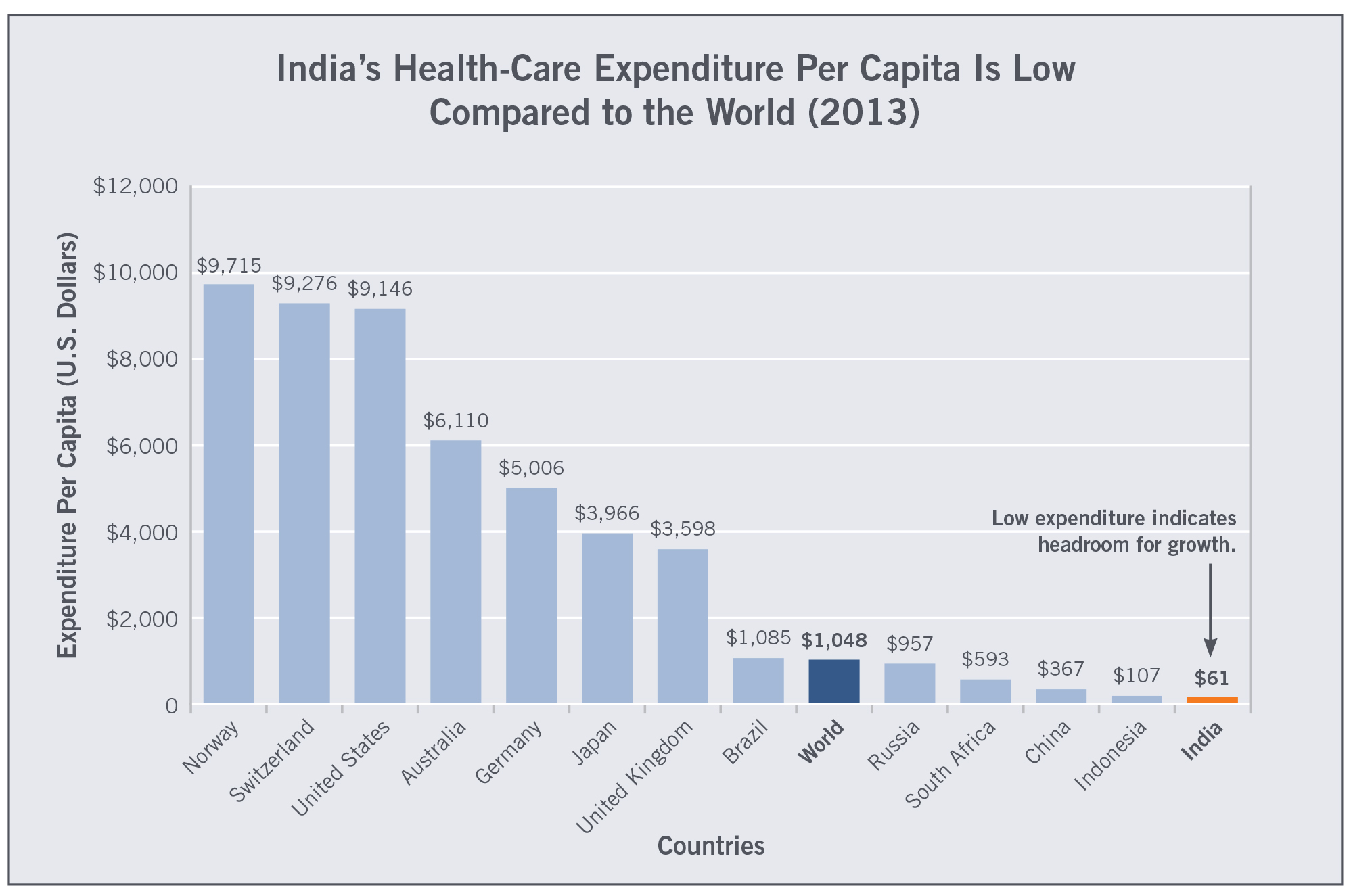

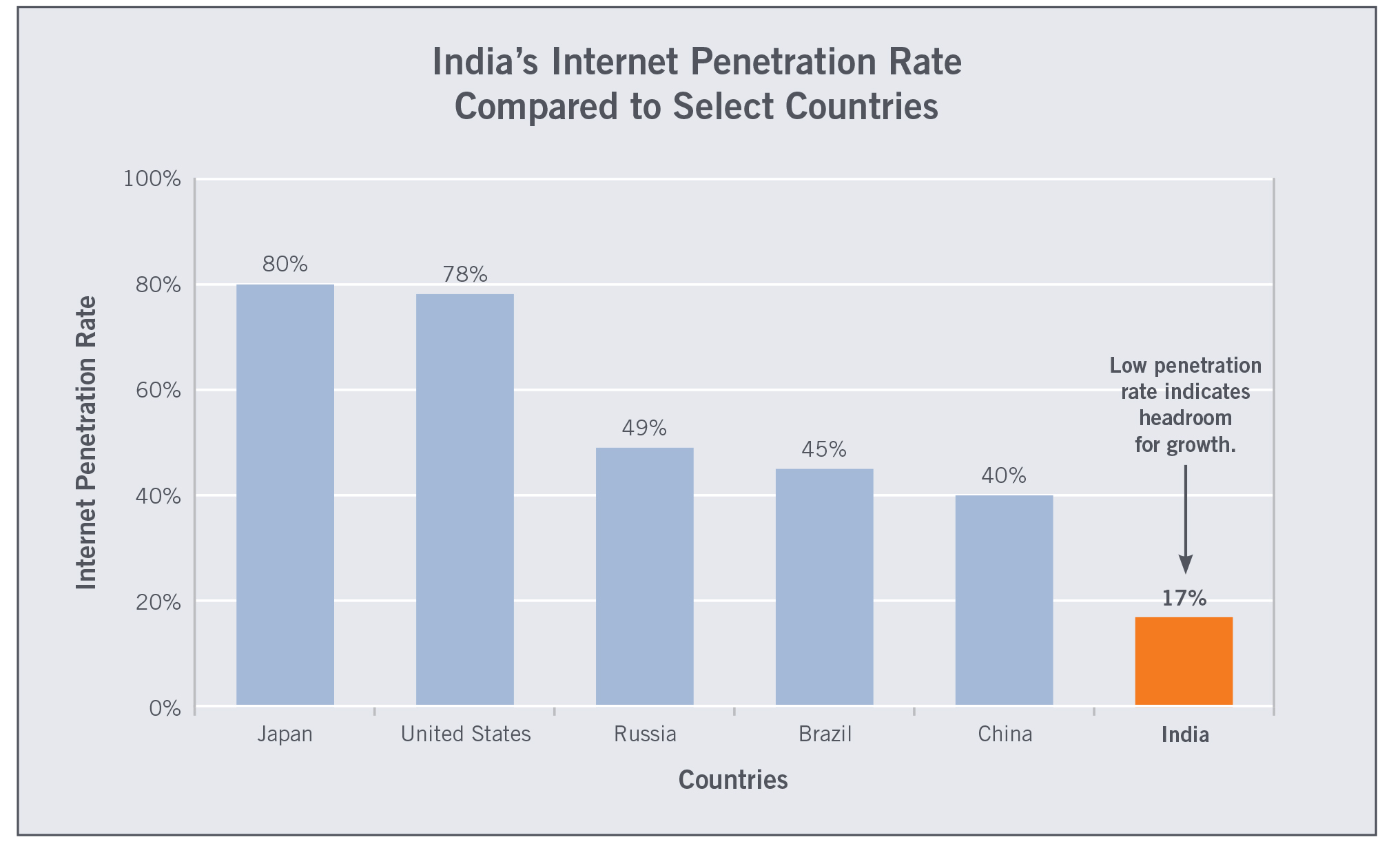

While many of our Indian companies operate globally, the majority are focused on meeting domestic consumer demands within India itself. Given the enormous size of the country’s population and the under-penetration of consumer products and services, we believe these companies have tremendous headroom for growth. This growth potential is a big part of what makes Indian stock valuations so attractive. The charts below indicate the low penetration levels in India for insurance, health care and internet access.

