Is Weak Productivity to Blame for Sluggish Consumer Spending?

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits

This week I presented at the MoneyShow in Dallas, where sentiment toward gold was a bit muted compared to other recent conferences I’ve attended. The yellow metal has certainly taken a breather following its phenomenal first half of the year, but the drivers are still firmly in place for another rally: low to negative government bond yields; economic and geopolitical uncertainty; and a lack of faith in global monetary policy.

I want to thank my friend Kim Githler for hosting the MoneyShow. Every year since she founded the event in 1981, she’s captivated audiences with her intelligence, sharp wit and honesty.

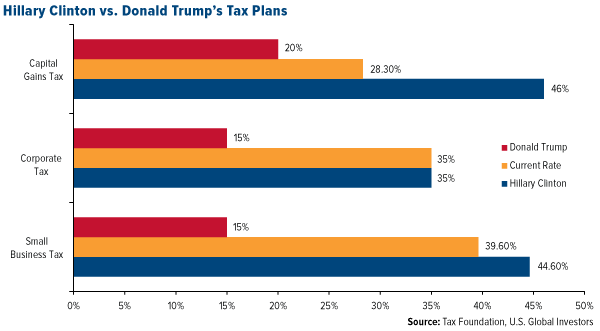

One of the highlights of the event was listening to American economist Art Laffer, whose “Laffer curve” shows that the government can actually bring in more revenue if tax rates are kept low. Art’s theory was used as the basis for President Ronald Reagan’s free-trade, low-tax policies. Later, Art actually supported Bill Clinton because he was willing to streamline taxes and regulations.

The same cannot, I’m afraid, be said of his wife Hillary, who plans to raise taxes at nearly every level.

Although bad for your pocketbook and savings, the possibility of higher taxes is expected to increase interest in tax-free municipal bonds, especially among top earners. For over a year now, muni bond funds have seen positive weekly inflows, with $147 million going in during the week ended October 17. I expect this trend to continue as we head closer to the election, and beyond.

The Republicans at the event, meanwhile, were almost unanimously disappointed in their candidate Donald Trump. Many of the grievances had to do with his inability to stay on message. If he would simply stick to key issues such as public safety, immigration and minimizing taxes and regulations, he might have a clear shot at the presidency. Instead, he too easily walks into personal traps set by the media and the Clinton campaign.

Where’s the Retail Spending?

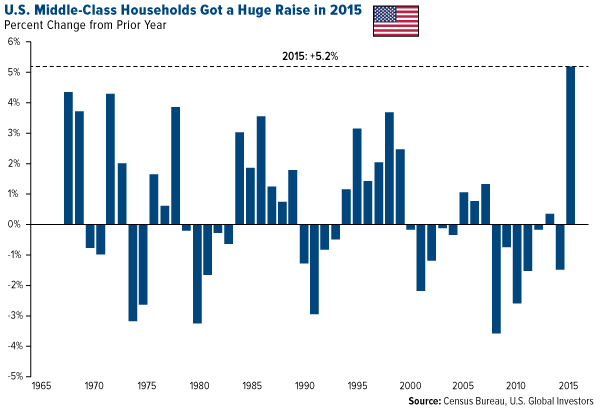

Maybe you haven’t heard yet, but you got a raise in 2015 without even realizing it. At least, that’s what the Census Bureau revealed last month. U.S. household income rose 5.2 percent, the fastest on record.

This falls in line with other recent news that appears to show that the U.S. economy is humming once again, nearly a decade after the 2007-2008 financial crisis.

With unemployment at 5 percent, initial jobless claims fell to a four-decade low this month, while the labor-force participation rate—the share of working-age Americans who are working or actively seeking work—has finally begun to perk up. Also improving is the voluntary quits rate, which indicates workers now have enough confidence in the labor market to walk away from their current jobs and quickly find new ones.

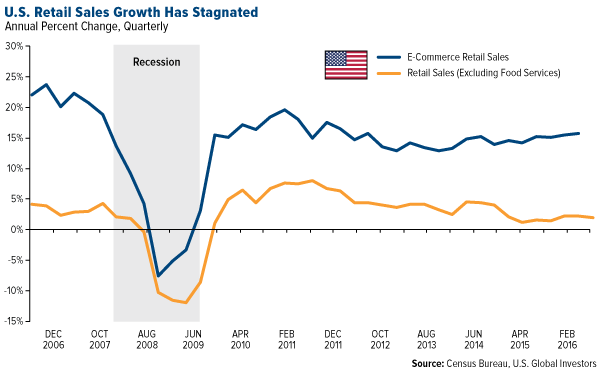

As encouraging as this all is, I have to look at the consumer discretionary sector and wonder why we’re not seeing healthier consumption. (This is important, as spending accounts for roughly two-thirds of gross domestic product.) If more Americans have better-paying jobs, as the data seem to indicate, and they’re feeling good about parting with their money, why aren’t retail sales surging?

