I am somewhat exhausted; I wonder how a battery feels when it pours electricity into a non-conductor?

― Arthur Conan Doyle; The Adventure of the Dying Detective

In Brief:

- Though long-in-the tooth, the current business expansion is not about to roll over. Decision Economics, Inc. (DE) expects sluggish global growth to pick up some steam and extend into 2017 and beyond.

- Failure by unorthodox monetary policies to stimulate faster growth, coupled with rising populist sentiment, are pressuring governments to use fiscal policies to pick up the slack. DE projects a modest increase in public spending to help lift growth across the G7 in 2017.

- In our view, U.S. equities continue as the asset class of choice, but subject to periodic pullbacks brought on by pressure on corporate profit margins and political uncertainty. Though reducing overall equity market exposure, DE maintains a strategically Strong Overweight position in equities for global portfolios, anticipating stronger global economic growth and a rebound in profits in 2017 (Chart 1).

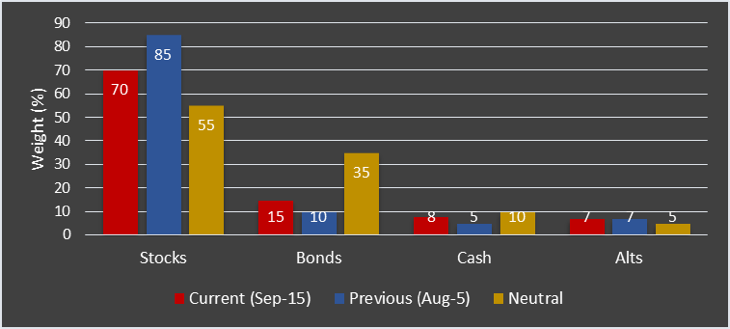

Chart 1: Broad Global Asset Allocation

Source: Decision Economics, Inc. (DE)

*Managing Director and Director of Investment Strategy, Decision Economics, Inc. (DE).

([email protected], Tel 207-781-5005)

- Recently, yields on high-grade sovereign bonds have backed up. But bond prices will remain firm in the wake of tepid global growth, well-anchored inflation expectations, and heightened geopolitical risks. The DE global allocation maintains an Underweight position in Fixed Income, but is raising marginally the exposure to the asset class in global portfolios as a windward anchor against choppy equity markets (Chart 1).

- Rising hedging costs and reduced carry trade flows are expected marginally to undermine dollar strength. Deferred action by the Federal Reserve in raising interest rates could cause some dollar slippage in 4Q2016. Despite recent stability, sterling weakness lies ahead as the U.K. economy struggles to avoid recession.

Global Growth – On a Wing and a Prayer

More than seven years after the Great Recession, the global economic landscape still is not reassuring. Growth has continued to lag and downward revisions to forecasts have become standard. Absent any obvious engines to rev up demand, we project a grinding world economy that gains traction incrementally. Headwinds include ongoing deleveraging in the aftermath of the financial crisis, sluggish world trade, and constrained credit growth by commercial banks facing higher capital requirements and heavy loads of nonperforming loans, especially in Europe and China.

In the U.S., robust consumer spending, supported by gains in employment and income, has been the primary driver of growth. But business capital spending has gone MIA. The restructuring of corporate balance sheets has been more cosmetic than substantive. Taking advantage of cheap credit, businesses, both top-rated and lower-quality, have bought back shares, boosted dividend payouts, and aggressively pursued mergers and acquisitions.

Meanwhile, the leverage of business balance sheets, measured as the ratio of debt to net worth, now stands significantly above pre-crisis levels. Extended balance sheets could lead to higher debt defaults, undermining capital spending when interest rates begging to rise. At the same time, federal government spending has been constrained by budget sequestration and polarized politics, while state and local governments struggle under the weight of underfunded pension obligations.

In the E.U., weak growth in the wake of fiscal austerity has been endemic. Having wiped out a generation of consumers in the aftermath of the financial crisis, and still facing high unemployment, soft bank lending and weak trade flows, Europe is well on the way to a Japan-style “Lost Decade.”

In Japan, Prime Minister Abe’s three-arrow policy – expansionary monetary and fiscal policies, coupled with delayed structural reforms – has yet to put the economy on a sustainable growth path, or resuscitate inflation expectations. Similarly in China, economic growth has slowed as the government tries to re-orient the economy toward domestic consumption. Massive production overcapacity in many sectors as a result of weakened demand for exports and falling profit margins are stifling business spending, undermining economic growth. A worrisome build up of debt across all sectors presents yet another hurdle to China’s economic growth.

