In order to make sense of what is taking place in our economy, capital markets and even our society, we are working within a paradigm in which we assume that our form of democracy and capitalism is changing at a more rapid pace than before. While our form of government is stable our form of democracy is evolving. This assumption underscores the current debate around such issues as direct government intervention in our capital markets, domestic surveillance on the “war on terror, “ the ability for large banks to fail, and what the appropriate price is for a consumer to pay for a drug produced by a pharmaceutical company. American citizens have a high degree of freedom in our society, including the ability to participate in politics and choose our leaders. But, many issues that may include social justice, power, wealth, regulation, and corporate ambition continue to shape our democracy in evolving ways and impact our capital markets. This presidential election, with two of the most unpopular candidates in recent history, may be another example of this evolving democracy.

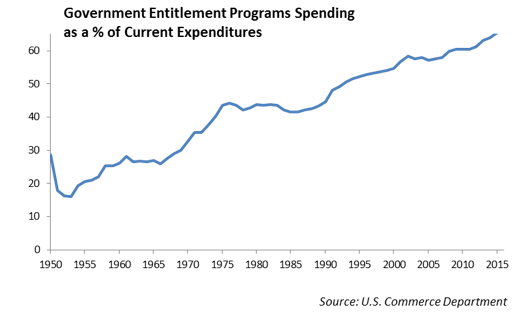

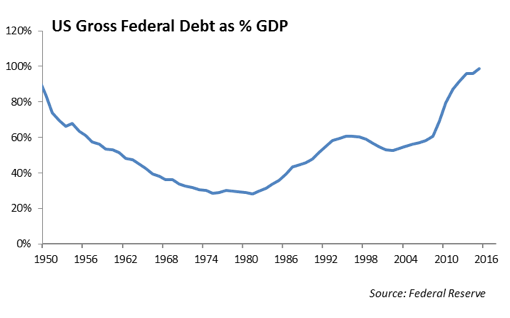

The most frequent question we have been getting recently is: “How will the election impact the financial markets?” While political uncertainty may marginally weigh on economic growth, at the end of the day, the Presidential election does not matter. The surviving candidate will need to work with Congress in order to effectively legislate and govern this country. The dysfunction playing out in the election campaign, for the moment, is taking the focus off the dysfunction that has besieged Congress over the past eight years. And, at the end of the day, there is still no political will to address the growing cost of the entitlement programs, which now represent over 60% of the annual government outlays. Since 2008, U.S. debt has grown to 100% of GDP from 60%; however, the domestic economy has grown by less than 1% adjusted for inflation. The use of debt to fund our way of life is not limited to just the United States. According to a study published by the Bank for International Settlements, global debt hit 235% of gross domestic product at the end of 2015. This is up from 212% prior to the Financial Crisis.

In order to maintain a modicum of economic stability and growth during the fragile economic recovery that followed the Financial Crisis, our central bank, along with most other central banks of developed countries, has flooded the capital markets with money which helped to grease the wheels of commerce by lowering interest rates. However, these aggressive monetary programs, which in some countries have produced negative interest rates, have supplanted sound fiscal policy initiatives. Remember, monetary policy and fiscal policy should work together alongside each other to propel growth in an economy. The leadership of our evolving form of democracy does not have the vision, the courage, or the political will to implement fiscal reforms which will help limit the growth in debt and set a foundation for domestic economic growth. With this presidential election, we expect four more years of dysfunction between the administrative and legislative branches of government regardless of who is elected president.

A growing concern from our economic analysis is the increase in dispersion in income levels in the United States. We thought the class system that defined life in Great Britain, Europe and the United States at the turn of the 20th century was long gone. After World War II, a college education and job training provided a strong catalyst for a growing middle class. However, flying back to the United States from London last week, we were struck that Virgin Airlines has a passenger travel status called “Upper Class”. Sadly, we wonder if this were true of society today as well. We view the growing income inequality in the United States as one of the more devastating trends in our democracy. In his recent book Capital in the Twenty-First Century, French economist Thomas Picketty makes the point that unless we do something, capitalism today is on a one-way journey toward inequality. Since the Financial Crisis, we have been living through years of wage stagnation, lopsided tax policies and distorted labor markets which are influencing our political agenda and priorities as a society. The recent years of dysfunction in Congress have done little to help change this direction.

