As a young Army paratrooper, much of my training was focused on learning to operate under chaotic circumstances. The battlefield is nothing if not chaotic, especially in the pitch black of night, which is how we often trained. Initially, I found this to be highly stressful, as I had only a vague sense of what was going on and what I was supposed to be doing. Fortunately, the 82nd Airborne Division had many “understanding” leaders who were extremely eager to provide some “gentle guidance” to help square away a new soldier. After a bit of this “gentle guidance,” I became increasingly comfortable operating within the chaos – gaining a clearer sense of the battlefield, what my job was, how that job fit into the unit’s broader mission and, very importantly, how to use my equipment (trust me, moving around with night vision goggles is a lot harder than it seems in the movies). With time, I began to view the chaos that is endemic to the battlefield not as a source of stress, but rather as something that, with the right planning, training and tools, can be overcome and turned into an advantage.

Staying calm in volatile markets

Unfortunately, too many investors have the mindset of an inexperienced soldier, viewing the chaos or volatility in emerging markets as a major negative, something to be avoided. From our perspective at Invesco Fixed Income, the exact opposite is true. We view volatility in emerging markets as a potential opportunity relative to developed markets. When there is a high level of market uncertainty – often driven by a combination of economic, political and social instability – the availability of potentially attractive investment opportunities can grow. The 2008 financial crisis is perhaps the broadest example of this concept. When the dust began to settle, prices across a wide range of assets rebounded sharply from their extreme, fear-induced lows. However, successfully investing in such situations requires the ability to determine when market prices are misaligned from the health of a company. This is a central part of our investment process.

Emerging markets have seen extreme price movements in recent years

While global financial crises are rare, scaled-down versions can play out in emerging markets more frequently. In the last two years, we have seen significant dislocations in the major emerging market economies of Russia and Brazil that pushed asset prices to extreme levels. Russian corporate credit spreads, for example, peaked at 1,222 basis points in December 2014 as tensions escalated with Ukraine (Figure 1). While this is well below the financial crisis peak of 1,989 basis points, it still represents almost 900 basis points of spread widening in less than a year.1 To put that move in context, during the financial crisis, US investment grade corporate bond spreads widened by only 580 basis points and, since then, the biggest spread widening in US investment grade has been only 130 basis points.2

The point here is twofold:

- First, once the geopolitical situation between Russia and Ukraine began to stabilize (not improve, but stabilize) and investors began to assess the situation more objectively, it did not take long for bond spreads to more accurately reflect fundamentals.

- Second, as Figure 1 highlights, the volatility of US investment grade corporate bonds is quite muted by comparison, even though the Russian corporate universe comprises relatively high-quality issuers.

While investing in markets like Russia during periods of turmoil is challenging and requires robust analytical skills, the potential returns can be significant. Past performance is never a guarantee of future results, but it is notable that from December 2014’s peak in spreads until the end of August 2016, Russian corporate bonds returned 63%.3

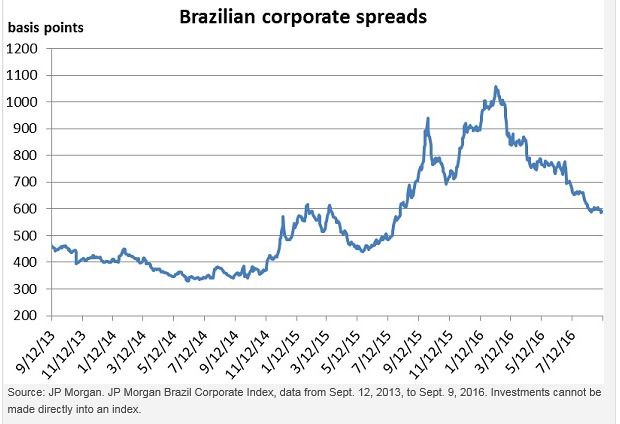

Brazil has faced widespread turmoil since late in 2014, but the spread widening has not been quite as severe as it was in Russia (only around 700 basis points from October 2014 to March 2016), and the spread recovery, so far, is only half as far along (Figure 2). Similar to Russia, as the political and economic turmoil in Brazil began to stabilize and sentiment toward the country began to improve, supported in part by expectations that the sitting president would be removed, asset prices began to more accurately reflect the true risk related to the situation, driving a total return of 31% from the peak spreads reached in February.4

Understanding, but not underestimating, emerging market risks

As these two examples show, there is significant upside potential in such market dislocations. That said, it is important not to understate the risks related to investing in such situations. There is always a high level of uncertainty during these periods, making it difficult to assess the potential depth and duration of the crisis. With Ukraine, for example, contrary to Russia and Brazil, the economic problems that it faced in recent years were much deeper, and the sovereign, as well as almost the entire corporate sector, had to restructure in 2015. While money has been made in the Ukraine, much more has been lost. Investors that were too early in calling an end to the crisis, or picked the wrong corporate bonds, likely face permanent capital losses.

The message here is not that investing in such markets is easy — it is certainly not. Rather, the point is that for skilled and experienced investors, who are able to do the requisite deep fundamental and macro analysis, volatility in emerging markets can provide investment opportunity. In particular, Invesco Fixed Income believes that credit investing may be an ideal way to gain exposure to such markets as the defined cash flows and senior place in the capital structure can help investors mitigate the uncertainty and lengthy time to resolution inherent in such situations. For example, while Russian corporate bonds have returned 22% in US dollar terms since the beginning of 2014 (prior to the annexation of Crimea), Russian equities are down 30% in US dollar terms over that same period.5 Ultimately, while it may prove difficult to net the full upside highlighted in the prior examples, and while past performance is not a guarantee of future results, the opportunity exists to do much better than the average total return bond fund, which has returned about 3% annually over the last five years.6

1 Source: JP Morgan CEMBI Broad Diversified Russia Sub-Index, Jan. 1, 2007, to Aug. 31, 2016.

2 Source: JP Morgan CEMBI Broad Diversified Russia Sub-Index, Barclays US Aggregate Corporate Index, Jan. 1, 2007, to Aug. 2016.

3 Source: JP Morgan Emerging Markets Index, data as of Aug. 31, 2016.

4 Source: JP Morgan CEMBI Broad Diversified Brazil Sub-Index, data from Feb. 11, 2016, to Sept. 9, 2016.

5 Source: JP Morgan CEMBI Broad Diversified Russia Sub-Index, RTSI Equity Index, data from Jan. 6, 2014, to Sept. 19, 2016.

6 Source: Bloomberg L.P., data as of Sept. 12, 2016.

Important information

A basis point is one hundredth of a percentage point.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. Each entity is an indirect, wholly owned subsidiary of Invesco Ltd. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC, investment adviser. Invesco PowerShares Capital Management LLC (Invesco PowerShares) and Invesco Distributors, Inc., ETF distributor, are indirect, wholly owned subsidiaries of Invesco Ltd.

©2016 Invesco Ltd. All rights reserved.

Emerging market bonds: Investing with conviction in volatile markets by Invesco