Instead, sales growth, excluding food services, has steadily been weakening. E-commerce sales growth looks strong, but the entire industry can’t be propped up by Amazon alone.

Confirming this is Bank of America Merrill Lynch’s latest report on debit and credit card spending, which showed a “substantial slowdown” in retail sales, ex-autos, in September, according to Zero Hedge.

Despite the release of the iPhone 7 in September, BofAML didn’t see “a spike in electronic store sales akin to prior releases of Apple devices. It may be a reflection of the iPhone 7 or perhaps the trend in electronic store sales ex-iPhone is sluggish.”

The bank raises a couple of good points here. Apple’s latest smartphone was met with criticism stemming from its lack of a headphone jack, which might have dissuaded some consumers from upgrading.

And as many others have pointed out, it’s possible we’ve finally reached “iPhone fatigue.” Most everyone now owns a satisfactory smartphone—so long as it doesn’t explode—so consumers could simply be holding out for the next must-have gadget. Maybe they’ll find it in Facebook’s virtual reality Oculus Rift headset, but with its price tag still hovering above $800, it might take some time before consumers feel comfortable enough to buy it.

Automobiles and Housing Affected, Too

This goes far beyond smartphones. Big-ticket items such as automobiles and homes are also seeing sluggish, or even negative, growth. The S&P Global Ratings recently cut its automobile sales estimate for the year to 17.5 million from 17.8 million.

Facing inventory build-up, Ford Motor announced it would temporarily halt production at four of its factories both here in the U.S. and Mexico, Bloomberg reports. One of these factories, in Kansas City, builds the bestselling F-150 pickup.

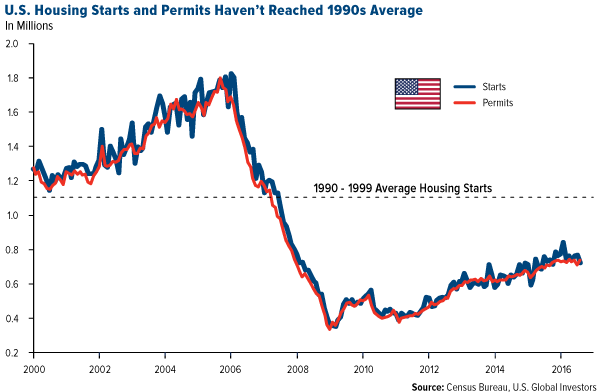

Meanwhile, the momentum of new housing starts and permits has also slowed, with starts falling in September for the second straight month. Despite improvement since the housing bubble, we still aren’t close to where we were pre-recession, let alone the 1990s average.

The Slowest Recovery Since the Great Depression

Household income is up, unemployment is down—and yet sales are stagnant. It’s a paradox.

A paradox, that is, until we examine another economic indicator: labor productivity.

In simple terms, productivity means labor efficiency—producing more goods and services without working longer hours. And when productivity rises, it increases our standards of living.

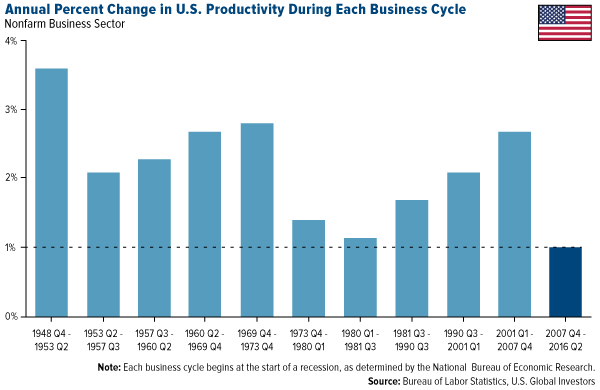

Since the end of World War II, productivity rose pretty steadily. But growth has been near-anemic for close to a decade now and is currently running lower than it’s ever been.

Consider the following chart. Each bar represents a new business cycle following a recession. Crawling along at 1 percent annually, today’s productivity growth is weaker than the previous 10 cycles. In the September quarter, it actually fell 0.6 percent.

The big question is: Why is this happening?

The answer depends on who or which economist you ask.

Possible factors that have been tossed around include the aging of the workforce, the strong dollar (which reduces the competitiveness of U.S. companies) and a slowdown in capital spending by businesses since the recession.