The Economy

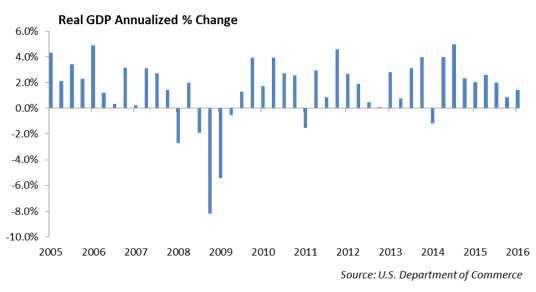

The domestic economy has been relatively stable and appears to be growing at 1.5% to 1.8% measured by Gross Domestic Product. We see no reason at this point for that to change. An increase in employment opportunities is critical to getting our economy on a path toward sustained growth. The unemployment rate has been consistently below 5% and we are seeing gains in jobs begin to moderate. The economy has produced an average of 200,000 jobs per month over the past year; however, the participation in the labor force has been bumping near its lowest level in 40 years. While the median household income rose 5.2% last year, its biggest annual increase since 1967, it remains below the high levels of 2007.

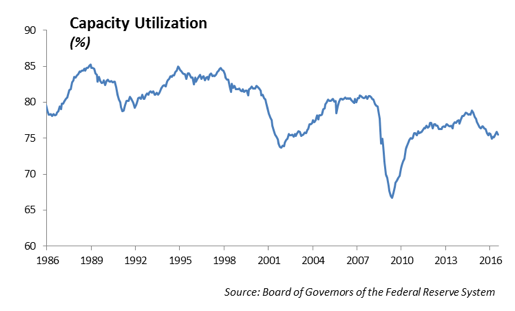

There are clear signs that the economy is showing signs of improvement. Retail sales, job growth, and industrial production are showing signs of improvement. We are at that point in the economic recovery where we would normally begin to see inflation pressures due to tightening in the labor market, but it is just not happening. We believe there are two main reasons for this. First, the job growth in the economy is skewed toward low level service sector and part-time jobs that do not offer higher wages. Second, there is still a high level of excess capacity in the economy. Capacity utilization peaked at 78% in 2014 and has been consistently in decline trailing to 76%. While the fall off is not dramatic, it does underscore the slack in the economy and the challenge that the Fed has to continue to stimulate growth with a limited set of tools.

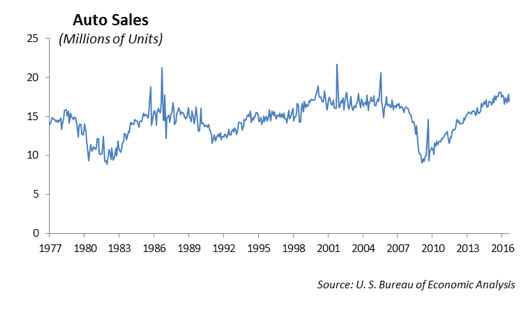

With a modest improvement in disposable income and improved household balance sheets, the consumer sector appears to be doing well. We expect the holiday shopping season to be better than last year and think it will be a boost to a struggling retail sector. However, the manufacturing sector has showed signs of slowing and we are focused on the recent decline in domestic auto sales. Auto lending has been fairly aggressive over the past two years, and we are watching non-performing loans and loan loss reserves increase in the sub-prime auto loan market.

We are challenged to reconcile our current economic growth paradigm with historic domestic growth of 4.5% to 6.0% (which we experienced in the 1990’s). The domestic economy has the potential for higher growth, but continues to be plagued by slack resources including imbalances in the labor market, excess capacity and slow productivity gains. At our core, we are fundamental free market capitalists. We believe small business is the engine that drives domestic economic growth. Through small business growth comes job growth and increases in wages. Over the past eight years, the heart of the problem is the lack of business formation in the economy. There are a number of reasons for this including increased regulatory environment and lack of private credit expansion.

Monetary Policy

There is a significant amount of attention placed by the mainstream media on the Fed’s next move in interest rates. The Fed is still trying to move away from its emergency liquidity policies it implemented after the Financial Crisis in 2008 – 2009 and is still operating in an artificially low policy range for targeted interest rates. As a result, the next 25 basis point increase in short term interest rates will not have a material impact on the flow of private credit as the economy and capital markets benefit from extremely low interest rates.

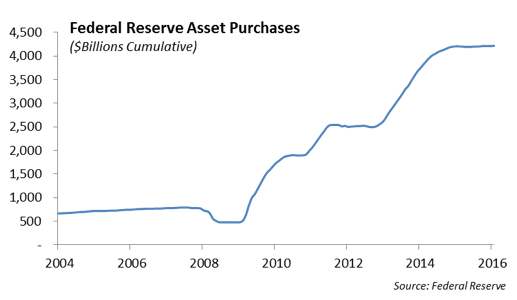

The Federal Reserve took historic steps to prop up our economy and capital markets during the financial crisis and, in doing so, effectively marshalled in a new monetary regime using quantitative easing to help lower interest rates. This new monetary regime has shifted a focus from measuring a targeted Fed Funds rate to calibrate short term interest rates in an attempt to impact private credit flows and, ultimately the pace of economic growth. We believe that monetary regimes do shift over time and we are operating in a new regime that leverages the Federal Reserve’s balance sheet in order to impact the level of interest rates along the yield curve. Since the Financial Crisis, the Federal Reserve has implemented four bond buying programs totaling $4.5 trillion which have effectively lowered interest rates along the yield curve.

