You’ve got to know when to hold ‘em

Know when to fold ‘em,

Know when to walk away,

And know when to run.

CCR Wealth Management’s Outlook communication seeks to update our clients on market conditions currently affecting or which may affect asset values and investment performance. Our commentary often responds to a prevailing market “narrative” that is bandied-about in the news and various media channels and is therefore often on the minds of our clients. As our regular readers know, we stay generally light on market “data”, blow-by-blow recaps of recent quarterly index interest rate or currency movements-except where it has become part of the “narrative”. Today these items are all easily obtained with a few clicks on the internet. They usually have limited utility in forming or in-forming a relevant longer-term investment strategy.

We do, however, try to provide our clients with “food for thought” in our commentary about market conditions or investment narratives which intersect with recent or expected returns, volatility, or other newsworthy investment topics. For two years we have been recommending our clients adjust their expectations to choppy markets and lower average returns. We have also discussed the various ingredients at play which produces such results. In doing so, on occasion we have also made reference to Behavioral Finance topics which best encompass or describe some of the cognitive or emotional tendencies investors exhibit when investing in more volatile markets. In the last year we have touched on “Recency Bias”, and the “Gambler’s Fallacy”, for example.

Behavioral Finance is a broad field, but much of it is concerned with recognizing cognitive and emotional biases which prevent investors from making optimal investment decisions. The study of Behavioral Finance provides a framework to recognize the commonality of such tendencies across all investors and hopefully, with such awareness, to improve our investment approaches. We hasten to point out that investment professionals (from pension managers to analysts to traders and financial advisors) are also subject to behavioral biases which may cloud decision-making, and which requires awareness. Behavioral biases are, simply put, a by-product of human nature.

We daresay the quote atop this page will be familiar to the majority of our clients as the lyrics of the “The Gambler”, a song made famous by Kenny Rodgers in 1978. In volatile markets, it is not unusual to witness “long-term investors” suddenly view the capital markets as a casino, with the odds stacked against them to boot. We have often thought of these lyrics when reflecting on the actions of some clients (both past and present) and the propensity of many investors to subconsciously substitute their long-term investment strategy for retirement with a highly emotional, headline-driven, “lightly informed” strategy akin to taking their chips off the table at a gambling casino. Decisions based on “hunches”, “gut feelings”, or last night’s ‘Mad Money’ with Jim Cramer episode subvert more rational evaluations. Unfortunately, many investors consider “walking away” or even “running” viable components of a long-term investment strategy. They are not. They never have been. All evidence backs this up.

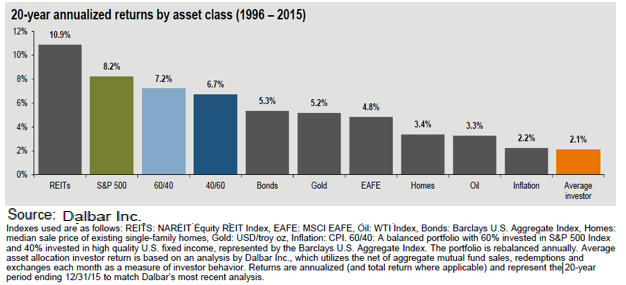

The Dalbar Quantitative Analysis of Investor Behavior is an annual in-depth study of individual investor behavioral patterns, gathered through examining vast amounts of mutual fund trading data. The 2015 edition is the 22nd iteration of the analysis. According to the study, the rolling track-record of investors is consistent and telling. Over 20 years, investors don’t even keep pace with inflation. Among the report’s findings; Psychological factors (behavioral biases) were the number 1 reason, accounting for over 50% of investors’ shortfall versus a relevant benchmark. In a nutshell, it is human nature to sell low and buy high. High commissions and fees was the number two reason, at about a 25% attribution, followed by a lack of capital (to remain fully invested). In other words: Presidential politics, geopolitical uncertainty, and market volatility cause investors to repeatedly head for the exits.

We recently attended a Wealth Management summit in New York. A quote from one of the presenters, Andrew Goldberg of JP Morgan is particularly appropriate:

“Your portfolio is like a bar of soap.

The more you touch it, the smaller it gets!”

