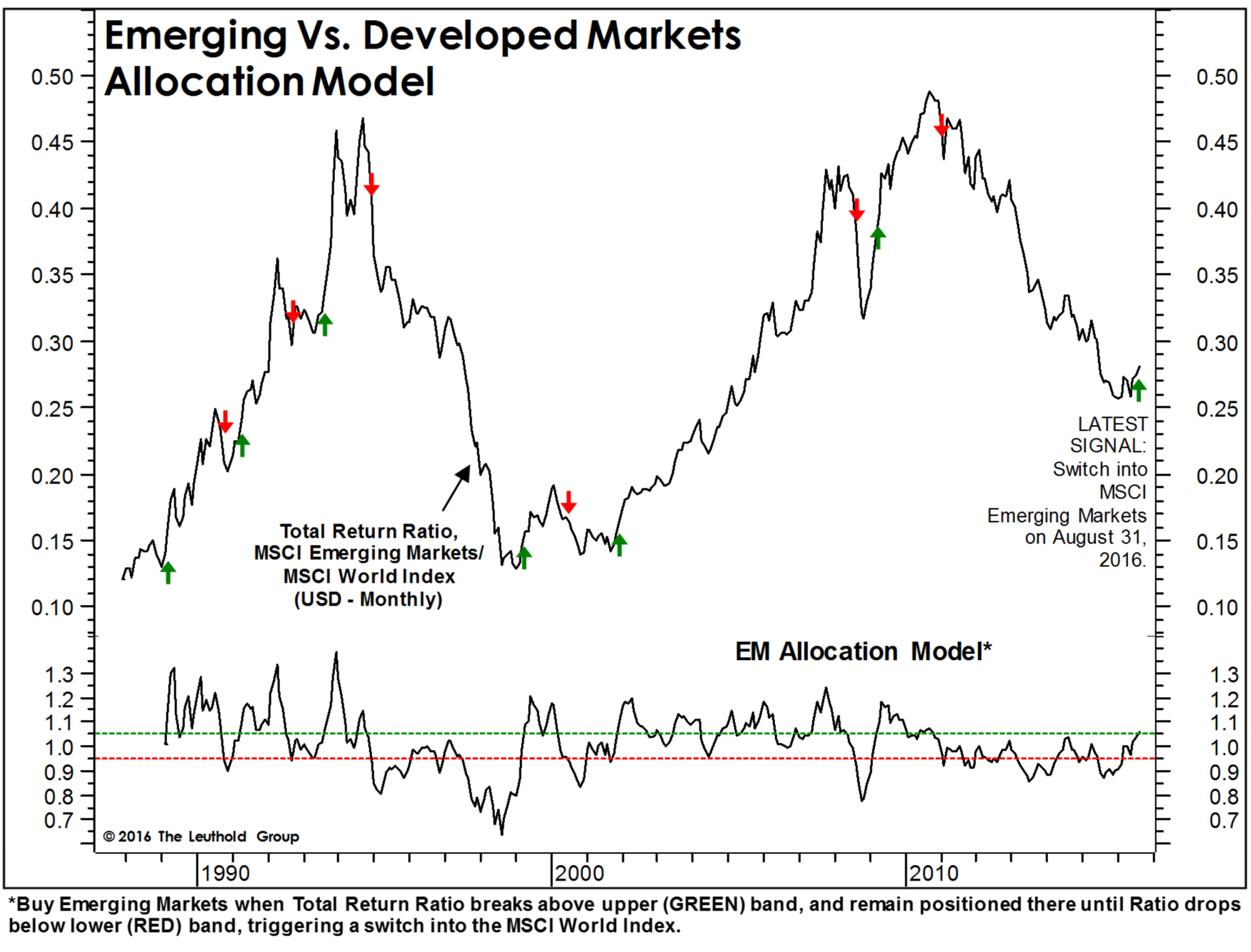

Our Emerging Markets Allocation Model triggered a BUY signal at the end of August after 5 1/2 years in bear mode (Chart 1), and we’ve responded by boosting the EM position in the Leuthold Core Portfolio to 5.5% of assets, up from 3%.

No, the model did not bottom-tick the January lows in EM stocks… but bottom-fishing is not inherent in the model’s design. And we’d emphasize that the model sidestepped perhaps half a dozen putative relative strength lows in EM stocks over the past few years.