One of the leading theories, presented by economist Robert J. Gordon in his recent book “The Rise and Fall of American Growth,” argues that 19th and 20th-century innovations—air conditioning, indoor plumbing, the microwave, the automobile—were much more impactful on workers’ productivity than modern inventions such as the internet, cloud computing and smartphone apps. (Indeed, we’d probably all agree that these things often waste, instead of enhance, our time and energy.)

$740 Billion in New Compliance Costs

We can add to the list the growing mountain of regulations, a topic I’ve discussed many times before. According to the American Action Forum, there’s been, on average, one costly regulation—or “hidden” tax—implemented every day of the Obama administration. This has added about $740 billion and 194 million paperwork hours to the burden. Although designed with good intentions, these regulations, and the compliance costs associated with them, often stand in the way of efficiency.

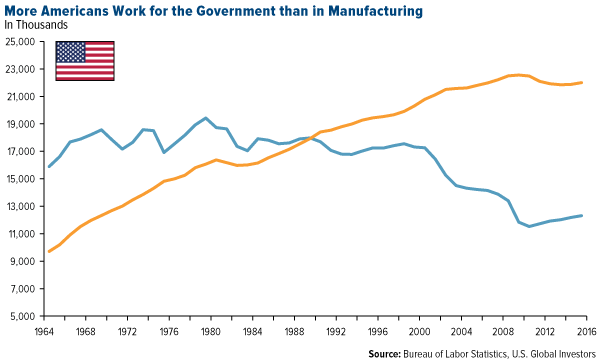

Also increasing are the number of government jobs, which aren’t exactly known to drive innovation. Although we’ve seen an uptick in new manufacturing positions during the last decade, jobs have over the long-run been on the decline.

To get productivity back on track, and therefore consumer spending, the U.S. should strongly consider regulation reform.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 0.04 percent. The S&P 500 Stock Index rose 0.38 percent, while the Nasdaq Composite climbed 0.83 percent. The Russell 2000 small capitalization index gained 0.47 percent this week.

- The Hang Seng Composite gained 0.93 percent this week; while Taiwan was up 1.54 percent and the KOSPI rose 0.51 percent.

- The 10-year Treasury bond yield rose 6 basis points to 1.74 percent.

Domestic Equity Market

Strengths

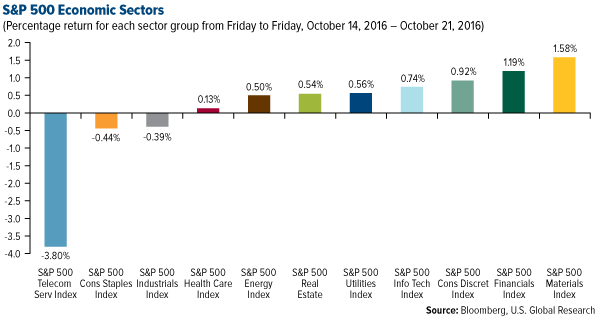

- Materials was the best performing sector for the week, increasing by 1.58 percent versus an overall increase of 0.41 percent for the S&P 500.

- Netflix was the best performing stock for the week, increasing 25.65 percent. The company raced past forecasts for subscriber growth in the third quarter.

- Microsoft hit an all-time high after its earnings beat estimates. Better-than-expected earnings and revenue ran shares of Microsoft up by more than 5 percent and to its first record-high print since December 1999.

Weaknesses

- Telecommunications was the worst performing sector for the week, falling by -3.80 percent versus an overall increase of 0.41 percent for the S&P 500.

- Southwestern Energy was the worst performing stock for the week, falling -10.16 percent. The company’s stock dropped on concern for low pricing as it ramps up production.

- Verizon tumbled after adding fewer subscribers than expected. Verizon said net additions for FIOS video totaled 36,000, but analysts estimated a gain of 59,000. At the same time, demand for higher Internet speeds increased, reflecting the shift away from traditional cable-TV bundles and toward more customizable streaming services.

Opportunities

- AT&T and Time Warner are reportedly talking about a merger, according to Ed Hammond, Alex Sherman and Scott Moritz at Bloomberg. The talks are informal, and neither side has hired an adviser, according to the report.

- Qualcomm might finally put its cash to work. The tech giant is said to be in the final stages of talks to acquire NXP for $110 to $120 a share, or about $40 billion, according to Bloomberg. Qualcomm has about $30 billion in cash, most of which is overseas, so acquiring a foreign company is attractive.

- Tesla says cars will have self-driving hardware. The electric-car maker announced on Wednesday that all new cars, including the Model 3, would have the ability to be fully autonomous. "The foundation has been laid for fully autonomous, it's twice as safe as a human, maybe better," CEO Elon Musk said during a media call Wednesday evening.