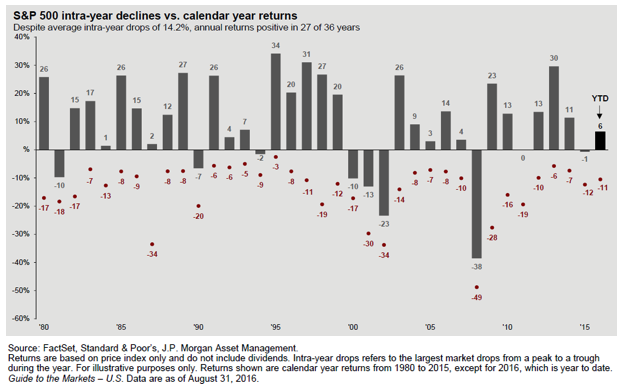

Volatility is the norm in equity markets—not the exception. Regular readers will recognize the following chart, which has been updated to reflect 35 ½ years of market returns and mid-year corrections through June 30th of this year:

When you think about it, 35 years arguably encompasses the majority of an individual’s investment horizon. Considering the chart above, if you have a tendency to “sell” at the red dots, it becomes fairly clear how you end up with the average investor’s 20-year performance of 2.1%, as Dalbar’s research shows.

We recently read a blog written by Massimiliano Saccone, CFA, titled “Asset Managers are from Mars, Investors and from Venus”. In it, Saccone observes:

“Asset managers mistakenly expect investors to think, communicate and react the way asset managers do; investors mistakenly expect asset managers to feel, communicate and respond the way investors do.”

One of the noteworthy things about this statement, aside from the general truism of the idea, is the replacement of the words “think” with “feel” in the comparison between asset managers and investors. This gets to the heart of Behavioral Finance. As with gamblers, “feelings” (hunches, gut feelings, moods) often drive investment decisions of individuals, whereas asset managers are consigned to the colder, harder facts of discounted cash flow models, corporate finance and intrinsic valuation. As Financial Advisors, our role is frequently to be an intermediary between the two.

Our next two Outlooks will consider some Behavioral Finance topics in more depth, beginning this month with a broad overview of what separates Behavioral Finance from Traditional Finance, and what some of the ramifications may be to individual investors. We are not armchair psychologists, of course. Nor do we seek to “cure” clients of human nature! Our coverage of the topic is premised on the fact that awareness of behavioral finance issues and traits may improve our investment approach, strategy, and hopefully our investment outcomes.

To put this into context, there are investors with an extraordinarily large cash position in retirement plans which came about through selling assets in early 2009. This decision made purely on emotional input in an extreme market environment (we know this from firsthand experience). Some of these cash positions still exist, though the S&P 500 is up nearly 300% since the sell-out. In other instances, some investors have made regrettable decisions more recently in each of the two ~10+% market corrections we have experienced in the last twelve months. In both cases, the investments sold were diversified equity and bond mutual funds. The asset managers which run the funds did not sell their holdings. Instead, these instances of market dislocation provided buying opportunities in the cold, hard fact-driven world of asset valuation—and the asset manager’s investment results certainly bear that out. Unfortunately, the investors who sold the funds have performance records of the average investor who buys high and sells low. Behavioral Finance shows us that this tends to be an ingrained, life-long characteristic for many. It is the antithesis of most sound investment strategies.

We have also witnessed the inverse; an ill-advised (from the standpoint of Traditional Finance) effort to boost performance though excessive concentration in single securities. Behavioral Finance studies have also shown that individuals tend to overweight upside potential in such circumstances. Both these behaviors, practiced often enough, end in sub-optimal results as it relates to their stated investment objectives. At worst, they can end in disaster.

Traditional Finance studies how investors should act, assuming all investors have access to the same information, and assuming all investors act rationally, and in their own interests. Behavioral Finance studies how investors actually do act, and attempts to understand why.

Traditional Finance is based on the logical assumption that investors are Risk Averse and will make optimal decisions to maximize return while minimizing risk. In other words, investors will choose an investment for a desired rate of return which has the least amount of risk associated with it from among all investment opportunities expected to provide the same return. These optimal decisions actually require significant cognitive costs, calculations, and research. Reality is quite different. Individuals rarely accommodate such logical and calculated optimization on a consistent basis over time. Human Nature is quite apart from quantitative analysis.

The study of Behavioral Finance includes a number of theoretical assumptions derived from investor behavior studies. One such theorem is Prospect Theory, an axiom of which holds that investors are actually Loss Averse, as opposed to being risk averse (as in Traditional Finance).