Beyond the areas presented in these charts, we consider consumer products and services to be in a range of industries. These include everything from toothpaste to cell phones and from paint to home finance, all of which are in the early stages of use in India compared to more developed countries. For example, about half of Indians don’t yet have bank accounts. And in a country of over 1.3 billion people, there are less than 10 million mortgages outstanding—most with very low balances.

Recently, investors in India have been encouraged by healthy loan growth, rising corporate profits, and a pickup in monsoon rains that bode well for strong crop output and reduced inflation. The monsoon accounts for more than 70% of the rainfall Indian farmers depend on to grow crops. And because food and beverage costs represent about half of the country’s consumer-price index, an above-average monsoon season helps keep inflation down.

Besides food, the cost of energy also has a significant impact on household and government finances in India.

Sources: Swiss Re, Sigma No 4 /2015, Macquarie Research, September 2015.

Sources: World Bank, Macquarie Research, September 2015.

Sources: IAMAI, Macquarie Research, September 2015.

The steep decline in the price of oil from the highs of 2014 provided a windfall for consumers and allowed the government to curtail spending on the expensive fuel subsidies that had been offered to millions of citizens.

But the government has also raised spending in areas such as infrastructure development and compensation of personnel. For example, in a move designed to boost consumption, Prime Minister Narendra Modi’s cabinet recently approved substantial increases in the salaries of federal-government employees. These increases—coupled with improvements in the banking sector and implementations of key economic initiatives and reforms—add to our bullishness on India.

INDIA’S PLACE WITHIN THE EMERGING-MARKET UNIVERSE

We think India is particularly well-situated to benefit from some general themes affecting emerging markets, which we discussed in two white papers issued in February and March of 2016.

These themes included the following:

- The U.S. dollar looked overvalued to us.

- Emerging-market currencies, by the same token, were likely undervalued.

- The effects of China’s slowing economic growth on local conditions in other emerging markets would probably be limited.

- Commodity prices appeared to be stabilizing.

- Many emerging markets showed signs of improving political conditions.

- Economic reforms were setting the stage for better growth opportunities in emerging markets.

- Emerging-market stock valuations relative to projected growth rates were among the most attractive we’d seen in the preceding five years.

Today, these themes seem to be playing out largely as we had expected. And, broadly speaking, our current outlook is for more of the same.

Another reason we find India so appealing relative to other emerging markets is because it has tended to resist extremes during the last decade, which has made for a more-stable investing environment.

In other words, unlike the volatile conditions we’ve seen in Brazil, Russia and China, we think of India as the “Goldilocks” of emerging markets—not too hot, and not too cold. Also, compared to most developed-market companies, Indian companies seem to have a better balance of reasonable valuations and strong growth prospects.

INDIA’S POLITICAL AND ECONOMIC HISTORY

To put current investment opportunities in perspective, it’s important to understand a bit about India’s political and economic history. After approximately 200 years of British rule, India gained its sovereignty in 1947.

For the next 45 years or so, India struggled under Soviet-inspired economic policies. Small and medium-size businesses were protected, but they were also heavily influenced and regulated by the government. In addition, the government owned and/or controlled many of the larger companies involved in power generation, transportation, sanitation, communications, banking and health care.

While India was a democracy at the time, the country’s top-down bureaucratic controls prevented the economy from making significant progress. Moreover, the country experienced political challenges—including the assassination of Prime Minister Indira Gandhi in 1984.

Things began to change in the early 1990s, although the road remained rocky. Turmoil in the Middle East lessened opportunities for Indians working abroad and led to a drop in foreign reserves. The collapse of the Soviet Union also hurt India’s economy because the two countries had been major trading partners, and India had relied on oil imports from the Soviets. So in 1991, as a condition of receiving help from the International Monetary Fund and the World Bank, India ended its closed-door economic policies.

Since the early 1990s, India has been on a path of improvement with lower tariff levels, currency exchange rate reform, liberalized industrial licensing and relaxed foreign direct investment restrictions. These changes have encouraged multinational corporations to initiate new operations and expand existing operations in India.

From a macro perspective, we believe several conditions have set India up for success. First, the country has been a democratic republic since 1950, which has created a relatively strong adherence to the rule of law.

Second, India’s growing movement toward capitalism has coincided with the country distancing itself economically from Russia starting in 1991.

Third, Indians generally place a high value on education, which in recent decades has led to particular success in the development of technology and health care.

Fourth, India has a long history of welcoming multinational corporations, which has created a culture of strong management, tight business controls, high accounting standards and good corporate governance. As discussed, the relaxation of foreign direct investment restrictions has only increased the activity of multinationals.