However, eight years after the Financial Crisis, the Fed is still stuck trying to jettison itself from these crisis management policy tools. And, we suspect that they have missed several opportunities to increase rates along the way. We also believe that the economic impact of these tools is waning which could have serious implications for the next downturn in economic activity.

We began 2016 with a “one-and-done” belief that the Fed would raise short term interest rates only once this year; however, if the data heading into the fourth quarter remains on track, we expect the Fed will increase rates in December. The reasons this is important are that the Fed believes that they need to be able to adjust rates lower if the economy were to slow and that there is a potential bubble forming in asset values including publicly traded securities and commercial real estate. Increasing interest rates may, at the margin help to curb the inflation in these assets. We doubt it.

From a global perspective, the push toward negative interest rates from central banks of developed countries is fraught with trouble. Societies that are premised on open and free capital markets will not sustain over the long term with negative interest rates. These policies ultimately penalize savers and benefit lenders while adding leverage to the financial system in an attempt to jump start economic growth. The consequence to these policies is that it increases debt in the system and weakens financial firms, including banks and insurance companies, which cannot invest their assets in securities that result in a sustained and viable spread over its liabilities. Paradoxically, in some countries it appears to also promote savings which is the opposite intended effect. The European Central Bank is considering curtailing their experiment with negative interest rates, which has been in place since 2014, due in part to the fear that bank lending is contracting.

The Financial System and Global Growth

The global economy appears to be caught in a spiral of slowing growth. The International Monetary Fund and the World Bank have revised their projects for global growth once again to 3.1% in 2016 and 3.4% in 2017. The discontent of slow economic growth and little meaningful job growth leads to discontent which leads to protectionism and trade renegotiation which leads to slow economic growth.

The banking system is critical to global economic growth because it is the primary source of credit. Without growth in credit there will not be economic growth. While the banking system has worked diligently to bolster capital levels under Basel III, several of the European banks are still undercapitalized. Several Italian banks are under scrutiny for their troubled loan portfolios. What is believed to be the oldest bank in the world, Monte dei Paschi di Siena, and the third largest lender in Italy, is facing a €5 billion recapitalization which is critical to the Italian banking system.

Germany has traditionally had more conservative banks; however, Deutsche Bank has been a source of volatility in the capital markets recently as a recent $14 billion fine by U.S. regulators for its malfeasance in the mortgage loan market leading up to the Financial Crisis combined with their weaker capital levels caused solvency concerns in the capital markets. A financial crisis always spreads through the global banking system. The markets are concerned about systemic risk and the contagion that spreads due to weak players in the banking system. We believe that Deutsche Bank has a profits problem and not a solvency problem and they will be able to shore up their capital position while retaining their investment grade ratings.

Traditional banking, in which a bank takes in deposits and lends money in the form of a loan, appears to be suffering under a post-Glass Steagall regulatory environment. This is best illustrated by the public debacle that Wells Fargo is going through over its inability to effectively manage its sales culture. Every major bank attempts to cross sell products and services to its clients in an effort to boost its fee income. When we combine this quest for higher fee income with the more stringent regulatory environment that banks are operating under after the Financial Crisis, loan growth has been relatively slow which has muted the flow of credit, which in turn, has been a contributing factor holding economic growth below its potential. In order to have sustained economic growth, we believe there must be private credit expansion. Without credit, capital market activity is limited. Private credit growth continues to be problematic and has been a contributing factor to limiting business formation, particularly in small business.

Brexit

Brexit will be part of our lexicon for the next several years and is one of the major issues facing the global economy. We were recently in London doing some work on the impact of Brexit on the British and U.S. economy. First, our initial assessment of a dramatic recession in the United Kingdom may have been wrong. The British economy appears vibrant and has shown initial resilience. Recent hard line rhetoric from Prime Minister Theresa May indicate she is not inclined to string out the separation and is leaning toward a hard exit.

Our talks with corporate leadership during our trip reveals a theme of uncertainty and optimism underscoring the next few years. The decisions to invest in new facilities, reconfigure logistics and supply chains, modify software and relocate corporate offices and employees will be at a significant cost and take a significant amount of time. Obviously, there is tremendous uncertainty around details at this point. We find it interesting that the recent EU decision to go after Apple for failure to pay €13 billion in Irish taxes (over the objections of Ireland) may prove to work in favor of Britain as it works to retain business. Apple’s announcement last month that it would create a European headquarters in London and move 1,400 jobs is one example.