Thinking in terms of Loss (an outcome) rather than Risk (a degree of fluctuation) leads to an emotional bias in Behavioral Finance known a “Loss Aversion”. Without the context of the differences between loss and risk made above, it would seem logical that we all should be “loss averse” as investors. However, this behavioral bias is one of mentally applying the definition of a loss (a terminal condition) to any asset that has fluctuated downward in price (a temporary condition). Furthermore, Loss-Averse investors tend to place a higher value on a temporarily negative fluctuation than they do on a positive fluctuation of the same amount. Loss Aversion can have different consequences, but the root is the same illogical thought process as when viewing a portfolio in a volatile market. Commonly, Loss Aversion can trigger a portfolio liquidation to “stop the bloodletting” of a market experiencing downside volatility. This of course, locks in losses (buying high, selling low). Loss aversion can also lead to a number of other particularly non-optimal investment behaviors when looked at from an individual securities basis (versus at the portfolio level):

- Selling “winners” and holding onto losers (again, mentally “gains” and “losses” are not valued equally). Investors wish to avoid “taking a loss” for emotional reasons so they do not sell something that has declined (even though the investment fundamentals have deteriorated). Holding deteriorating securities and selling appreciating securities also negatively impacts the risk characteristic of the portfolio.

- Evaluating gains and losses based on a reference point (i.e. the investor’s cost basis or what price the investment is worth today compared to last month), rather than the true intrinsic value of the underlying company, which should be the focus.

Consequences of Loss Aversion include holding positions at a loss longer than is justified, selling gainers earlier than is justified, excessive trading, holding riskier positions, or even treating money made on a trade differently than other funds. Ultimately, these are behaviors that will produce a life-long tendency to “buy high”, and “sell low”. They are brought about by attaching personal, emotional signals to various components within their investment portfolios or their portfolios as a whole, viewing investments in a binary “gain/loss” context, and ultimately failing to consider updated, fundamental reasons for which they made the investment in the first place.

In summary, as investors, we can all benefit from understanding the difference between risk (something we have control over) and loss (a terminal condition). The first step in applying a more objective approach to our investment strategies is not to conflate the two. Objectivity rather than emotion will be the foundation for improved investment results over time.

In our next Outlook, we will discuss a handful of common, specific behavioral biases, both cognitive and emotional. Many of us may even recognize these tendencies in ourselves.

Market Outlook

It has been said that this is “the most unloved bull market” in history. Pessimism drips through the media, as it did in the earliest months of this year when a bevy of financial shows on CNBC and CNN were posing the question: “Is the US already in recession?” The absurdity of this question aside (recession is something only known from ex-post economic data)—plenty of talking heads were willing to entertain the question, with many affirming “yes” or “soon to be”.

We will give six reasons you, as astute and objective investors should continue to discount this talk. Consider this: as we write in the waning days of September, the S&P 500 is up over 6%, unemployment is under 5%, you can get a mortgage for less than 4%, gasoline is under $3, inflation is less than 2%, and there’s been only 1 recession in the last fourteen years. CCR Wealth Management discounted recession talk in the first quarter of this year when it was rampant—despite concerns about the December rate hike and the Chinese “melt-down”. Our view has not changed.

We believe the bull market in equities will continue—though, as a broken record, so will the volatility we have experienced in the last 18 months. Recently released US GDP figures for the second quarter were revised up to 1.40% from 1.10%, supported by strong consumer spending and healthy exports. A meaningful pick-up in the inventory cycle and an increase in business spending could possibly see third quarter GDP come in close to twice this level. Some recession! We continue to see a positive backdrop for equity investing, though with continued periodic drawdowns like those we experienced a year ago, and in the first quarter. Stay invested!

We acknowledge it is possible the upcoming Presidential election may contribute to volatility—but we must also acknowledge that it may not. Most polls suggest a continuation of a divided government, and 4 weeks out from the actual election, the market seems to assume a status-quo election result (divided government). There is no objective reason to expect a change in GDP direction or stock market trends based on the outcome of the vote. We have covered this ground before—so we will leave the statement at that.