Central Bank Policies – Boxing with a Cloud

Unorthodox policies and massive transfusions of liquidity by the major central banks have failed to produce strong growth for the world economy. Their willingness to reach deep into their tool kits for different ways to “get a bang for the buck” brings to mind the story of the young tenor in his first appearance at La Scala. After several encores and totally exhausted, he pleads with the audience, “Thank, thank you. I am grateful for your enthusiasm and great support, but I cannot go on any longer.” To which a voice from the back of the house shouts, “You have to keep on trying until you get it right.”

In the U.S., validating market expectations, the Federal Reserve decided at its September 21st meeting to leave the federal funds rate unchanged. The excuse was that despite robust gains in consumer spending and the fall in the unemployment rate below 5 percent more evidence was required, showing broader gains in employment. But with several indicators flashing yellow, including weaker retail sales, industrial production and manufacturing new orders, a dovish stance was defensible. Also, with inflation still lagging behind the official 2 percent target, the Fed felt no urge to take action. Other factors that might have played a role would include concern about a strengthening of the dollar, and pressure on heavy dollar borrowers, especially in emerging markets.

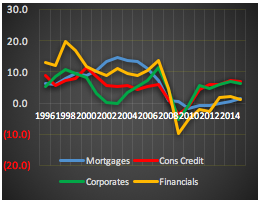

Chart 2: Growth in Debt (%)

Source: Federal Reserve Board, Flow of Funds

Plentiful Liquidity, but Limited Credit

Parenthetically, obsessing over a one-quarter percentage point increase in the Fed funds rate from such a low level is missing the point. Except during extreme circumstances, e.g. in the early 1980s, it has been the availability, not the price, of credit that has had the greatest impact on economic activity. Restrained credit growth, especially bank lending, has been a primary cause of the global malaise since the Great Recession. In the U.S., the collapse in mortgage lending since 2008 is striking (Chart 2).

After growing at an average rate of 11.6% in the 2000 – 07 period, mortgage lending has averaged zero growth in the last eight years. The big rebound in nonfinancial corporate debt since 2008 has been of no help in promoting capital spending. Instead, businesses have chosen to refinance more expensive debt, buy back shares, or boost mergers and acquisitions activity. The anemic growth in financial sector debt, a major fuel in encouraging spending, has been the result of new regulations aimed at improving the stability of the financial system. Japan and the E.U. are experiencing similar weak growth in debt, though there are signs that bank lending in the E.U. is starting to crawl up.

Overall, it is possible that the shock of the financial crisis has changed the price elasticity of credit by borrowers and lenders alike. This attitude toward the use of credit is consistent with symptoms following the bursting of previous credit bubbles and the ensuing deleveraging, but it seems to be more pronounced this time around.

Bank of Japan (BOJ) – Triumph of Hope over Experience

Meanwhile in Japan, the much-anticipated comprehensive review by the Bank of Japan (BOJ) of monetary policy was received by the financial markets with a big yawn. Instead of bold new initiatives, the central bank chose to add yet another acronym, QQE+YCC (Qualitative and Quantitative Easing with Yield Curve Control) to the existing platform of ZIRP, NIPR, and QQE that describes its unorthodox policy mix. Although marketed as a new approach to stimulate growth by keeping long yields down, while reviving dormant inflation expectations, YCC represents essentially old-fashioned debt monetization potentially of gargantuan proportions. To nail the yield on the 10-year JGB at zero, its primary objective, the BOJ would have to buy all the bonds offered at that rate.

Under the new policy, the BOJ, which already holds over one-third of outstanding government debt, could become the largest source of funds to the government. In that case, this form of government self-financing becomes a synonym for “helicopter money.” It is possible that this new policy tack could work in theory. But as history convincingly shows, central banks can control the quantity of money, or its price, but not both at the same time.

Bond Markets – Up the Down Staircase

In the aftermath of Brexit, the spasm that forced government bond yields to record levels has eased and yields have experienced a modest rebound. The bounce back was further encouraged by major central banks holding the line against any further easing at this time. Though the rally in global bonds has run its course, government yields are likely to stay within a tight band around present levels, reflecting sub-par growth, ongoing easy central bank policies, and well-anchored inflation expectations. In the U.S., the 10-year Treasury yield is expected to remain in the 1.5% - 2% range through early 2017. Subsequently, a slight upward drift in global yields is expected later next year on the back of more activist fiscal policies and further firming in global economic activity.