Threats

- eBay shares slid 10 percent in early trading on Thursday after the company announced weak guidance for the fourth quarter. The ecommerce company said it expects adjusted earnings per share from continuing operations to be in a range of $0.52 to $0.54 for the crucial holiday season. That was near the low end of analysts' forecast for $0.54, according to Bloomberg.

- Wells Fargo is being investigated on suspicion of identity theft. California prosecutors are looking into whether the bank’s creation of millions of fraudulent accounts constitutes identity theft, Bloomberg reports.

- American Express posted its lowest quarterly revenue in over five years. The credit-card giant earned $1.20 a share on revenue of $7.77 billion, which was its lowest in over five years as a result of losing its Costco contract.

The Economy and Bond Market

Strengths

- A major fallout from the housing crash is now at the lowest level since 2008. Distressed sales — foreclosures and short sales — as a percent of residential sales fell to 4 percent in September. Distressed and short sales made up about one-third to one-half of all sales in 2012.

- China's GDP was in line. The Chinese economy grew at a 6.7 percent year-over-year clip in the third quarter, causing some economists to suggest it's a sign the Chinese economy is stabilizing as this is the third straight quarter with 6.7 percent year-over-year growth.

- Britain's jobs report looked good. Data from the Office for National Statistics showed Britain's unemployment rate held at 4.9% while those claiming benefits for the first time rose by just 700 from August to September, well shy of the 3,000 claimants that economists were expecting.

Weaknesses

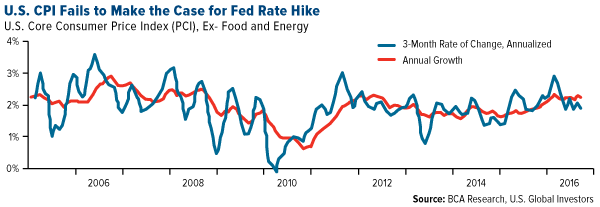

- The below-expected 0.1 percent month-over-month rise in U.S. core CPI failed to cement the case for a Federal Reserve rate hike in December. The annual growth rate moderated slightly to 2.2 percent from 2.3 percent, while the three-month annualized rate slowed to 1.8 percent from 2.1 percent.

- Housing starts unexpectedly plunged by 9 percent at a seasonally adjusted annual rate of 1.05 million. Starts of multi-family structures with five or more units fell 39 percent, and were the biggest drag on overall construction.

- Empire manufacturing unexpectedly collapsed to -6.8. That number is below economists' expectations of an increase to 1.00, and a drop from the prior month's reading of -2.0.

Opportunities

- Next Friday's U.S. third quarter GDP will take center stage. Economists are expecting 2.5 percent growth versus the prior quarter’s 1.4 percent. A firm rebound in the third quarter is needed to dismiss the recent weakness as a temporary soft patch.

- According to James Iselin, the managing director at Neuberger Berman, the ratio of 10-year municipal yields to Treasury yields may be on the way to surpassing 100 percent again. That would increase the attractiveness of munis of treasuries and would likely bring buyers into the market.

- After a strong two years, the U.S. dollar has remained more or less flat during the last few months, with the trade-weighted dollar index hovering near a range of 93 to 98. But now, some analysts are arguing that the greenback could have some room to grow. According to a Morgan Stanley team led by Hans W. Redeker in a recent note, the foundation for a powerful U.S. dollar rally is in place as the outlook is stronger than it was last year.

Threats

- Medical costs are rising faster than pretty much everything else right now. The Bureau of Labor Statistics released the latest data for the Consumer Price Index measure of inflation, which rose by 0.3 percent month-on-month and 1.5 percent year-on-year in September. On the month-over-month scale, headline CPI was boosted most by medical costs.

- S&P cut the debt of Europe’s biggest potash producer one step to a level below investment grade. The downgrade means that the bonds have no investment-grade ratings that would make it eligible for the European Central Bank’s asset-purchase program. Before the buying began, the ECB said it wouldn’t have to automatically sell notes downgraded to junk, but it has also said it will take steps to manage risks in its holdings. The central bank has bought 34 billion euros ($37 billion) of investment-grade corporate bonds since starting its stimulus program in June.

- Almost everyone the Federal Reserve questioned for its Beige Book had terrible things to say about Houston's economy, especially its construction and labor markets.

