With all of the talk of the Federal Reserve taking action and raising rates in the next couple months, investors naturally are considering how they position their portfolios. Duration is one metric fixed income investors often pay attention to as they assess a potential interest rate impact. Duration is a measure of interest rate sensitivity (the percentage change in the price of a bond for a 100 basis point move in rates), so the lower the duration the theoretically less sensitive that bond/portfolio is to interest rate movements.

By the nature of the shorter maturities and higher yields, the high yield bond market generally has a shorter duration than investment grade and municipal bonds, meaning high yield bonds are less sensitive to interest rate moves. Yet even within the high yield bond market we are seeing some products and vehicles with a lower duration than others. Like most aspects of investing, you don’t want to consider duration in a vacuum, investing only according to what vehicle has the lowest duration. As noted above, duration measures a price change due to a rate move, but the price changed needs to be coupled with the portfolio’s yield to get a better idea of the expected return under various scenarios. Let’s look at some of scenarios to see how this plays out.

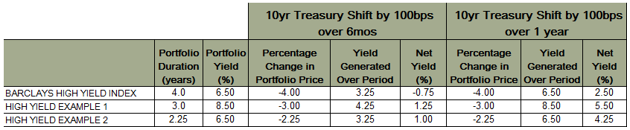

First, let’s hypothetically say you could achieve a portfolio with a duration of 2.25 years, so a 100 bps change in rates over 6mos would mean that the price of your portfolio would theoretically decline by 2.25%. If your starting current yield on the portfolio was 6.5%, meaning you theoretically generate 3.25% of income over that 6mos, then you are looking at a theoretical net gain of 1% (3.25% – 2.25%) over the period of rising rates. However, if you can build a portfolio in the high yield bond and loan market investing according to both maximizing yield and considering duration (keep in mind, loans are floating rate obligations so can serve to lower a portfolio’s duration), let’s say you can build a portfolio with a duration of 3.0 years and a current yield of around 8.5%. In this case, your theoretical sensitivity to a 100bps movement over 6mos would be a price change of 3.0%, but you would be theoretically generating 4.25% of income over the 6mos, so your net theoretical gain would be 1.25%. If that 100bps interest rate movement is over a year instead of 6 months, that yield benefit gets even larger, putting you at a theoretical net gain of 4.25% for the hypothetical short duration portfolio versus a theoretical gain of 5.5% for the higher yielding portfolio.1 And of course, if rates don’t move or even decline from current levels, then the higher yielding portfolio would not only benefit from the higher starting yield but potentially a theoretical positive price movement per the duration calculation.

Below we graphically depict a this and other scenarios that show how duration and yield would theoretically interplay during periods of rising rates for a variety of scenarios.2

We see this as compelling evidence that investing purely according to a short duration strategy and not factoring in yield is not necessarily the wisest way to approach this environment. At the end of the day, yield matters. A higher yield can go a long way in making up for relatively small differences in duration. Thus we believe there are benefits to having the flexibility to build a portfolio that not only maximizes yield but also lowers duration as not only a better way to address interest rate risk, but can also provide less interest rate sensitivity relative to the broader high yield market and other products without this same flexibility. Furthermore, even if rates do rise, it very well can take longer than many expect as we have seen over the last year, making the argument for the higher yielding portfolio versus the purely short duration portfolio even stronger. For more, see our piece “Strategies for a Rising Rate Environment.”

1 The duration and price movement relationships are theoretical approximates and calculations are provided for illustration only. These calculations assume that credit spreads, among other factors, remain constant and do not factor in any fees or expenses or changes in price movements for other reasons, including security fundamentals, etc. Actual results may be materially different.

2 The duration and price movement relationships are theoretical approximates and calculations are provided for illustration only. These calculations assume that credit spreads, among other factors, remain constant and do not factor in any fees or expenses or changes in price movements for other reasons, including security fundamentals, etc. Actual results may be materially different. Barclays High Yield Index as of 10/7/16, with “duration” based on the Macaulay duration to worst and “yield” based on a current yield assumption of average portfolio coupon divided by the average portfolio price.

Although information and analysis contained herein has been obtained from sources Peritus I Asset Management, LLC believes to be reliable, its accuracy and completeness cannot be guaranteed. Information on this website is for informational purposes only. As with all investments, investing in high yield corporate bonds and loans and other fixed income, equity, and fund securities involves various risk and uncertainties, as well as the potential for loss. Past performance is not an indication or guarantee of future results.