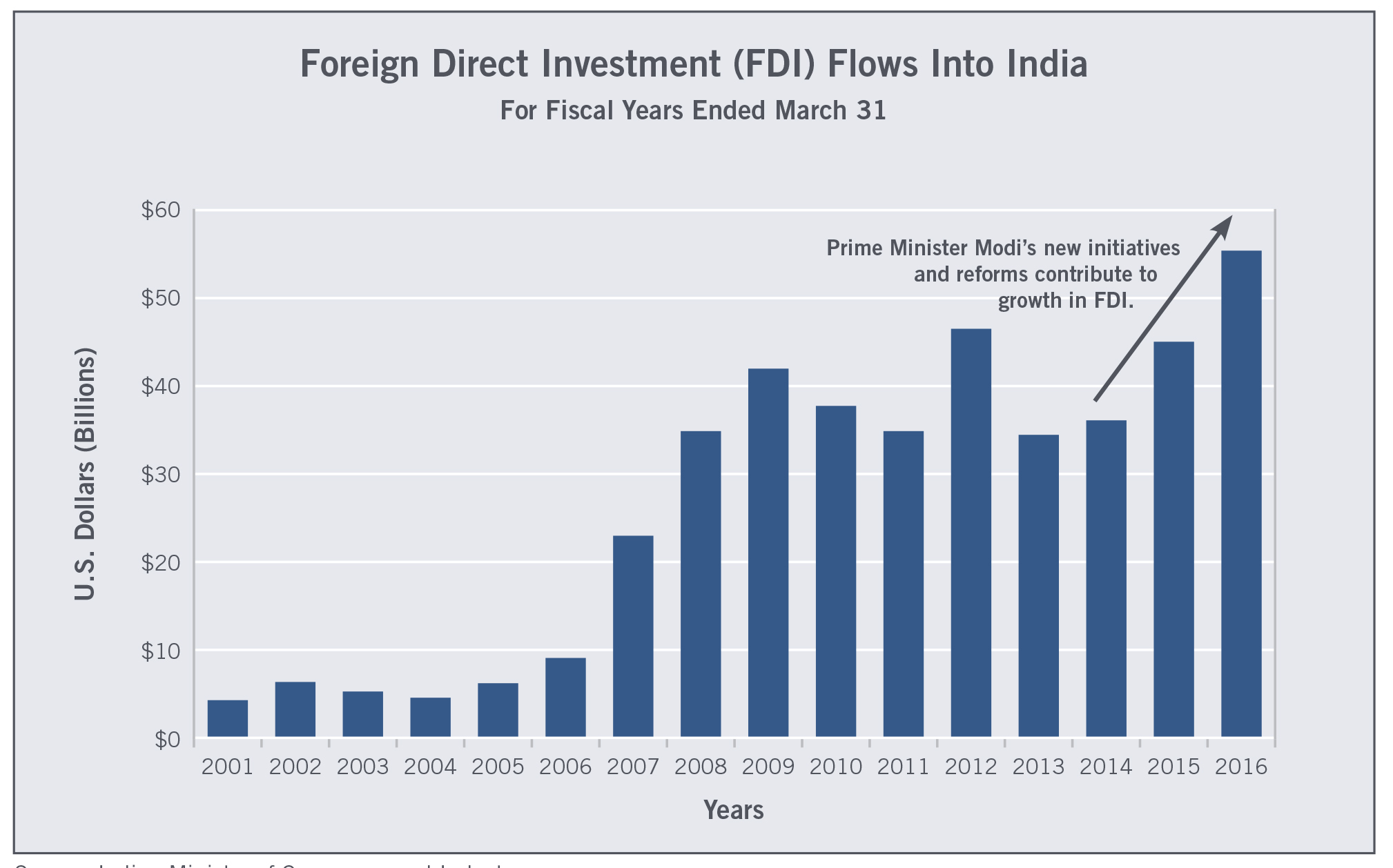

Fifth, the preceding conditions have helped to expand India’s workforce and middle-class population— with a corresponding increase in domestic demand for consumer products. In turn, increased domestic demand has created a virtuous cycle whereby foreign direct investment has become more plentiful, and multinational corporations and local businesses have increased their willingness to expand because they have ready customers. Foreign direct investment flows are presented in the following chart.

Source: Indian Ministry of Commerce and Industry.

INDIA’S ECONOMY AND STOCK MARKET SINCE THE 1990s

After strong progress in the early 1990s, the Indian economy and stock market needed time to digest the radical changes from the post-Soviet era—moving in fits and starts until about 2003. From that point, gross domestic product (GDP) and the stock indices rose in almost uninterrupted parabolic trends until the global financial crisis (GFC) of 2008. Although other emerging markets were also on a positive streak from 2003 through most of 2007, India generally led the way.

In 2008, India and other emerging markets were hit particularly hard due to the global risk-off trade. But they bounced back in 2009 and 2010—again with India leading the way—as investors resumed their world-wide search for growth.

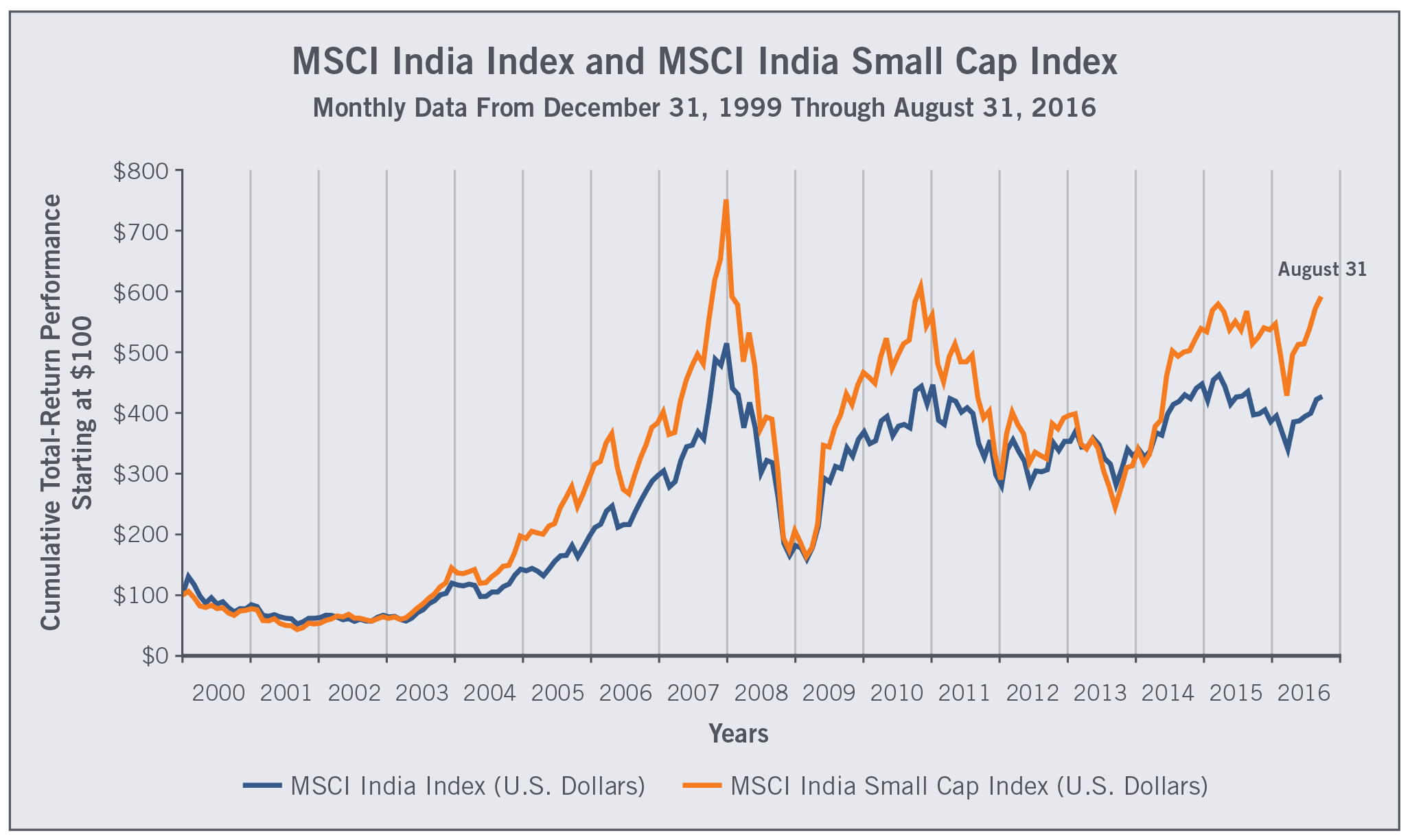

From where we stand today, the past six-year period reminds us of India’s up-and-down path that ended around 2002. At that point in 2002, India’s economy and stock market were set up for durable gains, notwithstanding significant volatility along the way. The MSCI India Index USD and the MSCI India Small Cap Index USD are presented in the following chart, which shows that both indices have made substantial progress since 2002.

Another interesting point is that some broad measures of stock valuations—i.e., price to book value and price to EBITDA (earnings before interest, taxes, depreciation and amortization)—in the Indian market during the early 2000s were similar to valuations we see currently. In other words, unlike many developed-country stock markets that have already exceeded their pre-2008 levels, we think Indian equities have yet to see their full resurgence since the end of the GFC.

RECENT CHALLENGES IN INDIA

As an emerging market, India is subject to the broad short-term trends and scenarios that affect the emerging market group. During the past several years, those trends and scenarios have mostly been related to the following:

- Fears of rising interest rates coming from the U.S. Federal Reserve (Fed), although only one such small increase has actually occurred.