Gold Market

This week spot gold closed at $1,266.28, up $14.85 per ounce, or 1.19 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week slightly higher by 6.99 percent. Junior miners underperformed seniors for the week, as the S&P/TSX Venture Index climbed only 2.27 percent. The U.S. Trade-Weighted Dollar Index finished the week up 0.69 percent.

|

Date |

Event |

Survey |

Actual |

Prior |

| Oct-17 |

Eurozone CPI Core YoY |

0.8% | 0.8% | 0.8% |

| Oct-18 |

U.S. CPI YoY |

1.5% | 1.5% | 1.1% |

| Oct-18 |

China Retail Sales YoY |

10.7% | 10.7% | 10.6% |

| Oct-19 |

U.S. Housing Starts |

1175k | 1047k | 1150k |

| Oct-20 |

ECB Main Refinancing Rate |

0.000% | 0.000% | 0.000% |

| Oct-20 |

U.S. Initial Jobless Claims |

250k | 260k | 247k |

| Oct-25 |

U.S. Consumer Confidence Index |

101.0 | -- | 107.1 |

| Oct-26 |

U.S. New Home Sales |

600k | -- | 609k |

| Oct-27 |

Hong Kong Exports YoY |

-0.1% | -- | 0.8% |

| Oct-27 |

U.S. Durable Goods Orders |

0.1% | -- | 0.1% |

| Oct-27 |

U.S. Initial Jobless Claims |

255k | -- | 260k |

| Oct-28 |

Germany CPI YoY |

0.8% | -- | 0.7% |

| Oct-28 |

U.S. GDP Annualized QoQ |

2.5% | -- | 1.4% |

Strengths

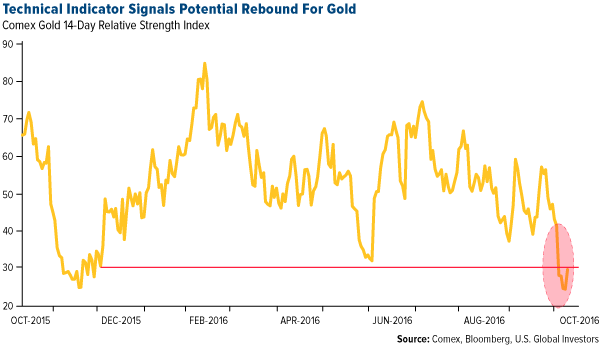

- The best performing precious metal for the week was gold. Gold was hammered down while Chinese markets were closed in the prior week, triggering a technical buy signal and possibly the best entry point in over year to add to positions.

- After gold price discounts hit a record high of $100 an ounce in July, prices in India swung to a premium for the first time in nine months this week, reports Reuters, around $2 an ounce. The Business Standard also reported this week that the sixth tranche of the sovereign gold bond scheme in India is set to launch on October 24, with bonds being offered at a discount to attract more customers.

- It seems the relatively new Shanghai Gold Exchange (SGE) gold price benchmark has been leading the way in terms of setting the direction of the global gold price level, writes Lawrie Williams, following the recent $60 price drop of the metal during China’s Golden Week. Williams’ colleague Julian Phillips adds that the Shanghai physical market for gold is thought to better represent physical gold prices than COMEX paper market prices. In fact, the Dubai gold exchange has signed a contract to use the Shanghai Fixings in place of the London Fixings. In a related note from S&P Global this week, China’s central bank added 5 metric tons to its gold reserves in September, making total gold holdings now at 1,838 tons.

Weaknesses

- The worst performing precious metal for the week was palladium, falling 3.66 percent. Extending a selloff sparked by weak trade data from China, palladium fell to a three-month low, reports Bloomberg. Palladium prices have fallen nearly $100 over the last three weeks.

- Hedge funds are cutting bullish bets on gold at the fastest pace this week, sending the yellow metal near four-month lows, reports Bloomberg. Money managers cut net-long wagers by 25 percent, according to U.S. Commodity Futures Trading Commission data released last week. In the past two reports, the article continues, the position has fallen by around 180,000 contracts. This drop could potentially be setting up a rebound for the metal. Similarly, the increased odds of a December rate hike are sending gold mining shares downward, following the biggest rally in a decade.

- According to Bloomberg, China said its consumption of non-ferrous metals will expand through the year 2020 at less than half the pace seen in the first five years of the decade. The Ministry of Industry and Information Technology said the nation’s economy is “entering a new normal” in which demand growth for metals will slow to a medium-low pace from a high-speed one.

Opportunities

- James Steel, respected chief precious metals analyst with HSBC, has written a note indicating that higher gold prices are likely to come out of the global trade slowdown, writes Zero Hedge. “Demand for gold is often stimulated by the same factors that fan protectionist and populist sentiment,” Steel said. “Abrupt declines in cross border trade, investment and immigration, the dislocation of global economic policies, and a beggar-thy-neighbor approach to trade, is almost tailor-made for higher gold prices.”