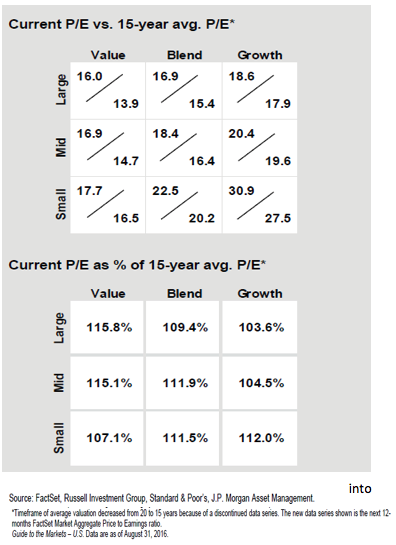

Valuations (price multiples of stocks) has been a topic of concern for some market watchers for the last couple of years. While our view has been that stocks, while not particularly expensive, have not been cheap, we are definitely seeing pockets in the market that can now be described as historically expensive. We do not apply this view to the market as a whole. So-called “value stocks” which tend to share high-dividend/low P/E ratio valuation and lower volatility characteristics now appear quite richly valued. As the chart to the right depicts, some areas of the “value” style are trading 115%-116% of their historical averages. Digging further into into the data, there are sectors like utilities, consumer staples, some industrials, and even energy which look quite rich. We will be reducing our exposure to investments focused on some of these areas of the market—many of which we purchased for dividend yield several years ago. Much of this growth in valuation has occurred in just the last 15 months, as investors have sought high dividend income since higher interest rates have remained out of sight. But current valuations are difficult to justify.

Non-US stocks have actually performed well since the initial sell-off following the Brexit vote, with the MSCI EAFE index outperforming the S&P 500 by approximately 4.0% since the June 27 bottom. We have used this performance boost to reduce our exposure to non-US equities, as outlined in our July Outlook. We expect the Brexit process to be a long one, with potentially contentious negotiations—which have yet to even begin. Political risks remain, including a December 4th Italian referendum vote on constitutional reforms being put forth by Prime Minister Matteo Renzi who is seeking to streamline the famously dysfunctional Italian legislative process. A “yes” vote could pave the way for genuinely pro-growth legislation (a rarity in Europe). However, a “no” vote could lead to Renzi’s resignation and a sizeable anti-EU bloc could vie for power in Italy. We remain engaged global investors despite our lowered weightings to equities outside the US.

Our fixed income models have not changed, though the bond market continues to confound investors around the globe. Central Banks around the world have spent $13 Trillion in asset purchases in an effort to supposedly kick-start economies. What would happen to the S&P 500 if $13 Trillion was pumped into it? Negative interest rates in Europe and Japan has us scratching our head—who lends money with the certainty of getting less back upon repayment of the loan? The only answer, in a rational world, is one who expects to sell the loan for a capital gain (loans are bonds, and as with all financial assets, are valued as the present value of all discounted future cash flows. If there are no cash flows, what is the value of the bond?). We believe we are witnessing the Greater Fool theory play out before our eyes. But no investor has ever lived through an interest rate phenomenon remotely similar to this, so opinions on how this plays out are varied—to say the least.

In our July Outlook we supposed a rate hike in the US was likely off the table for the year given the market tumult immediately following the Brexit vote. Clearly things have improved since then—both in market conditions abroad and economic data at home. We amend this forecast to suggest a rate hike looks likely after the election, either in November or December.

Interest rates that are worth noting for investors today are the LIBOR benchmarks. Since “Money Market Reform” has been implemented, investors have been forced to choose between traditional credit-backed money markets which will now have a “floating” NAV (and are subject to gates and liquidity restrictions), or choose government-backed markets where the NAV will remain $1 (our clients received notice of this choice this Spring). Already $1 Trillion has moved into short term Treasuries, which has caused a flood of supply in the credit markets (commercial paper, primarily). The result has been an increase of 81% in the one-year LIBOR benchmark and the six-month LIBOR benchmark has more than doubled (up 130%). These developments are worth noting because many home-owners have taken advantage of extraordinarily low interest rates in recent years by using ARMS, or adjustable rate mortgages. These adjustable rates are pegged to LIBOR. For some, higher mortgage payments may soon become a reality.

The views are those of CCR Wealth Management LLC and should not be construed as specific investment advice. Investments in securities do not offer a fixed rate of return. Principal, yield and/or share price will fluctuate with changes in market conditions and, when sold or redeemed, you may receive more or less than originally invested. All information is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. Investors cannot directly invest in indices. Past performance does not guarantee future results. Securities and Advisory Services offered through Cetera Advisors LLC. Registered Broker/Dealer, Member FINRA/SIPC.

Cetera Advisors LLC and CCR Wealth Management LLC are not affiliated companies.

© CCR Wealth Management LLC