- The strength of the U.S. dollar, which detracted from emerging-market performance for dollar-based investors.

- The slowdown in China’s economic growth, which was feared to impact the country’s emerging-market trading partners—despite the fact that India and China are relatively independent of each other.

- Additional fears that China’s slowdown would precipitate competitive currency devaluations as emerging market countries vied to make their exports more attractive to developed countries.

Source: Morningstar.

- The fall in oil and other commodity prices starting in 2014, even though India is not a large commodity exporter and actually benefits from cheaper oil.

Another challenge was that India suffered from bad loans primarily on the books of state-owned banks that engaged in unsound lending to mismanaged infrastructure companies during the boom coming out of the GFC. India also experienced significant inflation due to high energy prices before 2014 and due to ongoing inefficiencies in power generation, transportation, sanitation, government bureaucracy and taxation. In addition, two poor monsoon seasons caused smaller crop yields and higher food prices.

OPTIMISM FOR INDIA GOING FORWARD

Countering the short-term challenges described above, the following factors make us optimistic regarding India’s political, economic and financial-market conditions in the years ahead.

We think future rate increases from the Fed will be much more muted than originally predicted. We also think the U.S. dollar is still overvalued and emerging market currencies—including the Indian rupee—are undervalued. In addition, while we’re not particularly bullish on China, we think the Chinese economy will muddle through without disrupting most other emerging markets. And when it comes to oil, India is a major importer; so the country should benefit if the price stays at levels lower than during the years leading up to 2014.

Concerning the bad loans on the books of state-owned banks and India’s significant inflation rate, we’ve been impressed by the actions of the RBI, which is the country’s central bank. Dr. Raghuram Rajan, the Governor of the RBI for the three years ended in September of 2016, has been compared to Paul Volcker, the widely acclaimed Fed Chairman who fought inflation in the U.S. from 1979 through the mid-1980s.

Throughout his term, Rajan encouraged India’s state-owned banks to get their problems behind them by writing down bad loans. He also refused to aggressively lower the RBI’s bank rate during the past few years. By keeping interest rates relatively stable, Rajan sought to reduce the current-account deficit, tame consumer-price inflation, defend the Indian rupee from unreasonable devaluation, and encourage well-disciplined investment practices by Indians and foreigners alike.

Although Rajan has now left the RBI, we have confidence in Dr. Urjit Patel, the new Governor who had previously been a deputy under Rajan. We believe Patel will continue to follow Rajan’s game plan. And if consumer-price inflation—which is a better measure than wholesale-price inflation—continues to show improvement, we think Governor Patel may finally have scope to ease interest rates somewhat. With the solid economic foundation that was largely created by Rajan’s policies, a slightly more- accommodative monetary stance may be warranted to help spur growth, especially in an environment where many developed-country central banks have implemented near-zero or even negative interest rates.

In addition to credible central-bank policies in India, we believe there are other reasons for optimism on the inflation front. One reason is that agricultural production methods and regulations will continue to improve. Already, India has made significant agricultural progress, without which the two recent subpar monsoon seasons would have been much more impactful on inflation.

Another reason for optimism is that efficiencies in the Indian economy should improve as the government maintains focus on reforms related to taxation, labor laws, business formation, ongoing corporate compliance, bankruptcy, land rights, general infrastructure spending, transportation systems, energy pricing, power distribution, telecom-spectrum auctions, industrial licenses, foreign investment, municipal finance and the overall regulatory environment.

THE MODI ADMINISTRATION’S NEW INITIATIVES AND REFORMS

Narendra Modi became India’s 15th Prime Minister in May of 2014. Since then, we believe Modi has solidified his support, despite some minor setbacks. Now, with India at a crucial point in its development, much hinges on the Modi administration’s success in implementing its new initiatives and reforms.

We think the recent gains of Modi’s Bharatiya Janata Party (BJP) in state elections have increased the likelihood for consensus on key issues. In the state of Assam, the BJP and its allies made history by winning control of their first state government in India’s northeast. Moreover, the rout of India’s Congress Party carries the message that voters expect their elected leaders to work together to further the country’s growth and development.

The initiatives that the Modi administration has announced are intended to improve conditions within India and to advance the country on the world stage. A few of these initiatives are described below.

- “Make in India” encourages domestic and multinational companies to manufacture their products in India. Make in India places particular emphasis on attracting foreign direct investment.

- “Digital India” has three main goals: 1) Expand the country’s digital infrastructure. 2) Deliver more services digitally. 3) Promote digital literacy. In addition, the Digital India initiative intends to connect rural areas with high-speed internet networks. An outgrowth of this initiative should be more jobs in technology services and electronics manufacturing.

- “Startup India” is aimed at promoting bank financing to boost entrepreneurship and create jobs. Some of the initiative’s key objectives are reducing patent registration fees, easing the burdens of bankruptcy, lowering capital-gains taxes, reducing red tape, improving intellectual-property rights and teaching the skills that are important for entrepreneurs.

In addition to these high-profile initiatives with catchy names, the Modi administration is working on basic priorities such as developing all forms of infrastructure, caring for the environment, enhancing agricultural productivity, improving education and providing affordable housing.

The Modi administration is also seeking reforms of old, bureaucratic practices. Probably the most-important reform is a measure widely supported in Parliament to replace the complicated mix of federal, state and interstate sales taxes with a nationwide goods-and-services tax (GST). Finance Minister Arun Jaitley described the GST as the biggest tax reform since India’s independence.

If enacted, the GST would ease the burden of double taxation and significantly lower the cost of doing business in India, while streamlining tax administration and enforcement. These factors, in turn, are expected to lead to better domestic productivity, improved international competitiveness, stronger economic growth, and higher tax revenues for both the federal government and the states.

In another hopeful sign of things to come, India’s Parliament recently passed a national bankruptcy law designed to streamline the insolvency-resolution process. Because the new law increases the bargaining power of creditors, it’s expected to discourage borrowers from defaulting and lead to better asset recovery by banks and other lenders. In establishing a more-effective way of resolving failed loans, the bankruptcy law removes a major hurdle to the financing of small businesses and other companies important to India’s long-term economic growth.

