We Believe Congress Is About to Give this Asset Class a Huge Promotion

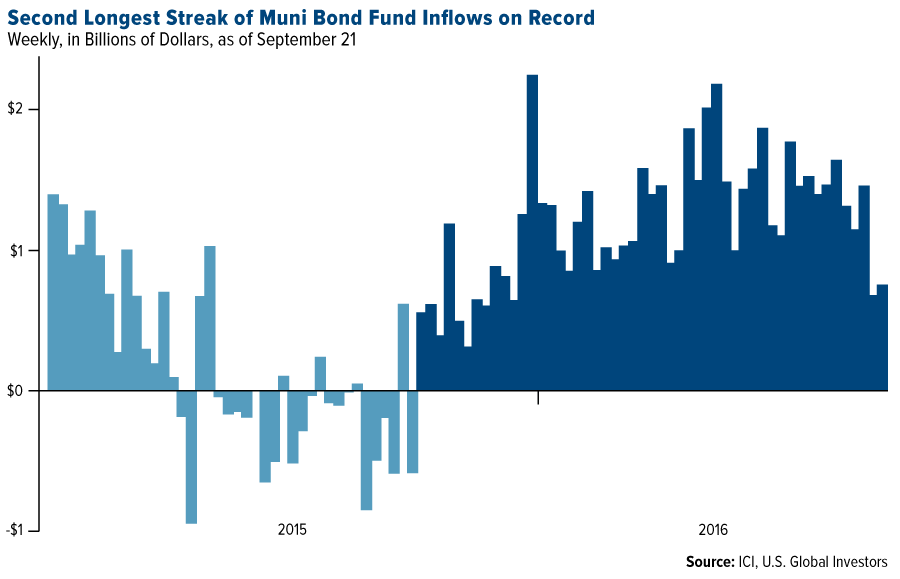

It appears there’s no shortage of investor love for municipal bond funds. September 28 was the 52nd straight week of inflows into state and local government debt, marking the second longest streak on record, according to the Investment Company Institute (ICI). Year-to-date, munis have attracted more than $48 billion in new cash.

Although I can’t say how long this rally will last, the drivers for the $3.7 trillion muni market remain the same now compared to a year ago: stock market volatility; a thirst for tax-free income and capital preservation; and a need for safety in a world beset by perceived threats, from geopolitical uncertainty in the European Union to the upcoming U.S. presidential election, the most divisive and controversial in modern history.

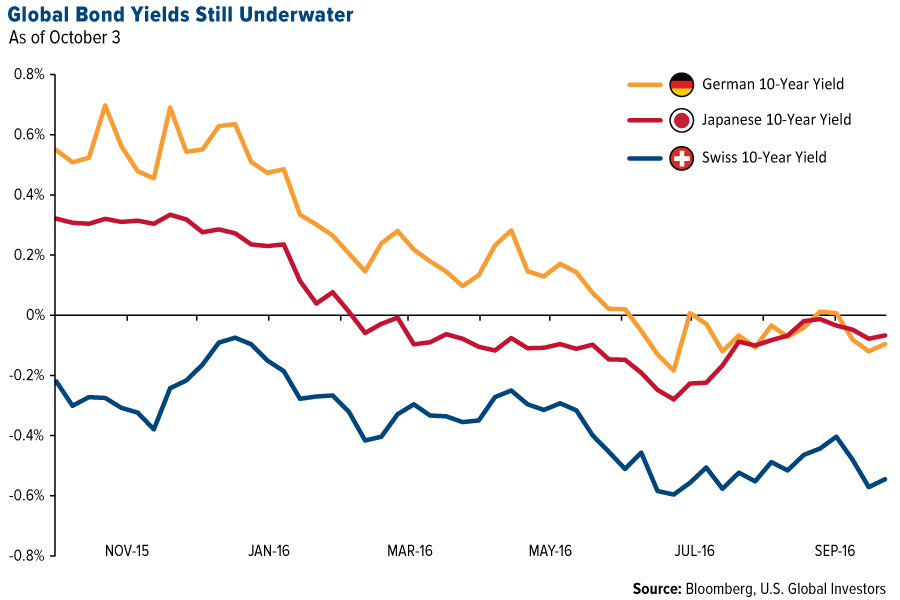

And it isn’t just American investors who favor munis. With government debt still yielding negative rates in Japan, Germany, Switzerland and elsewhere, foreign investors continue to add to their muni holdings, even though they’re ineligible to receive the securities’ U.S. tax benefit.

According to Bloomberg, foreign buyers held close to $90 billion in munis as of June 30, up from $74 billion during the same period in 2013.

Senators: Munis Are “High Quality Liquid Assets”

For these reasons and more, a group of U.S. senators introduced a bipartisan bill last week that would promote munis to the highest quality of assets.

The “high quality liquid assets” category currently includes cash, Treasuries and debt issued by government agencies such as Fannie Mae and Freddie Mac. The new bill, if passed and turned into law, would elevate municipal debt to this easiest-to-trade group.

This would give banks more reserve options, as they’re required by law to hold enough highly liquid assets to last them at least 30 days in the event of an economic crisis.

A similar bill has already passed the House. The Senate bill is sponsored by Mike Rounds (R., S.D.), Charles Schumer (D., N.Y.) and Mark Warner (D., Va.).

A Ringing Endorsement

I agree with the senators’ position on munis’ liquidity and comparative stability. In fact, it’s a wonder why this hasn’t happened before now. Moving munis into the “high liquidity” category would serve as sterling confirmation of what so many investors, from individuals to mutual funds to banks, already know about them.

It’s unclear at the moment when the Senate bill might be put to a vote, but I’m hoping for a victory and that the president will sign it. When new details surface, I’ll let you know.