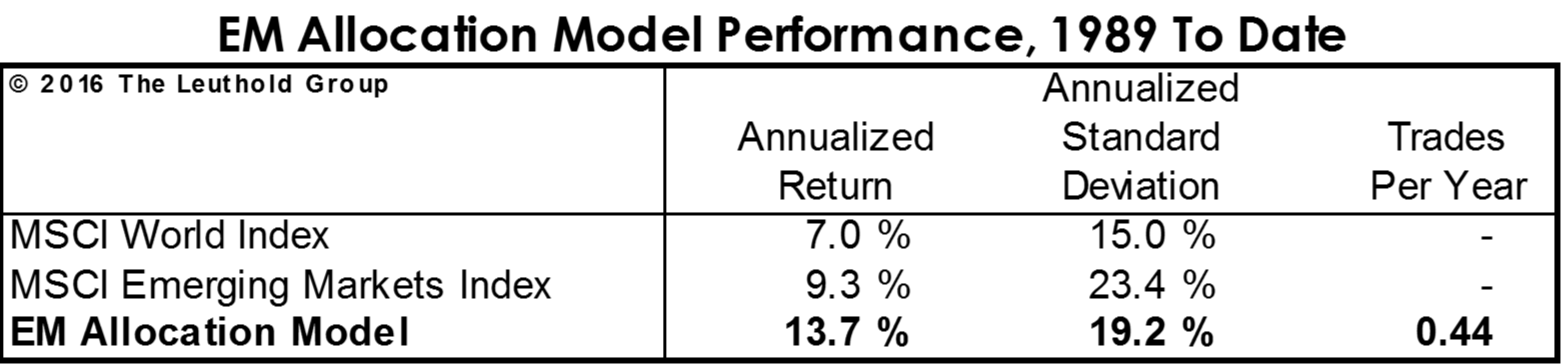

The model’s upgrade is consistent with a cyclical leadership run of perhaps one to four years in EM equities relative to their Developed country counterparts. Historically, the Allocation Model has outperformed the Emerging Markets Index by 440 bps and the MSCI World Index by 670 bps on an annualized, total return basis. Volatility of the strategy (19.2% annualized) has been exactly halfway between that of the World Index and the EM Index (Table 1). The model dictates a shift once every 27 months, on average, with the big winners usually lasting considerably longer.

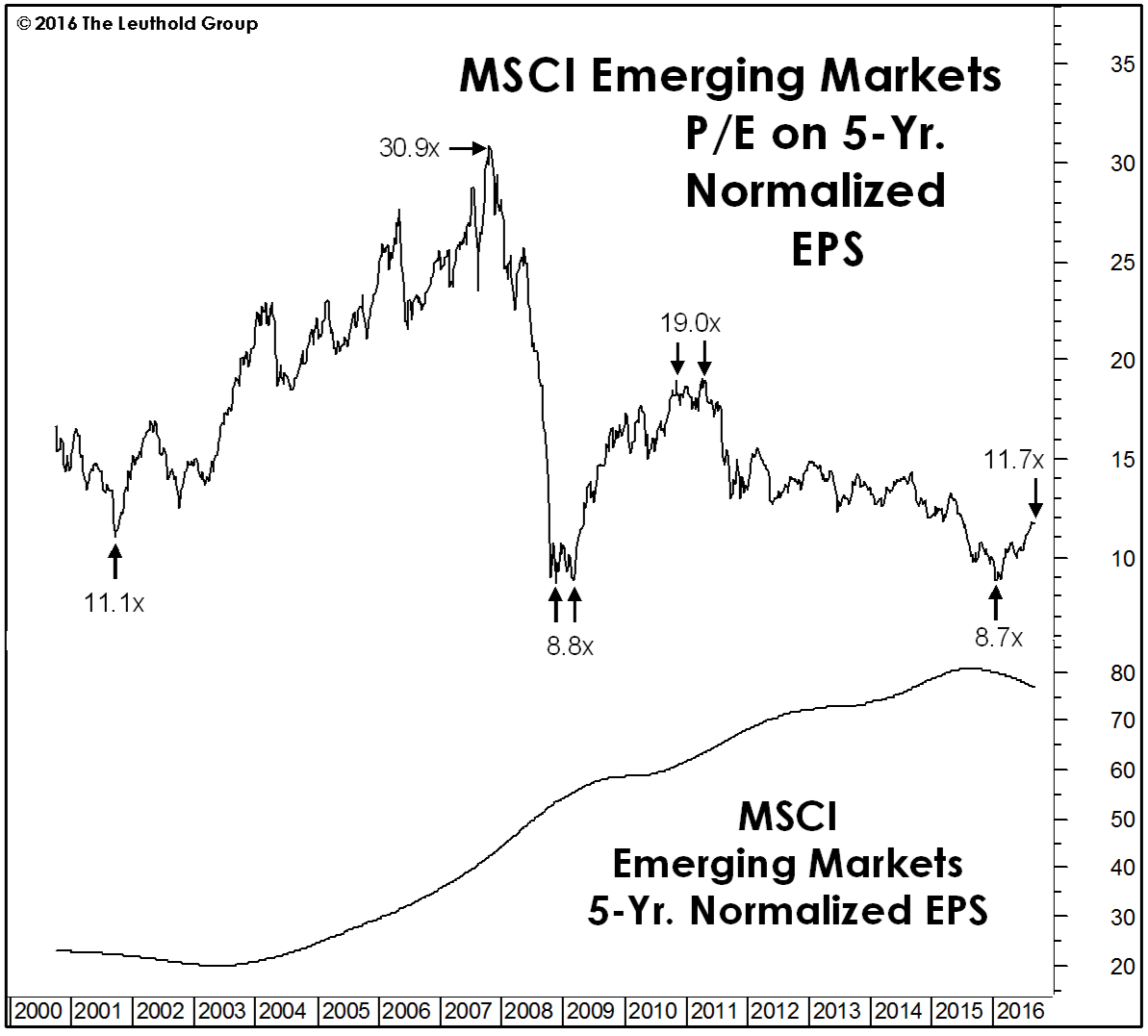

Our secular opinion on EM equities is agnostic. We’ve never held the view that superior GDP growth in the Emerging Market economies would necessarily translate into superior outcomes for shareholders. Dilution via share issuance and an EM obsession with market share over profitability are key economic risks, and political risks are too numerous to mention. But the EM Model has triggered, and it has done so with the MSCI Emerging Markets Index trading at a relatively cheap 11.7x 5-Yr. Normalized EPS (Chart 2).

With the benefit of hindsight, the best time to buy EM was at the January lows when the Normalized P/E briefly undercut its 2008-09 “double bottom” of 8.8x. But the current figure of 11.7x is nonetheless down a third from the 17.6x prevailing at the Allocation Model’s last SELL signal (February 2011), and is on par with the valuation low that immediately followed the 9/11 attacks. And today’s reading occurs with EM 5-Yr. Normalized EPS in a downtrend. In other words, EM earnings results have been so weak for so long that even our Normalized figure looks compromised.