INDIA’S YOUNG DEMOGRAPHICS SHOULD SUPPORT ECONOMIC GROWTH BASED ON JOB CREATION AND HOUSEHOLD FORMATION

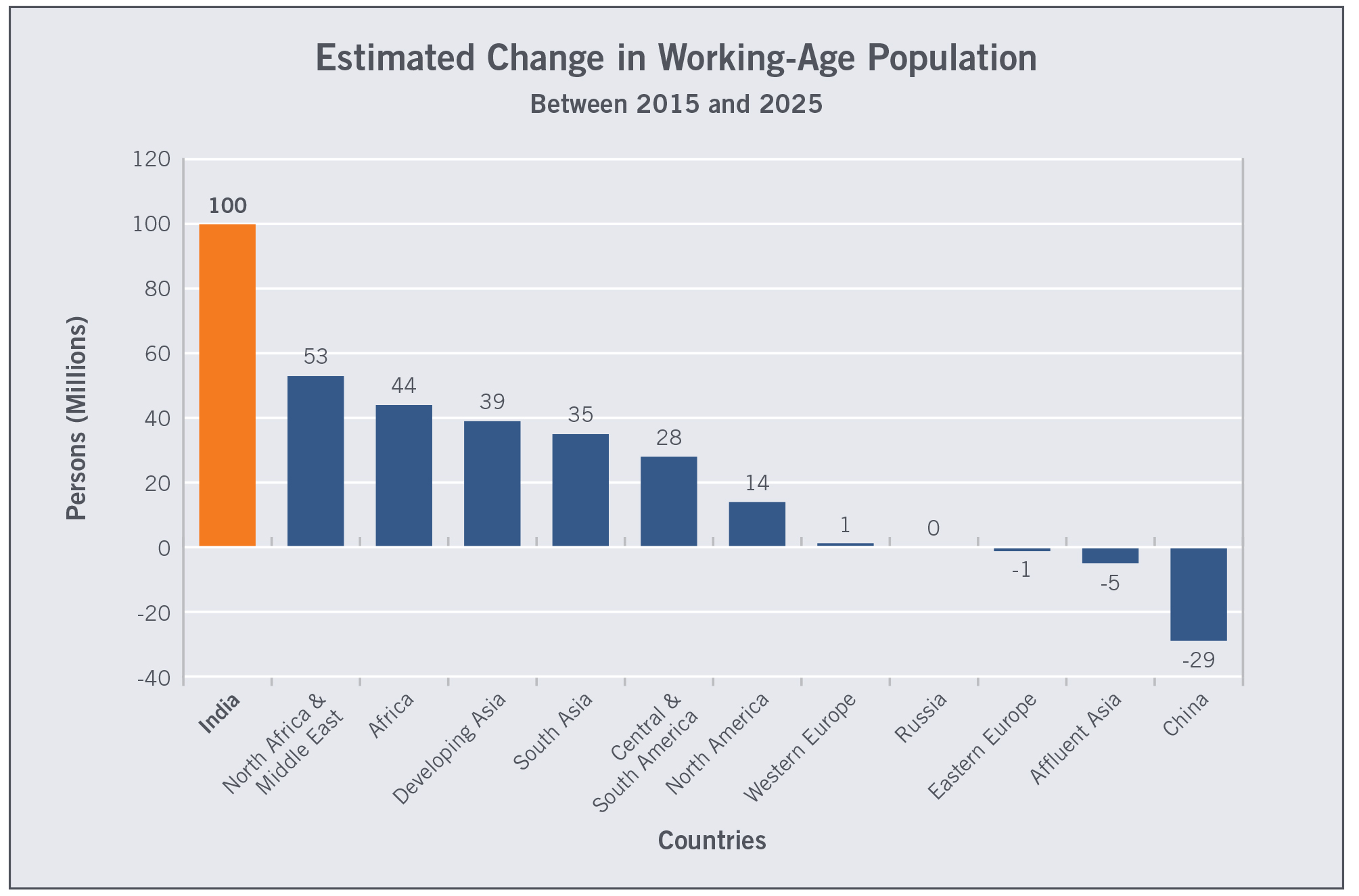

India is a diverse nation of over 1.3 billion people with fantastic demographics. As shown in the first chart on page 9, India leads the world in terms of the estimated change in working-age population. Moreover, with improved agricultural methods, there will be a migration from rural to urban areas. These changes mean India will have to create approximately 10 million jobs per year for decades to come.

While that may seem like a daunting challenge, we think India is well-positioned to meet the challenge with a focus on expanding the country’s power, water, sanitation, transportation and telecommunications infrastructure. In addition, relative to other emerging markets, India has a head start in areas like pharmaceuticals, information technology and business-process outsourcing—which are products and services desired around the world.

As India addresses its infrastructure needs and focuses on its globally competitive industries, the corresponding job growth, rising wages and expanding middle class should lead to more demand for domestic goods and services. This domestic demand, then, should create further opportunities for local businesses and multinationals providing consumer products and services—everything from soft drinks to skin-care products and from fashionable clothing to motorcycles.

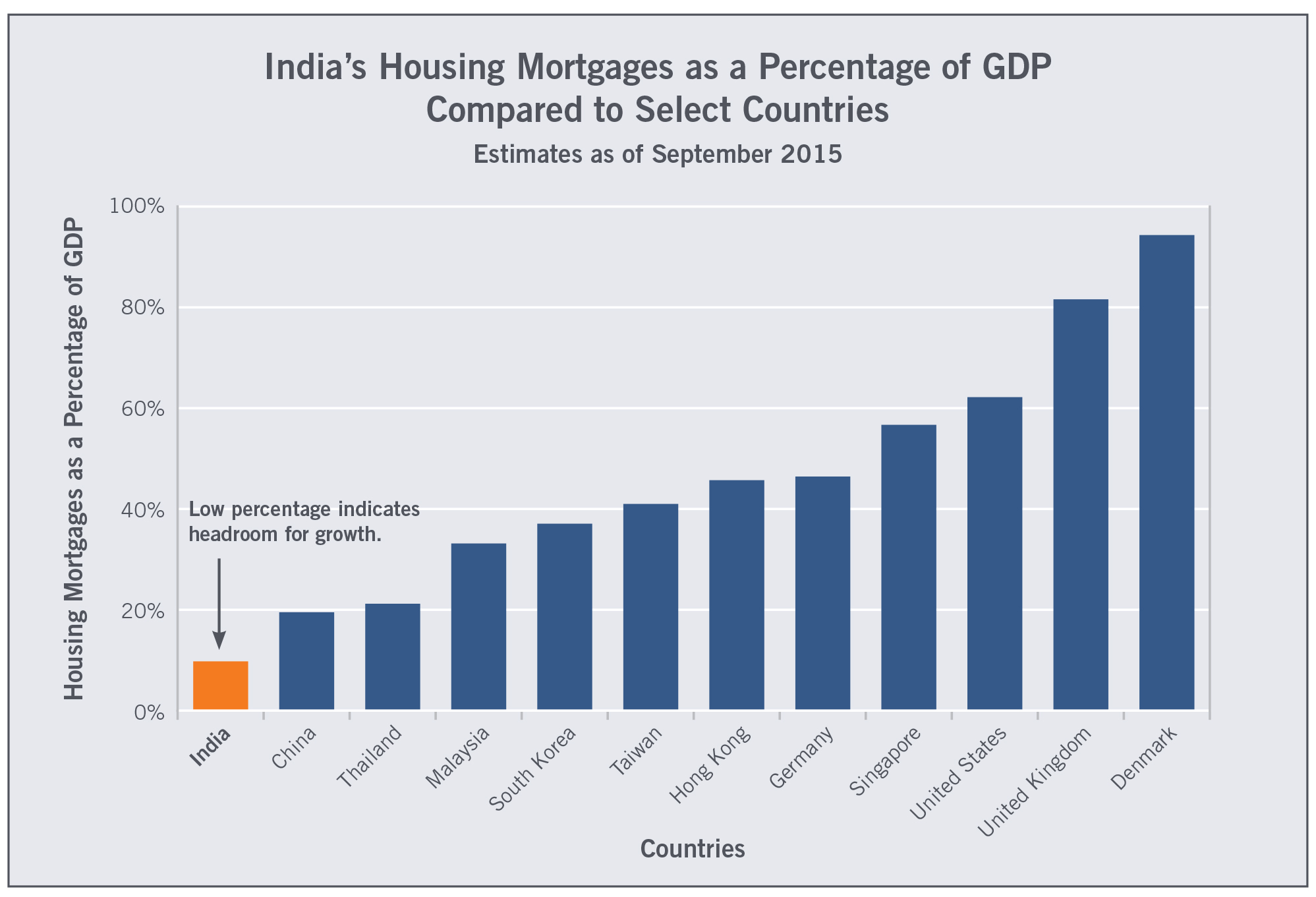

Rapid household formation is another trend occurring in India. The country’s transition from joint-family living arrangements to nuclear-family homes has created growing demand for mortgages, building materials, paints, furniture, and other household-related products and services. One of the reasons investment opportunities are attractive in these areas is because penetration among Indian consumers is so low that the headroom for growth is phenomenal. For example, the under-penetration of mortgages is shown in the second chart on page 9.