- A survey of attendees at this year’s London Bullion Market Association in Singapore show that gold is set to rise around 7 percent by the time of the 2017 conference. General manager at Heraeus Metals in Hong Kong, Dick Poon, says gold can surge to $1,400 in 2017 as the Fed holds back from further monetary tightening in at least the first half after an increase in December, reports Bloomberg. Portfolio manager Terence Kooyker at Blenheim says he is bullish on gold too, and bearish on oil. Kooyker says faster U.S. inflation and low interest rates will support gold, adding that “gold always performs best when nobody thinks you should own it.”

- In a note this week, Macquarie Research initiated coverage of Rye Patch Gold with an outperform recommendation. The group writes that Rye Patch is transforming from an explorer royalty company to a junior producer on the back of its July 2016 acquisition of the Florida Canyon mine (FCM) in Nevada. Macquarie sees FCM offering investors a key opportunity for high returns, given that the stock is trading around 70 percent discount to junior producer peers.

Threats

- Earlier this year, it was reported that California’s Public Employees’ Retirement System (Calpers), the largest in the U.S., earned only 0.6 percent on its investments last fiscal year, reports Financial Sense. In order to meet its long-term goal, however, the pension needs to be returning over 12 times that amount. Calpers’ Chief Investment Officer Ted Eliopoulus writes that it is a significant policy issue and the system must average at least 7.5 percent a year to match its assumed rate of return or turn to taxpayers to make up the difference.

- To add to the point above, author of California Dreaming: Lessons on How to Resolve America’s Public Pension Crisis, Lawrence McQuillan writes that the total unfunded liability in California alone is $950 billion all-in when looking at state and local pension plans. Again, that is just California. This is a huge “ticking time bomb,” he continues, noting that if you look nationally and use realistic numbers, it’s around $4 trillion when looking at all state and local government pension plans across the country. Investors should always think in terms of portfolio diversification as pension funds may not hold any gold exposure.

- The world’s biggest central banks are bulking up their balance sheets, reports Bloomberg. The combined assets of the 10 largest central banks now total $21.4 trillion, a 10-percent increase from the end of last year. “The accelerating expansion of central banks’ balance sheets comes as debate rages over whether their asset purchases and continued low interest rates are creating bubbles, especially in the bond market,” the article continues. Almost 75 percent of the world’s central bank assets are controlled by just four policymakers in China, the U.S., Japan and the eurozone.

Energy and Natural Resources Market

Strengths

- Crude oil prices rose to a 15-month high as inventories in the U.S. decline and many members of OPEC are further reducing output. This week’s inventory draw marks the tenth weekly inventory drawdown in the last 11 weeks.

- The best performing sector for the week was the BI Global Coal Producers Index. The index rose 17 percent for the week as coal prices rallied on the back of recent heavy rainfalls in Australia that threaten to disrupt supply from the world’s largest coking coal exporter.

- CF Industries Holdings Inc., a major global fertilizing company, was the best performing stock in the broader natural resource space for the week. The stock gained 16.3 percent after a proxy advisory firm recommended investors vote in favor of the proposed Agrium/Potash Corp deal. The deal will help consolidate the fertilizer sector, which investors believe could result in greater pricing power and profitability.

Weaknesses

- U.S. housing starts missed by 9 percent for the month of September. Prospective home buyers cited problems finding affordable properties. The weaker monthly reading suggests weakness in construction materials, as well as the paper and forest sector.

- The worst performing sector for the week was the S&P 500 Paper and Forest Products Index. The index dropped 2.7 percent for the week, tracking lumber prices down, and reacting to the negative housing starts September print.

- The worst performing stock for the week in the broader natural resource space was Kaiser Aluminum. The manufacturer of aerospace products dropped 10.1 percent to a 52-week low after a disappointing third quarter earnings’ call. The company downgraded its profit guidance as it expects weaker aerospace deliveries.

Opportunities

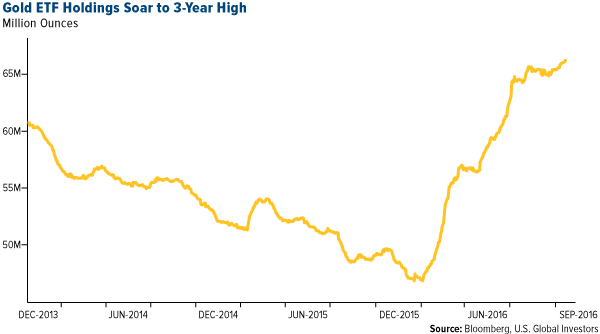

- Gold ETF holdings surged to a three year-high. Money managers and speculators have cut net-long positions in gold futures by record amounts over the past two weeks hurting the price of the commodity; however, physical gold investors have continued to accumulate gold as ETF holdings climb to three year-highs, signaling a potential bullish move forward for gold.

