When equity investors chase what’s hot, it often ends in tears. Today, the safety trades that have been so popular earlier this year are actually looking quite dangerous.

We’ve seen this film before. There are countless examples throughout modern market history of investors following crowds into performance fads and getting crushed on the way down. From the Japanese stock market crisis in 1992 to the technology bubble in 2000 to the US housing crash in 2007, market manias are often seductive.

These days, investors in global stocks are eager to combat volatility and protect against downturns. The quest for a smoother ride has led many to increase allocations to passive portfolios exposed to certain risk characteristics—or factors—which are seen as relatively safe. Less volatile stocks, as characterized by their lower beta, and stocks that offer higher-dividend yield have been especially popular.

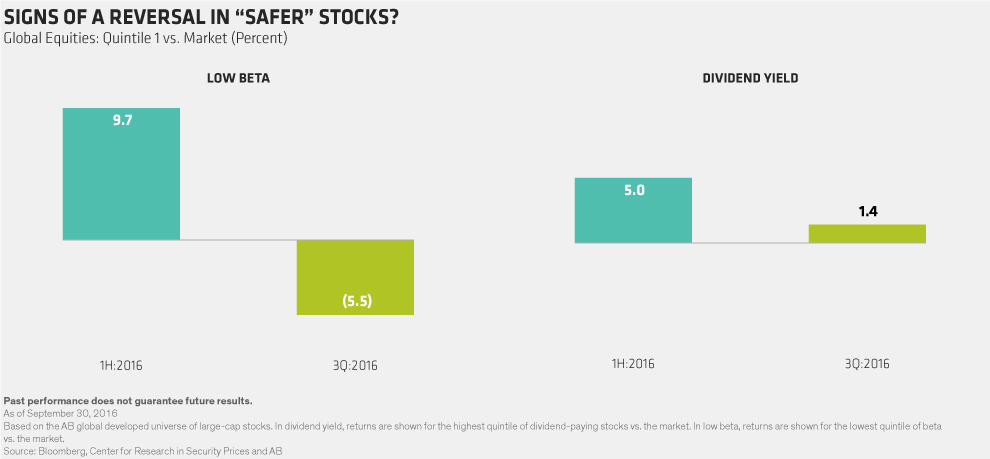

Recent trends may be signaling that a reversal is imminent. For example, low-beta stocks outperformed the market in the first half of 2016, but underperformed in the third quarter (Display). Similarly, returns from the highest group of dividend-payers were especially strong in the first quarter but have lost steam since then.

Exchange-traded funds (ETFs) with factor exposure to low-beta or high-dividend yields don’t always provide protection as expected. When the S&P 500 Index dropped 2.5% on September 9 amid concerns about the Fed’s next moves, the MSCI US low-volatility and high-dividend-yield indices fell by 3.2% and 2.7% respectively. While just a single day, it highlights how passive index-tracking vehicles that are supposed to protect investors from market shocks don’t always get the job done.

DANGEROUS DISTORTIONS

These performance trends are worrying, given the distortions that have been stoked by heightened demand for certain factors. Globally, low-beta stocks have become so popular that their price/book valuations trade at a 28% premium to the broader market (Display, left). Meanwhile, their riskier high-beta counterparts trade at a 37% discount. The valuation gap between safer and riskier stocks persists around the world and is particularly pronounced in Europe (Display, right).

Stocks that pay high dividends are also very expensive. In US markets, high-dividend stocks trade at lofty valuations. And sectors like consumer staples are trading at very high multiples, globally and especially in the US. We’ve seen in the past how crowded trades like these can unwind quickly, wreaking havoc on performance for investors who are overexposed.

RESISTING TEMPTATION

Following factor fads can seem tempting. Passive factor funds that position investors in stocks with low beta or higher dividends are cheaper than active portfolios and they’re simple to understand.

Yet these advantages may mask some serious risks. By piling indiscriminately into all stocks that score high on a certain factor, a portfolio may hold many stocks that have unattractive fundamentals. And factor performance can be volatile, as this year’s patterns show.

So what can investors do to avoid being trapped by the factor of the moment? We believe several approaches can reap the benefits of equity factors or avoid the risks of the latest craze:

ACTIVE STYLE: The performance of some equity factors can be very effective over the long term. And screening for stocks that score high on various style metrics is a good way to discover investment candidates. But instead of blindly buying all stocks that surface in a screen, select holdings from this group through detailed fundamental research on industry dynamics and company-specific strengths. For example, when applied to a value approach, an investor would screen for the most attractively valued stocks and then dig deeper to identify those with the strongest recovery potential. This allows a portfolio to avoid cheap stocks with weaker business and earnings profiles that could become traps.

NEUTRALIZING FACTORS: In a core equity portfolio, we believe that minimizing the influence of factors can lead to better results. Having chosen stocks based on active fundamental principles, the portfolio manager must combine them, and monitor them collectively. This may involve a consistent assessment of how the portfolio may have an unintentional exposure to a particular factor. It also reduces the risk that a portfolio’s returns will get hit when a factor trend reverses. And it frees up the risk budget of a portfolio to concentrate risk where a manager has skill—in stock selection.

FACTOR FUNDS: Timing factors can be rewarding in a portfolio that is capable of dynamically assessing the shifting risk/reward profiles of different factors. These funds aim to capture systemic risk premiums through market cycles, by providing exposure to different sources of factor returns that have low correlations with one another. With an approach like this, an investor might choose today to have an underweight position in stocks offering stability and high-dividend yields.

DEFUSING THREATS

In the search for safety, it’s very tempting for investors to follow crowds. But with stocks that score high on low-beta and high-dividend yield trading at unusually elevated premiums, we think buying blanket exposure based on equity factors that seem safe can actually be very dangerous. Instead, look for managers that know how to make the best of what factors have to offer while avoiding the risks that can make factor fads become a fatal flaw for performance.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams. AllianceBernstein Limited is authorised and regulated by the Financial Conduct Authority in the United Kingdom.