Against the backdrop of relatively stable bond yields, DE has raised the overall exposure to Fixed Income in the global bond portfolio marginally as a wayward anchor against choppy equity markets. There is continued focus on U.S. Treasuries (also because of their safe haven status against geopolitical risks), investment-grade corporates, as well as dollar and non-dollar emerging market sovereign bonds.

Equity Markets – Losing Froth

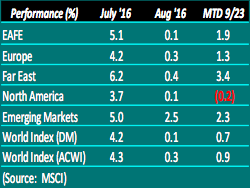

Table 1: World Equity Markets (USD)

After rebounding smartly from the Brexit spasm in July, world equity markets have tailed off since, weighted down by tepid economic prospects, banking stresses in Europe, the lack of further aggressive easing by the major central banks, and political and geopolitical risks (Table 1). In the U.S., the lack of props also includes flagging activity in mergers and acquisitions, share buybacks, and political uncertainty.

With the two most unpopular presidential candidates in the country’s history stealing the spotlight, not enough attention has been given to the all-important Congressional races. Whoever gets elected president, he or she will have to work with Congress to implement policies. And further down the road, there is the appointment to the vacant seat at the Supreme Court. No one is capable of winning this trifecta.

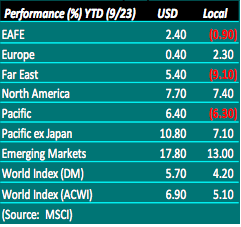

Table 2: World Equity Markets

Lofty valuations are yet another concern baffling equity markets. There are strong opinions on both sides of the aisle, but deciding on the proper measure of risk in today’s dystopian financial environment is largely a judgment call. Recognizing, however, that this market is equally hated by bulls and bears suggests that valuation is an imperfect yardstick. Among other things, the profile of the indexes is different over different market cycles, and rarely, if ever, are alike. As our friend Craig Drill of Craig Drill Capital has often said, “Valuation tends not to be an important variable during a bull market…only when it ends.” In DE’s view, with interest rates staying low, the expected rebound in earnings into 2017 suggests this bull market has resilience.

Despite losing some froth, global stock markets have generated respectable returns so far this year (Table 2). This underscore’s DE’s main theme that equities continue as the asset class of choice. Emerging markets have been the best performers YTD (as of 9/23) both in local currency and USD terms on the back of low U.S. yields and overall stable oil and commodity prices. In comparison, the Far East region fell in local currency terms, brought down by Japan’s steep swoon. But thanks to the yen’s strengthening, the region recovered all of the losses and then some. Europe lagged seriously beaten down by hefty losses in Italy and Spain, mostly bank related.

Asset Allocations – Is TINA (There Is No Alternative) the Answer?

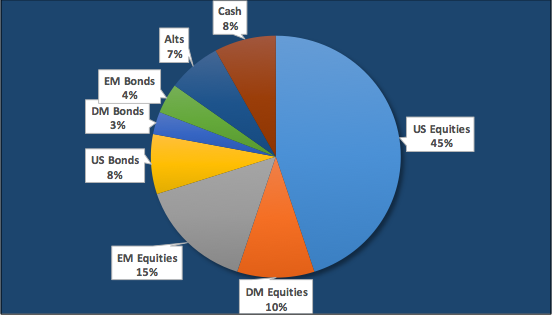

DE’s Baseline asset allocation (60% probability) this month extends our main investment theme: despite getting long-in-the tooth and periodic pullbacks, the bull market in stocks, unless tripped by political events or policy mistakes, has further to run. Underlying this theme, DE projects a durable, albeit slow-paced global economic expansion in 2017, supported by a moderate firming in final demands, mostly consumption-driven, continuing highly accommodative central bank policies, a touch of fiscal stimulus, relatively stable oil and commodity prices, and range-bound currencies against the dollar. Chart 3 shows DE’s global allocations across major asset classes in a Baseline global portfolio as of mid-September.

This cautiously positive posture on stocks, however, does not imply full-steam-ahead for risk assets. This is a challenging investment landscape, overshadowed by slow growth with downside risks and high valuations. Global portfolio diversification across all major asset classes represents the prudent way for investors to preserve capital.

Chart 3: Global Asset Allocation

Source: Decision Economics, Inc. (DE)

© Decision Economics, Inc.