- Halliburton, one of the largest global oil service companies, reported earnings ahead of street expectations. The data suggests North American activity has stabilized, a positive signal for other oil services companies and the energy sector as a whole.

- “The oil price will go higher with or without OPEC,” according to Oppenheimer’s Fadel Gheit. Despite attention being centered on talks of production cuts among OPEC members, Gheit believes that much of it is irrelevant as the lack of capital spending over the past years will force a rebalancing of the market and lift oil prices.

Threats

- The outlook for industrial and base metals in the fourth quarter of 2016 is looking weak according to a Bank of America survey of market participants. With commodity prices having rallied in 2016, and the fourth quarter being the weakest seasonal quarter, prices may well weaken into year-end. Participants did add that they expect prices to strengthen by early 2017.

- The spectacular rally in coking coal prices will end in tears according to CLSA. Coking coal prices have rallied 200 percent year-to-date, with a substantial run in the last two months. As CLSA argues, a recent change in China’s policy will bring more supply online in the coming month which poses a threat to this price level. CLSA believes there is potential for further momentum in the short-term but forecast a correction by the first quarter of 2017.

- Ford delivered a blow to the auto parts industry, with negative read-through for steel and aluminum demand. Ford is suspending production in select plants to help clear excess inventories and resize to meet current demand.

China Region

Strengths

- Both Aggregate and New Yuan Loan Financing data came in higher than analysts’ expectations. New yuan loans came in at 1.22 trillion for the September period, ahead of 1 trillion and up from 948.7 billion in August, while Aggregate Financing came in at 1.720 trillion, up from 1.470 trillion and ahead of expectations for 1.390 trillion.

- China’s third quarter GDP was in-line with analysts’ expectations for a year-over-year third quarter GDP print at a 6.7 percent growth rate, which remains right within the overall 2016 guidance from the Chinese government for a range of 6.5-7.0 percent GDP growth.

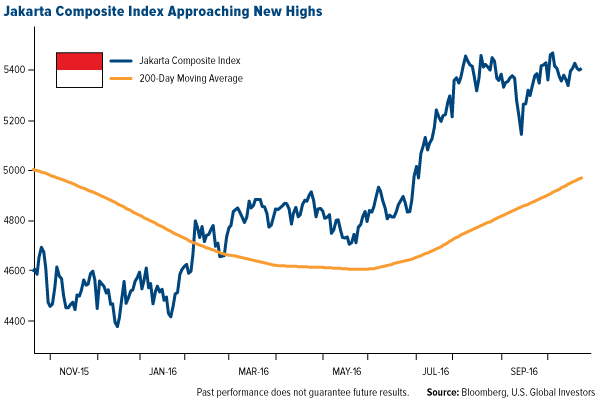

- The Jakarta Composite Index remains within close striking distance of its recent highs as the index continues to consolidate its gains of recent months. The Bank of Indonesia surprised a majority of analysts this week with an unexpected rate cut as well as hints that additional cuts may be in order in future.

Weaknesses

- The renminbi continues to weaken, hitting six-year lows as the on-shore yuan touched 6.7670, while the offshore yuan fell to 6.7761.

- Year-over-year industrial production in China came in at a gain of 6.1 percent, slightly weaker than expectations for a gain of 6.4 percent and below the previous (August) print of 6.3 percent.

- Indonesian exports and imports both missed for the September period. Analysts’ expectations for exports were a year-over-year gain of 0.60 percent, but the actual print was a decline of 0.59 percent, while expectations for a gain in imports of 4.7 percent were missed by an actual print that showed a decline of 2.26 percent.

Opportunities

- Malaysia’s Prime Minister Najib Razak has pledged to control expenditures as the country grapples with a continued period of energy prices lower than in recent years. The Malaysian government is presently estimating a 2017 GDP growth rate of between 4 percent and 5 percent, with a narrowing fiscal shortfall. Malaysia is the region’s only net energy-exporter.

- China is set to overtake the United States and take the title of the world’s largest aviation market by 2024, Bloomberg reports, as the number of people flying may almost double to 927 million by 2025.

- In addition to the expected aim of stemming a potential bubble, one potential upside to the recent property curbs in mainland China has been an uptick in Hong Kong properties and property developers as mainland buyers consider subsidies and incentives to buy in Hong Kong instead.