Prime Minister Theresa May has indicated that she will invoke Article 50 of the Lisbon Treaty by the end of March 2017. This will trigger the two year period in which a country begins the negotiating process to exit the European Union. Regardless of how fast Great Britain and the European Union move toward a real separation, the infrastructure and job skills that exist in Great Britain, particularly London, will take a long time to replicate in the major cities in Europe. Within the financial services industry, for example, there is not one city that has the infrastructure, technology and skilled labor pool to support securities trading and investment on the scale that London has at this point.

Investment Strategy

We believe that there is a natural ceiling to how high interest rates can move in the global capital markets. With the ten year U.S. Treasury yield over 1.75%, the United States is offering one of the most attractive investment rates of all developed countries. As the Fed pushed rates higher, we would expect more capital to flow into U.S. dollar denominated securities, which in turn would pressure the US dollar exchange rate higher and U.S. interest rates lower.

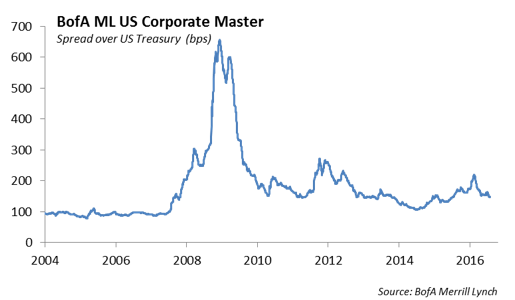

We are in the eighth inning of a credit cycle that has been stimulated through aggressively low interest rates; but at the same time has been hampered by a general lack of loan growth through the banking system. We expect to see an increase in distressed credits and workouts in the bond market. However, in contrast recent bank earnings show that the banks are actually reducing their allowance for loan losses this past quarter. Since the problems in the energy sector, which peaked in the first quarter, we have seen significant spread tightening in the high yield sector and are close to the tight levels of 2005. Much of the high yield energy sector has been able to restructure their capital and avoid bankruptcy.

The unusual low level of volatility that is gripping the capital markets has helped to tighten spreads in the investment grade bond market. Along with tighter spreads and low interest rates, corporations have issued record levels of debt to fund their stock repurchase programs. So far in 2016, investment grade non-financial debt issuance hit a record with over $670 billion according to Dealogic, surpassing the total year 2015 issuance of $660 billion. The use of increased leverage to fund stock repurchase programs can erode credit fundamentals and long-term will prove troublesome for bond investors.

Equities

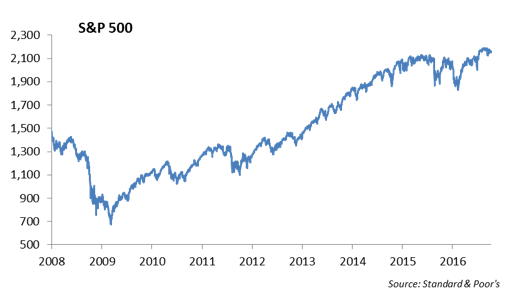

The S&P 500 increased 7.84% year-to-date through the end of the third quarter. The underlying fundamentals supporting domestic equity valuations appear generally stable; however, operating earnings for the S&P 500 are set to fall for the sixth straight quarter. In addition, the overall risk in the market appears higher in front of the Presidential election. Also, the generous stimulus from the Fed seems to be running its course and the eventual transition to a more normalized monetary policy may be weighing on the market. The consensus for estimated growth in S&P 500 earnings for 2017 is expected to be a robust 20% due to the roll off of declining energy earnings. However, we believe earnings will come in much lower due to our macro outlook. In a large part, the turmoil in the energy sector over the past year will be behind us and oil appears to be stabilizing between $45 and $50 per barrel over the near term.

As investors chased yield throughout this year, prices on high dividend stocks have been driven up. For example, year-to-date total returns in the telecom sector are +10%. We believe that low volatility stocks, including stocks in the domestic telecom, utilities and real estate investment trusts, are vulnerable given the run up in prices. We are concerned, given extended valuations in these sectors that expected returns will be challenged given our assumptions for earnings growth.

The recovery rally in energy stocks this past quarter has been strong and still has room to move further. With news that the Organization of Petroleum Exporting Countries agreed to cut production, this should help supply and be a catalyst for oil prices to creep higher. In addition, we are constructive on stocks in the technology and healthcare sectors as we move into the end of the year.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2016 Winthrop Capital Management

Read more commentaries by Winthrop Capital Management