INDIA VERSUS OTHER EMERGING MARKETS

Global investors often focus on emerging-market companies that export commodities and low-tech manufactured goods to developed nations. We believe there’s a significant problem with this focus. To a large extent, developed nations are facing disinflation along with an oversupply of many goods. Therefore, the world probably doesn’t need more commodity-oriented and low-tech-manufacturing companies. That’s why we concentrate on companies in other industries—companies such as those in India that sell higher value-added products and services.

Other problems with companies that sell lower value-added products and services are that the returns on equity (ROEs) tend to be relatively small and the commodity businesses in particular are frequently state-owned. At Wasatch Funds, we typically avoid investing in state-owned enterprises (SOEs) because they’re often run more for the benefit of the government than for the benefit of shareholders.

Note: To calculate working-age population, Macquarie Research used the definition of 15-64 years for economies including Africa, Central & South America, Developing Asia, India, North Africa & Middle East and South Asia. For the rest, Macquarie used the definition of 15-74 years to calculate working-age population as the life expectancy in these countries is higher.

Sources: Global Demographics, Macquarie Research, September 2015.

Source: Macquarie Research, September 2015.

On the other hand, Indian companies, partially due to their domestic focus and their expertise in finance, health care and technology, more often exhibit the quality characteristics we look for:

- High ROEs

- Significant cash flows from operations, preferably higher than net income

- Strong free cash flows

- Healthy sales and earnings growth, with headroom for continued growth over the long term

- High value-added goods and services

- Competitive advantages

- Meaningful ownership by company insiders

These characteristics, which aren’t as prevalent in other countries, tend to refute the claim of some investors that Indian companies are among the more-expensive ones in the emerging-market universe.

For our part, rather than invest in an inexpensive Chinese bank operating in a hypercompetitive market, as an example, we’d prefer to pay a somewhat greater price for a high-quality Indian pharmaceutical company that can grow earnings over a long period of time. And our experience in India has been that an investment can keep working for years on end. Conversely, in countries with few barriers to entry, with cut-throat competition and with highly speculative investor behavior, we’ve found that we have to be more trading-oriented because opportunities don’t tend to last as long.

An important point mentioned earlier is that some broad measures of stock valuations—i.e., price to book value and price to EBITDA—in the Indian market during the early 2000s were similar to valuations we see today. Moreover, Indian stocks overall have achieved durable gains since the early 2000s even though performance, like in most countries around the world, has been volatile. Another point to consider when looking at today’s valuations relative to the early 2000s is that today’s cost of capital (i.e., the level of interest rates) is much lower than back then. This point would seem to argue for even higher valuations today. Also note that interest rates could go lower because RBI Governor Rajan held the line on rates during the last three years.

COUNTRY EXPOSURE ALONE IS NOT A GOOD MEASURE OF RISK

In our international, global and emerging markets funds, we certainly consider our exposure to each individual country. But we don’t think that country exposure alone tells us much about the risk a fund is taking.

In the case of India, we think some of the macro forces tend to lower our risk—even if we have a large weighting in the country. These macro forces include the following:

- Political developments are moving in the right direction.

- Current-account and fiscal deficits are under reasonable control.

- Personal savings rates are comparatively high.

- Aggregate government, corporate and household debt as a percentage of GDP is relatively low at 128% for India versus…

- 175% for emerging markets as a group

- 244% for the U.S.

- 249% for China

- 257% for the Eurozone

- 379% for Japan

- Inflation has been tamed.

- Interest rates are attractive to investors, but are not too onerous on borrowers.

And when we look at India’s general portfolio characteristics, we draw similar conclusions about risk. For example, as of August 31, 2016, the five-year beta for the MSCI India Index USD was 0.89, which was below the baseline comparison of 1.00 for the MSCI Emerging Markets Index USD. The betas for the MSCI Brazil Index USD, the MSCI China Index USD and the MSCI Russia Index USD were 1.62, 1.08 and 1.30, respectively, which were much higher than for India and for the baseline.

The same trend holds in looking at betas of small-cap indices: 1.09 for the MSCI India Small Cap Index USD versus 1.00 for the MSCI Emerging Markets Small Cap Index USD, 1.52 for the MSCI Brazil Small Cap Index USD, 1.22 for the MSCI China Small Cap Index USD and 1.54 for the MSCI Russia Small Cap Index USD.

One reason for the relatively low betas of the India indices is less susceptibility to currency fluctuations. Because India has a very diversified business environment, there’s more of a balance among companies that benefit from a stronger rupee and companies that benefit from a weaker rupee. In countries that are dominated by exporters of commodities or low-tech manufactured goods, by contrast, currency movements may create more volatility in business operations and in stock prices. So we look at exposure to the Indian rupee more as a source of diversification than as a source of increased risk.