Threats

- Philippine President Rodrigo Duterte spent the week visiting China after having been invited to Beijing by Chinese President Xi Jinping. While there, Mr. Duterte announced his “separation” from the United States, noting that between his country and China, “the roots of our bonds are very deep,” also suggesting that, “Foreign policy now veers toward” China. Indeed, Mr. Duterte asserted, “No more American interference.” Once again, Philippine cabinet members have downplayed the president’s remarks, but the 71-year-old populist leader appears to be flagging a real pivot toward China, or perhaps simply snubbing the U.S., fishing for a better deal (or perhaps both).

- While home price appreciation did slow somewhat in some of the largest Chinese cities—Beijing and Shanghai new home prices dropped 3.7 and 2.5 percent, respectively, according to Bloomberg news—the average new home price across the 70 cities which are tracked rose the most in more than seven years in September, up 1.8 percent from the August period, fueling continued caution and concerns about the potential of a developing bubble.

- The expectations for a potential U.S. interest rate hike and an accompanying rise in the U.S. dollar could continue to exert collective pressure in certain sectors across Asia.

Emerging Europe

Strengths

- Hungary was the best-performing country this week, gaining 4.2 percent. The Budapest stock exchange appreciated 23.6 percent year-to-date, the strongest performer in emerging Europe, supported by government pro-growth actions. This week, Hungarian government announced it will payroll taxes early next year.

- The Russian ruble was the best-performing currency this week, gaining 94 basis points against the dollar. Major emerging Europe currencies lost against the dollar, but the ruble was supported by Russian companies selling dollars this week and buying rubles in preparation to pay 1.1 trillion rubles ($17.6 billion) in taxes due before month-end.

- The utility sector was the best-performing sector among eastern European markets this week.

Weaknesses

- Romania was the worst-performing country this week, losing 55 basis points. Banks underperformed this week as Romanian lawmakers approved a bill allowing the conversion of Swiss-franc loans into local currency at below-market rates. The bill also will allow conversions at the historical rates to already converted Swiss-franc loans.

- The Hungarian forint was the worst-performing currency this week, losing 1.65 percent against the dollar. Eurostat published revised debt figures for Hungary, and debt level fell to 74.4 percent of gross domestic product from 75.7 a year earlier. The deficit narrowed to 1.6 percent from 2.1 percent. However, Eurostat is skeptical about the quality of data reported by Hungary and is reviewing Hungarian central bank operations.

- The materials sector was the worst-performing sector among eastern European markets this week.

Opportunities

- JPMorgan Chase raised its recommendation to overweight Russian stocks because prices don’t reflect recovery in oil prices, saying that the energy sector stocks are pricing in $45 per barrel oil, not $50 per barrel where crude trades. Russian shares on the MICEX Index are trading at 6.2 times estimated 12 month earnings, the lowest level among emerging markets.

- The yield on Czech Republic’s two-year government notes fell to a record low of -1.05 percent, below Switzerland’s two-year yield. Demand for Czech bonds is driven by the country’s growing economy and investors’ expectation that the koruna will appreciate after the cap on the currency is lifted.

- Rosneft, Russia’s largest oil producer, announced buying India’s second biggest refinery Essar Oil Ltd. This acquisition will boost Russia’s access to the most important long-term growth market. Rosneft is targeting a market of 1.3 billion people that imports more than 80 percent of its crude requirements. The International Energy Agency forecast that India will be the world’s fastest-growing oil-consuming nation through 2040. Rosneft also sees the potential to expand in the Asia-Pacific region by supplying fuel to Indonesia, Vietnam, the Philippines and Australia.

Threats

- Ojer Telekom, the parent of Turk Telekom AS, missed September’s $290 million payment on a record $4.75 billion loan. The company received this loan three years ago and since then the lira has lost about 40 percent against the dollar, making it harder to service foreign debt. If the lira depreciates more against the dollar, Turkey’s heavy borrowers may find it difficult to service foreign exchange debt.

- The European Central Bank (ECB) kept its quantitative easing program and interest rates unchanged, providing no support to revive the eurozone economy. Draghi has expressed confidence inflation will return to the ECB’s goal of just below 2 percent by early 2019 at the latest. ECB may have to redesign the QE program to ensure the EUR80 billion monthly bond-buying program can continue, after concerns that eligible assets might be running low.

- The European Union is considering imposing more sanction on Russia due to its action in Syria, where numerous reports have tied Moscow to war crimes in its efforts to reinforce Syrian President Bashar al-Assad’s regime. Talks over new sanctions split Europe as not all members of the eurozone want to move forward with it.

© US Global Investors

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All