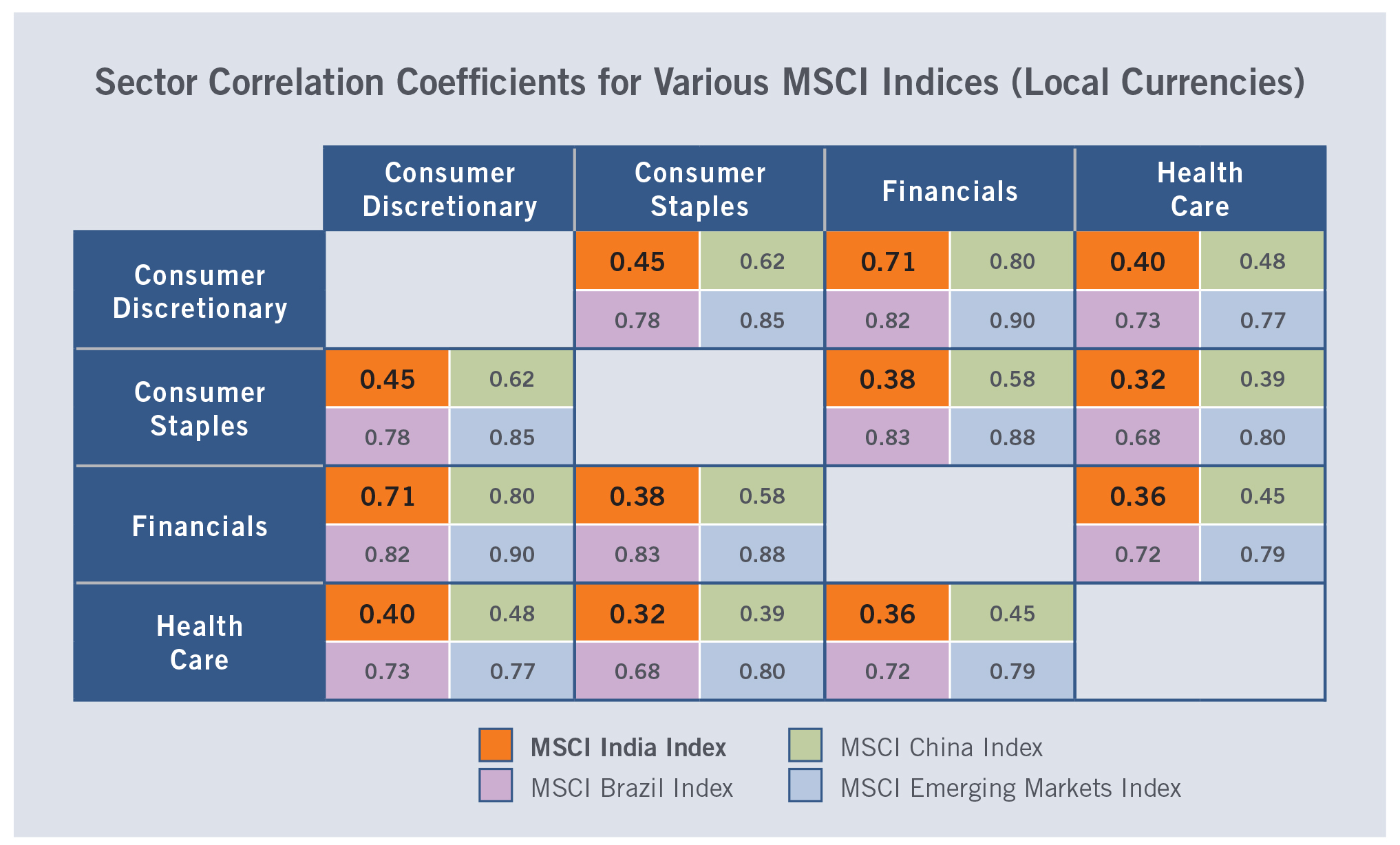

Another way of analyzing risk is to consider sector correlations. We’re most interested in consumer discretionary, consumer staples, financials and health care because these sectors typically have the largest weightings among our Indian holdings. If we look at correlations among these sectors within the MSCI India Index, the MSCI Brazil Index, the MSCI China Index and the MSCI Emerging Markets Index for the five years ended August 31, 2016, we find that the Indian correlations are lower than the Brazilian, Chinese and overall index correlations in every single case. These findings are shown in the table below.

When we think about India, a hardware-versus-software analogy comes to mind. A system can operate to some extent with outdated hardware as long as the software is giving the correct instructions. But state-of-the-art hardware is of little value if the software is providing the wrong signals. So while India’s “hardware” (i.e., infrastructure) needs to be upgraded, the country’s “software” (i.e., political, economic and social fabric) is in fairly good shape. And in terms of this analogy, it’s easier to improve the hardware of a country than the software, which is based on engrained cultural issues.

To summarize, India has one of the fastest-growing economies in the world and is home to a diverse group of businesses. While many of these businesses operate internationally, we’re finding some of the best investment opportunities in those that serve the domestic population, which totals more than 1.3 billion people. In fact, India will soon represent over 20% of all the people on the entire planet. But in order for us to benefit as investors from India’s inherent diversification, we have to invest in the best companies across several different industries and sectors.

THE WASATCH ADVANTAGE: LONG-TERM EXPERIENCE IN INDIA

At Wasatch, we’ve been investing in India for well-over 10 years and our firm is among the relatively few U.S.-based investment advisors that run actively managed funds exclusively invested in Indian stocks. Additionally, compared to their benchmarks, many of our international, global and emerging markets funds are over-weighted in India.

One of our first Indian holdings was HDFC Bank Ltd., which at the time of our initial investment in 2003 had a market capitalization of about USD$2 billion. The market cap has now grown to over USD$50 billion. HDFC Bank exemplifies our focus on banking and financial services, and demonstrates the potential for long-duration growth in India.

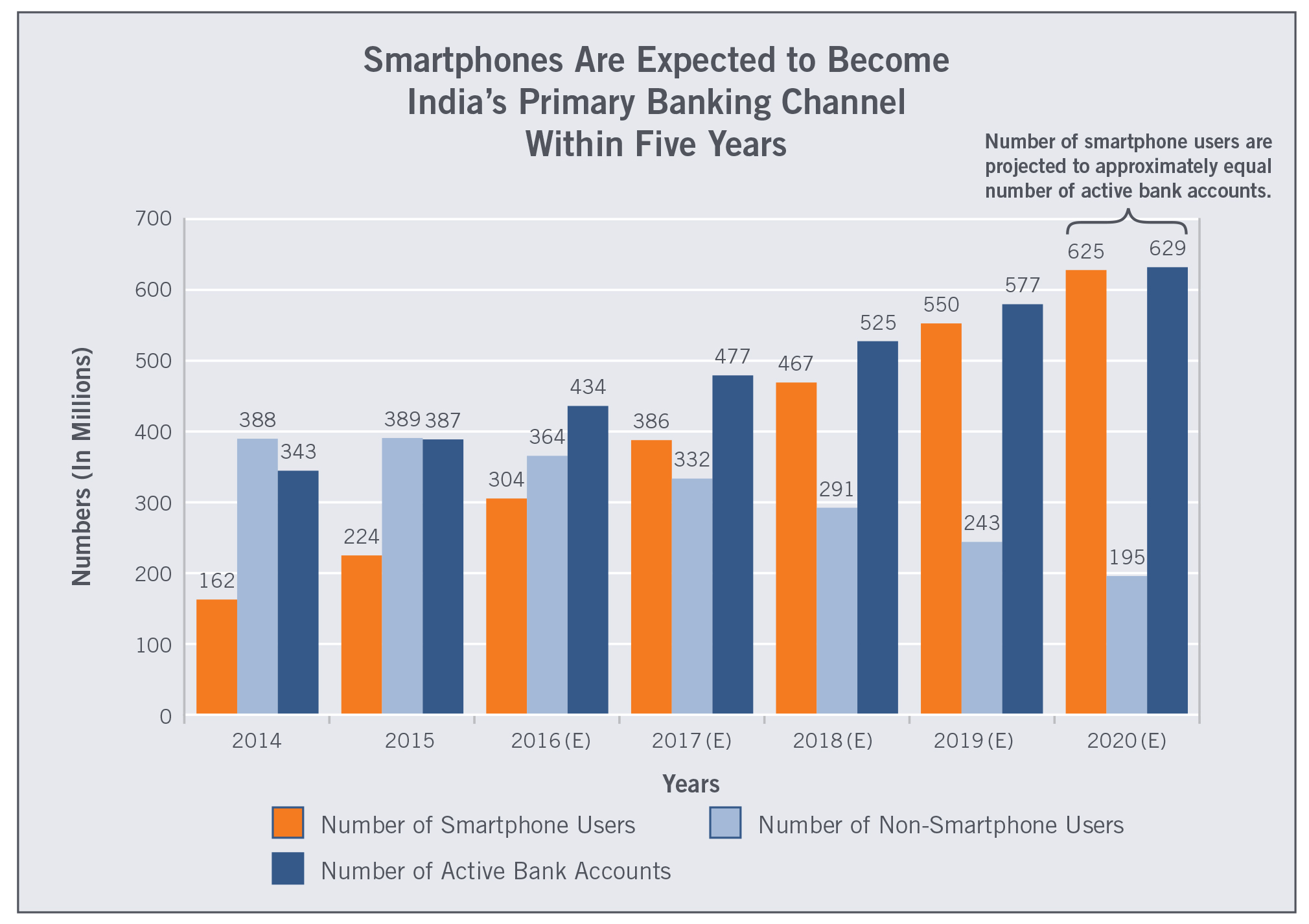

Currently, we think the proliferation of smartphones in India will expand access to banking as all transactions can be accomplished on mobile devices. The projected numbers of smartphone users and active bank accounts are presented in the chart below. From an investment perspective, we believe mobile banking will create exceptional opportunities in the years ahead.

Source: Bloomberg. The chart reports correlation coefficients for the five-year period ended August 31, 2016.

On the other hand, we typically avoid investments in infrastructure and power companies, which are prone to heavy debt levels, earnings disappointments and inconsistent cash flows. Similarly, we’ve never invested in state-owned banks, which we’ve found to be poorly managed compared to their counterparts that are more beholden to shareholder interests.

Another important point is that Wasatch’s investments in India are researched and monitored by a full team of portfolio managers and analysts. Ajay Krishnan leads our effort in India, but six other members of the team also travel to the country regularly.

On average, team members visit India two times per year and meet with around 50 companies during each visit. That’s about 100 company meetings per year, and over 1,000 since we started investing in India more than a decade ago. As a result, when it comes to India, we believe the depth and breadth of our knowledge and experience set us apart from most other investment professionals.

SUMMARY

Perhaps the best way to summarize our optimism regarding India is to look at the chart showing labor productivity growth on page 13.

Despite amazing technological advances in recent years, productivity-growth trends have actually slowed in most major economies. These trends, combined with aging populations in many countries, mean that businesses are competing for market share in industries that often are expanding slowly. Such conditions can make for a more-difficult investment environment.

In India, by contrast, labor productivity growth is at a higher level and has been increasing. Additionally, India should benefit from the Modi administration’s new initiatives and reforms. Furthermore, about 65% of Indians still live in rural areas, which leaves plenty of room for expansion due to urbanization and the rise of the middle class.

These factors mean that domestically oriented Indian businesses are often operating in industries that are getting bigger relatively quickly. From an investor’s perspective, such growth industries are the sweet spots for picking stocks.

Sources: BCG analysis, Kotak Institutional Equities.

*GDP-weighted average of 13 emerging-market countries. **Output-per-person employed, annualized rate of growth; based on data from The Conference Board. Source: © BCA Research 2016 (www.bcaresearch.com).

RISKS AND DISCLOSURES

Investing in foreign securities, especially in emerging markets, entails special risks, such as currency fluctuations and political uncertainties, which are described in more detail in the prospectus. Investing in small and micro-cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds.

Diversification does not eliminate the risk of experiencing investment losses.

An investor should consider investment objectives, risks, charges, and expenses carefully before investing. To obtain a prospectus, containing this and other information, visit www.WasatchFunds.com or call 800.551.1700. Please read it carefully before investing.

Information in this document regarding market or economic trends or the factors influencing historical or future performance reflects the opinions of management as of the date of this document. These statements should not be relied upon for any other purpose. Past performance is no guarantee of future results, and there is no guarantee that the market forecasts discussed will be realized.

The investment objective of the Wasatch Emerging India Fund is long-term growth of capital.

Portfolio holdings are subject to change at any time. References to specific securities should not be construed as recommendations by the Funds or their Advisor. Current and future holdings are subject to risk.

As of June 30, 2016, the Wasatch Emerging India Fund held 0.9% of its net assets in HDFC Bank Ltd.

CFA® is a trademark owned by CFA Institute.

ALPS Distributors, Inc. is not affiliated with Wasatch Advisors.

DEFINITIONS

Beta is a quantitative measure of the volatility of a given stock relative to the overall market. A beta above one is more volatile than the overall market, while a beta below one is less volatile.

Someone who is “bullish” or “a bull” is optimistic with regard to the stock market’s prospects.

A Consumer Price Index (CPI) is a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food and medical care. The CPI is calculated by taking price changes for each item in the predetermined basket of goods and averaging them. The goods are weighted according to their importance.

Correlation, in the financial world, is a statistical measure of how asset classes, sectors, securities, markets, or countries move in relation to each other.

The correlation coefficient is a number between -1.0 and 1.0. If there were no relationship between two variables, the correlation coefficient would be 0. As the strength of the relationship between the two variables increases, so does the correlation coefficient. A perfect positive fit gives a coefficient of 1.0. A perfect negative fit gives a coefficient of -1.0.

Earnings growth is a measure of growth in a company’s net income over a specific period, often one year.

Foreign direct investment (FDI) is an investment made by a company or individual in one country in business interests in another country, in the form of either establishing business operations or acquiring business assets in the other country, such as ownership or controlling interest in a foreign company.

The global financial crisis (GFC) of 2008 is considered by many economists to have been the worst financial crisis since the Great Depression of the 1930s.

Gross domestic product (GDP) is a basic measure of a country’s economic performance and is the market value of all final goods and services made within the borders of a country in a year.

The International Monetary Fund (IMF) is an international organization established in 1945 that aims to promote international trade and monetary cooperation, and stabilization of the world’s currencies. The IMF maintains a monetary pool from which member nations can draw in order to correct a deficit in their balance of payments. It is a specialized agency of the United Nations.

Price-to-book value is a ratio used to compare a company’s book value to its current market price. Book value is the value of a security or asset as entered in a company’s books. Price to EBITDA is the ratio of a company’s stock price to its per share Earnings Before Interest, Taxes, Depreciation and Amortization.

Price to EBITDA is similar in concept to the price to earnings ratio.

Return on equity (ROE) measures a company’s efficiency at generating profits from shareholders’ equity.

“Risk-off” is when investors become more cautious and take money out of the market, not being willing to risk it, thus risk off.

Valuation is the process of determining the current worth of an asset or company.

The World Bank is a collection of international organizations that aid countries in their process of economic development with loans, advice and research. It was founded in the 1940s to aid Western European countries after World War II with capital.

The MSCI India Index is designed to measure the performance of the large and mid cap segments of the Indian market. With 74 constituents, the index covers approximately 85% of the Indian equity universe. The MSCI Brazil Index is designed to measure the performance of the large and mid cap segments of the Brazilian market. With 60 constituents, the index covers about 85% of the Brazilian equity universe. The MSCI China Index captures large and mid cap representation across China H shares, B shares, Red chips and P chips. With 151 constituents, the index covers about 85% of this China equity universe. The MSCI Russia Index is designed to measure the performance of the large and mid cap segments of the Russian market. With 21 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in Russia. The MSCI Emerging Markets Index captures large and mid cap representation across 23 emerging market countries. With 836 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country.

The MSCI India Small Cap Index is designed to measure the performance of the small cap segment of the Indian market. With 249 constituents, the index represents approximately 14% of the free float-adjusted market capitalization of the India equity universe. The MSCI Brazil Small Cap Index is designed to measure the performance of the small cap segment of the Brazilian market. With 50 constituents, the index represents approximately 14% of the free float-adjusted market capitalization of the Brazil equity universe. The MSCI China Small Cap Index is designed to measure the performance of the small cap segment of the China market. With 441 constituents, the index represents approximately 14% of the free float-adjusted market capitalization of the China equity universe. The MSCI Russia Small Cap Index is designed to measure the performance of the small cap segment of the Russian market. The index represents approximately 14% of the free float-adjusted market capitalization in Russia. The MSCI Emerging Markets Small Cap Index includes small cap representation across 23 emerging market countries. With 1,907 constituents, the index covers approximately 14% of the free float-adjusted market capitalization in each country.

You cannot invest in these or any indices.

Source: MSCI. The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties or originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

© 2016 Wasatch Funds. All rights reserved. Wasatch Funds are distributed by ALPS Distributors, Inc. WAS004242 10/30/2017

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits